|

市场调查报告书

商品编码

1436003

疫苗物流 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Vaccine Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

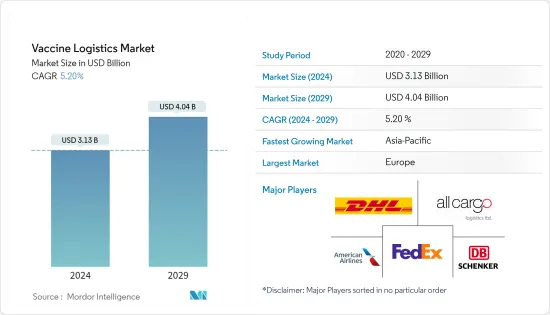

2024年疫苗物流市场规模估计为31.3亿美元,预计到2029年将达到40.4亿美元,在预测期内(2024-2029年)CAGR为5.20%。

新疫苗、免疫计划和服务提供策略的多样性、目标人群的扩大、冷链基础设施要求的增加以及资金不足是可能进一步影响疫苗运输市场的一些新现实。

现有系统难以跟上国家和国际免疫规划不断变化的步伐,特别是在开发出 COVID-19 疫苗之后,导致缺货、本可避免的浪费和冷链能力不足。所有上述因素都具有相当大的覆盖范围、性能和成本影响。

由于COVID-19疫情带来的疫苗储存服务需求大幅成长,药厂着力打造冷链物流。因此,随着研发力道的加大,未来几年疫苗冷链物流市场可能会出现新的成长前景。

疫苗物流市场趋势

製药业的成长

随着政府采取措施促进全球製药业的成长并加剧市场内的竞争,全球对製药物流的需求可能会增加。随着全球製药业持续强劲成长,温控产品子类别也蓬勃发展。世界各地的製药商越来越关注产品品质和敏感度。复杂生物药物的开发以及荷尔蒙治疗、疫苗和复杂蛋白质的运输需要冷链改进,从而需要温控运输和仓储。

药品和医疗器材的温控物流是医疗保健物流业中一个显着成长的部分。此外,对有效的冷链物流服务以维持商品品质的需求的增加正在推动市场的成长。

到 2027 年,对创新药物的需求将推动肿瘤学支出达到约 3,700 亿美元,几乎是目前水准的两倍。

印度是全球最大的仿製药供应商,占全球供应量的20%,也是全球领先的疫苗製造商,市占率达60%。

医疗保健领域快速通道援助的重要性日益增加,也推动了医药物流市场的发展。此外,透过建立单一来源配销通路来降低分销成本正在推动对医药物流的需求。

冷链物流发展

大多数疫苗不具备热稳定性,包括用于白喉、破伤风、百日咳 (DTP) 以及麻疹、腮腺炎和德国麻疹 (MMR) 的疫苗。通常,不热稳定且未正确冷藏的疫苗会在短时间内变质,因为这些疫苗含有生物物质,如果不在 2°C 至 8°C 之间储存,就会降解。因此,大多数疫苗依赖冷藏或冷链配送,其中包括几个阶段。

能够在不同温度下分多个部分装载货物的冷藏车正在进一步开发并受到欢迎。冷链服务供应商还安装无线射频识别 (RFID) 和工业物联网 (IIoT),透过提供对敏感产品的位置、属性和状况的更多了解来帮助解决冷链效率低下的问题。

该公司还在开发具有封闭温控系统的高科技货柜,以便在货物仓库和飞机之间无缝运送对温度敏感的货物。这些容器专为製药业而设计。

2022 年 8 月,Azenta Inc. 同意收购 B Medical Systems Sa rl 及其子公司。此次收购透过提供独特的解决方案来安全、可追溯地运输温度敏感样本,从而扩展了 Azenta 的冷链能力。作为 Azenta 的一部分,B Medical 将获得样本管理的丰富知识和工程技能,并扩大在北美和欧洲的市场份额。

疫苗物流行业概况

疫苗物流市场分散,由大和、德国邮政敦豪集团和日本通运等国际公司主导。这些国际公司正专注于透过收购来实施扩张策略。他们的强大影响力帮助他们比小企业更容易扩张市场。

随着 COVID-19 大流行,在政府投资不断增加的支持下,市场对冷藏仓库、快速和受控配送服务以及疫苗大宗运输的需求预计将增加,这为市场参与者提供了扩大其业务的机会从长远来看,影响范围和效率。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究成果

- 研究假设

- 研究范围

第 2 章:研究方法

- 分析方法

- 研究阶段

第 3 章:执行摘要

第 4 章:市场动态与洞察

- 当前的市场状况

- 市场动态

- 司机

- 温控包装技术创新

- 加强医疗基础设施的跨境合作与倡议

- 限制

- 供应链中断和运输瓶颈可能会阻碍疫苗的及时分发

- 机会

- 采用区块链和物联网技术可以提高透明度和可追溯性

- 司机

- 技术趋势和自动化

- 政府法规和倡议

- 产业价值链/供应链分析

- 聚焦环境/温度控制存储

- 产业吸引力-波特五力分析

- COVID-19 对市场的影响

第 5 章:市场细分

- 按服务

- 运输

- 陆(公路和铁路)

- 空气

- 海

- 仓储

- 加值服务(包装、标籤等)

- 运输

- 按最终用户

- 医院

- 药品製造商和分销商

- 其他最终使用者(血库、诊所等)

- 按地理

- 亚太

- 中国

- 日本

- 澳洲

- 印度

- 新加坡

- 马来西亚

- 印尼

- 泰国

- 韩国

- 亚太其他地区

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 欧洲其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 哥伦比亚

- 阿根廷

- 南美洲其他地区

- 中东

- 埃及

- 卡达

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 中东其他地区

- 亚太

第 6 章:竞争格局

- 市场集中度概览

- 公司简介

- DHL Global Forwarding

- AllCargo Logistics

- American Airlines

- DB Schenker

- FedEx Corporation

- Kuehne Nagel

- Nippon Express

- Yamato Logistics

- Americold Logistics

- lynden international logistics

- DP World

- Coldman Logistics

- Cavalier Logistics*

- 其他公司

第 7 章:全球疫苗物流市场的未来

第 8 章:附录

The Vaccine Logistics Market size is estimated at USD 3.13 billion in 2024, and is expected to reach USD 4.04 billion by 2029, growing at a CAGR of 5.20% during the forecast period (2024-2029).

The wide variety of new vaccines and immunization schedules and service delivery strategies, the expanding target population, the increased cold-chain infrastructure requirements, and insufficient funding are some of the new realities that may further impact the vaccine transportation market.

The existing systems are struggling to keep pace with the changing landscape of national and international immunization programs, especially after the development of the COVID-19 vaccine, resulting in stock-outs, avoidable wastage, and inadequate cold-chain capacity. All the aforementioned factors have considerable coverage, performance, and cost implications.

Due to the enormous rise in demand for vaccine storage services brought on by the COVID-19 epidemic, pharmaceutical companies focused their efforts on creating cold chain logistics. Therefore, the vaccine cold chain logistics market will probably see new growth prospects in the coming years due to the increasing R&D initiatives.

Vaccine Logistics Market Trends

Growth in the Pharmaceutical Sector

With government initiatives to improve the pharmaceutical industry's growth worldwide and fuel competition within the market, the demand for pharma logistics may increase globally. As strong growth continues across the global pharmaceuticals industry, the sub-category of temperature-controlled products is also surging. Pharmaceutical manufacturers around the world are increasingly focusing on product quality and sensitivity. The development of complex biological-based medicines and the shipment of hormone treatments, vaccines, and complex proteins, which require cold chain refinements, result in a need for temperature-controlled transportation and warehousing.

Temperature-controlled logistics for pharmaceutical products and medical devices is a significantly growing segment of the healthcare logistics industry. Moreover, the increase in the need for effective cold chain logistics services to maintain the quality of goods is fueling the growth of the market.

Demand for innovative drugs will drive oncology spending to approximately USD 370 billion by 2027, almost double the current level.

India is the largest provider of generic medicines globally, occupying a 20% share in global supply by volume, and is the leading vaccine manufacturer globally with a market share of 60%.

The rising importance of fast-track assistance in the healthcare sector is also driving the market for pharmaceutical logistics. Moreover, decreasing the distribution cost by creating a single-source distribution channel is boosting the demand for pharmaceutical logistics.

Development in Cold Chain Logistics

Thermal stability is not a property of most vaccines, including those used against diphtheria, tetanus, pertussis (DTP), and measles, mumps, and rubella (MMR). Typically, vaccines that are not heat-stable and not properly refrigerated spoil over a short period because these vaccines contain biological matter that degrades when not stored between 2°C and 8°C. As a result, most vaccines rely on refrigerated or cold-chain distribution, which consists of several stages.

The refrigerated trucks that can hold goods in multiple segments at different temperatures are being developed further and gaining popularity. Cold chain service providers are also installing radio-frequency identification (RFID) and Industrial Internet of Things (IIoT) to help address cold chain inefficiencies by providing increased insights into the location, properties, and condition of sensitive products.

Companies are also developing high-tech containers with a closed temperature-controlled system to deliver temperature-sensitive goods between cargo warehouses and aircraft seamlessly. These containers are specially designed to serve the pharmaceutical industry.

In Aug 2022, Azenta Inc. has agreed to acquire B Medical Systems S.a r.l. and its subsidiaries. This acquisition expands Azenta's cold chain capabilities by providing distinct solutions for safely and traceably transporting temperature-sensitive specimens. As part of Azenta, B Medical will gain substantial knowledge and engineering skills in sample management and an expanded market presence in North America and Europe.

Vaccine Logistics Industry Overview

The vaccine logistics market is fragmented and is dominated by international companies, such as Yamato, Deutsche Post DHL Group, and Nippon Express. These international companies are focusing on expansion strategies through acquisitions. Their strong presence helps them expand in the market more easily than the smaller players.

With the COVID-19 pandemic, the market is expected to experience an increased demand for refrigerated warehouses, fast and controlled delivery services, and the bulk transportation of vaccines, backed by the increasing government investment providing opportunities to the players in the market to expand their reach and efficiency in the long run.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 technology innovation in temperature controlled packaging

- 4.2.1.2 Cross Border collaborations and initiative to enhance healthcare infrastructure

- 4.2.2 Restraints

- 4.2.2.1 Supply chain distruption and transportation bottlenecks can hinder timely vaccine distribution

- 4.2.3 Opportunities

- 4.2.3.1 Adoption of blockchain and IoT technology can improve transparency and tracebility

- 4.2.1 Drivers

- 4.3 Technological Trends and Automation

- 4.4 Government Regulations and Initiatives

- 4.5 Industry Value Chain/Supply Chain Analysis

- 4.6 Spotlight on Ambient/Temperature-controlled Storage

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.1.1 Land (Road and Rail)

- 5.1.1.2 Air

- 5.1.1.3 Sea

- 5.1.2 Warehousing

- 5.1.3 Value-added Services (Packaging, Labeling, etc.)

- 5.1.1 Transportation

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Drug Manufacturers and Distributors

- 5.2.3 Other End Users (Blood Banks, Clinics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 Australia

- 5.3.1.4 India

- 5.3.1.5 Singapore

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Thailand

- 5.3.1.9 South Korea

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 North America

- 5.3.3.1 United States

- 5.3.3.2 Canada

- 5.3.3.3 Mexico

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Colombia

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Egypt

- 5.3.5.2 Qatar

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Rest of the Middle East

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles*

- 6.2.1 DHL Global Forwarding

- 6.2.2 AllCargo Logistics

- 6.2.3 American Airlines

- 6.2.4 DB Schenker

- 6.2.5 FedEx Corporation

- 6.2.6 Kuehne Nagel

- 6.2.7 Nippon Express

- 6.2.8 Yamato Logistics

- 6.2.9 Americold Logistics

- 6.2.10 lynden international logistics

- 6.2.11 DP World

- 6.2.12 Coldman Logistics

- 6.2.13 Cavalier Logistics*

- 6.3 Other Companies

7 FUTURE OF THE GLOBAL VACCINE LOGISTICS MARKET

8 APPENDIX

非紧急医疗运输市场:按类型、产品类型、最终用户划分 - 全球预测 2024-2030

非紧急医疗运输市场:按类型、产品类型、最终用户划分 - 全球预测 2024-2030 2024 年非紧急医疗运输全球市场报告

2024 年非紧急医疗运输全球市场报告 2024 年病患运输服务全球市场报告

2024 年病患运输服务全球市场报告 医疗运输市场:按类型和最终用途行业 - 2024-2030 年全球预测

医疗运输市场:按类型和最终用途行业 - 2024-2030 年全球预测 医疗保健分销 -市场占有率分析、行业趋势/统计、2024-2029 年成长预测

医疗保健分销 -市场占有率分析、行业趋势/统计、2024-2029 年成长预测 2024 年医疗保健分销全球市场报告

2024 年医疗保健分销全球市场报告 南美洲和中美洲非紧急医疗运输市场预测至 2028 年 - 区域分析 - 按服务类型和应用

南美洲和中美洲非紧急医疗运输市场预测至 2028 年 - 区域分析 - 按服务类型和应用 2028 年亚太地区非紧急医疗运输市场预测 - 区域分析 - 按服务类型和应用

2028 年亚太地区非紧急医疗运输市场预测 - 区域分析 - 按服务类型和应用 医疗保健分销市场报告:2030 年趋势、预测和竞争分析

医疗保健分销市场报告:2030 年趋势、预测和竞争分析 医疗保健分销市场:按类型、最终用户划分 - 俄罗斯-乌克兰衝突、高通胀的累积影响 - 2023-2030 年全球预测

医疗保健分销市场:按类型、最终用户划分 - 俄罗斯-乌克兰衝突、高通胀的累积影响 - 2023-2030 年全球预测