|

市场调查报告书

商品编码

1433925

压力标籤:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Pressure Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

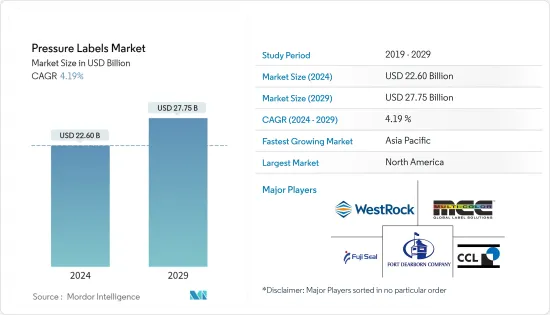

压力标籤市场规模预计到2024年为226亿美元,预计到2029年将达到277.5亿美元,在预测期内(2024-2029年)复合年增长率为4.19%。

製药业的成长,加上其在各个领域的广泛应用,是压力标籤市场的主要驱动力。最新的技术创新和对压力标籤产品不断增长的需求预计将推动市场成长。

主要亮点

- 全球最受欢迎的标籤技术仍然是感压标籤。广泛应用于食品工业。其应用范围不仅限于食品和饮料行业,还包括製药、消费品、个人护理和建筑等其他行业。

- 根据应用的不同,感压标籤可以使用各种黏剂製成永久性或可移除的。此外,极端温度不会对恶劣应用中使用的压感密封剂产生不利影响。它可以处理较厚的标籤(例如扩展内容标籤)的重量,使其适合各种最终用户应用,例如汽车用品、清洁产品、酒精、葡萄酒和烈酒、食品和饮料。

- 此外,随着消费者对永续性发展意识的不断增强,PS标籤的表面材料由可回收材料组成。此外,由于技术进步,许多公司已经开发出不影响回收的专有黏剂。借助此类永续技术,感压标籤有望巩固其行业领导者的地位。

- 此外,越来越多的感压标籤製造商正在使用 PE、PP、PET 和 PVC 聚合物薄膜材料为其产品提供附加功能。这些包括强度、防潮性、颜色、表面光滑度、透明度、高光泽度、耐用性和机械阻力。感压标籤带来的重要趋势包括永续性、坚固性、RFID、防伪标籤的兴起以及作为面材的可移除和可重新定位的薄膜。

- 儘管出现了 COVID-19 的情况,但食品、饮料和医疗保健行业仍显示出更令人鼓舞的成长。这些产业的供应商积极参与基本消费品和医疗保健产品标籤材料的持续生产和提供。然而,随着销售和生产的停止,大多数商家的损失更加严重。随着竞争的加剧和印刷装潢技术的发展,原料价格也在上涨。此外,俄罗斯和乌克兰之间的战争也影响整个包装生态系统。

压力标籤市场趋势

饮料最终用户市场预计将推动压力标籤的成长

- 由于对包装品牌产品的需求不断增长以及消费者对产品真实性和其他方面的了解不断增加,饮料最终用户类别预计将在预测期内实现最快的成长。

- 感压标籤至关重要,因为饮料标籤需要在各种情况下贴在容器上。无论应用环境是室温还是更具挑战性的温度(例如 20°F 至 40°F),饮料标籤的黏合剂设计都需要快速黏贴并在指定时保持在原位。儘管寒冷、潮湿和持续的产品处理,标籤和黏剂仍必须保持足够的耐用性。

- 防伪标籤的扩张预计将是压力标籤需求的驱动因素之一。这对食品企业尤其重要,因为它可以防止抄袭并证明用餐的真实性。防伪措施还可以帮助企业减少因假冒造成的收益和客户忠诚度损失。压力标籤主要用于食品和药品标籤,以透过 RFID 或条码追踪减少伪造。

- 标籤供应商正在透过创建和提供标籤产品来响应永续性趋势,以帮助饮料製造商实现永续性相关的包装目标。在回收系统中,可回收且易于从 PET 容器上剥离的感压标籤是 PET 容器上使用的标籤的一项新进步。例如,Hammer Packaging Inc. 与基材製造商密切合作,推动永续性计画。感压标籤业务涉及创造性解决方案的开发。

- 根据美国蒸馏酒委员会 (DISCUS) 的数据,优质烈酒占烈酒类别供应商总收入的比例最高,达 33%。同年,Value Spirits 的总收入成长最快。价值型烈酒与前一年同期比较成长8%,顶级烈酒成长3.8%。优质烈酒占供应商总收入的很大一部分这一事实表明,消费者对奢侈品和奢侈品的需求正在增加。这种模式显示消费者愿意花更多的钱购买优质产品和服务。因此,压力标籤市场可以透过提供优质标籤选项来满足这一需求,从而提高昂贵烈酒的感知价值和美学吸引力。例如,特殊饰面、压花、烫金或散发出优雅和独特气息的独特标籤材料。

北美市场预期成长

- 在美国,采用无线射频识别技术变得越来越重要,该技术使用无线电波来收集和通讯感压标籤上的信息。食品、饮料和药品只是监控、认证和防伪技术整合的最终用户产业。

- 根据美国人口普查局的报告,2021 年美国食品零售额达 8,803 亿美元,高于 2020 年的 8,502 亿美元。而且,2022年该产业年营收超过9,470亿美元,与前一年同期比较增7.6%。因此,未来几年食品包装产业的扩张可能会增加对感压标籤的需求。

- 作为该新产品线的一部分,莫霍克宣布与芬欧蓝泰标籤美洲公司建立策略关係。 Mohawk Renewal 亚麻纸和草纸表面材料可提供捲筒式感压标籤标籤解决方案。

- 合作伙伴关係也推动了该地区的市场需求。例如,Mark Andy 和芬欧蓝泰标籤最近在北美感压标籤产业建立了策略合作关係。此次合作将使这些公司能够开发包括环保柔弹性凸版印刷和数位转换器在内的印刷解决方案。

- 由于PSL的适应性,对PSL的需求不断增加。这迫使行业运营商提高能力,以满足不断增长的市场需求。例如,芬欧蓝泰标籤宣布打算于 2022 年 12 月在美国华盛顿州温哥华开设一个新航站楼。新工厂扩大了芬欧蓝泰标籤的分切和分销能力,同时支援该公司的北美终端网路。为了支持客户取得成功并满足对感压标籤不断增长的需求,芬欧蓝泰标籤持续投资于营运改善。

压力标籤行业概况

压力标籤市场高度分散,市场份额由 Multi-color Corporation、CCL Industries Inc、Westrock Company 和 Fuji Seal International Inc 等几家中小型企业占据。这也使得市场竞争激烈。

- 2022 年 10 月 - Multi-Color Corporation (MCC) 宣布签署协议,收购 Flexcoat 在巴西的标籤和层压板业务。中冶集团拟加大巴西产品扩张的投资。 Flexcoat 客户可以透过购买获得各种尖端标籤技术,从而增加他们的产品选择。

- 2022 年 5 月 - CCL Industries 宣布 Bolt 收购了 Avery。此次收购将有助于扩大CCL Industries的产品系列併提高区域製造能力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- 市场驱动因素

- 数位印刷技术的演变

- 市场限制因素

- 缺乏能够承受恶劣天气条件的产品

COVID-19 的市场影响

第六章市场区隔

- 按印刷工艺

- 凹版印刷

- 弹性凸版印刷

- 萤幕

- 凸版印刷

- 喷墨

- 原版印刷、原版印刷

- 按最终用户产业

- 食品

- 饮料

- 卫生保健

- 化妆品

- 家庭使用

- 工业(汽车、工业化学品、耐用消费品/非耐用消费品)

- 后勤

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 其他亚太地区

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争形势

- 公司简介

- Fort Dearborn Company

- Multicolor Corporation

- CCL Industries Inc

- Westrock Company

- Fuji Seal International Inc.

- Taylor Corporation

- Huhtamaki Group

- Taghleef Industries Inc(Al Ghurair Group)

- Coveris

- Avery Dennison Corp

- UPM Raflatac, Inc

- Inland Printing Co. Ltd

- Constantia Flexibles Group GmbH

- Folienprint RAKO GmbH

- Herma GmbH

- Skanem AS

第八章投资分析

第9章市场的未来

The Pressure Labels Market size is estimated at USD 22.60 billion in 2024, and is expected to reach USD 27.75 billion by 2029, growing at a CAGR of 4.19% during the forecast period (2024-2029).

Growth in the pharmaceutical industry, coupled with its vast application scope in diverse sectors, is the major driver for the pressure labels market. The latest innovations in pressure label products and rising demand is expected to fuel the market growth.

Key Highlights

- The most popular label technology worldwide will continue to be pressure-sensitive labels. They are used extensively in the food business. Their uses extend beyond the food and beverage industry, including the pharmaceutical, consumer goods, personal care, and other sectors, including construction.

- Depending on the application, different adhesives can make pressure-sensitive labels permanent or releasable. Furthermore, temperature extremes would not harm pressure-sensitive sealants for heavy-duty applications. They are appropriate for applications across a range of end-users, including automotive items, cleaning products, alcohol, wine, spirits, food, and beverage, because they can handle the weights of thick labels, such as expanded content labels.

- Additionally, in keeping with consumers' increased awareness of sustainability, the face stock of PS Labels is comprised of recyclable materials. Furthermore, through technical breakthroughs, numerous businesses created unique adhesives that do not obstruct recycling. Pressure Sensitive labels are anticipated to strengthen their position as industry leaders with the aid of sustainable technologies like these.

- Additionally, a growing portion of pressure-sensitive label makers uses PE, PP, PET, and PVC polymer film materials to provide their products with additional functionality. It includes strength, moisture resistance, color, smoothness on the surface, transparency, high gloss, durability, and mechanical resistance. Important trends offered by pressure-sensitive labels include sustainability, robustness, RFID, a rise in anti-counterfeit labels, and detachable and repositionable films as face stock.

- The food, beverage, and healthcare sectors showed more encouraging growth despite the COVID-19 scenario. The suppliers to these sectors are actively engaged in the ongoing production and provision of label materials for essential consumer and healthcare products. However, with sales and production on hold, most merchants' losses are worsening. Along with increased competition and developing printing and decorating technologies, the price of raw materials is also rising. Further, the Russia-Ukraine war also impacts the overall packaging ecosystem.

Pressure Labels Market Trends

Beverage End-User Segment is Expected to Drive Growth of Pressure Labels

- With the rising demand for packaged and branded products and rising consumer knowledge of the authenticity and other aspects of the product, the beverage end-user category is anticipated to see the fastest growth over the projection period.

- Because beverage labels must stick to the container in various situations, pressure-sensitive labeling is essential. Whether the application environment is room temperature or something more difficult, like 20F to 40F, an adhesive design for beverage labeling should stick rapidly and stay in place as needed. Despite cold, dampness, and continuous product handling, the label and adhesive must maintain the appropriate durability.

- One driving demand for Pressure Labels is anticipated to be the expansion of Anti-Counterfeit Labels. As it discourages copying and verifies the meal's authenticity, this is particularly crucial for the food business. Anti-counterfeiting measures also assist businesses in reducing revenue and customer loyalty losses brought on by counterfeiting. Pressure labels are mostly used to label food and pharmaceutical products to decrease counterfeiting using RFID or barcode tracking.

- Label suppliers are responding to sustainability trends by creating and providing label goods to assist beverage manufacturers in achieving their sustainability-related packaging goals. In recycling systems, pressure-sensitive labels that are recyclable and effortlessly removed from PET containers are new advances for labels used on PET containers. For instance, Hammer Packaging Inc. collaborates closely with substrate producers to promote sustainability initiatives. For its pressure-sensitive label business, it includes developing creative solutions.

- The highest percentage of supplier gross income in the spirits category, 33%, belongs to high-end spirits, according to the Distilled Spirits Council of the United States (DISCUS). Value spirits saw the fastest increase in gross income during that same year. Value spirits had an increase of 8% over the prior year, while premium spirits saw an increase of 3.8%. The fact that premium spirits comprised the greatest portion of supplier gross income suggests increased consumer demand for high-end and upscale goods. This pattern implies consumers are prepared to shell out more money for premium goods and services. Consequently, the Pressure Labels Market can satisfy this need by offering premium labeling options that raise expensive spirits' perceived value and aesthetic appeal. Some examples might include specialized finishing, embossing, foil stamping, or distinctive label materials that exude elegance and exclusivity.

North America is Expected to Register Market Growth

- The incorporation of radio-frequency identification, which employs radio waves to gather and communicate information in pressure-sensitive labels, became more important in the United States. Food, drinks, and medicines are only end-user verticals with technological integration for monitoring, authentication, and anti-counterfeiting items.

- The US Census Bureau reports that retail food store sales in the United States reached USD 880.30 billion in 2021 instead of USD 850.20 billion in 2020. Additionally, the industry had yearly sales of over USD 947 billion in 2022, representing a 7.6% rise over the same period in 2021. Thus, the need for pressure-sensitive labels will rise in the upcoming years due to the expanding food packaging sector.

- Mohawk declares a strategic relationship with UPM Raflatac Americas as a part of this new product line. Mohawk Renewal Hemp and Straw paper face stocks can provide roll-fed, pressure-sensitive labeling solutions.

- Partnerships are also driving the market demand in the region. For instance, Mark Andy and UPM Raflatac recently formed a strategic relationship in the North American pressure-sensitive label industry. This collaboration should enable these players to create printing solutions that are both flexographic and digital converters friendly to the environment.

- The demand for PSLs is rising as a result of their adaptability. The industry's operators are compelled by this to increase their capabilities, allowing them to meet the escalating demand of the market. As an illustration, UPM Raflatac declared intentions to open a brand-new terminal in Vancouver, Washington, in the United States, in December 2022. The new location will expand UPM Raflatac's slitting and distribution capabilities while supporting the company's North American terminal network. To support the success of its clients and meet the increasing demand for pressure-sensitive labels, UPM Raflatac consistently invests in operational enhancements.

Pressure Labels Industry Overview

The Pressure Labels Market is highly fragmented as several small and medium-sized players, such as Multi-color Corporation, CCL Industries Inc, Westrock Company, and Fuji Seal International Inc, contain a share in the market. Also, this makes the market extremely competitive too.

- October 2022- Multi-Color Corporation (MCC) announced the signing of a deal to acquire Flexcoat's label and lamination businesses in Brazil. MCC intends to increase its investment in Brazil's product expansion. Flexcoat's clients can access a wider variety of cutting-edge label technologies and increased product choices through the purchase.

- May 2022- CCL Industries announced that Bolt acquired Avery. The acquisition will help CCL Industries expand its product portfolio and increase its regional production capacity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Market Drivers

- 4.4.1 Evolution of Digital Print Technology

- 4.5 Market Restraints

- 4.5.1 Lack of Products with Ability to Withstand Harsh Climatic Conditions

5 Impact of COVID-19 on the Market

6 MARKET SEGMENTATION

- 6.1 By Print Process

- 6.1.1 Gravure

- 6.1.2 Flexography

- 6.1.3 Screen

- 6.1.4 Letterpress

- 6.1.5 Inkjet

- 6.1.6 Other Processes (Offset Lithography, Electrophotography)

- 6.2 By End-User Industry

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Healthcare

- 6.2.4 Cosmetics

- 6.2.5 Household

- 6.2.6 Industrial (Automotive, Industrial Chemicals, and Consumer and Non-consumer Durables)

- 6.2.7 Logistics

- 6.2.8 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Spain

- 6.3.2.5 Rest of Europe

- 6.3.3 Asia Pacific

- 6.3.3.1 China

- 6.3.3.2 India

- 6.3.3.3 Japan

- 6.3.3.4 Rest of Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fort Dearborn Company

- 7.1.2 Multicolor Corporation

- 7.1.3 CCL Industries Inc

- 7.1.4 Westrock Company

- 7.1.5 Fuji Seal International Inc.

- 7.1.6 Taylor Corporation

- 7.1.7 Huhtamaki Group

- 7.1.8 Taghleef Industries Inc (Al Ghurair Group)

- 7.1.9 Coveris

- 7.1.10 Avery Dennison Corp

- 7.1.11 UPM Raflatac, Inc

- 7.1.12 Inland Printing Co. Ltd

- 7.1.13 Constantia Flexibles Group GmbH

- 7.1.14 Folienprint RAKO GmbH

- 7.1.15 Herma GmbH

- 7.1.16 Skanem AS