|

市场调查报告书

商品编码

1435953

通讯营运管理:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Telecom Operations Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

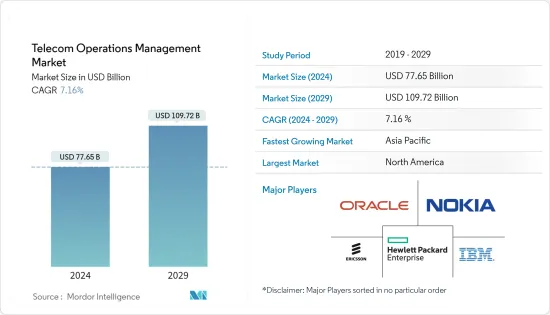

2024年通讯营运管理市场规模预估为776.5亿美元,预估至2029年将达1,097.2亿美元,预测期间(2024-2029年)复合年增长率为7.16%。

由于 COVID-19感染疾病迫使数百万员工和学生留在家里,电信业者应对其网路频宽需求增加 30% 至 40%,有必要为营运做好适当准备。据 FieceTelecom 称,冠状病毒大流行已促使各种规模的企业加速其数位转型计画。已经致力于数位转型和实施云端策略的公司能够更好地度过大流行的头几週。 Verizon Business 调查结果反映了几点,其中 43% 的受访者目前计划透过数位和相关技术来发展业务。此外,30% 的企业已经增加了以数位方式交付产品和服务的新方式。

主要亮点

- 电讯业被认为是积极进行数位转型的行业之一,因为它是全球数位化的主要推动力,也正在见证市场环境的巨大变化。我是。

- 电讯业对互通性和技术的投资加强了全球经济中资本流动和资讯的模式转移,并为整个产业全新经营模式的出现奠定了基础。随着频宽需求的迅速增长和行动网路用户数量的增加,通讯服务供应商正在不断发展以提供先进和创新的解决方案。

- 此外,传统网路加上 5G 网路不断增加的基础设施需求,创造了一个复杂的环境,对通讯服务供应商(CSP) 来说是一个挑战。因此,越来越需要在电讯实施技术先进的营运支援系统。

- 对低成本资料和语音服务不断增长的需求正在推动市场成长。这激励服务供应商以批发价从 MNO 购买网路服务,并以低于 MNO 的价格将其作为配套服务出售。

- 现在大多数组织都是多供应商、多重云端的,这增加了网路架构的复杂性,并进一步扩大了有待开拓的市场。此外,由于这些组织的目标是使用有限的资源来满足需求并简化变更流程,因此他们需要更灵活、更具适应性的网路架构。

- 此外,云端、机器对机器 (M2M) 交易和行动货币等服务的成长预计将在预测期内进一步增加对通讯营运管理的需求。

- 此外,随着企业变得更加行动化并采用 BYOD 等新概念来改善员工互动和易用性,提供快速、高品质的网路变得至关重要。组织期待在业务中积极采用 BYOD,从而推动预测期内的市场成长。

通讯营运管理市场趋势

云端预计将经历显着成长

- 世界各地的电信业者正在踏上以云端为中心的转型之旅,以推动新的服务、商机和体验。通讯业者可以透过将云端原生、开放、模组化的解决方案与完全託管的高效能云端平台相结合来加速他们的工作。云端提供者正在重点关注几个战略区域来支援电信业者。其中包括帮助电信业者将 5G 作为商业服务平台收益,透过资料驱动的体验增强客户参与度,以及帮助提高核心通讯系统的营运效率。其中包括:

- 2021 年 10 月,戴尔科技推出新的通讯软体、解决方案和服务,帮助通讯服务供应商(CSP) 加速开放、云端原生网路的部署并创造新的商机。 Open RAN (ORAN) 等新兴技术为 CSP 提供了广泛的选择来部署支援未来成长的网路基础架构。

- Google与 Amdocs 合作,使通讯服务供应商能够在 Google Cloud 上运行 Amdocs 市场领先的产品组合,并为企业客户提供新的资料分析、站点可靠性工程和 5G 边缘解决方案。 Amdocs 宣布 Altice USA 已在 Google Cloud 上运作Amdocs 的资料和情报系统,作为 Amdocs 和 Google Cloud 联合开拓倡议的一部分。此外,与 Netcracker 的新合作伙伴关係将把整个数位 BSS/OSS 和编配堆迭部署到 Google Cloud。服务供应商现在可以按需扩展和购买关键任务 IT 应用程式、存取无限的 Google Cloud 资源、降低拥有成本并加快新服务的可用性。

- 2021年6月,AT&T与微软合作,将其5G行动核心网路迁移至微软Azure混合云端。微软将收购AT&T的网路云平台技术,该技术运行AT&T的5G核心。该交易还包括购买 AT&T 工程和生命週期管理软体来运行容器化或虚拟网路服务。

- 此外,ZENIC ONE(UME)系统是第一个整合人工智慧和巨量资料的系统,透过工具和应用程式增加管理和控制。因此,系统即时收集设备上报的运作信息,结合AI智能巨量资料分析监控网路运作状态,快速辨识问题并恢復服务,维运效率得以大幅提升。此类案例预计将有力推动市场成长。

- 爱立信预计,2021年全球智慧型手机用户数将超过60亿,预计未来几年将增加数亿。用户的增加将推动预测期内的市场成长。此外,数位印度计划等倡议预计将改善通讯营运中云端平台或云端为基础的模型的集成,从而推动市场成长。

北美预计将占据很大份额

- 由于业务运营解决方案的支出较高,预计北美将在接受调查的通讯运营管理市场中占据很大份额。此外,由于通讯之间的激烈竞争,该地区的电讯高度发达,该地区的电讯分析市场预计将进一步扩大。用于客户支援的IT基础设施和技术的不断进步、大量的市场供应商以及管理日常业务和帮助台软体熟练的技术专业知识的可用性正在推动通讯运营管理市场的增长。当地社区。

- 市场上出现了一些新的参与者,进一步推动了市场的成长。例如,阿达尼集团于2022年7月确认进入行动电话通讯领域,并计画于2022年推出。作为其市场扩张计划的一部分,该公司计划在澳洲推出三家新的无线服务供应商。该公司是最早进入该领域的印度公司之一。该集团还提案在北美市场投资10亿美元。

- 此外,消费行为的变化、行动互联网和智慧型手机的普及、支付能力的提高以及本地相关内容的可用性的增加正在推动电子商务、金融服务、视讯和社交媒体的成长。因此,北美对通讯营运管理的需求不断上升。

- 连网型设备设备和行动装置的显着增加正在推动对增强网路服务的需求。北美一直处于技术采用的前沿,因此该地区的连网型设备采用率最高。

- 例如,根据思科系统公司的数据,2018年北美地区人均设备和连接数量为8.2个,预计到2023年将达到13.4个,是全球所有地区中最高的,是最好的。预计此类趋势将成为区域市场成长的主要动力。

- 此外,物联网、多重云端环境和人工智慧等技术进步增加了网路架构的复杂性。根据 GSMA 的数据,到 2025 年,北美的物联网连接数量预计将从 2019 年的 28 亿增加到 54 亿。因此,这些技术的引入增加了对灵活、适应性强的网路架构的需求,推动了市场的成长。区域性的。

通讯营运管理产业概述

通讯营运管理市场竞争激烈且分散。这是由于 IBM 公司、Oracle 公司、Telefonaktiebolaget LM Ericsson、Hewlett Packard Enterprise Development LP 和诺基亚公司等重要公司的存在。知名公司正在结盟并宣布创新解决方案,以增加市场占有率。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌意强度

- 替代产品的威胁

- 评估 COVID-19感染疾病对市场的影响

- 行业用例

第五章市场动态

- 市场驱动因素

- 营运成本和复杂性增加

- 市场挑战

- 缺乏高效率的系统整合商

第六章市场区隔

- 按发展

- 本地

- 云

- 按类型

- 软体

- 网路管理

- 客户和产品管理

- 收益管理

- 库存管理等

- 服务

- 软体

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争形势

- 公司简介

- IBM Corporation

- Telefonaktiebolaget LM Ericsson

- Oracle Corporation

- Hewlett Packard Enterprise Development LP

- Nokia Corporation

- Amdocs Inc.

- Netcracker Technology Corp

- Cisco Systems Inc.

- Accenture PLC

- SAP SE

- NEC Corporation

- Comarch SA

- ZTE Corporation

- ServiceNow Inc.

- TATA Consultancy Services Limited

第八章投资分析

第九章市场机会与未来趋势

The Telecom Operations Management Market size is estimated at USD 77.65 billion in 2024, and is expected to reach USD 109.72 billion by 2029, growing at a CAGR of 7.16% during the forecast period (2024-2029).

With the outbreak of COVID-19, telecom companies should be well equipped to handle the operations for meeting the 30% to 40% increase in bandwidth demand on their networks as millions of employees and students became homebound. According to FieceTelecom, the coronavirus pandemic has pushed companies of all sizes to accelerate their digital transformation plans. The companies that had already engaged in the adoption of digital transformation and cloud strategies were better able to sustain in the first few weeks of the pandemic. Verizon Business' survey results echoed some of the points, including 43% of the respondents now planning to expand their businesses through digital and related technologies. Also, 30% have already added new methods for delivering their products and services digitally.

Key Highlights

- The telecommunications industry is regarded as one of the significant adopters of digital transformation, both as a key driver of worldwide digitization and as an industry witnessing a large-scale change in its market environment.

- Investment by the telecommunications industry in interoperability and technology has reinforced a paradigm shift in capital flows and information through the global economy while providing the building blocks for the emergence of entirely new business models across industries. With the rapidly growing demand for bandwidth and the increasing number of mobile Internet users, communication service providers are evolving to offer advanced and innovative solutions.

- Also, legacy networks, combined with the growing infrastructure requirements for 5G networks, have created a complex environment, making it challenging for communication service providers (CSPs). Hence, the need for the adoption of technologically advanced operations support systems in telecommunications is increasing.

- The continuously growing need for low-cost data and voice services is boosting the market growth. This is encouraging the service providers, who purchase the network services from the MNOs at wholesale rates and sell these as bundled services at lower rates than those of MNOs.

- The market studied is augmented by the increasing complexity in network architectures, as most enterprise organizations have multi-vendor, multi-cloud configurations. Furthermore, as these organizations aim to meet the demand with limited resources and streamline their change processes, they require more flexible and adaptable network architectures.

- In addition, the increasing number of services such as cloud, Machine to Machine (M2M) transactions, and mobile money are further expected to augment demand for telecom operations management over the forecast period.

- Furthermore, with businesses going mobile and adopting new concepts like BYOD to increase employee interaction and ease of use, it has become essential to provide a high speed and quality network. The organizations are looking forward to adopting BYOD aggressively in their operations, thereby fueling the market growth over the forecast period.

Telecom Operations Management Market Trends

Cloud is Expected to Witness Significant Growth

- Telecom companies worldwide are embarking on transformation journeys centered on the cloud to drive new services, revenue opportunities, and experiences. The telecom operators can accelerate the journey by combining their cloud-native, open and modular solutions with the fully managed, high-performing Cloud platform. Cloud providers are focusing on some strategic regions to support telecommunications companies. These include helping telecommunications companies monetize 5G as a business services platform, empowering them to engage their customers through data-driven experiences better, and assisting them in improving operational efficiencies across core telecom systems.

- In Oct 2021, Dell Technologies introduced new telecom software, solutions, and services to help communications service providers (CSPs) accelerate their open, cloud-native network deployments and create new revenue opportunities. New technologies like Open RAN (ORAN) give CSPs a broader set of options for deploying network infrastructure to support future growth.

- Google announced a partnership with Amdocs to enable communications service providers to run Amdocs' market-leading portfolio on Google Cloud and to deliver new data analytics, site reliability engineering, and 5G edge solutions to enterprise customers. Amdocs announced that Altice USA had gone live with Amdocs data and intelligence systems on the Google Cloud as part of the Amdocs and Google Cloud joint go-to-market initiative. Also, a new partnership with Netcracker to deploy its entire Digital BSS/OSS and Orchestration stack on Google Cloud. Service providers can now scale and purchase their mission-critical IT applications on-demand, access unlimited Google Cloud resources, reduce ownership costs, and accelerate new services' availability.

- In June 2021, AT&T partnered with Microsoft to shift its 5G mobile core network to Microsoft Azure's hybrid cloud. Microsoft is acquiring AT&T's Network Cloud platform technology that runs AT&T's 5G core. The deal also involves buying AT&T engineering and lifecycle management software that runs containerized or virtualized network services.

- Moreover, the ZENIC ONE (UME) system integrates Artificial Intelligence and Big Data for the first time to add management and control with tools and applications. Therefore, the system can collect the information related to the operation reported by the device in real-time and combine AI intelligent big data analysis to monitor the network operation status, promptly pinpoint problems and recover services, thus significantly improving the O&M efficiency. Such instances are expected to provide a strong impetus for market growth.

- As per Ericsson, the number of smartphone subscriptions worldwide surpassed six billion in 2021 and is expected to grow further by several hundred million in the next few years. This increase in users will drive market growth over the forecasted period. Additionally, initiatives such as the Digital India initiative are expected to uplift the cloud platform integration or cloud-based model in telecom operation that will drive the market growth.

North America is Expected to Hold Significant Share

- North America is anticipated to occupy a significant share in the telecom operations management market studied, owing to the region's high expenditure on business operation solutions. Besides, telecommunications in the region is highly developed with intense competition among the communication providers, which is expected further to boost the market for telecom analytics in the region. The continuous advancements in IT infrastructure and technology used for customer support, a significant number of market vendors, and the accessibility of proficient technical expertise in managing the daily operations and helpdesk software contribute toward the telecom operations management market growth region.

- The market is witnessing several new players, further driving the market growth. For instance, in July 2022, Adani Group confirmed its entry into the cellular telecom space and will do so with a rollout in 2022. The company is expected to release three new wireless service providers in Australia as part of its planned expansion into the market, making it one of the first Indian firms to enter this area. The group has also proposed to invest USD 1 billion in the North American market.

- Furthermore, the shift in consumer behavior, along with rising mobile internet adoption and smartphone, improved affordability, and the increasing availability of locally relevant content, has led to a boom in mobile services across areas such as e-commerce, financial services, video, and social media. As a result, the demand for telecom operations management has been witnessing an upward trend in North America.

- Substantial growth in connected and mobile devices is spurring the demand for enhanced network services. Since North America has always remained at the forefront of technology adoption, the region witnessed the maximum adoption of connected devices.

- For instance, according to Cisco Systems, the average number of devices and connections per capita in North America stood at 8.2 in 2018 and is expected to reach 13.4 by 2023, which is the highest amongst any other region globally. Such trends are expected to act as major drivers for growth in the regional market.

- Further, deploying technological advancements, such as IoT, multi-cloud environments, or AI, increases network architectures' complexity. According to the GSMA, the number of IoT connections in North America is expected to reach 5.4 billion in 2025, compared to 2.8 billion in 2019. Hence, deploying these technologies is increasing the demand for flexible and adaptable network architectures, thereby fueling the market growth in the region.

Telecom Operations Management Industry Overview

The Telecom Operations Management Market is highly competitive and fragmented. This is due to the presence of significant players such as IBM Corporation, Oracle Corporation, Telefonaktiebolaget LM Ericsson, Hewlett Packard Enterprise Development LP, Nokia Corporation, etc. The prominent companies are entering into collaborations and are launching innovative solutions to increase their market share.

- February 2022 - Telecom Egypt and Grid Telecom have signed a strategic MoU for new subsea cable options between Greece and Egypt. The two companies will explore connectivity options between Greece and Egypt, as well as the use of Telecom Egypt's and Grid Telecom's networks and international footprint through interconnectivity to neighboring countries.

- September 2021 - Vodafone in Oman has signed an agreement with Ericsson to deploy, operate and maintain a new 4G and 5G core and radio access (RAN) greenfield network. Ericsson will supply a complete core network solution based on Ericsson Cloud Core, Cloud VoLTE, and NFVI, as well as an end-to-end transport network solution.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Denition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Assessment of Impact of COVID-19 on the Market

- 4.4 Industry Use Cases

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Operational Costs and Complexity

- 5.2 Market Challenges

- 5.2.1 Shortage of Efficient System Integrators

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Type

- 6.2.1 Software

- 6.2.1.1 Network Management

- 6.2.1.2 Customer and Product Management

- 6.2.1.3 Revenue Management

- 6.2.1.4 Inventory Management and Others

- 6.2.2 Services

- 6.2.1 Software

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Telefonaktiebolaget LM Ericsson

- 7.1.3 Oracle Corporation

- 7.1.4 Hewlett Packard Enterprise Development LP

- 7.1.5 Nokia Corporation

- 7.1.6 Amdocs Inc.

- 7.1.7 Netcracker Technology Corp

- 7.1.8 Cisco Systems Inc.

- 7.1.9 Accenture PLC

- 7.1.10 SAP SE

- 7.1.11 NEC Corporation

- 7.1.12 Comarch SA

- 7.1.13 ZTE Corporation

- 7.1.14 ServiceNow Inc.

- 7.1.15 TATA Consultancy Services Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年电信营运管理全球市场报告

2024 年电信营运管理全球市场报告 全球电信运营管理市场

全球电信运营管理市场 通信网络能源效率将每年提高12%:每兆瓦时能源消耗的流量将从2020年的12.3TB增长到2022年的15.5TB,但进一步提高效率对于降低成本和排放至关重要

通信网络能源效率将每年提高12%:每兆瓦时能源消耗的流量将从2020年的12.3TB增长到2022年的15.5TB,但进一步提高效率对于降低成本和排放至关重要 电信运营管理市场:2023-2028年全球行业趋势、份额、规模、增长、机会及预测

电信运营管理市场:2023-2028年全球行业趋势、份额、规模、增长、机会及预测 2016-2022 年电信运营费用 (OPEX) 分析:2022 年网络运营费用和折旧成本驱动的网络运营费用将占电信公司总运营费用的一半

2016-2022 年电信运营费用 (OPEX) 分析:2022 年网络运营费用和折旧成本驱动的网络运营费用将占电信公司总运营费用的一半 电信营运管理市场:依软体类型、服务、部署类型划分 - 2023-2030 年全球预测

电信营运管理市场:依软体类型、服务、部署类型划分 - 2023-2030 年全球预测 Web 3.0的通讯业者:驾驭不断变化的服务和基础设施格局

Web 3.0的通讯业者:驾驭不断变化的服务和基础设施格局 通讯业者的5G代价 - 2022年债务增加,较低利润:COVID以后,投资剧增,部分通讯业者陷入困境- 随着利率上升和新收入未能出现,需要管理债务增加

通讯业者的5G代价 - 2022年债务增加,较低利润:COVID以后,投资剧增,部分通讯业者陷入困境- 随着利率上升和新收入未能出现,需要管理债务增加 健康市场上通讯业者的策略

健康市场上通讯业者的策略 通讯运用管理的全球市场 2022-2026

通讯运用管理的全球市场 2022-2026