|

市场调查报告书

商品编码

1689954

阿尔法甲基苯乙烯:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Alpha Methylstyrene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

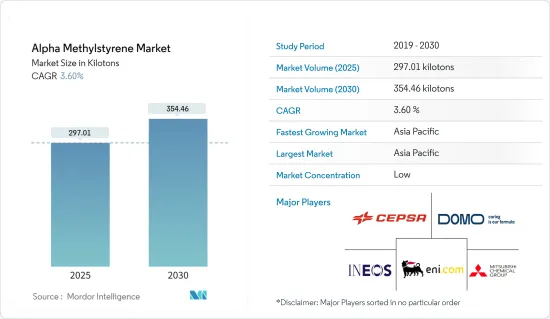

预计 2025 年 α 甲基苯乙烯市场规模为 297.01 千吨,到 2030 年将达到 354.46 千吨,预测期内(2025-2030 年)的复合年增长率为 3.6%。

由于所有行业都停止了生产流程,COVID-19 对市场产生了负面影响。封锁、社交距离和贸易制裁已导致全球供应链网路严重中断。不过,预计这种情况将在 2021 年恢復,有利于预测期内的市场。

主要亮点

- 从中期来看,ABS 树脂製造需求的增加以及电子产业对 α 甲基苯乙烯的需求上升是推动市场发展的关键因素。

- 另一方面,生产α-甲基苯乙烯过程中排放的危险废弃物可能会抑制市场的成长。

- 对耐用蜡和耐热黏合剂的需求不断增加,这可能会在未来几年为市场带来好处。

- 亚太地区贡献了最高的市场占有率,并可能在预测期内占据市场主导地位。

阿尔法甲基苯乙烯市场趋势

汽车产业占市场主导地位

- 甲基苯乙烯是生产 ABS 树脂的中间体。此外,ABS 塑胶在汽车工业中用作金属替代品。为了实现轻量化,ABS树脂被用于汽车的各种零件。 ABS 常用于仪表板组件、座椅靠背、安全带组件、方向盘、车门滑轨、柱饰板和仪錶面板等零件。

- 根据国际汽车製造商协会(OICA)预测,2022年全球汽车产量将达到8,501万辆,而2021年为8,020万辆,成长率为6%。

- 此外,电动车产量的增加可能会增加市场对市场研究的需求。例如,根据 EV Volumes 的数据,2022 年将交付总合1,050 万辆新的 BEV 和 PHEV,比 2021 年成长 55%。

- 亚太地区是全球最有价值汽车製造商的所在地。中国、印度、日本和韩国等新兴经济体努力加强製造业基础,建立高效率的供应链以提高盈利。

- 中国是全球最大的汽车生产基地,根据中国工业协会的数据,预计2022年汽车总产量将从去年的2,610万辆增加3.4%至2,720万辆。

- 德国是欧洲主要汽车製造国之一。根据德国工业协会(VDA)统计,2022年7月德国汽车产量为263,400辆,较2021年同期成长7%。此外,德国对电动车的需求也在成长。因此,各公司都在该国增加电动车的产量。例如,2023年6月,福特宣布在德国科隆开设电动车中心,这是一座高科技生产工厂。

- OICA 表示,在北美,2022 年的汽车产量将达到 1,770 万辆,较 2021 年的约 1,610 万辆增长 10%。

- 因此,预计预测期内对 α 甲基苯乙烯的需求将随着汽车产量的扩大而成长。

亚太地区主导 Alpha 甲基苯乙烯市场

- 亚太地区在全球α-甲基苯乙烯市场中占有突出份额,预计在预测期内将继续占据市场主导地位。

- 国家统计局发布的资料显示,中国轮胎产业取得了显着成长,反映出国内和国际市场对轮胎的需求不断增加。

- 根据中国国家统计局的数据,截至2023年5月,中国塑胶製品月产量约600万吨。自2020年1月以来,塑胶製品月产量最高的是2021年12月,为795万吨。

- 此外,中国是化学加工中心,占世界化学产品的很大一部分。在中国这个全球最大的化学品市场,预计2023年化学品产量成长将略有放缓。继俄乌战争之后,全球供应链已经因能源和原料成本上升、疫情、经济不确定性和政治动盪而紧张,而2022年化学工业又遭遇了进一步的瓶颈。根据BASF《化工产业展望》,预计2023年中国化学品产量将小幅下降5.9%。不过,新建化工厂的投资正在增加,这将在中期内支撑对AMS的需求。

- 印度是亚太地区继中国之后最大的橡胶生产国和消费国之一。在印度,65%以上的橡胶产量用于製造汽车轮胎(50%)和自行车轮胎和内胎(15%)。此外,该国拥有近 66 家轮胎生产厂和约 41 家轮胎製造公司。

- 据IBEF称,2022年4月至9月塑胶出口总额为63.8亿美元。在此期间,塑胶原料、医疗製品、管线及配件出口分别比去年同期成长32.3%、24.8%和17.9%。

- 因此,预计预测期内各行业需求的增加将推动该地区研究市场的发展。

Alpha 甲基苯乙烯产业概况

甲基苯乙烯市场比较分散。市场的主要企业包括 ENI SpA、INEOS、Cepsa、三菱化学和 Domo Chemicals。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- ABS 树脂製造需求增加

- 电子业对 α-甲基苯乙烯的需求不断增加

- 限制因素

- α-甲基苯乙烯生产过程中的危险废弃物排放

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场区隔

- 应用

- ABS 製造

- 塑胶添加剂和中间体

- 胶水

- 被覆剂

- 其他用途

- 最终用户产业

- 胎

- 车

- 电子产品

- 塑胶

- 其他最终用户产业

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 世界其他地区

- 南美洲

- 中东和非洲

- 亚太地区

第六章 竞争格局

- 併购、合资、合作、协议

- 市场占有率(%)/排名分析

- 主要企业策略

- 公司简介

- AdvanSix

- Altivia

- Cepsa

- Chang Chun Group

- Deepak

- Domo Chemicals

- Eni SPA

- INEOS

- Kraton Corporation

- Kumho P&B Chemicals.,inc.

- Mitsubishi Chemical Corporation

- Prasol Chemicals Limited

- Rosneft

- Seqens

- SI Group, Inc.

- Solvay

- Yangzhou Lida Chemical Co., Ltd.

第七章 市场机会与未来趋势

- 对耐用蜡和耐热黏合剂的需求不断增加

- 其他机会

The Alpha Methylstyrene Market size is estimated at 297.01 kilotons in 2025, and is expected to reach 354.46 kilotons by 2030, at a CAGR of 3.6% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the condition is recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

- In the medium term, the major factors driving the market studied are the increasing demand for the manufacturing of ABS resins and increasing demand for alpha-methyl styrene in the electronics segment.

- On the flip side, hazardous waste release during the production of alpha methyl styrene is likely to restrain the market growth.

- Increase in demand for durable waxes and heat-resistant adhesives is likely to act as an opportunity for the market in coming years.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Alpha Methylstyrene Market Trends

Automotive Industry to Dominate the Market

- Alpha methyl styrene is an intermediate for the production of ABS resin. Further, ABS resin is used as a replacement for metal in the automotive industry. Various automotive parts that look for weight reduction factors use ABS thermoplastic. ABS is commonly used for parts that include dashboard components, seat backs, seat belt components, handles, door loners, pillar trim, and instrument panels.

- According to the Organization Internationale des Constructeurs d'Automobiles (OICA), global automotive vehicle production reached 85.01 million in 2022, with a growth rate of 6% as compared to 80.20 million vehicles manufactured in 2021, thereby indicating an increased demand for alpha methyl styrene from the automotive industry.

- Furthermore, the rising production of electric vehicles is likely to enhance the market demand for the market-studied. For instance, according to the EV Volumes, a total of 10.5 million new BEVs and PHEVs were delivered during 2022, an increase of 55 % compared to 2021.

- Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27.2 million units in 2022, registering an increase of 3.4 % compared to 26.1 million units produced last year.

- In Europe, Germany is among the vital manufacturer of vehicles. According to the German Association of the Automotive Industry (VDA), Germany produced 263,400 units of cars in July 2022, registering a growth rate of 7% compared to the same period in 2021. Additionally, the demand for electric cars is increasing in Germany. Thus, various companies are increasing the production volume of electric cars in the country. For instance, in June 2023, Ford announced the inauguration of the Cologne Electric Vehicle Center, a hi-tech production facility in Germany.

- In North America, according to the OICA, automotive production in 2022 accounted for 17.7 million units, an increase of 10% compared to that in 2021, which was around 16.1 million units.

- Therefore, the demand for alpha methyl styrene is expected to grow with the expanding automotive production during the forecast period.

Asia-Pacific to Dominate Alpha Methyl Styrene Market

- Asia-Pacific holds a prominent share in the alpha-methylstyrene market globally and is expected to dominate the market during the period of forecast.

- As per the data released by the National Bureau of Statistics, China's tire industry is experiencing substantial growth, reflecting the increasing demand for tires in the domestic as well as international markets.

- According to the National Bureau of Statistics of China, as of May 2023, China produces roughly 6 million metric tons of plastic products monthly. Since January 2020, the highest monthly output of plastic products was recorded in December 2021, at 7.95 million metric tons.

- Furthermore, China is a hub for chemical processing, accounting for a major chunk of global chemicals. In China, the world's largest chemicals market, a slight slowdown in chemical production growth is expected in 2023. Following Russia and Ukraine war, the chemical industry experienced a year marked by further bottlenecks in global supply chains already strained by rising energy and raw material costs, pandemic, economic uncertainty, and political turmoil in 2022. Continuing on the tumultuous grounds, China is expected to register a slightly weaker growth of 5.9% in chemical production in 2023, as per the BASF's chemical industry outlook. However, the increasing investments in the construction of new chemical plants support the demand for AMS in the mid-term.

- India is one of the largest producers and consumers of rubber after China in the Asia-Pacific region. In India, over 65% of the rubber produced is used for manufacturing automotive (50%) and bicycle tires and tubes (15%). Moreover, the country has almost 66 tire-producing plants and about 41 tire-producing companies.

- According to IBEF, total plastics exports between April-September 2022 stood at USD 6.38 billion. During this period, the exports of plastic raw materials, medical items, and pipes and fittings increased by 32.3%, 24.8%, and 17.9% over the same time last year.

- Thus, rising demand from various industries is expected to drive the market studied in the region during the forecast period.

Alpha Methylstyrene Industry Overview

The alpha methyl styrene market is fragmented in nature. Some of the major companies in the market include ENI S.p.A., INEOS, Cepsa, Mitsubishi Chemical Corporation, and Domo Chemicals, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand For the Manufacturing of ABS Resins

- 4.1.2 Increasing Demand For Alpha-methyl Styrene In the Electronics Segment

- 4.2 Restraints

- 4.2.1 Hazardous Waste Release During the Production of Alpha Methyl Styrene

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume and Value)

- 5.1 Application

- 5.1.1 ABS Manufacture

- 5.1.2 Plastic Additives and Intermediates

- 5.1.3 Adhesives

- 5.1.4 Coatings

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Tire

- 5.2.2 Automotive

- 5.2.3 Electronics

- 5.2.4 Plastics

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AdvanSix

- 6.4.2 Altivia

- 6.4.3 Cepsa

- 6.4.4 Chang Chun Group

- 6.4.5 Deepak

- 6.4.6 Domo Chemicals

- 6.4.7 Eni S.P.A.

- 6.4.8 INEOS

- 6.4.9 Kraton Corporation

- 6.4.10 Kumho P&B Chemicals.,inc.

- 6.4.11 Mitsubishi Chemical Corporation

- 6.4.12 Prasol Chemicals Limited

- 6.4.13 Rosneft

- 6.4.14 Seqens

- 6.4.15 SI Group, Inc.

- 6.4.16 Solvay

- 6.4.17 Yangzhou Lida Chemical Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Demand for Durable Waxes and Heat-resistant Adhesives

- 7.2 Other Opportunities

全球α-甲基苯乙烯市场规模、份额、趋势和成长分析报告(2026-2034年)

全球α-甲基苯乙烯市场规模、份额、趋势和成长分析报告(2026-2034年) α-甲基苯乙烯二聚体市场按等级、形态、应用和最终用途产业划分,全球预测(2026-2032年)

α-甲基苯乙烯二聚体市场按等级、形态、应用和最终用途产业划分,全球预测(2026-2032年) α-甲基苯乙烯市场规模、份额和成长分析(按纯度、应用和地区划分):产业预测(2026-2033 年)全球 2025-2032 年 α-甲基苯乙烯市场预测(按类型、应用、最终用途、等级和分销管道)2026-2032 年 α-甲基苯乙烯市场(依纯度、最终用途产业及地区划分)

α-甲基苯乙烯市场规模、份额和成长分析(按纯度、应用和地区划分):产业预测(2026-2033 年)全球 2025-2032 年 α-甲基苯乙烯市场预测(按类型、应用、最终用途、等级和分销管道)2026-2032 年 α-甲基苯乙烯市场(依纯度、最终用途产业及地区划分) 世界及美国的Alpha甲基苯乙烯(AMS)市场:预测(2024年~2030年)

世界及美国的Alpha甲基苯乙烯(AMS)市场:预测(2024年~2030年) α-甲基苯乙烯全球市场 2024-2028

α-甲基苯乙烯全球市场 2024-2028 全球α-甲基苯乙烯市场2024-2031

全球α-甲基苯乙烯市场2024-2031 2030 年 α-甲基苯乙烯市场预测:按纯度、应用、最终用户和地区进行的全球分析

2030 年 α-甲基苯乙烯市场预测:按纯度、应用、最终用户和地区进行的全球分析 阿尔法甲基苯乙烯全球市场规模、份额和趋势分析报告 - 按纯度、最终用途、地区、展望和预测,2024-2031 年

阿尔法甲基苯乙烯全球市场规模、份额和趋势分析报告 - 按纯度、最终用途、地区、展望和预测,2024-2031 年