|

市场调查报告书

商品编码

1437885

农业感测器:市场占有率分析、行业趋势和统计、成长预测(2024-2029)Agricultural Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

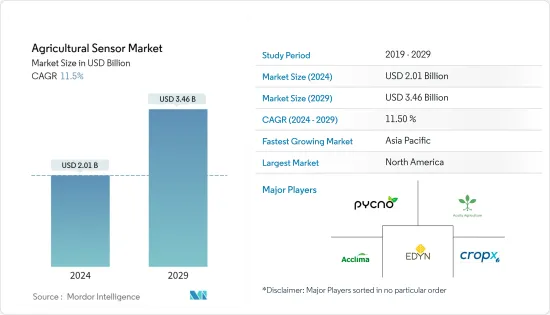

农业感测器市场规模预计到 2024 年为 20.1 亿美元,预计到 2029 年将达到 34.6 亿美元,在预测期内(2024-2029 年)增长 11.5%。复合年增长率为

主要亮点

- 农业生产需求的增加、技术实践的变化、精密农业的集中、低耕管理、先进技术等是推动农业感测器市场的一些因素。

- 农业感测器预计将在该地区全面扩展。由于精密农业中精确定位的需求,位置感测器近年来受到广泛关注。在中国,2018年,以「天、地、空间」为座右铭的大型农业数位园区在黑龙江现代农业示范区成立。 「Sky」是卫星遥感探测资料,「Space」是感测资料,即无人机遥感探测资料,「Ground」是地面物联网资料。

- 许多农业技术公司正在开发创新,透过专注于无线平台来使农业变得更容易,这些平台可以实现产量监测、作物健康监测、田间测绘、灌溉调度、作物管理等方面的即时决策。我们开发了一个模型,支持处境不利的农民。农产品价格波动;

- 北美仍然是市场最大的地理区域,并占据主要市场占有率。随着智慧农业技术的大量投资和广泛采用,感测器农业在预测期内显示出显着增长的潜力。严格的环境法规、大大小小的农场主越来越多地采用精密农业以及提高田间生产力的产量监测技术预计将推动市场的发展。

农业感测器市场趋势

减少劳动力需求

精准室内农业技术需要新技术来应对气候条件变化和熟练劳动力减少的挑战。当仅在室内种植作物时,农民可以控制光照水平、养分水平和湿度水平。具有强大功能的小型控制系统的传感器使公司能够实现系统自动化并以更好的方式提高产量比率。安装感测器后,可减少劳动力约20.0%。农业感测器可以解决室内农场的劳动力挑战。

大型工业室内农场使用的感测器可侦测水污染、农药残留、营养缺乏、疾病侵袭等。室内农业和农业感测器的结合提高了作物的生产能力,并有可能推动未来农业感测器市场的发展。

因此,土壤湿度感测器等高科技灌溉工具可以帮助农民确定每个区域所需的水位。支援物联网的设备上的智慧灌溉应用程式可以帮助控制和监控灌溉设备,并根据不断变化的需求进行调整。两者都代表了在地下水位下降的地区可以实施精准灌溉的广泛领域。这些因素可能会在预测期内推动市场。

北美市场占据主导地位

北美是农业感测器最大的区域市场。政府对增加农业产量的大力支持、基础设施支持的可用性以及对智慧和岁差农业方法的接受增加了先进农业解决方案的采用。在北美,土壤湿度感测器的采用正在迅速增加。土壤湿度计用于运动草坪场,以更有效地监测和转化草坪。研究表明,透过使用感测器,农民可以最大限度地减少干旱压力,并将保护性耕作维护和人事费用减少至少 20%。

美国是精密农业技术的早期采用者,这是该地区在全球市场中占最大份额的一个主要因素。近年来,美国农业部门在采用智慧农业实践方面经历了一场突破性的革命。物联网(IoT)行动电话设备、基于齿轮感测器的灌溉和施肥设备、阀门位置感测器等基于感测器的技术的出现在该领域相对较新,也是国内出现的新现象..对感测器的需求主要是由于机械化率的提高和农民采用的智慧农业实践。加拿大对现代农业方法的高度认可促进了该行业的发展。

农业感测器产业概况

农业感测器市场较为分散,市场上有各种中小企业和少数大型企业,竞争激烈。市场上的主要企业包括 Edyan、Acclima Inc.、CropX inc.、Pycno、Acquity Agriculture 等。全球不同地区的区域市场和本土企业的发展是市场区隔的主要驱动力。北美和亚太地区是竞争对手活动最活跃的两个地区。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章 简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场限制因素

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 新进入者的威胁

- 竞争公司之间的敌意强度

第五章市场区隔

- 类型

- 湿度感测器

- 电化学感测器

- 机械感测器

- 空气流量感知器

- 光学感测器

- 压力感测器

- 水感测器

- 土壤感测器

- 牲畜感测器

- 其他类型

- 目的

- 酪农管理

- 土壤管理

- 气候管理

- 水资源管理

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 泰国

- 日本

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 非洲

- 南非

- 非洲其他地区

- 北美洲

第六章 竞争形势

- 最采用的策略

- 市场占有率分析

- 公司简介

- Libelium Comunicaciones Distribuidas Sl

- Auroras

- Acquity Agriculture

- Pycno

- Agsmarts Inc.

- Edyn

- Acclima Inc.

- Caipos GmbH

- Vegetronix Inc.

- Sentek Ltd

- Aquaspy Inc.

- CropX

第七章市场机会与未来趋势

The Agricultural Sensor Market size is estimated at USD 2.01 billion in 2024, and is expected to reach USD 3.46 billion by 2029, growing at a CAGR of 11.5% during the forecast period (2024-2029).

Key Highlights

- Increasing demand for agricultural production, changing technology practices, and increasing intensification, including precision agriculture, low-till management, and advanced technology, are a few factors driving the agricultural sensors market.

- Agricultural sensors are expected to achieve complete expansion in the region. Location sensors have gained immense traction in recent years for the need for precise positioning in precision agriculture. In China, a large-scale agriculture digital zone was established in the Heilongjiang Modern Agriculture Demonstration Zone in 2018 under the motto 'Sky, Earth, and Space,' where "Sky" stood for satellite remote sensing data, "Space" for drone remote sensing data, and "Ground" for ground IoT data.

- Many agritech companies developed innovative models for easing farming practices by focusing more on wireless platforms to enable real-time decision-making regarding yield monitoring, crop health monitoring, field mapping, irrigation scheduling, harvesting management, etc., for helping the farmers from adverse price fluctuations of their produce.

- North America remains the largest geographical segment of the market and accounts for a major market share. High investments and wide adoption of smart farming techniques show huge potential growth for sensor farming during the forecast period. Stringent environmental regulations and the rising adoption of precision farming and yield monitoring practices by large and small farm owners to upsurge the productivity of fields are expected to drive the market.

Agricultural Sensor Market Trends

Decreased Number of Labor Requirements

Precision and indoor farming techniques demand new techniques to address the challenges of fluctuating climatic conditions and decreased skilled labor force. The farmer can control light amounts, nutrition levels, and moisture levels when they are growing crops solely indoors. Sensors with small-scale control systems with robust functionality would allow businesses to automate their systems and increase yields in a better way. The post-adoption of sensors may reduce the labor force by around 20.0%. Agricultural sensors can address the labor challenge in indoor farms.

Big industrial indoor farms use sensors that can sense water contamination, pesticide residues, nutrient shortages, disease attacks, etc. The combination of indoor farming and agricultural sensors will likely enhance crops' production capacities, which may drive the agricultural sensors market in the future.

As such, high-technology irrigation tools, such as soil moisture sensors, can help farmers determine the level of water requirement in each area. Smart irrigation applications in IoT-enabled devices can help control and monitor the irrigation equipment to adjust it based on changing requirements. Both represent a wide scope for undertaking precision irrigation in regions with depleted groundwater levels. These factors are likely to drive the market during the forecast period.

North America Dominates the Market

North America is the largest regional market for agricultural sensors. Strong government support to increase agricultural production, availability of infrastructure support, and acceptance of smart and precession farming methods increased the deployment of advanced farming solutions. In North America, the adoption of soil moisture sensors has rapidly increased. Soil moisture instruments are used in the sports turf segment for more efficient monitoring and conversion of turfgrass. Studies indicate that adopting sensors helps farmers minimize drought stress and reduces maintenance and labor costs of protected cultivation by at least 20%.

The United States is the early adopter of precision farming technologies, the primary factor responsible for the region's most significant share in the global market. The US agricultural sector has undergone a groundbreaking revolution regarding adopting smart farming practices in recent years. Although the advent of sensor-based technologies, such as Internet of Things (IoT) cellular devices, gear tooth sensor-based irrigation and fertilization equipment, and valve position sensors, is relatively new in the domain, the country has been witnessing a new-found demand for sensors, primarily due to the increased rate of mechanization and smart agricultural practices adopted by the farmers. A considerable acceptance of modern agriculture methods by Canada is contributing to industry growth.

Agricultural Sensor Industry Overview

The agricultural sensor market is fragmented, with various small and medium-sized companies and a few big players operating in the market, resulting in stiff competition. Some of the major players in the market include Edyan, Acclima Inc., CropX inc., Pycno, and Acquity Agriculture. The development of regional markets and local players in different parts of the world is the major factor for the fragmented nature of the market. North America and Asia-Pacific are the two regions showing maximum competitor activities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of Substitute Products

- 4.4.4 Threat of New Entrants

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Humidity Sensor

- 5.1.2 Electrochemical Sensor

- 5.1.3 Mechanical Sensor

- 5.1.4 Airflow Sensor

- 5.1.5 Optical Sensor

- 5.1.6 Pressure Sensor

- 5.1.7 Water Sensor

- 5.1.8 Soil Sensor

- 5.1.9 Livestock Sensor

- 5.1.10 Other Types

- 5.2 Application

- 5.2.1 Dairy Management

- 5.2.2 Soil Management

- 5.2.3 Climate Management

- 5.2.4 Water Management

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Thailand

- 5.3.3.4 Japan

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Libelium Comunicaciones Distribuidas Sl

- 6.3.2 Auroras

- 6.3.3 Acquity Agriculture

- 6.3.4 Pycno

- 6.3.5 Agsmarts Inc.

- 6.3.6 Edyn

- 6.3.7 Acclima Inc.

- 6.3.8 Caipos GmbH

- 6.3.9 Vegetronix Inc.

- 6.3.10 Sentek Ltd

- 6.3.11 Aquaspy Inc.

- 6.3.12 CropX

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

农业感测器市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

农业感测器市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 2032 年农业感测器市场预测:按感测器类型、连接性、电源、农场规模、应用和地区进行的全球分析

2032 年农业感测器市场预测:按感测器类型、连接性、电源、农场规模、应用和地区进行的全球分析 作物扫描器市场按技术、平台类型、应用、交付方式和最终用户划分-2025-2032年全球预测农业感测器市场按产品、感测器类型、连接类型、应用、最终用户和部署模式划分 - 全球预测,2025-2032

作物扫描器市场按技术、平台类型、应用、交付方式和最终用户划分-2025-2032年全球预测农业感测器市场按产品、感测器类型、连接类型、应用、最终用户和部署模式划分 - 全球预测,2025-2032 2025年全球农业感测器市场报告2032 年农业感测器市场预测:按类型、农场类型、应用、最终用户和地区进行的全球分析

2025年全球农业感测器市场报告2032 年农业感测器市场预测:按类型、农场类型、应用、最终用户和地区进行的全球分析 全球农业感测器市场

全球农业感测器市场 农业感测器市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年农场感测设备的全球市场到 2030 年农业感测器市场预测:按类型、连接性、应用和区域分類的全球分析

农业感测器市场规模、份额、趋势分析报告:按类型、应用、地区、细分市场预测,2025-2030 年农场感测设备的全球市场到 2030 年农业感测器市场预测:按类型、连接性、应用和区域分類的全球分析