|

市场调查报告书

商品编码

1432671

工厂自动化/工业控制:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Factory Automation and Industrial Controls - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

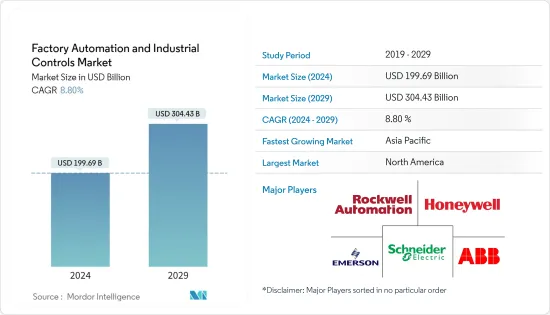

工厂自动化和工业控制市场规模预计到2024年为1996.9亿美元,预计到2029年将达到3044.3亿美元,在预测期内(2024-2029年)复合年增长率为8.80%,预计将增长。

自动化和控制系统减少製造错误,节省时间和成本,并提高客户满意度。建造用于规划、产品开发和供应链物流的智慧工厂是越来越多地采用智慧系统、组件、机械和设备透过自动化和自我最佳化来改进流程的结果。这是影响市场的一个重要方面。

主要亮点

- 自动化产业正在透过製造的数位和实体方面的结合进行彻底变革,旨在提供最佳效能。此外,对实现零废弃物生产和缩短时间的关注正在加速市场成长。

- 工业物联网 (IIoT) 和工业 4.0 是整个物流链开发、生产和管理的新技术方法的核心,称为智慧工厂自动化,其中机器和设备透过互联网和 IT 连接起来。主导工业领域的趋势。

- 此外,由于工业4.0 和物联网(IoT) 的普及,製造业发生了巨大转变,正在推动企业变得敏捷,并透过自动化补充和增强人力的技术来推进生产,并减少因流程故障而导致的工业事故。我们需要采取明智的创新方法。

- 此外,世界各地的汽车製造商都认识到,下一代机器人和自动化技术具有革命性的潜力,可以在生产力、品质、安全性和成本参数方面改变汽车产业。机器人自动化系统需求也预计将受益于机器人自动化支出逐年增加。

- 各领域的人事费用都在快速上涨。此外,品质标准也变得越来越严格。考虑到这一点,工厂自动化可以降低生产、营运和人事费用。

- COVID-19 的爆发迫使世界各地的企业和製造设施关闭,扰乱了市场。製造业对工业自动化系统的需求下降导致了重大损失,特别是在今年前两个季度。幸运的是,随着工厂重新开业和工业运营恢復,2021 年前几个月出现了积极的復苏迹象。工业 4.0 技术的进步正在增加各个工业领域对机器人等自动化解决方案的需求。

工厂自动化和工业控制市场趋势

汽车产业预计将录得显着成长

- 汽车工业是重要产业之一,在全球自动化製造设备中占有很大份额。已经证实,各汽车製造商的生产设施都实现了自动化,以保持准确性和效率。此外,以电动车取代传统汽车的趋势预计将增加汽车产业的需求。

- 在许多工业领域,工业4.0技术的发展增加了对机器人等自动化解决方案的需求。由于技术,工厂可以全年 365 天、每天 24 小时运转,无需人工监管。例如,组装机器人比专用设备更容易使用,并且比人类移动得更快、更准确。机械臂可以执行诸如在汽车製造设施中驱动螺丝、安装挡风玻璃和安装轮圈等任务。机械臂因提高生产力和效率、同时降低人类工人的成本和风险而享有盛誉。

- 此外,人工智慧正在整个汽车价值链中使用,从设计和生产等製造业务到保险和预测性维护等支援活动。然而,当今人工智慧最令人兴奋的应用之一是交通运输,它正在帮助创建无人驾驶车辆和驾驶员辅助系统。

- 此外,现代汽车等品牌正在大力投资智慧移动解决方案,以保持领先于竞争对手的优势。随着汽车变得更加智慧和连网型,拥有一家专门从事机器人和人工智慧的公司从长远来看将是一笔巨大的资产。 2021年6月,现代汽车宣布从Softbank Corporation收购波士顿动力公司的管理权。该交易对这家美国机器人开发商的估值为11亿美元,其中现代汽车持有80%的股份,Softbank Corporation仍持有20%。

- 由于采用智慧工厂,汽车产业有机会增加产量、减少製造停机时间、提高供应链效率并更快地回应市场需求。计划工期是汽车产业面临的最重要挑战之一。快速的计划投资回报,加上经济实惠的自动化和成本创新,有助于製造商透过提高生产力来提高竞争力。

北美占据主要市场占有率

- 主要汽车製造商都位于北美,并受益于强大的基础设施和政府对电动车的支持。此外,年轻人对豪华和高檔汽车的日益偏好预计将提供有利可图的机会。

- 由于越来越注重减少汽车排放气体,汽车产业的重点正在转向电动车。各国政府和环境机构正在製定更严格的排放法规和法律,以解决日益严重的环境问题,这可能会增加电力传动系统和节能柴油引擎的生产成本。因此,过去五年来,北美对电池式电动车的需求达到了历史最高水准。

- 此外,由于数位化、自动化程度的提高和新的经营模式,汽车产业也将经历类似的变化。由于以下因素,汽车产业正在出现四种颠覆性技术主导的趋势:行动多样化、自主性、电动和连结性。然而,随着租赁汽车和二手车市场的日益普及,参与企业市场可能会面临困难。物流和配送服务的成长,以及亚马逊等主要电子商务公司持有的扩张,将对商用车的需求产生重大影响。

- 采用工厂自动化解决方案可以帮助这些製造商降低成本、提高生产力并提高品质。近日,加拿大皇家银行(RBC)与微软合作推出Go Digital计划,协助加拿大企业投资智慧自动化技术和云端解决方案。该计划针对加拿大食品製造商,并计划在未来扩展到其他行业。

- 此外,在北美,2022年第一季来自汽车製造商和零件製造商的机器人订单占总量的47%。多家汽车製造商已宣布增加工厂的资本支出,以支持未来的电动车车型或提高电池产能。有了这些重要倡议,未来几年对工业机器人的需求可能会增加。

工厂自动化与工业控制产业概况

全球工厂自动化和工业控制市场竞争激烈,由多家大公司组成。市场似乎适度分散。在这个市场上拥有压倒性份额的主要公司正在专注于扩大海外基本客群。这些公司利用策略合作计划来增加市场占有率和盈利。此外,我们也致力于透过收购从事工厂自动化和工业控制的新兴企业来增强我们的产品能力。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 日益关注能源效率和降低成本

- 自动化趋势日益增长

- 市场挑战

- 贸易摩擦与实施挑战

第六章市场区隔

- 副产品

- 透过工业控制系统

- 集散控制系统(DCS)

- 可程式逻辑控制器(PLC)

- 监控/资料采集 (SCADA)

- 产品生命週期管理 (PLM)

- 人机介面 (HMI)

- 製造执行系统(MES)

- 企业资源规划(ERP)

- 其他工业控制系统

- 现场设备

- 机器视觉系统

- 机器人(工业)

- 感测器和发射器

- 马达与驱动器

- 其他现场设备

- 透过工业控制系统

- 按最终用户产业

- 车

- 化工/石化

- 公用事业

- 製药

- 食品和饮料

- 油和气

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Company

- ABB Limited

- Mitsubishi Electric Corporation

- Siemens AG

- Omron Corporation

- Yokogawa Electric Corporation

- General Electric Co.

- Texas Instruments Inc.

- Robert Bosch GmbH

第八章投资分析

第9章 未来展望

The Factory Automation and Industrial Controls Market size is estimated at USD 199.69 billion in 2024, and is expected to reach USD 304.43 billion by 2029, growing at a CAGR of 8.80% during the forecast period (2024-2029).

Automation and control systems decrease manufacturing errors, which saves time and money and increases customer satisfaction. The creation of smart factories for planning, product development, and supply chain logistics is a result of the increased adoption of smart systems, components, machinery, and equipment for the improvement of processes through automation and self-optimization. This is a key aspect influencing the market.

Key Highlights

- The automation industry has been revolutionized by the combination of digital and physical aspects of manufacturing aimed at delivering optimum performance. Further, the focus on achieving zero waste production and a shorter time to reach the market has augmented the growth of the market.

- The Industrial Internet of Things (IIoT) and the Industrial 4.0 are at the center of the new technological approaches for the development, production, and management of the entire logistics chain, otherwise known as smart factory automation, and are dominating the trends in the industrial sector, with machinery and devices being connected via internet.

- Moreover, massive shifts in manufacturing due to Industry 4.0 and the acceptance of IoT require enterprises to adopt agile, smarter, and innovative ways to advance production with technologies that complement and augment human labor with automation and reduce industrial accidents caused by process failure.

- Additionally, automakers worldwide are aware of the revolutionary potential of the next generation of robots and automation technologies to transform the automotive industry in terms of productivity, quality, safety, and cost parameters. The need for robot automation systems is also anticipated to benefit from rising robotic automation spending year over year.

- The cost of labor has risen exponentially in many different areas. Additionally, the standards for quality are becoming stricter. In light of this, factory automation may result in lower production, operating, and labor expenses.

- The market was disrupted when the COVID-19 epidemic forced the closure of enterprises and manufacturing facilities worldwide. Significant losses were incurred, particularly in the first two quarters of the year, as a result of the drop in demand for industrial automation systems in the manufacturing sectors. Fortunately, there have been encouraging signs of a resurgence in the first few months of 2021, owing to the reopening of the plants and the restart of industrial operations. Industry 4.0 technology advancements have increased demand for automated solutions like robots across a wide range of industrial industries.

Factory Automation and Industrial Controls Market Trends

Automotive is Expected to Register a Significant Growth

- The automotive industry is one of the prominent sectors that hold a significant share in worldwide automated manufacturing facilities. It is observed that the production facilities of various automakers are automated to maintain accuracy and efficiency. Further, the growing trend of replacing conventional vehicles with EVs is expected to augment the automotive industry's demand.

- In many industrial areas, the demand for automated solutions like robots has increased due to developments in Industry 4.0 technology. Because of technology, factories can operate without human supervision for 24 hours daily, 365 days per year. For instance, assembly robots are simpler to use than specialized equipment and can move more quickly and precisely than people. Robotic arms can do activities like screw driving, windshield installation, and wheel mounting in auto manufacturing facilities. They have a reputation for boosting productivity and efficiency while lowering expenses and dangers for human workers.

- Additionally, AI is used in the automotive value chain, from manufacturing duties like design and production to supporting activities like insurance and predictive maintenance. However, one of AI's fascinating uses today is transportation, where it powers the creation of driverless vehicles and driver assistance systems.

- Further, brands such as Hyundai have invested heavily in smart mobility solutions to stay ahead of their competitors. With cars becoming smarter and more connected, having a company specializing in robotics and AI can be a great asset in the long run. In June 2021, Hyundai Motor Company recently confirmed that they had bought a controlling interest in Boston Dynamics from SoftBank. According to the deal, the American robotics developer has been valued at USD 1.1 billion, and Hyundai has 80% shares while SoftBank still owns 20%.

- The automotive industry has chances to increase production, decrease manufacturing downtime, improve supply chain efficiency, and respond more quickly to market demands thanks to smart factories. The length of a project is one of the top issues facing the automotive sector. Rapidly paying off projects, together with affordable automation and cost innovation, aid manufacturers in becoming more competitive by enhancing productivity.

North America to Hold a Significant Market Share

- Major automotive OEMs are based in the nation, benefiting from a substantial infrastructure and the government's support for electric vehicles. In addition, the increasing inclination of young people for luxury and premium vehicles is predicted to present lucrative opportunities.

- The automotive industry's attention has switched to electric vehicles due to the growing emphasis on decreasing vehicle emissions. Governments and environmental agencies are rolling out stringent emission rules and laws to address growing environmental concerns, which could increase the cost of producing electric drive trains and fuel-efficient diesel engines. As a result, over the past five years, battery electric car demand in North America has reached an all-time high.

- Additionally, the automotive industry will similarly undergo a change fueled by digitization, rising automation, and new business models. Four disruptive technology-driven trends are emerging in the automobile industry as a result of these factors: diversified mobility, autonomous driving, electrification, and connection. However, market participants may face difficulties due to the growing popularity of rental and used car markets. Growing logistics and delivery services, along with the expansion of vehicle fleets by major e-commerce players like Amazon, etc., significantly impact the demand for commercial cars.

- The adoption of factory automation solutions can help these manufacturers in cost savings, enhance productivity, and improve quality. Recently, the Royal Bank of Canada (RBC) collaborated with Microsoft and launched the Go Digital program to help Canadian businesses invest in smart automation technologies and cloud solutions. The program is available to Canadian food manufacturers and will continue expanding to other industries.

- In addition, in North America, orders for robots from automakers and component manufacturers accounted for 47% of all orders in the first quarter of 2022. Several automakers have announced investments better to outfit their plants for future electric drive car models or to boost battery production capacity. These significant initiatives will increase the demand for industrial robots in the coming years.

Factory Automation and Industrial Controls Industry Overview

The Global Factory Automation and Industrial Controls Market is highly competitive and consists of several major players. The market appears to be moderately fragmented. The major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. These companies are leveraging on strategic collaborative initiatives to increase their market shares and profitability. The companies operating in the market are also acquiring start-ups working on factory automation and industrial control systems to strengthen their product capabilities.

- July 2022 - Rockwell Automation, Inc., the world's largest company dedicated to industrial automation and digital transformation, announced the launch of the PowerFlex AC variable frequency drive portfolio in the Asia Pacific to support an array of motor control applications. This will provide customers more flexibility, performance, and intelligence in their next generation drive through TotalFORCE Technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Energy Efficiency and Cost Reduction

- 5.1.2 Growing Trend Towards Automation

- 5.2 Market Challenges

- 5.2.1 Trade Tensions and Implementation Challenges

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 By Industrial Control Systems

- 6.1.1.1 Distributed Control System (DCS)

- 6.1.1.2 Programmable Logic Controller (PLC)

- 6.1.1.3 Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.4 Product Lifecycle Management (PLM)

- 6.1.1.5 Human Machine Interface (HMI)

- 6.1.1.6 Manufacturing Execution System (MES)

- 6.1.1.7 Enterprise Resource Planning (ERP)

- 6.1.1.8 Other Industrial Control Systems

- 6.1.2 Field Devices

- 6.1.2.1 Machine Vision Systems

- 6.1.2.2 Robotics (Industrial)

- 6.1.2.3 Sensors and Transmitters

- 6.1.2.4 Motors and Drives

- 6.1.2.5 Other Field Devices

- 6.1.1 By Industrial Control Systems

- 6.2 By End-User Industry

- 6.2.1 Automotive

- 6.2.2 Chemical and Petrochemical

- 6.2.3 Utility

- 6.2.4 Pharmaceutical

- 6.2.5 Food and Beverage

- 6.2.6 Oil and Gas

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Rockwell Automation Inc.

- 7.1.3 Honeywell International Inc.

- 7.1.4 Emerson Electric Company

- 7.1.5 ABB Limited

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Siemens AG

- 7.1.8 Omron Corporation

- 7.1.9 Yokogawa Electric Corporation

- 7.1.10 General Electric Co.

- 7.1.11 Texas Instruments Inc.

- 7.1.12 Robert Bosch GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK

2025年工厂自动化全球市场报告

2025年工厂自动化全球市场报告 工厂自动化感测器市场(按组件、按技术、按最终用途、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

工厂自动化感测器市场(按组件、按技术、按最终用途、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 半导体工厂自动化:技术问题与市场预测2025年工厂自动化感测器全球市场报告

半导体工厂自动化:技术问题与市场预测2025年工厂自动化感测器全球市场报告 机器人製造和现场组装解决方案市场—全球产业规模、份额、趋势、机会和预测(按组件、按技术、按应用、按地区、按竞争、预测和机会,2020-2030 年)

机器人製造和现场组装解决方案市场—全球产业规模、份额、趋势、机会和预测(按组件、按技术、按应用、按地区、按竞争、预测和机会,2020-2030 年) 全球电脑整合製造市场全球工厂自动化感测器市场工厂自动化市场规模、份额、趋势分析报告:按组件、技术、最终用途、地区、细分市场预测,2025-2030 年

全球电脑整合製造市场全球工厂自动化感测器市场工厂自动化市场规模、份额、趋势分析报告:按组件、技术、最终用途、地区、细分市场预测,2025-2030 年 2030 年工厂自动化平台即服务市场预测:按组件、部署、技术、应用、最终用户和地区进行的全球分析

2030 年工厂自动化平台即服务市场预测:按组件、部署、技术、应用、最终用户和地区进行的全球分析 工厂自动化市场规模:份额、成长分析、按设备、按解决方案、按行业垂直、按地区 - 行业预测 2025-2032

工厂自动化市场规模:份额、成长分析、按设备、按解决方案、按行业垂直、按地区 - 行业预测 2025-2032