|

市场调查报告书

商品编码

1641838

远端资讯处理:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

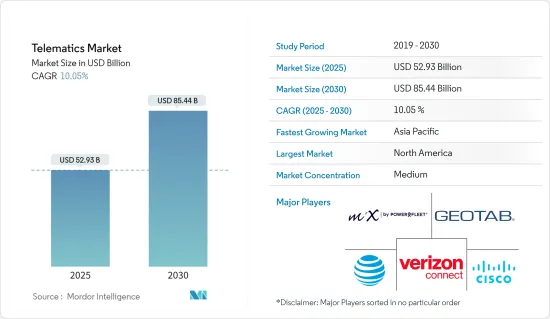

预计 2025 年远端资讯处理市场规模为 529.3 亿美元,到 2030 年将达到 854.4 亿美元,预测期内(2025-2030 年)的复合年增长率为 10.05%。

远端资讯处理市场是汽车产业内一个快速发展的领域,由技术进步和对即时资料解决方案日益增长的需求推动。远端资讯处理技术能够将车辆的资料传输到外部系统,使公司能够监控和管理车辆,追踪车辆性能并确保安全。随着物联网 (IoT) 功能的整合,远端资讯处理系统变得越来越复杂,可以透过资料分析更深入地了解车辆的运作。这些解决方案涵盖各种应用,包括车队管理、GPS 追踪和汽车保险。

远端资讯处理主要企业与创新:

主要亮点

- 持续创新:MiX Telematics、Geotab Inc.、Verizon Telematics 等主要企业不断创新,以提供更精准、更全面的资讯服务。

- 消费应用:远端资讯处理技术在个人消费者中也越来越受欢迎,目标商标产品製造商 (OEM) 和售后市场供应商都提供嵌入式和携带式设备。消费者兴趣的增加是由于对增强安全功能、车辆诊断和提高燃油经济性的需求不断增长。

- 云端基础的解决方案:此外,对云端基础的远端资讯处理解决方案的需求日益增加,允许远端资讯处理资料与企业系统无缝整合。这不仅简化了车队管理,而且还降低了营运成本。

远端资讯处理市场细分:

主要亮点

- OEM)和售后市场参与者:远端资讯处理市场按OEM)和售后市场参与者提供的解决方案进行细分,包括基于智慧型手机、可携式和嵌入式设备。这些设备专为满足不同的消费者需求而量身定制,包括入门级、中层级和高端解决方案。

- 按地区分類的市场:北美、欧洲和亚太地区主导着车用通讯系统市场。消费者对远端资讯处理技术优势的认识不断提高,加上有关车辆安全和效率的严格规定,推动了该技术的采用。

连网型设备的激增扩大了市场潜力

主要亮点

- 连网型设备的兴起正在极大地影响远端资讯处理市场。随着越来越多的车辆配备了支援物联网的远端资讯处理系统,车辆与基础设施之间的资料传输变得更加顺畅和高效。

- 商业远端资讯处理这对于依靠即时资料来管理大型车队的商业远端资讯处理解决方案尤其重要。公司可以监控绩效指标并提高业务效率,从而受益于优化的路线、燃料使用和维护。

- 消费者对连网汽车的需求:连网汽车远端资讯处理正在经历显着成长,消费者选择提供 GPS 追踪、即时交通更新和紧急应变能力等先进功能的汽车。基于智慧型手机的远端资讯处理应用程式为消费者提供了轻鬆存取车辆资料的途径,进一步推动了这一成长。

- 云端基础的平台:云端基础的远端资讯处理平台的采用透过实现远端资料存取彻底改变了车队管理。这些平台具有扩充性和适应性,可满足从交通运输到个人车辆所有权等多个行业的需求。

汽车诊断需求推动创新

主要亮点

- 对无缝车辆诊断的需求不断增长,推动了远端资讯处理系统的进步,尤其是在车队管理方面。

- 车队健康监测:管理大型车队的公司需要即时车辆健康资料,以避免代价高昂的故障并减少停机时间。远端资讯处理资料分析使车队管理人员能够追踪引擎健康状况、燃油消费量和轮胎压力等关键性能指标,从而实现预防性保养。

- 预防性诊断:对于消费者而言,车辆内建的远端资讯处理系统将实现主动诊断,并自动发出定期维护警报。这大大降低了车辆意外故障的风险并提高了安全性。这些简单的诊断工具正在成为连网汽车应用的重要组成部分,进一步推动需求。

- 远端资讯处理创新:随着对更智慧、资料主导的诊断的需求不断增加,远端资讯处理软体和硬体创新正在推动成长,使商用车主和个人车主都受益。

远端资讯处理市场趋势

智慧型手机解决方案可望占据主要市场占有率

随着连网汽车解决方案的发展以及汽车、运输和物流等行业的日益应用,全球远端资讯处理市场正在经历快速成长。影响市场的关键趋势包括基于智慧型手机的远端资讯处理日益增长的重要性以及亚太地区的显着扩张。

- 基于智慧型手机的解决方案:这些解决方案由于其效率和可近性而成为主流。车队管理远端资讯处理越来越依赖智慧型手机应用程式来提供 GPS 追踪、驾驶员行为监控和车辆诊断等功能,而无需专用硬体。

- 燃油经济性和性能分析:智慧型手机应用程式中的远端资讯处理资料分析透过提供有关燃油消耗、驾驶行为和车辆性能的即时洞察来改变业务运营。

- 基于使用情况的保险 (UBI):智慧型手机远端资讯处理还支援 UBI,远端资讯处理资料可协助保险公司根据驾驶行为更准确地计算保费。这种节省成本的效果正在推动 UBI 在保险业广泛采用。

亚太地区可望强劲成长

亚太地区的远端资讯处理应用正在显着成长,这主要得益于对联网汽车和物联网远端资讯处理解决方案的需求不断增长。

- 中国汽车市场中国正经历连网汽车远端资讯处理的蓬勃发展,其係统提供即时追踪和诊断等先进功能。政府推行的促进远端资讯处理以减少排放气体和改善交通流量的政策促进了这一增长。

- 印度物流业随着越来越多的公司希望透过云端基础的系统来优化路线和提高燃油效率,印度的物流和运输领域越来越多地采用远端资讯处理技术。

- 日本远端资讯处理创新:日本持续引领远端资讯处理领域的创新,特别是在连网汽车生态系统的远端资讯处理与物联网的整合方面。日本汽车製造商处于开发下一代远端资讯处理解决方案的前沿。

车联网产业概况

远端资讯处理市场是一个半综合市场,由全球企业集团和专业参与者组成。

多样化的市场参与者:AT&T、Geotab Inc.、Cisco Systems Inc.、Verizon 和 MiX Telematics 等主要参与者提供一系列远端资讯处理解决方案。全球通讯公司正在利用网路基础设施,而专业公司则专注于车辆追踪和管理。

新兴策略:市场参与者的关键成功因素包括整合人工智慧预测分析、进军电动车用通讯系统处理领域以及提供更具扩充性的云端基础的解决方案。与汽车製造商合作并实现服务多样化对于未来的成长至关重要。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 连网型设备的兴起

- 对便利车辆诊断的需求庞大

- 市场限制

- 资料外洩的威胁

- 高成本

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场区隔

- 按频道

- 目的地设备製造商(OEM)

- 售后市场

- 按解决方案

- 智慧型手机

- 可携式的

- 嵌入式

- 依产品类型

- 硬体

- 服务(入门级、中层级、高阶)

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

第六章 竞争格局

- 公司简介

- Mix Telematics

- AT&T Inc.

- Geotab Inc.

- Verizon Telematics

- Cisco Systems Inc.

- Aplicom Oy

- Microlise Ltd

- LG Electronics Inc.

- Trimble Inc.

- Ctrack Global(Inseego Corp. Company)

第七章投资分析

第八章 市场机会与未来趋势

The Telematics Market size is estimated at USD 52.93 billion in 2025, and is expected to reach USD 85.44 billion by 2030, at a CAGR of 10.05% during the forecast period (2025-2030).

The telematics market is a rapidly evolving sector within the automotive industry, driven by advancements in technology and rising demand for real-time data solutions. Telematics technology enables the transmission of data from vehicles to external systems, allowing companies to monitor and manage their fleets, track vehicle performance, and ensure safety and security. With the integration of Internet of Things (IoT) capabilities, telematics systems are becoming increasingly sophisticated, providing deeper insights into vehicle operations through data analytics. These solutions span across various applications such as fleet management, GPS tracking, and automotive insurance.

Key Players and Innovations in Telematics:

Key Highlights

- Ongoing innovation: Key players like MiX Telematics, Geotab Inc., and Verizon Telematics are continuously innovating to offer more accurate and comprehensive data services, which are essential for businesses relying on vehicle operations.

- Consumer applications: Telematics technology is also gaining popularity among individual consumers, with original equipment manufacturers (OEMs) and aftermarket providers offering both embedded and portable devices. This surge in consumer interest is attributed to the increasing demand for enhanced safety features, vehicle diagnostics, and improved fuel efficiency.

- Cloud-based solutions: Additionally, cloud-based telematics solutions are growing in demand, allowing for seamless integration of telematics data with enterprise systems. This not only simplifies fleet management but also reduces operational costs.

Telematics Market Segmentation:

Key Highlights

- OEMs and aftermarket players: The telematics market is segmented by the solutions provided by OEMs and aftermarket players, which include smartphone-based, portable, and embedded devices. These devices are tailored to meet the needs of diverse consumers, with entry-level, mid-tier, and high-end solutions available.

- Geographical markets: North America, Europe, and Asia-Pacific dominate the automotive telematics market. The widespread adoption is driven by stringent regulations concerning vehicle safety and efficiency, alongside rising consumer awareness of telematics technology benefits.

Surge in Connected Devices Expands Market Potential

Key Highlights

- The rise of connected devices is significantly shaping the telematics market. With more vehicles now equipped with IoT-enabled telematics systems, data transmission between vehicles and infrastructure has become smoother and more efficient.

- Commercial telematics: This is particularly crucial for commercial telematics solutions, which rely on real-time data to manage large fleets. Companies benefit from optimized routing, fuel usage, and maintenance, thanks to the ability to monitor performance metrics and enhance operational efficiency.

- Consumer demand for connected vehicles: Connected car telematics is seeing substantial growth, with consumers increasingly opting for vehicles that offer advanced features like GPS tracking, real-time traffic updates, and emergency response capabilities. Smartphone-based telematics applications have further boosted this growth by providing consumers with easy access to vehicle data.

- Cloud-based platforms: The adoption of cloud-based telematics platforms has transformed vehicle management by allowing remote data access. These platforms provide scalability and adaptability, catering to the needs of diverse industries, from transportation to personal vehicle ownership.

Demand for Vehicle Diagnostics Fuels Technological Innovation

Key Highlights

- The growing demand for seamless vehicle diagnostics is pushing advancements in telematics systems, particularly within fleet management.

- Fleet health monitoring: Companies managing large fleets require real-time vehicle health data to avoid costly breakdowns and reduce downtime. By using telematics data analytics, fleet managers can track key performance indicators such as engine health, fuel consumption, and tire pressure, enabling preventive maintenance.

- Proactive diagnostics: For consumers, telematics systems embedded in vehicles allow for proactive diagnostics, with automatic alerts for routine maintenance. This significantly reduces the risk of unexpected vehicle failures and enhances safety. These easy diagnostics tools are becoming an integral part of connected car applications, further fueling demand.

- Telematics innovation: The market continues to see innovations in telematics software and hardware as the demand for smarter, data-driven diagnostics grows, benefiting both commercial and personal vehicle owners.

Telematics Market Trends

Smartphone Solution is Expected to Hold a Major Market Share

The global telematics market is experiencing rapid growth, driven by advancements in connected vehicle solutions and their increased adoption across industries such as automotive, transportation, and logistics. Key trends shaping the market include the rising importance of smartphone-based telematics and significant expansion in the Asia-Pacific region.

- Smartphone-based solutions: These solutions are becoming dominant due to their efficiency and accessibility. Fleet management telematics increasingly relies on smartphone apps, offering features such as GPS tracking, driver behavior monitoring, and vehicle diagnostics without needing specialized hardware.

- Fuel efficiency and performance analytics: Telematics data analytics within smartphone apps is transforming business operations by providing real-time insights into fuel consumption, driving behavior, and vehicle performance.

- Usage-based insurance (UBI): Smartphone telematics also supports UBI, where telematics data helps insurers calculate premiums more accurately based on driving behavior. This cost-saving benefit is driving its adoption within the insurance industry.

Asia Pacific is Expected to Witness Significant Growth

The Asia-Pacific region is witnessing significant growth in telematics adoption, largely driven by the rising demand for connected cars and IoT-enabled telematics solutions.

- China's automotive market: China is experiencing a boom in connected car telematics, with systems offering advanced features like real-time tracking and diagnostics. Government policies promoting telematics to reduce emissions and enhance traffic flow are contributing to this growth.

- India's logistics sector: In India, telematics adoption in logistics and transportation is increasing as companies seek to optimize routes and improve fuel efficiency through cloud-based systems.

- Japan's telematics innovation: Japan continues to lead telematics innovation, particularly in integrating telematics with IoT for connected car ecosystems. Japanese automakers are at the forefront of developing next-generation telematics solutions.

Telematics Industry Overview

The telematics market is semi consolidated, featuring a mix of global conglomerates and specialized players.

Diverse market players: Major players like AT&T, Geotab Inc., Cisco Systems Inc., Verizon, and MiX Telematics offer various telematics solutions. Global telecommunications companies leverage their network infrastructure, while specialized firms focus on fleet tracking and management.

Emerging strategies: Key success factors for market players include integrating AI-driven predictive analytics, expanding into electric vehicle telematics, and offering more scalable cloud-based solutions. Partnerships with automotive manufacturers and diversification of services will be critical for future growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Connected Devices

- 4.2.2 Huge Demand of Easy Vehicle Diagnostics

- 4.3 Market Restraints

- 4.3.1 Threat of Data Breaches

- 4.3.2 High Costs Associated With Installations

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of COVID-19 impact on the market

5 MARKET SEGMENTATION

- 5.1 By Channel

- 5.1.1 Original Equipment Manufacturers (OEM)

- 5.1.2 Aftermarket

- 5.2 By Solution

- 5.2.1 Smartphone

- 5.2.2 Portable

- 5.2.3 Embedded

- 5.3 By Offering Type

- 5.3.1 Hardware

- 5.3.2 Services (Entry-level, Mid-tier, High-end)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia

- 5.4.4 Australia and New Zealand

- 5.4.5 Latin America

- 5.4.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Mix Telematics

- 6.1.2 AT&T Inc.

- 6.1.3 Geotab Inc.

- 6.1.4 Verizon Telematics

- 6.1.5 Cisco Systems Inc.

- 6.1.6 Aplicom Oy

- 6.1.7 Microlise Ltd

- 6.1.8 LG Electronics Inc.

- 6.1.9 Trimble Inc.

- 6.1.10 Ctrack Global (Inseego Corp. Company)

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球汽车后市场远端资讯处理硬体市场 - 第四版

全球汽车后市场远端资讯处理硬体市场 - 第四版 车载资讯服务市场预测至2032年:按组件、技术、连接性、车辆类型、应用、销售管道和地区分類的全球分析

车载资讯服务市场预测至2032年:按组件、技术、连接性、车辆类型、应用、销售管道和地区分類的全球分析 汽车远端资讯处理服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车远端资讯处理服务市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 共享单车/踏板车车载资通讯系统的全球市场 - 第4版2032 年远端资讯系统晶片市场预测:按处理器核心、节点大小、核心组件整合、车辆类型、应用和地区进行的全球分析

共享单车/踏板车车载资通讯系统的全球市场 - 第4版2032 年远端资讯系统晶片市场预测:按处理器核心、节点大小、核心组件整合、车辆类型、应用和地区进行的全球分析 全球车载资讯服务市场按解决方案类型、连接类型、车辆类型、部署类型、应用程式和最终用户划分-2025-2032 年预测售后服务车载资讯服务市场(按组件类型、应用、连接类型、最终用户、分销管道和部署模式划分)-2025-2032年全球预测车用通讯系统市场(按组件、连接类型、车辆类型、应用和最终用户划分)—2025-2032 年全球预测车队远端资讯处理系统市场按车辆类型、部署类型、应用、通讯技术、组件类型和最终用户行业划分 - 全球预测 2025-2032远端资讯处理和车辆电子市场(按组件类型、连接性、车辆类型、安装和应用)—2025-2032 年全球预测

全球车载资讯服务市场按解决方案类型、连接类型、车辆类型、部署类型、应用程式和最终用户划分-2025-2032 年预测售后服务车载资讯服务市场(按组件类型、应用、连接类型、最终用户、分销管道和部署模式划分)-2025-2032年全球预测车用通讯系统市场(按组件、连接类型、车辆类型、应用和最终用户划分)—2025-2032 年全球预测车队远端资讯处理系统市场按车辆类型、部署类型、应用、通讯技术、组件类型和最终用户行业划分 - 全球预测 2025-2032远端资讯处理和车辆电子市场(按组件类型、连接性、车辆类型、安装和应用)—2025-2032 年全球预测