|

市场调查报告书

商品编码

1687746

硅光电:市场占有率分析、产业趋势与统计数据、成长预测(2025-2030 年)Silicon Photonics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

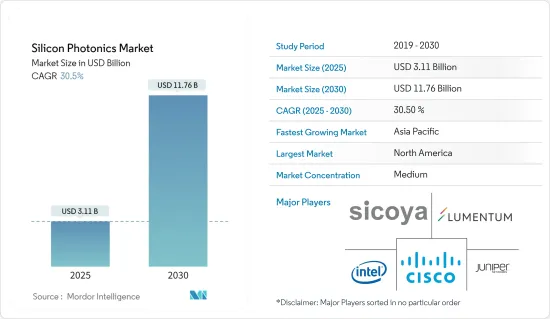

预计 2025 年硅光电市场规模为 31.1 亿美元,到 2030 年将达到 117.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 30.5%。

硅光电是一种新兴技术,利用光线在电脑晶片内部传输资料。硅光电是一种旨在取代铜线的技术,可提供更高的频宽、更长的传输距离和更好的能源效率。

关键亮点

- 网路流量的快速成长是硅光电市场的主要驱动力之一。随着对高速资料传输的需求不断增加,资料中心和电信业者正在寻找更有效率、更经济的解决方案来处理不断增长的网路流量。硅光电技术为这项挑战提供了有利的解决方案,与传统的铜基系统相比,它能够实现更快、更可靠、更具成本效益的资料传输。

- 这有助于利用现有网路基础设施提供高速宽频连线和许多宽频服务。此外,随着网路用户逐年增加,用于提高平均下行和上行速度以提供服务的投资也在增加。根据GSMA预测,5G全球市场渗透率将从2024年的22%成长至2030年的64%。

- 此外,各国正采取各种倡议,加速部署5G和6G通讯。例如,2022年8月,国防部推出了三个新的「超越5G创新计画」计划,其中包括创建6G技术研发中心。通讯领域的这种加强可能会推动市场成长。

- 热效应的风险是市场成长面临的一大挑战。当硅吸收光时就会产生热效应,导致机器温度升高。温度升高可能会导致设备性能下降甚至故障。

硅光电市场趋势

汽车产业将强劲成长

- 硅光电是汽车领域的新兴技术,它将有助于发展基于事件的感测器 (EBS) 和神经型态相机等感测器,并改进雷射雷达。正在利用硅光电技术升级的汽车产品包括ADAS(高级驾驶辅助系统)、脸部辨识系统、感测器和侦测技术、雷射雷达系统以及许多其他汽车使用的系统。硅光电系统正在提高汽车的安全性、功能性和性能。此外,巡航控制系统中的硅光电具有多种优势,包括提高准确性、速度和效率。

- 近年来,光电彻底改变了汽车产业,超越了简单的照明功能,提供了成像、感测、智慧显示、媒体通讯网路等领域的最尖端科技。因此,光电正在向新的维度发展,远远超出汽车照明、汽车製造和品管的范畴。毫不奇怪,汽车产业对硅光电等基于创新光电学的技术表现出越来越大的兴趣。

- 公车产量的上升可能为市场成长提供丰厚的机会。例如,根据 OICA 的数据,2022 年印度的公车和客车产量将达到约 75,000 辆,高于 2021 年的 34,700 辆。此外,根据国际能源总署(IEA)的预测,2016年至2022年期间,中国一直是註册电动公车最多的国家。 2021年和2022年,中国註册电动公车的数量将分别达到5万辆和5.4万辆。

- 自动驾驶和自动驾驶汽车的日益普及是 ADAS 市场的主要成长要素。例如,根据国家安全委员会的数据,到2026年,大约71%的註册车辆将配备后视摄影机,60%的註册车辆将配备后停车感应器。预计 ADAS 采用率的提高将推动市场的成长。各类个人和商用车辆製造商正在全球建立工厂,这也推动了市场的发展。

北美占据主要市场占有率

- 美国是资料中心市场突出的国家之一。由于该国主要参与者的扩张努力,该国的多租户资料中心租赁活动正在增加。

- 资料中心流量的增加,以及人工智慧和物联网等新兴领域的技术快速进步,导致全国资料流量的增加。根据思科预测,到 2023 年,连网装置的数量将从 2018 年的 27 亿增加到 46 亿。此外,预计到 2023 年,智慧型手机将占所有连网装置的 7%。

- 大大小小的企业的数位化以及相关的数位服务正在迅速增加对更大的技术堆迭来储存、计算、连接和分析资料的需求。这也导致了云端服务的采用。企业采用数位化将为该地区的硅光电市场创造新的机会。

- 预计加拿大无线通讯业者将在 2020 年至 2026 年期间投资约 258 亿美元用于 5G 基础设施部署。这些措施将扩大该国 5G 基础设施的覆盖范围,为市场研究供应商创造重大机会。

- 据爱立信称,400 万加拿大智慧型手机用户计划在未来 12 至 15 个月内升级到 5G,而十分之八的现有 5G 用户表示他们不想回到 4G。过去两年,5G用户成长了六倍。然而,消费者的认知度较低,15% 的用户声称在加拿大拥有 5G 网络,但使用的是 4G 设备,另有 18% 的用户拥有 5G 设备,但未升级到 5G 合约。

- 在终端用户产业技术进步的推动下,加拿大地区预计也将显着采用硅光电技术。此外,预计活性化研发活动和技术投资将成为增加招募的主要动力。

硅光电市场概况

硅光电市场高度分散,主要参与者包括 Sicoya GMBH、英特尔公司、思科系统公司、Lumentum Operations LLC(Lumentum Holdings Inc.)和瞻博网路公司。这些公司正在透过伙伴关係和收购来加强其产品供应并获得可持续的竞争优势。

- 2023年10月,Lumentum Holdings Inc.在苏格兰格拉斯哥举行的2023年欧洲光通讯会议上展示了其最新解决方案并共用了其行业观点。此外,Lumentum 也展示了其高功率1310 nm分布回馈回馈雷射 (DFB),在 25°C 时光纤输出光功率超过 400 mW。据称,这些新型超高高功率13xx 雷射器采用共封装光学元件、外部雷射光源解决方案和硅光电收发器,为下一代资料中心的 AI 和 ML 应用提供宽频化。

- 2023 年 9 月,博通宣布将与台积电和英伟达合作开发硅光电和共封装光学元件 (CPO)。台积电目前已组建了一支超过200人的研发团队,瞄准利用硅光电技术研发高速运算晶片的新机会,并计画最早于2024年下半年开始生产。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 购买者和消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 和其他宏观经济因素对市场的影响

第五章市场动态

- 市场驱动因素

- 透过使用基于硅光电的收发器来降低功耗

- 资料中心之间对高速连线和高资料传输容量的需求日益增加

- 市场限制

- 热效应风险

第六章市场区隔

- 按应用

- 资料中心和高效能运算

- 通讯

- 车

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 其他的

第七章竞争格局

- 供应商市场占有率

- 公司简介

- Sicoya GMBH

- Intel Corporation

- Cisco Systems Inc.

- Lumentum Operations LLC(Lumentum Holdings Inc.)

- Juniper Networks Inc.

- Global Foundries Inc.

- Broadcom Limited

- Molex Inc.(Koch Industries)

- Marvell Technology Inc.

- Macom Technology

- Coherent Corporation

- Hamamatsu Photonics KK

第八章投资分析

第九章:未来市场展望

The Silicon Photonics Market size is estimated at USD 3.11 billion in 2025, and is expected to reach USD 11.76 billion by 2030, at a CAGR of 30.5% during the forecast period (2025-2030).

Silicon photonics is a growing technology that utilizes optical rays to transfer data within computer chips. It is a favorable technology to replace copper wires, providing greater bandwidth, longer transmission distance, and better energy efficiency.

Key Highlights

- The rapidly growing internet traffic is one of the significant drivers of the silicon photonics market. With increasing demand for high-speed data transfer, data centers and telecommunications companies are seeking more efficient and cost-effective solutions to handle the growing volume of Internet traffic. Silicon photonics technology offers a favorable solution to this challenge, providing faster, more reliable, and more cost-effective data transfer than traditional copper-based systems.

- This helps provide high-speed broadband connections and many broadband services over the existing network infrastructure. Additionally, a growing number of Internet users over the years also resulted in rising investments to develop average downlink and uplink speeds to provide services. According to GSMA, 5G is projected to increase from a global market penetration of 22% in 2024 to 64% in 2030.

- In addition, countries are taking various initiatives to boost the deployment of 5G and 6G communication. For instance, in August 2022, the Department of Defense launched three new Innovative Beyond 5G Program projects, including creating an R&D hub for 6G technology. Such enhancement in the telecommunication sector may propel the market's growth.

- The risk of thermal effect significantly challenges the market's growth. The thermal effect occurs due to the absorption of light by silicon, which can increase the temperature in the machine. This increase in temperature can lead to a reduction in performance or even device failure.

Silicon Photonics Market Trends

Automotive Segment to Witness Major Growth

- Silicon photonics is an emerging technology in the automotive sector that helps advance sensors like event-based sensors (EBS) and neuromorphic cameras and improves LIDAR. Some automotive products being upgraded to incorporate silicon photonics technology include Advanced Driver Assistance Systems (ADAS), face recognition systems, sensors & detection technology, LiDAR systems, and many other systems used in vehicles. Silicon photonics-enabled systems enhance a vehicle's safety, functionality, and performance. Moreover, silicon photonics-enabled systems in cruise control offer several benefits, such as enhanced accuracy, speed, and efficiency.

- In recent years, photonics has revolutionized the automotive industry, transitioning from mere lighting functions to providing cutting-edge technology for imaging, sensing, smart displaying, and media communication networks. Consequently, photonics has taken on new dimensions far beyond lighting in cars and automotive manufacturing and quality control. Unsurprisingly, the automotive industry is showing an increased interest in innovative, photonics-based technologies such as silicon photonics.

- The increasing production of buses is likely to offer lucrative opportunities for market growth. For instance, according to OICA, around 75 thousand buses and coaches were produced across India in 2022, an increase from 34.7 thousand buses and coaches in 2021. Furthermore, according to the International Energy Agency (IEA), between 2016 and 2022, China consistently registered the most significant number of electric buses. In 2021 and 2022, the number of electric bus registrations in China amounted to 50 and 54 thousand, respectively.

- The increasing adoption of self-driving or autonomous vehicles is a primary growth factor for the ADAS market. For instance, according to the National Safety Council, by 2026, approximately 71% of registered vehicles will be equipped with rear cameras, while 60% will have rear parking sensors. Such increasing adoption of ADAS would aid the growth of the market studied. Various manufacturers of personal and commercial vehicles are establishing their facilities globally, which is also driving the market studied.

North America Holds Significant Market Share

- The United States is one of the prominent countries in the data center market. Multi-tenant data center leasing activities in the country have been rising owing to expansion activities by some of the major companies in the country.

- The growing data center traffic, along with rapid technological advancements in emerging areas, such as AI and IoT, is leading to increased data traffic across the country. According to the forecasts by Cisco, there will be 4.6 billion networked devices by 2023, rising from 2.7 billion in 2018. In addition, smartphones are expected to account for 7% of all networked devices by 2023.

- The digitization of enterprises, be they small or large, and the resulting digital services rapidly develop a need for larger technology stacks in order to store, compute, connect, and analyze data. It also leads to the adoption of cloud services. The adoption of digitization of enterprises creates new opportunities for the silicon photonics market in the region.

- It is expected that wireless operators in Canada will invest approximately USD 25.8 billion in deploying 5G infrastructure between 2020 and 2026; as a result, the government is also encouraging telecom equipment manufacturing. These initiatives will broaden the scope of the country's 5G infrastructure and provide a massive opportunity for market study vendors.

- As per Ericsson, in Canada, 4 million smartphone users plan to upgrade to 5G over the next 12-15 months; 8 in 10 current 5G users don't want to return to 4G. The 5G user base has increased six-fold over the past two years. However, consumer awareness is low; 15% of users claim they are on 5G but use a 4G handset in Canada, while another 18% own a 5G capable device but have not upgraded to a 5G subscription.

- The Canadian region is also expected to exhibit a significant adoption rate of silicon photonics technology due to technological advancements across its end-user industries. Also, the increasing research and development activities, coupled with several investments in technology, are expected to act as major drivers for the growth in adoption.

Silicon Photonics Market Overview

The silicon photonics market is highly fragmented, with major players like Sicoya GMBH, Intel Corporation, Cisco Systems Inc., Lumentum Operations LLC (Lumentum Holdings Inc.), and Juniper Networks Inc. They are adopting partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In October 2023, Lumentum Holdings Inc. showcased its latest solutions and shared industry perspectives at the European Conference on Optical Communication 2023 in Glasgow, Scotland. Lumentum's ultra-high power, 1310 nm distributed-feedback laser (DFB) was also demonstrated at over 400 mW optical power ex-fiber at 25°C. These new ultra-high power 13xx lasers were claimed to enable higher bandwidth for AI and ML applications by using co-packaged optics, external laser source solutions, and silicon photonics transceivers for the next generation of data centers.

- In September 2023, Broadcom announced that it is working with TSMC and Nvidia to develop silicon photonics and co-packaged optics (CPO). TSMC has already formed an R&D team of over 200 employees to target emerging opportunities in high-speed computing chips based on silicon photonics technology, with production expected to start as early as the second half of 2024.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyer/consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products and Services

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Reduction in Power Consumption With the Use of Silicon Photonics Based Transceivers

- 5.1.2 Growing Need for High-Speed Connectivity and High Data Transfer Capabilities Across Data Centers

- 5.2 Market Restraints

- 5.2.1 Risk of Thermal Effect

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Data Centers and High-performance Computing

- 6.1.2 Telecommunications

- 6.1.3 Automotive

- 6.1.4 Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Vendor Market Share

- 7.2 Company Profiles

- 7.2.1 Sicoya GMBH

- 7.2.2 Intel Corporation

- 7.2.3 Cisco Systems Inc.

- 7.2.4 Lumentum Operations LLC (Lumentum Holdings Inc.)

- 7.2.5 Juniper Networks Inc.

- 7.2.6 Global Foundries Inc.

- 7.2.7 Broadcom Limited

- 7.2.8 Molex Inc. (Koch Industries)

- 7.2.9 Marvell Technology Inc.

- 7.2.10 Macom Technology

- 7.2.11 Coherent Corporation

- 7.2.12 Hamamatsu Photonics KK

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

2025年硅光电全球市场报告

2025年硅光电全球市场报告 硅光电市场:全球组件、产品、最终用户和地区—2030 年预测

硅光电市场:全球组件、产品、最终用户和地区—2030 年预测 硅光电市场规模、份额、按组件、产品、最终用户和地区分類的成长分析 - 2025-2032 年产业预测

硅光电市场规模、份额、按组件、产品、最终用户和地区分類的成长分析 - 2025-2032 年产业预测 硅光电市场分析及2034年预测:类型、产品、技术、组件、应用、材料类型、设备、流程、最终用户

硅光电市场分析及2034年预测:类型、产品、技术、组件、应用、材料类型、设备、流程、最终用户 硅光电市场(依产品类型、组件、波导管和最终用途)-2025-2030 年全球预测

硅光电市场(依产品类型、组件、波导管和最终用途)-2025-2030 年全球预测 硅光子学·光积体电路的全球市场(2025年~2035年)

硅光子学·光积体电路的全球市场(2025年~2035年) 硅光子市场:全球产业分析、市场规模、占有率、成长、趋势与未来预测(2025-2032)

硅光子市场:全球产业分析、市场规模、占有率、成长、趋势与未来预测(2025-2032) 硅光子市场 - 全球产业分析、规模、占有率、成长、趋势及 2032 年预测

硅光子市场 - 全球产业分析、规模、占有率、成长、趋势及 2032 年预测 2025-2033 年硅光子市场报告(按产品、组件(光波导、光调製器、光电探测器、波分复用滤波器、雷射)、应用和地区划分)

2025-2033 年硅光子市场报告(按产品、组件(光波导、光调製器、光电探测器、波分复用滤波器、雷射)、应用和地区划分) 硅光子学IC实验机的全球市场:2030年为止的预测

硅光子学IC实验机的全球市场:2030年为止的预测