|

市场调查报告书

商品编码

1443905

软性显示器:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Flexible Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

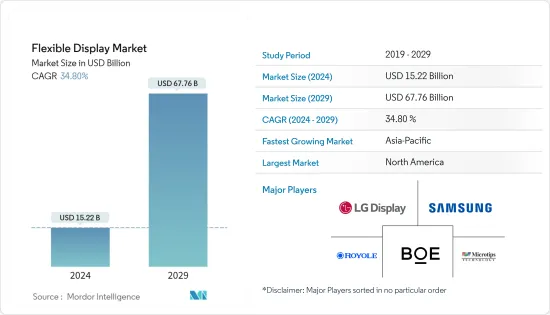

预计2024年软性显示器市场规模为152.2亿美元,预计2029年将达到677.6亿美元,预测期间(2024-2029年)复合年增长率为34.80%。

智慧型手机和穿戴式装置、连网型技术和其他智慧家庭产品的需求不断增长是推动软性显示器技术需求的主要因素。

主要亮点

- 与传统显示技术相比,软性显示器具有许多优势。轻质、可弯曲、超薄、防碎、不易破碎、方便携带、低能耗。虽然曲面显示器在视角和影像品质深度方面比平面显示器有了显着改进,但它们与柔性和可折迭显示器不同。

- 软性显示器最重要的优点是耐用性。由于萤幕可以弯曲和操纵,因此它比目前使用的固体玻璃结构更能吸收跌落和碰撞的衝击力。未来软性显示器的其他潜在应用包括整合到服装中,根据周围环境立即改变颜色或图案。这一潜力的实现预计将显着增加对软性显示器的需求。

- 智慧型手机市场正在推动全球对柔性萤幕的需求。因此,各个供应商都加大了对智慧型手机领域的关注。除此之外,该供应商还致力于增加其在电视和电脑(笔记型电脑和桌上型电脑萤幕)领域的影响力,并相应地创新其产品。例如,2021年1月,TCL华星在CES 2021上发表了两款创新产品:6.7吋AMOLED可捲动显示器和17吋印刷OLED捲动显示器。

- OLED 显示器类型由于其简单的设计、出色的影像品质和有限的弹性而最近变得流行。 OLED 萤幕不需要背光,可以做得很薄并模製成特定的形状。目前,OLED 显示器类型对于电视和电脑显示器等大萤幕来说价格昂贵。然而,该细分市场仍享有规模经济。

- 预计最初的市场需求将来自亚太地区、北美和欧洲消费电子产业的新兴国家,而柔性 OLED 显示器的采用将推动市场的发展。柔性OLED被认为是下一代智慧型手机市场的最佳解决方案之一,即使在需求较低的市场,这种显示技术也正在赢得市场份额。

- 然而,可用性初始阶段的成本和承受能力问题、复杂的製造流程、季节性需求模式和不确定的经济前景可能会阻碍预测期内的市场成长。

- 冠状病毒感染疾病(COVID-19)对市场产生了负面影响,特别是在大流行的早期阶段,因为各国实施的封锁措施扰乱了行动电话和显示器生产的供应链。然而,随着智慧型手机、笔记型电脑等产品的高需求带动消费性电子市场快速復苏,软性显示器市场预计在预测期内将进一步成长。

软性显示器市场趋势

软性显示器在智慧型手机和平板电脑的采用迅速成长

- 儘管软性显示器的采用仍处于早期阶段,但该技术因其具有许多优势而被视为智慧型手机行业的下一个重大事件。例如,您可以在观看影片内容时快速增加设备的尺寸,然后根据需要缩小尺寸以适合您的口袋。

- 此外,它还提高了设备的美观性和功能性。例如,软性显示器可以为客户在行动装置上提供更好的多工处理能力。对于智慧型手机来说,折迭式显示器可能会消除对平板电脑作为辅助设备的需求。显示器是智慧型手机的视觉输出表面,旨在承受弯曲、弯曲和扭曲。

- 各种研究人员正在努力提高软性显示器的可靠性和成本效率,从而促进新型显示器的开发。例如,2021年4月,TCL开发了一种折迭捲概念,利用折迭式铰链和从手机扩展到平板电脑的扩展机制,将6.87英寸行动电话变成10英寸平板电脑。该公司还展示了一款采用两个铰链的三折折迭式概念的智慧型手机设备(最大为 10 吋平板电脑)。这是一个独特的概念,针对完全不同的用户群。

- OLED 是一种新兴的显示技术,越来越多地应用于许多行动装置。 OLED 是显示器产业最新一代的技术,与老式 LED 和 LCD 相比,可提供卓越的性能和增强的光学特性。此外,三星、摩托罗拉和 LG 等智慧型手机製造商也越来越多地使用这些柔性 OLED 显示器。

- 随着智慧型手机用户的增加,预计该行业将为软性显示器提供商创造重大机会。例如,根据爱立信的数据,截至年终,智慧型手机用户约为63亿,约占所有行动电话用户的77%。到 2027 年,这一数字预计将达到 78 亿。

预计亚太地区将占据重要市场占有率

- 亚太地区正在成为软性显示器发展的领先地区,特别是在消费性电器产品产业。该地区国家,特别是东亚(中国、台湾、日本、韩国、新加坡)国家正在经历稳定成长,主要与软性显示器有关。

- 随着各行业的最终用户强调高品质显示器的重要性,亚太地区对 OLED 显示器的需求不断增加。材料技术的进步进一步促进了软性显示器和软性电子产品产品新应用的开发,预计这些应用将在预测期内占据市场需求和收益的重要份额。

- 区域市场受到市场参与者整合的推动,导致许多先进的显示技术主导市场。此外,亚洲国家是显示器製造晶圆代工厂的所在地,使该地区在市场上占据主导地位。

- 亚太软性显示器市场的新兴企业正在为其技术申请专利,这可能会加剧市场竞争。三星和 LG Display 等亚太地区领先的软性显示器製造商正在大力投资加强其生产设施,以推出新产品。

- 智慧型手錶等穿戴式装置的出现也有望为市场提供需求产生动力。据思科系统公司称,亚洲连网穿戴装置数量预计将从 2021 年的 2.582 亿台增至 2022 年的 3.11 亿台。预计此类趋势将支持预测期内的市场成长。

软性显示器行业概况

软性显示器市场适度分散,有许多地区和全球参与者。汽车应用中的柔性萤幕以及智慧型手机和电视的日益普及正在为软性显示器市场创造利润丰厚的机会。为了进一步加强其在市场上的影响力,供应商正在增加研发支出,以使他们的技术更加可靠和更具成本效益。该市场的主要企业包括 LG Display、三星电子和京东方科技集团有限公司。

- 2022年2月,京东方宣布开发出萤幕内支援的OLED柔性「N」形折迭式显示技术,可实现向内和向外折迭式。据该公司介绍,该显示器原型机采用了原始尺寸的 12.3 英寸柔性 AMOLED 显示屏,可向外折迭至 8.6 英寸尺寸,向内折迭至可携式5.6 英寸尺寸,具有性别差异。

- 2022年1月,软性显示器公司柔宇科技与领先的机器人公司CIOT达成策略伙伴关係。作为协议的一部分,CIOT将从柔宇科技采购感测器、软性显示器以及软硬体整合解决方案。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌意强度

- 替代产品的威胁

- 产业价值链分析

- 技术简介

- 新型冠状病毒感染疾病对市场生态系的影响

第五章市场动态

- 市场驱动因素

- 消费性电器产品创新

- 对更高影像品质的需求不断增长

- 市场限制因素

- 更高的研发成本和高度活跃的市场

- 市场机会

第六章市场区隔

- 按显示类型

- OLED

- 液晶

- EPD(电子纸显示器)

- 其他显示类型(LED)

- 按基板材质

- 玻璃

- 塑胶

- 其他基板

- 按用途

- 智慧型手机和平板电脑

- 智慧穿戴

- 电视数位电子看板系统

- 个人电脑和笔记型电脑

- 其他应用(车辆、大众交通工具、智慧家电)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区

第七章 竞争形势

- 公司简介

- LG Display Co. Ltd

- Samsung Electronics Co. Ltd

- ROYOLE Corporation

- e-ink Holdings

- BOE Technology Group Co. Ltd

- Guangzhou Oed Technologies Co. Ltd

- FlexEnable Technology Limited

- Chunghwa Picture Tubes Ltd

- Huawei Technologies Co. Ltd

- Sharp Corporation

- Plastic Logic

- Innolux Corporation

- AU Optronics Corp.

- TCL Electronics Holdings Limited

- Microtips Technology

第八章投资分析

第9章市场的未来

The Flexible Display Market size is estimated at USD 15.22 billion in 2024, and is expected to reach USD 67.76 billion by 2029, growing at a CAGR of 34.80% during the forecast period (2024-2029).

The growing demand for smartphones and wearable devices, and the increasing demand for connected technologies and other smart home products, are major factors driving the demand for flexible display technology.

Key Highlights

- Flexible displays offer various advantages over conventional display technologies. They are lightweight, bendable, ultra-thin, shatter-proof, unbreakable, portable, and have low energy consumption. Although curved displays offer notable improvements over flat displays regarding viewing angle and depth of picture quality, they differ from flexible and foldable ones.

- The most significant advantage of flexible displays is their durability. Since this screen can be bent and manipulated, it tends to absorb fall and collision impact better than solid glass structures currently in application. Other potential applications of flexible displays in the future include the integration in clothing that changes color or pattern instantly as per the surroundings. The realization of this potential is expected to boost the demand for flexible displays significantly.

- The smartphone market drives the global demand for flexible screens. As a result, various vendors are increasing their focus on the smartphone segment. Apart from this, vendors are also focusing on enhancing their presence in the TV and computer (Laptops and Desktop screens) segment and innovating their product offerings accordingly. For instance, in January 2021, TCL CSOT launched two innovative products, a 6.7-inch AMOLED Rollable Display and a 17-inch Printed OLED Scrolling Display, at CES 2021.

- OLED display type has recently gained popularity due to its simplified design, better image quality, and limited flexibility. OLED screens do not involve backlighting and can be thinned and molded into specific shapes. OLED display types are currently expensive for large screens, such as televisions and computer monitors. However, they still gain benefits for economies of scale in this segment.

- Initial market demand is expected from emerging economies in the consumer electronics segment of APAC, North America and Europe, thereby driving the market due to the adoption of flexible OLED displays. As the flexible OLED is considered one of the best solutions for the next-generation smartphone market, this display technology is gaining shares even in a market with lesser demand.

- However, higher cost and affordability issues in the initial stage of availability, complex manufacturing processes, seasonal demand patterns, and uncertain economic outlook might hinder the market growth during the forecast period.

- COVID-19 had a detrimental influence on the market, especially during the initial phase of the pandemic as lockdown measures imposed across various countries disrupted the supply chain for phone and display production. However, with the consumer electronics market recovering quickly, driven by high demand for products such as smartphones, laptops, and so on, the flexible display market is expected to grow further during the forecast period.

Flexible Display Market Trends

Adoption of Flexible Display to Grow Significantly in Smartphones and Tablets

- Although the adoption of flexible displays is still in the nascent stage, the technology is considered the next big thing for the smartphone industry, as the technology offers many benefits. For example, it lets the user quickly increase the size of the device when watching video content and makes it smaller to fit in their pocket when needed.

- Additionally, it also provides more aesthetics and functionality to the device. For instance, flexible displays can give customers better multitasking capabilities on mobile devices. In the case of smartphones, foldable displays can eliminate the need for a tablet as a secondary device in some cases. The display is a visual output surface designed to withstand being folded, bent, and twisted in smartphones.

- Various researchers have been working on making flexible displays reliable and cost-effective, leading to the development of new displays. For instance, in April 2021, TCL developed a Fold 'n' Roll concept that transforms a 6.87-inch phone into a 10-inch tablet, using a folding hinge and extendable mechanism to expand from phone to tablet. The company also showcased the Tri-Fold foldable concept smartphone device (up to 10-inch tablet) that relies on two hinges, which is a unique concept and targets an entirely different user group.

- OLED is an emerging display technology that is increasingly being used in many mobile devices. OLEDs are the latest generation technology in the display industry and provide superior performance and enhanced optical characteristics compared to older LEDs and LCDs. Furthermore, smartphone manufacturers like Samsung, Motorola, and LG are increasingly using these flexible OLED displays.

- With the number of smartphone users increasing, the industry is expected to create significant opportunities for flexible display providers. For instance, according to Ericsson, at the end of 2021, there were about 6.3 billion smartphone subscribers, accounting for about 77 % of all mobile phone subscriptions. This number is expected to reach 7.8 billion in 2027.

Asia-Pacific is Expected to Hold a Significant Market Share

- The Asia-Pacific is emerging as a leading region for developing flexible displays, particularly in the consumer electronics industry; countries in the region, particularly those in East Asia (China, Taiwan, Japan, South Korea, and Singapore), share a steady growth primarily related to flexible displays.

- OLED displays are witnessing increased demand in the Asia Pacific region as end-users across various industry verticals emphasize the importance of high-quality displays. Advancements in material technologies are further driving the development of new applications of flexible displays and flexible electronics, which are expected to account for a significant share of the market demand and revenues over and beyond the forecast period.

- The regional market is driven by the consolidation of market players, resulting in many advanced display technologies dominating the market. Moreover, Asian countries are the base for display manufacturing foundries, which positions this region in a dominating market position.

- Emerging players in the Asia-Pacific's flexible display market are filing patents for their technology, which is likely to increase the competition in the market. The leading flexible display manufacturers of the Asia-Pacific region, such as Samsung, LG Display, and others, are investing considerably in enhancing their production facilities to introduce new products.

- The emergence of wearables, such as smartwatches, and other devices, are also expected to provide the market with the impetus for demand generation. According to Cisco Systems, the number of connected wearable devices in Asia is expected to reach 311 million in 2022, from 258.2 million in 2021. Such trends are expected to support the market's growth during the forecast period.

Flexible Display Industry Overview

The Flexible Display Market is moderately fragmented, with many regional and global players. Flexible screens in automotive applications, and the growing adoption of smartphones and televisions, provide lucrative opportunities in the flexible display market. To further consolidate their market presence, the vendors are increasing their R&D expenses to make the technology more reliable and cost-effective. Some of the key players in the market are LG Display Co., Samsung Electronics Co. Ltd, and BOE Technology Group Co.

- In February 2022, BOE announced the development of OLED flexible 'N' shaped foldable display technology support in a screen that can achieve internal and external folding. According to the company, the display prototype is equipped with the original size of 12.3 inches of flexible AMOLED display, which after an exterior fold can become 8.6 inches size, and then after an internal folding can become a portable form of 5.6 inches.

- In January 2022, Royole Corporation, a flexible display firm, signed a strategic partnership with CIOT, a leading robotics company. As part of the agreement, CIOT will purchase sensors, flexible display screens, and software and hardware integration solutions from Royole Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Impact of COVID -19 on the Market Ecosystem

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Innovation in Consumer Electronics

- 5.1.2 Increase in Demand for Greater Picture Quality

- 5.2 Market Restraints

- 5.2.1 Higher R&D Cost and Highly Dynamic Market

- 5.3 Market Opportunities

6 MARKET SEGMENTATION

- 6.1 By Display Type

- 6.1.1 OLED

- 6.1.2 LCD

- 6.1.3 EPD (Electronic Paper Display)

- 6.1.4 Other Display Types (LED)

- 6.2 By Substrate Material

- 6.2.1 Glass

- 6.2.2 Plastic

- 6.2.3 Other Substrate Materials

- 6.3 By Application

- 6.3.1 Smartphones and Tablets

- 6.3.2 Smart Wearables

- 6.3.3 Televisions and Digital Signage Systems

- 6.3.4 Personal Computers and Laptops

- 6.3.5 Other Applications (Vehicle, Public Transport, and Smart Home Appliances)

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 LG Display Co. Ltd

- 7.1.2 Samsung Electronics Co. Ltd

- 7.1.3 ROYOLE Corporation

- 7.1.4 e-ink Holdings

- 7.1.5 BOE Technology Group Co. Ltd

- 7.1.6 Guangzhou Oed Technologies Co. Ltd

- 7.1.7 FlexEnable Technology Limited

- 7.1.8 Chunghwa Picture Tubes Ltd

- 7.1.9 Huawei Technologies Co. Ltd

- 7.1.10 Sharp Corporation

- 7.1.11 Plastic Logic

- 7.1.12 Innolux Corporation

- 7.1.13 AU Optronics Corp.

- 7.1.14 TCL Electronics Holdings Limited

- 7.1.15 Microtips Technology

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2024-2032 年按显示器类型(OLED、LCD、电子纸显示器等)、基板材料、应用和地区分類的柔性显示器市场报告

2024-2032 年按显示器类型(OLED、LCD、电子纸显示器等)、基板材料、应用和地区分類的柔性显示器市场报告 柔性显示技术市场 - 全球产业规模、份额、趋势、机会和预测,按显示类型、技术、最终用户产业、地区、竞争细分,2019-2029F

柔性显示技术市场 - 全球产业规模、份额、趋势、机会和预测,按显示类型、技术、最终用户产业、地区、竞争细分,2019-2029F 柔性显示器市场:按类型、材料和应用划分 - 2024-2030 年全球预测

柔性显示器市场:按类型、材料和应用划分 - 2024-2030 年全球预测 全球柔性显示器市场:市场规模、占有率、成长分析、按类型、按材料类型- 行业预测,2023-2030 年

全球柔性显示器市场:市场规模、占有率、成长分析、按类型、按材料类型- 行业预测,2023-2030 年 全球曲面显示器市场规模研究与预测,按类型(LCD、EPD、LED、OLED)、最终用户(消费电子、交通、零售、广告等)和区域分析,2023-2030 年

全球曲面显示器市场规模研究与预测,按类型(LCD、EPD、LED、OLED)、最终用户(消费电子、交通、零售、广告等)和区域分析,2023-2030 年 柔性显示器市场 - 按显示器类型、基板材料、按应用、地区、公司和地理位置细分的全球行业规模、份额、趋势、机会和预测,2018-2028 年预测和机会。

柔性显示器市场 - 按显示器类型、基板材料、按应用、地区、公司和地理位置细分的全球行业规模、份额、趋势、机会和预测,2018-2028 年预测和机会。 全球柔性显示器市场

全球柔性显示器市场 柔性显示市场:按显示类型、按基板材料、按应用、按地区:市场规模、份额、展望、机会分析,2023-2030 年

柔性显示市场:按显示类型、按基板材料、按应用、按地区:市场规模、份额、展望、机会分析,2023-2030 年 柔性显示器市场:2023-2028年全球行业趋势、份额、规模、增长、机会和预测

柔性显示器市场:2023-2028年全球行业趋势、份额、规模、增长、机会和预测 软性显示器的全球市场预测(2022年~2027年)

软性显示器的全球市场预测(2022年~2027年)