|

市场调查报告书

商品编码

1850397

自动化即服务:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Automation-as-a-Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

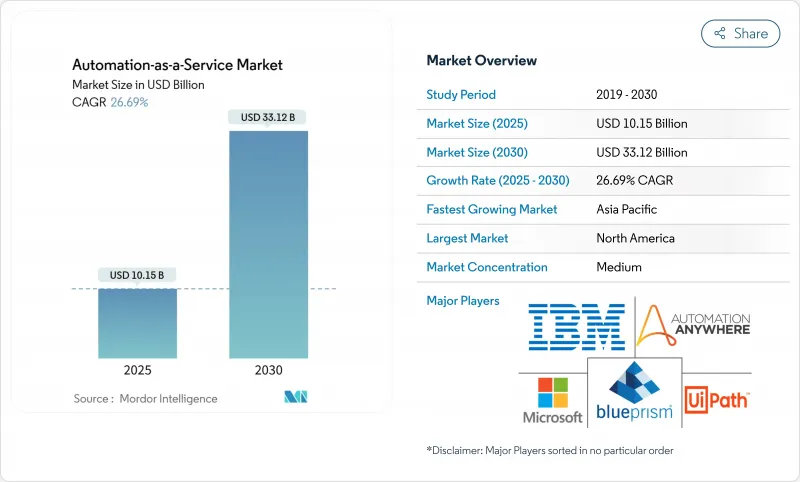

预计到 2025 年,自动化即服务市场规模将达到 101.5 亿美元,到 2030 年将达到 331.2 亿美元,年复合成长率为 26.7%。

随着企业将生成式人工智慧功能嵌入现有的机器人流程自动化投资中,并透过订阅收费降低资本支出,人工智慧的普及速度正在加快。强大的云端生态系、低程式设计工作室的兴起以及现成机器人领域市场的涌现,都在扩大潜在客户群。将流程挖掘诊断与事件驱动编配结合的集成,能够实现即时最佳化,从而将自动化程序从任务级改进提升到端到端的工作流程重构。拥有涵盖发现、建构和运行阶段的垂直整合技术堆迭的供应商,正在不断取代零散的解决方案,尤其是在需要统一管治的受监管行业。

全球自动化即服务市场趋势与洞察

业务流程自动化的需求不断增长

如今,44% 的新增自动化工作流程由业务部门创建,这表明非专业开发者正在为中央 IT 团队提供补充。营收营运计划占自动化工作流程的近一半,预示着自动化工作流程正向面向客户的用例转变。随着跨职能团队重新设计交接流程,市场对能够实现低程式码组合併同时管理细粒度权限的平台的需求日益增长。复杂性也不断增加:61% 的活跃机器人执行的是多步骤逻辑,而非单任务巨集。客户支援流程实现了三位数的成长,这表明在成本受限的经济週期中,自动化与客户留存策略紧密相关。

以云端优先的IT策略加速AaaS采用

多租用户架构使服务提供者能够在不安排停机的情况下向所有客户端实例推出新功能,从而缩短创新週期。基础设施即程式码模板透过标准化测试、预发布和生产层级的环境配置,进一步减少了摩擦。付费使用制使中小企业能够将自动化支出转移到营运预算中,并消除伺服器维护开销。采用混合架构的企业将对延迟敏感的工作负载部署在边缘,同时在云端集中编配策略,从而在自主规则和弹性扩展之间取得平衡。因此,以云端为中心的部署成长速度超过了整个自动化即服务市场的成长速度。

多租户云端中的资料安全和隐私问题

共用基础设施模型会增加横向移动的风险,尤其是在隔离控制失效的情况下,这对于金融服务和医疗保健行业的买家来说至关重要。当 AI Copilot 继承了广泛的 OAuth 权限范围时,这个问题会更加突出,因为它可能会透过提示注入的方式洩露敏感内容。欧洲监管机构正在强制执行严格的驻留权和自动决策揭露规则,要求供应商强制执行身份验证和日誌隔离以符合加密标准。供应商则透过客户管理的金钥、固定的区域资料储存和持续合规性仪表板来应对这些挑战。儘管采用新模式的势头强劲,但高度监管行业的买家正在分阶段采用风险较低的流程。

细分市场分析

到2024年,本地部署仍将占据自动化即服务市场68.4%的份额,这反映了各国政府严格的义务以及金融和公共部门的硬体投资。然而,随着企业将非关键工作流程和开发沙箱迁移到云端以减少基础设施维护,云端部署将以28.4%的复合年增长率成长。供应商现在提供满足审核要求的单一租户VPC选项,同时保持弹性扩充性和自动修补功能。边缘配置在本地处理对延迟敏感的任务数据,然后将增强后的有效负载路由到中央分析,从而创建兼顾性能和管治的混合拓扑结构。管理员可以根据成本和合规触发条件动态调整工作负载。这种灵活性使云端模式成为自动化即服务市场的长期成长引擎,尤其适用于从未拥有资料中心资产的待开发区数位化企业。

到2024年,解决方案将占总收入的66.8%,平台授权和机器人创作工作室将成为大多数买家的切入点。然而,随着企业寻求设计思维、变革管理和持续改进方面的专业知识,预计到2030年,服务业的收入将以28.1%的复合年增长率超过软体产业。託管服务提供者负责管理运作手册、监控机器人健康状况并应用安全补丁,使客户能够专注于核心创新。供应商生态系统中的顾问公司将流程挖掘诊断和超自动化蓝图打包,在不增加人员编制的情况下加快价值实现速度。随着复杂性的增加,服务品质成为关键的差异化因素,从而增强生态系统锁定,并提高整个自动化即服务市场的合约生命週期价值。

自动化即服务市场报告按部署类型(本地部署和云端部署)、组件(解决方案和服务)、业务功能(资讯科技、财务和会计、其他)、公司规模(大型企业和中小企业)、最终用户垂直行业(银行、金融服务和保险、通讯和 IT、零售和消费品、其他)以及地区进行细分。

区域分析

北美将在2024年以38.6%的收入主导,这得益于成熟的超大规模资料中心、密集的合作伙伴网路以及金融、医疗保健和公共服务等领域对平台的早期采用。美国企业正在部署认知机器人来协调ERP、CRM和垂直云平台上的数据,推动平台使用率高于全球平均。加拿大正在加速公共部门的采用,而墨西哥则利用自动化来增强其製造业近岸外包的竞争力。

亚太地区将实现最快成长,到2030年复合年增长率将达到27.3%。 《东协2025年数位发展总体规划》将促进跨国数位服务的标准化,推动公共部门自动化并迅速渗透到私部门。中国将扩大工厂机器人和城市机器人的应用规模,印度将实现IT服务工作流程的现代化,日本将利用对话式智能体解决老年护理领域的劳动力短缺问题。韩国将试办5G赋能的边缘自动化,澳洲将专注于提升采矿业的流程效率。

欧洲正在努力平衡创新与严格的资料保护监管。 GDPR 和提案的人工智慧管治法律要求纳入可解释的工作流程和审核日誌。瑞士、瑞典和德国的采用率最高,银行和製造商已将 AI Copilot 整合到关键营运中。南欧经济体依赖欧盟的数位化资金,从而催生了对平台即服务 (PaaS) 合约的新竞标。这些动态使自动化即服务 (AaaS) 市场在不同的宏观经济背景下保持了韧性。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 业务流程自动化的需求不断增长

- 云端优先的IT策略加速AaaS的采用

- 结合RPA和基因人工智慧实现超自动化

- 订阅和按使用量计费降低了中小企业的进入门槛。

- 特定领域机器人市场的出现

- 整合流程挖掘洞察,推动端到端自动化

- 市场限制

- 多租户云端中的资料安全和隐私问题

- 与传统/本地系统整合的复杂性

- 监管机构对演算法透明度和道德的审查

- 低程式码自动化管治人才短缺

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 评估宏观经济趋势对市场的影响

第五章 市场规模与成长预测

- 依部署类型

- 本地部署

- 云

- 按组件

- 解决方案

- 服务

- 按业务职能

- 资讯科技

- 财会

- 人力资源

- 销售与行销

- 营运/供应链

- 按公司规模

- 大公司

- 小型企业

- 最终用户

- BFSI

- 通讯/IT

- 零售和消费品

- 医疗保健和生命科学

- 製造业

- 政府和公共部门

- 其他终端使用者区域

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Automation Anywhere

- UiPath

- Blue Prism

- IBM

- Microsoft

- HCLTech

- Hewlett Packard Enterprise

- Kofax

- NICE

- Pegasystems

- ServiceNow

- Appian

- SAP

- Oracle

- Salesforce(MuleSoft/RPA)

- WorkFusion

- Celonis

- Nintex

- Workato

- AutomationEdge

第七章 市场机会与未来展望

The Automation-as-a-Service market size stands at USD 10.15 billion in 2025 and is forecast to reach USD 33.12 billion by 2030, advancing at a 26.7% CAGR.

Adoption is accelerating as enterprises embed generative-AI features into existing robotic-process-automation investments while containing capital outlays through subscription billing. Robust cloud ecosystems, the rise of low-code design studios, and the emergence of domain marketplaces for ready-made bots are widening the addressable customer base. Integrations that combine process-mining diagnostics with event-driven orchestration allow real-time optimization, pushing automation programs from task level gains to end-to-end workflow redesign. Vendors with vertically integrated stacks that span discovery, build and run phases continue to displace point solutions, especially in regulated industries that demand unified governance.

Global Automation-as-a-Service Market Trends and Insights

Rising Demand for Business-Process Automation

Business units now originate 44% of all newly automated workflows, signalling that citizen developers are complementing central IT teams. Revenue-operations projects account for nearly half of live automations, underscoring a pivot toward customer-facing use cases. As cross-functional teams re-engineer hand-offs, demand rises for platforms that can manage granular permissions while enabling low-code composition. Complexity is also increasing: 61% of active bots execute multistep logic rather than single-task macros. Customer support processes experienced triple-digit growth, showing that automation is firmly linked to retention strategies during cost-constrained economic cycles.

Cloud-First IT Strategies Accelerating AaaS Adoption

Multi-tenant architectures let providers roll out new capabilities to every client instance without scheduled downtime, shortening innovation cycles. Infrastructure-as-Code templates further reduce friction by standardising environment provisioning across testing, staging and production tiers. For SMEs, pay-as-you-go consumption shifts automation spending to operating budgets and removes server maintenance overhead. Enterprises with hybrid footprints place latency-sensitive workloads at the edge while orchestrating policies centrally in the cloud, balancing sovereignty rules with elastic scale. As a result, cloud-centric deployments are outpacing overall Automation-as-a-Service market growth.

Data-Security and Privacy Concerns in Multi-Tenant Clouds

Shared-infrastructure models increase lateral-movement risk if isolation controls fail, a top worry for financial-services and healthcare buyers. The issue is amplified when AI copilots inherit broad OAuth scopes, potentially exposing confidential content through prompt injections. European regulators enforce strict residency and automated-decision disclosure rules, forcing providers to certify encryption standards and segregate logs. Vendors respond with customer-managed keys, regionally pinned data stores and continuous compliance dashboards. Adoption momentum remains solid but buyers in highly regulated sectors proceed with staged rollouts that start with low-risk processes.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of RPA with Generative AI for Hyper-Automation

- Subscription and Usage-Based Pricing Lowering SME Entry Barriers

- Integration Complexity with Legacy/On-Prem Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise installations retained 68.4% share of the Automation-as-a-Service market in 2024, reflecting strict sovereignty mandates and sunk hardware investments within finance and public-sector domains. Nevertheless, cloud variants are expanding at a 28.4% CAGR as organisations migrate non-critical workflows and development sandboxes to reduce infrastructure upkeep. Vendors now provide single-tenant VPC options that satisfy audit requirements while preserving elastic scale and automated patching. Edge deployments process data locally for latency-sensitive tasks before routing enriched payloads to central analytics, creating a hybrid topology that balances performance with governance. Contracts increasingly bundle both operating modes under unified dashboards, enabling administrators to shift workloads dynamically based on cost or compliance triggers. This flexibility positions cloud models as the long-run growth engine of the Automation-as-a-Service market, particularly for green-field digital businesses that never owned data-centre assets.

Solutions accounted for 66.8% revenue in 2024 as platform licences and bot-authoring studios formed the entry point for most buyers. The services segment, however, is forecast to outpace software sales at 28.1% CAGR through 2030 as enterprises seek design thinking, change management and continuous-improvement expertise. Managed-service providers curate runbooks, monitor bot health and apply security patches, letting customers focus on core innovation. Advisory firms within the vendor ecosystem package process-mining diagnostics with hyper-automation blueprints, accelerating time to value without ballooning headcount. As complexity rises, service quality becomes a key differentiator, reinforcing ecosystem lock-in and boosting lifetime contract values across the Automation-as-a-Service market.

The Automation As A Service Market Report is Segmented by Deployment Type (On-Premise and Cloud), Component (Solution and Services), Business Function (Information Technology, Finance and Accounting, and More), Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (BFSI, Telecom and IT, Retail and Consumer Goods, and More), and Geography.

Geography Analysis

North America holds leadership with 38.6% revenue in 2024, supported by mature hyperscale data centres, a dense partner network and early platform adoption that spans finance, healthcare and public services. United States corporations deploy cognitive bots that reconcile data across ERP, CRM and vertical clouds, pushing platform utilisation rates above global averages. Canada accelerates public-sector use, while Mexico leverages automation to enhance near-shoring competitiveness in manufacturing.

Asia-Pacific registers the fastest growth at 27.3% CAGR through 2030. The ASEAN Digital Masterplan 2025 catalyses cross-border digital-service standards, spurring public-sector automation that quickly permeates private enterprises. China scales factory-floor robotics and city-administration bots, India modernises IT-service workflows, and Japan addresses labour shortages with conversational agents for elder-care. South Korea pilots 5G-enabled edge automations, while Australia focuses on mining-sector process efficiency.

Europe adopts a measured stance that balances innovation with rigorous data-protection oversight. GDPR and proposed AI-governance acts prompt demand for explainable workflows and built-in audit logs. Switzerland, Sweden and Germany exhibit the highest penetration rates, with banks and manufacturers integrating AI copilots into critical operations. Southern-European economies rely on EU funding for digitalisation, creating fresh bids for platform-as-a-service contracts. These dynamics keep the Automation-as-a-Service market resilient across varying macro-economic backdrops.

- Automation Anywhere

- UiPath

- Blue Prism

- IBM

- Microsoft

- HCLTech

- Hewlett Packard Enterprise

- Kofax

- NICE

- Pegasystems

- ServiceNow

- Appian

- SAP

- Oracle

- Salesforce (MuleSoft/RPA)

- WorkFusion

- Celonis

- Nintex

- Workato

- AutomationEdge

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for business-process automation

- 4.2.2 Cloud-first IT strategies accelerating AaaS adoption

- 4.2.3 Convergence of RPA with Gen-AI for hyper-automation

- 4.2.4 Subscription and usage-based pricing lowering SME entry barriers

- 4.2.5 Emergence of domain-specific bot marketplaces

- 4.2.6 Integration of process-mining insights to drive end-to-end automation

- 4.3 Market Restraints

- 4.3.1 Data-security and privacy concerns in multi-tenant clouds

- 4.3.2 Integration complexity with legacy/on-prem systems

- 4.3.3 Regulatory scrutiny over algorithmic transparency and ethics

- 4.3.4 Scarcity of low-code automation governance talent

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Component

- 5.2.1 Solution

- 5.2.2 Services

- 5.3 By Business Function

- 5.3.1 Information Technology

- 5.3.2 Finance and Accounting

- 5.3.3 Human Resources

- 5.3.4 Sales and Marketing

- 5.3.5 Operations / Supply-Chain

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-user Vertical

- 5.5.1 BFSI

- 5.5.2 Telecom and IT

- 5.5.3 Retail and Consumer Goods

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Verticals

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Automation Anywhere

- 6.4.2 UiPath

- 6.4.3 Blue Prism

- 6.4.4 IBM

- 6.4.5 Microsoft

- 6.4.6 HCLTech

- 6.4.7 Hewlett Packard Enterprise

- 6.4.8 Kofax

- 6.4.9 NICE

- 6.4.10 Pegasystems

- 6.4.11 ServiceNow

- 6.4.12 Appian

- 6.4.13 SAP

- 6.4.14 Oracle

- 6.4.15 Salesforce (MuleSoft/RPA)

- 6.4.16 WorkFusion

- 6.4.17 Celonis

- 6.4.18 Nintex

- 6.4.19 Workato

- 6.4.20 AutomationEdge

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

2026年全球自动化即服务市场报告

2026年全球自动化即服务市场报告 日本自动化服务市场规模、份额、趋势和预测:按组件、业务功能、公司规模、行业和地区划分,2026-2034年

日本自动化服务市场规模、份额、趋势和预测:按组件、业务功能、公司规模、行业和地区划分,2026-2034年 自动化服务市场 - 全球产业规模、份额、趋势、机会及预测(按部署类型、业务功能、公司规模、最终用户供应商、地区和竞争格局划分,2021-2031 年)

自动化服务市场 - 全球产业规模、份额、趋势、机会及预测(按部署类型、业务功能、公司规模、最终用户供应商、地区和竞争格局划分,2021-2031 年) 自动化即服务 (AaaS) 市场规模、份额和成长分析(按组件、部署类型、业务功能、组织规模、类型、最终用户行业和地区划分)—2026-2033 年行业预测数位客户体验和服务自动化市场-全球产业规模、份额、趋势、机会和预测,按分析工具、部署方式、应用领域、地区和竞争格局划分,2020-2030 年预测

自动化即服务 (AaaS) 市场规模、份额和成长分析(按组件、部署类型、业务功能、组织规模、类型、最终用户行业和地区划分)—2026-2033 年行业预测数位客户体验和服务自动化市场-全球产业规模、份额、趋势、机会和预测,按分析工具、部署方式、应用领域、地区和竞争格局划分,2020-2030 年预测 按组件、解决方案类型、公司规模、垂直行业和应用分類的自动化即服务市场 - 2025-2032 年全球预测

按组件、解决方案类型、公司规模、垂直行业和应用分類的自动化即服务市场 - 2025-2032 年全球预测 自动化即服务市场,按组件、按部署、按业务功能、按组织规模、按最终用户垂直、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测2025 年至 2033 年自动化即服务市场规模、份额、趋势及预测(按组件、业务功能、企业规模、垂直行业和地区划分)

自动化即服务市场,按组件、按部署、按业务功能、按组织规模、按最终用户垂直、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测2025 年至 2033 年自动化即服务市场规模、份额、趋势及预测(按组件、业务功能、企业规模、垂直行业和地区划分) AaaS(自动化即服务)市场:2025-2030 年预测

AaaS(自动化即服务)市场:2025-2030 年预测 2032 年客户经验和服务自动化市场预测:按类型、分析工具、部署模型、应用和地区进行的全球分析

2032 年客户经验和服务自动化市场预测:按类型、分析工具、部署模型、应用和地区进行的全球分析