|

市场调查报告书

商品编码

1435945

一次性塑胶包装:市场占有率分析、行业趋势和统计、成长预测(2024-2029)Global Single Use Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

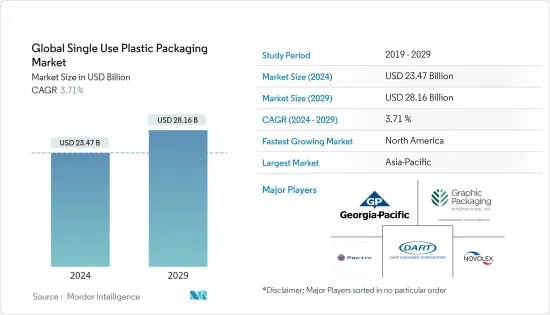

预计2024年全球一次性塑胶包装市场规模为234.7亿美元,预计到2029年将达到281.6亿美元,在预测期(2024-2029年)将成长37.1亿美元,复合年增长率为% 。

COVID-19 大流行为一次性塑胶包装供应商带来了极大的缓解。儘管许多国家已逐渐禁止此类包装并推广可重复使用的包装,但疫情改变了消费者和政府对包装的行为。

由于COVID-19的爆发,对能量饮料和保健食品的需求急剧增加。这些产品大部分采用一次性塑胶包装。全球范围内的订单规模如此之大,以至于该行业的製造商和包装公司甚至扩大了设施,这也得到了大多数政府的支持。

主要亮点

- 推动市场成长的因素包括对线上食品配送服务的需求不断增长以及一次性包装的使用带来了更多的便利性和实用性。儘管一次性塑胶对环境产生重大影响,但由于与其他材料相比,它们重量轻且耐用,因此仍然被大量使用。然而,随着一次性塑胶替代品普及显着的市场渗透,这种推动的有效性将逐渐减弱。

- 根据 Business Insider 报导,美国线上包装食品销售额预计将从 2012 年的 60 亿美元增至 2021 年的 1,660 亿美元。由于最终用户行业消费的增加,对一次性塑胶包装的需求也在增加。由于一次性包装成本低且可用性高,大多数最终用户都采用一次性包装。这也影响着世界各地的回收业。

- 随着一些国家禁止使用一次性塑料,一些公司正在将其生产线从塑料转向天然纤维。例如,BFG Eco Packaging 采用聚苯乙烯和聚丙烯製造盒子、盘子和托盘,并使用甘蔗纤维(一种来自砂糖过程的产品)来生产其产品。英国包装製造商 Vegwear 也关注基于纺织品的宏观趋势。该公司使用可再生植物性材料,因为天然纤维可提供经济耐用的外带盒。

- 欧盟到 2021 年对各种一次性塑胶产品的禁令正面临威胁,因为消费者和餐厅因为担心传染病而越来越依赖它们。与可重复使用的塑胶产品相比,消费者和供应商更喜欢一次性塑胶。例如,鑑于新冠疫情,星巴克宣布在全球所有门市暂停使用可重复使用的杯子。

一次性塑胶包装市场趋势

PET预计将显着成长

- 在原料树脂中,PET是一种主要材料,占据了80%以上的市场占有率,因为它成本低廉,并且可以轻鬆改变其物理性能,以满足广泛的客户需求。

- 聚对聚对苯二甲酸乙二酯(PET) 由于其高抗衝击性以及改进的防潮和气体阻隔性而用于碳酸饮料包装。它具有坚固的结构和高强度。此外,与高密度聚苯乙烯(HDPE)包装相比,具有紫外线阻隔性的宝特瓶的光泽外观往往对于延长产品保质期非常突出,并且玻璃般的透明度已成为各种包装的标准。

- 例如,2021年2月,可口可乐推出了13.2盎司的可口可乐、健怡可乐、零糖可乐和可口可乐口味等商标品牌。由 100% 再生 PET (rPET) 塑胶製成的瓶子在加州、佛罗里达州和东北部的一些州推出,今年夏天其他发泡饮料品牌也纷纷效仿。

- PET 包装的回收率高度依赖回收基础设施的可用性和可近性,因此这是影响特定地区市场成长的关键因素。例如,如今,居住在人口 125,000 人或以上的社区的美国居住者中有 94% 使用回收计划。

- 市场上的供应商致力于提高PET一次性塑胶包装的可回收性,以符合法规并在回收方面形成封闭回路型循环。随着人们越来越重视回收这些材料,预计 PET 一次性塑胶包装将会成长。

北美实现温和成长

- 食品服务业是重要的最终用户产业之一,在杯子和盖子市场中占据主要份额。线上食品配送服务的成长增加了对食品杯的需求。按地区划分,美国是世界第二大食品市场。用于食品包装的塑胶用量约占塑胶总量的 40%。此外,根据美国人口普查局的数据,美国外食服务总销售额达到 602 万美元。

- 政府的打击也对市场产生负面影响。然而,由于疫情持续,纽约州一次性塑胶袋禁令于2020年3月1日生效,并延至2020年5月15日。塑胶需求的激增可能只是暂时的改变。向循环经济转型的短期努力和目标。除此之外,塑胶製造链也可能面临压力。

- 此外,2020 年 10 月,美国能源局(DOE) 宣布为 12 个计划提供超过 2,700 万美元的资金,以支持先进塑胶回收再利用技术和可回收设计的新型塑胶的开发。

- 作为能源部塑胶创新挑战的一部分,这些计划还将帮助改进现有的回收工艺,将塑胶分解成可用于製造新产品的化学成分。此类倡议可支持一次性塑胶包装市场

- 儘管该地区多年来一直在考虑采取监管措施,但 COVID-19感染疾病减缓了此类法律的实施,并为市场带来了急需的缓解。此次疫情实际上推迟了欧盟将欧盟一次性塑胶指令(SUPD)转化为国家法律的立法程序。例如,义大利的塑胶税已从2020年延后到2021年,该国海洋保护机构Malevivo正在鼓励全面禁止塑胶杯。

一次性塑胶包装行业概况

全球一次性塑胶包装市场高度整合。一次性塑胶包装市场各公司之间的竞争由于 Dart Container Corporation、Georgia-Pacific LLC 和 Graphic Packaging International, Inc. 等几家主要企业的存在,公司之间的竞争加剧。收购使这些公司在市场上占据了更强大的地位。

- 2021 年 5 月 - Novolex 旗下欧洲热成型包装专家 Waddington Europe 透过添加开创性的热填充选项升级了其 TamperVisible 系列保护性包装产品。 TamperVisible 产品系列让最终用户放心,因为里面的食品就像准备时一样安全。

- 2021 年 5 月 - Interfor Corporation 与 Georgia-Pacific Wood Products LLC 和 GPGP Wood Products LLC 达成协议,收购位于密西根州 Bay Springs、阿拉巴马州费耶特、路易斯安那州德昆西和奥勒冈州Philomath 的四家锯木厂业务。收购价格为3.75亿美元,包括营运资金,将全部由库存现金提供资金。

- 2021 年 7 月 - Graphic Packaging Holding Company 推出 OptiCycle,这是一系列非聚乙烯 (PE) 涂层一次性食品包装产品,可取代传统 PE 和聚乳酸 (PLA) 涂层产品。该解决方案将由当地供应商在北美进行商业化,其设计目的是透过使液体隔离层与纸张顺利分离来实现轻鬆回收。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌意强度

- 市场驱动因素

- 市场挑战

- 市场机会

第五章 评估 COVID-19 对产业的影响

第六章食品服务业形势

- 按地区分類的食品服务市场需求

- 食品服务市场需求(依类别)

第七章 一次性塑胶包装的管理规定

第八章一次性塑胶包装的生命週期

第九章市场区隔

- 按材质

- 聚乳酸(PLA)

- 聚对苯二甲酸乙二酯(PET)

- 聚乙烯(PE)

- 其他类型的材料

- 依产品类型

- 瓶子

- 翻盖式

- 托盘、杯子、盖子

- 其他产品类型

- 按最终用户

- 快速服务餐厅

- 全方位服务餐厅

- 设施

- 零售

- 其他最终用户

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第10章竞争形势

- 公司简介

- Georgia-Pacific LLC

- Graphic Packaging International, Inc.

- Novolex

- Pactiv LLC

- Ardagh Group SA

第十一章 市场未来前景

The Global Single Use Plastic Packaging Market size is estimated at USD 23.47 billion in 2024, and is expected to reach USD 28.16 billion by 2029, growing at a CAGR of 3.71% during the forecast period (2024-2029).

The COVID-19 pandemic provided significant relief to the single-use packaging vendors. Although many countries were slowly banning such packaging and promoting reusable packaging, the outbreak changed the consumers' and governments' behavior toward them.

Due to the COVID-19 outbreak, the demand for nutritional drinks and healthy food increased exponentially. The majority of these products are packaged with single-use plastic. The orders were so huge on a global level that the manufacturers and packaging companies in the field even expanded their facilities, which was also supported by most of the governments.

Key Highlights

- Factors driving the market's growth include the growing demand for online food delivery services and the use of single-use packaging that offers increased convenience and utility. Single-use plastics are still being considerably used due to their lightweight and durable properties compared to other materials, despite having significant effects on the environment. However, the effect of the driver will gradually decrease once alternatives to single-use plastics gain significant traction in the market.

- According to Business Insider, online packaged food sales in the United States are expected to reach USD 166 billion in 2021 from USD 6 billion in 2012. The growth in end-user industry consumption is also increasing the demand for single-use packaging. Most of these end-users are adopting single-use packaging due to their low cost and easy availability. This has also affected the recycling industry across the world.

- Several companies are switching their production lines from plastic to natural fiber-based options due to the ban on single-use plastics in several countries. For instance, BFG Eco Packaging, which makes boxes, plates, and trays from polystyrene and polypropylene, makes products using sugarcane fiber, a sub-product obtained during the sugar manufacturing process. Also, banking on the fiber-based macro trend is Vegware, a UK packaging manufacturer, which uses renewable plant-based materials as the natural fibers provide an economical, sturdy takeaway box.

- The EU's ban on a range of single-use plastic items by 2021 came under threat as more consumers and restaurants became more dependent on disposable plastic products due to contagion fears. Consumers and vendors prefer single-use plastic to reusable plastic products. For instance, given the pandemic, Starbucks announced a temporary pause on reusable cups across its global outlets.

Single Use Packaging Market Trends

PET is Expected to Witness Significant Growth

- PET, among the raw material resin, is the dominant material capturing a market segment of more than 80% due to the easiness with which the physical property is altered to suit a wide variety of customer's needs while maintaining low costs.

- Polyethylene terephthalate (PET) is used for carbonated drinks packaging due to its high impact-resistant nature and improved moisture and gas barrier properties. They have a rigid structure with high strength. Moreover, compared to high-density polyethylene (HDPE) packaging, the glossy appearance of PET bottles with ultraviolet barriers often stand out for extending the shelf life of products, making the glass-like transparency a standard for a variety of packaging.

- For instance, in February 2021, Coca-Cola's trademark brands, which include Coke, Diet Coke, Coke Zero Sugar, and Coca-Cola Flavors, introduced a 13.2-oz. bottle made from 100% recycled PET (rPET) plastic in California, Florida, and select states in the Northeast, with other sparkling beverage brands following this summer.

- The rate of recycling of PET packaging highly depends on the availability and accessibility of recycling infrastructure and therefore serves as a significant factor impacting the growth of the market in a particular region. For instance, currently, 94 percent of U.S. residents living in communities with a population of more than 125,000 have recycling programs available to them.

- The vendors in the market are focusing on increasing the recyclability of PET single use packaging in order to adhere to the regulations as well as create a closed loop cycle in terms of recycling. The increasing emphasis on recycling of these materials is expected to provide growth prospects to PET single use packaging.

North America to Witness Moderate Growth

- The food service industry is one of the prominent end-user industries that hold a significant share in the cups and lids market. The growth of online food delivery services augmented the demand for food cups. Among regions, the United States is the second-largest food market across the world. The volume of plastic allocated to food packaging amounts to approximately 40% of plastics. Moreover, according to the US Census Bureau, the total foodservice sales in the United States amounted to USD 6.02 million.

- The government enforcements also harm the market. However, due to the ongoing pandemic New York State's ban on single-use plastic bags, which went into effect on March 1, 2020, it was postponed to May 15, 2020. Such a spike in plastic demand would likely lead to a temporary change in the short-term initiatives and goals of transitioning to a circular economy. Apart from this, it is likely to put pressure on the plastic manufacturing chain.

- Moreover, in October 2020, the US Department of Energy (DOE) announced over USD 27 million in funding for 12 projects that will support the development of advanced plastics recycling technologies and new plastics that are recyclable-by-design.

- As part of DOE's Plastics Innovation Challenge, these projects will also help improve existing recycling processes that break plastics into chemical building blocks, which can then be used to make new products. Such initiatives might support the single-use plastic packaging market

- In spite ofthe regulatory measures that have been on the table for the last few years in the region, the COVID-19 pandemic has stalled the imposition of such legislation and has provided the market with a much-needed lifer for the time. The pandemic has effectively postponed the legislative process of the European Union for the transposition of the EU Single-Use Plastic Directive (SUPD) into domestic law. For instance, Italy's Plastic tax has been postponed from 2020 to 2021, with Marevivo, the maritime protection agency of the country, encouraging a complete ban on plastic cups.

Single Use Packaging Industry Overview

The Global Single-Use Plastic Packaging Market is Highly Consolidated . The competitive rivalry amongst the players in the single-use packaging market is high owing to the presence of some key players such as Dart Container Corporation, Georgia-Pacific LLC, Graphic Packaging International, Inc., etc. Through strategic partnerships, mergers, and acquisitions, these players have been able to gain a stronger footprint in the market.

- May 2021- European thermoforming packaging specialist Waddington Europe, a division of Novolex, upgraded its TamperVisible range of protective packaging products by adding a pioneered Hot Fill option. The TamperVisible range of products reassures the end-user that the food inside is as safe as the day it was prepared.

- May 2021 -Interfor Corporation signed an agreement with Georgia-Pacific Wood Products LLC and GP Wood Products LLC to acquire four sawmill operations located in Bay Springs, Miss., Fayette, Ala., DeQuincy, La., and Philomath, Ore. The total purchase price of USD 375 million, including working capital, will be funded entirely from cash on hand.

- July 2021 - Graphic Packaging Holding Company launched OptiCycle, a line of non-polyethylene (PE) coated, single-use foodservice packaging, which is an alternative to classic PE and polylactic acid (PLA) coated products. The solution is to be commercialized in North America by a local supplier and designed to be easily recyclable by allowing the smooth separation of the liquid barrier layer from the paper.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.5 Market Challenges

- 4.6 Market Opportunities

5 ASSESMENT OF COVID-19 IMPACT ON THE INDUSTRY

6 FOODSERVICE INDUSTRY LANDSCAPE

- 6.1 Foodservice Market Demand by Region

- 6.2 Foodservice Market Demand by Category

7 SINGLE-USE PLASTIC PACKAGING REGULATIONS

8 LIFECYCLE of SINGLE-USE PLASTIC PACKAGING

- 8.1 (Collection, Sorting, Recycling. End Of Life)

9 MARKET SEGMENTATION

- 9.1 By Material

- 9.1.1 Polylactic Acid (PLA)

- 9.1.2 Polyethylene Terephthalate (PET)

- 9.1.3 Polyethylene (PE)

- 9.1.4 Other Types of Materials

- 9.2 By Product Type

- 9.2.1 Bottles

- 9.2.2 Clamshells

- 9.2.3 Trays, Cups & Lids

- 9.2.4 Other Product Types

- 9.3 By End-User

- 9.3.1 Quick Service Restaurants

- 9.3.2 Full Service Restaurants

- 9.3.3 Institutional

- 9.3.4 Retail

- 9.3.5 Other End-users

- 9.4 By Geography

- 9.4.1 North America

- 9.4.2 Europe

- 9.4.3 Asia-Pacific

- 9.4.4 Latin America

- 9.4.5 Middle East & Africa

10 COMPETITIVE LANDSCAPE

- 10.1 Company Profiles*

- 10.1.1 Georgia-Pacific LLC

- 10.1.2 Graphic Packaging International, Inc.

- 10.1.3 Novolex

- 10.1.4 Pactiv LLC

- 10.1.5 Ardagh Group S.A.

11 FUTURE OUTLOOK OF THE MARKET

2024年塑胶纸板包装全球市场报告

2024年塑胶纸板包装全球市场报告 软塑胶包装市场 - 全球产业规模、份额、趋势、机会和预测,按类型、基础树脂、印刷技术、最终用户、地区和竞争细分,2019-2029F

软塑胶包装市场 - 全球产业规模、份额、趋势、机会和预测,按类型、基础树脂、印刷技术、最终用户、地区和竞争细分,2019-2029F 2024 年 PCR 塑胶包装全球市场报告

2024 年 PCR 塑胶包装全球市场报告 2030 年塑胶包装市场预测:按产品、类型、材料类型、技术、最终用户和地区进行的全球分析

2030 年塑胶包装市场预测:按产品、类型、材料类型、技术、最终用户和地区进行的全球分析 2024 年塑胶替代包装全球市场报告

2024 年塑胶替代包装全球市场报告 全球塑胶包装 - 市场份额分析、行业趋势与统计、成长预测(2024 - 2029)

全球塑胶包装 - 市场份额分析、行业趋势与统计、成长预测(2024 - 2029) 2030 年塑胶瓦楞包装市场预测:按包装类型、材料类型、最终用户和地区进行的全球分析

2030 年塑胶瓦楞包装市场预测:按包装类型、材料类型、最终用户和地区进行的全球分析 到 2030 年消费后回收 (PCR) 塑胶包装市场预测:按产品、材料、最终用户和地区分類的全球分析

到 2030 年消费后回收 (PCR) 塑胶包装市场预测:按产品、材料、最终用户和地区分類的全球分析 软塑胶包装(软包装)市场报告:2030 年趋势、预测与竞争分析

软塑胶包装(软包装)市场报告:2030 年趋势、预测与竞争分析 软塑胶包装市场:按类型、印刷技术、应用划分 - 2024-2030 年全球预测

软塑胶包装市场:按类型、印刷技术、应用划分 - 2024-2030 年全球预测