|

市场调查报告书

商品编码

1444241

印刷油墨 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Printing Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

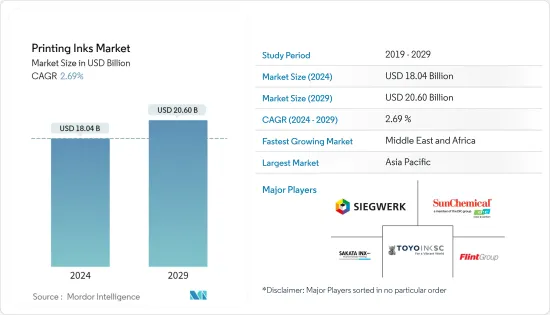

印刷油墨市场规模预计到2024年为180.4亿美元,预计到2029年将达到206亿美元,在预测期内(2024-2029年)CAGR为2.69%。

2020年,受COVID-19影响,各製造工厂关闭,包装需求下降。因此,这影响了包装行业印刷油墨的消耗。然而,食品和饮料行业开始復苏并显示出积极影响。 2021年,产业处于復苏过程中,製造商克服了疫情带来的许多挑战。

主要亮点

- 短期内,数位印刷行业需求成长以及包装和标籤行业需求成长等主要因素预计将推动市场成长。

- 另一方面,传统商业印刷业的衰退以及有关处置的严格法规预计将阻碍所研究市场的成长。

- 儘管如此,生物基和紫外线固化油墨的出现可能很快就会为全球市场创造利润丰厚的成长机会。

- 亚太地区在全球市场中占据主导地位,其中中国的消费量最大。

印刷油墨市场趋势

包装领域的需求不断增加

- 根据包装与加工技术协会 PMMI 发布的报告,全球包装产业的成长预计将从 2016 年的 368 亿美元增至 2021 年的 422 亿美元。发展中地区消费能力的增强预计将增加对包装的需求。

- 数位印刷正在迅速扩展到标籤生产和电子照相领域。由于数位印刷的应用不断增加,预计包装行业在未来十年将经历一场重大革命。

- 由于数位印刷具有快速週转的能力,因此深受各品牌商的欢迎。数位印刷的最新发展,例如数位纸盒切割、压痕和其他完成技术,增加了在软包装、瓦楞包装和折迭纸盒中更多应用的潜力。

- 喷墨製程具有非接触式、低成本等优点,广泛用于在各种基材上进行大幅面印刷,适合包装。它可以比碳粉系统更有效地整合到现有的转换生产线中。

- 随着中国、印度和美国等国家食品工业的发展和人口的增长,硬包装在过去几年中不断增加。

- 软包装是整个包装市场中最大的包装应用领域,具有多种优势,例如比硬包装所需材料少91%,节省空间约96%。此外,随着对永续性的日益关注,传统的硬质包装解决方案正在被创新的柔性包装解决方案所取代。

- 在食品业中,软包装因其吸湿性能、产品新鲜度和温度控製而受到青睐,同时能够保持产品的保质期。除瓶装水等其他产品外,捲烟及相关烟草产品是软包装产业的主要产品。

- 在食品业中,软包装因其吸湿性能、产品新鲜度和温度控製而受到青睐,同时能够保持产品的保质期。除瓶装水等其他产品外,捲烟及相关烟草产品是软包装产业的主要产品。

- 因此,包装产业对印刷油墨的需求预计在预测期内将快速成长。

中国将主导亚太市场

- 亚太地区主导了全球市场份额。随着建筑活动的不断增长和对家具的需求不断增加

- 中国是世界上最大的製造经济体和出口国,其包装需求庞大。 2022年9月,中国包装产业生产了1,160万吨包装纸和纸板,是当年全球最大的生产国。中国柔性、刚性、纸和纸板包装材料的使用呈成长趋势。包装行业的这一积极势头预计将提振印刷油墨的市场需求。

- 此外,包装产业成长显着,快递量呈上升趋势。 2021年我国快递总量约1,080亿件。

- 中国的纺织业僱用了数百万人,为国家的出口和经济做出了巨大贡献。中国服装布料业务获利且规模不断扩大,出口产业日益增长。

- 在国内和全球消费市场,中国服装布料产业在原材料品质、产业结构、现代高科技机械、标籤开发和工作流程等多个领域都在进步。

- 此外,该国纺织业对印刷油墨的需求也不断增加。儘管过去几年纺织业成长缓慢,但该国仍是世界上最大的服装出口国,拥有庞大的产能。

- 由于上述所有因素,该地区的印刷油墨市场预计在预测期内将会成长。

印刷油墨产业概况

全球印刷油墨市场部分整合,前五名厂商主导了全球市场份额。主要参与者包括 Sun Chemicals、Flint Group、Sakata Inx Corporation、Toyo Ink SC Holdings 和 Siegwerk Druckfarben AG & Co 等

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 数位印刷产业不断增长的需求

- 包装和标籤行业的需求不断增长

- 限制

- 传统商业印刷业的衰退

- 严格的处置规定

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场规模按数量计算)

- 类型

- 溶剂型

- 水性

- 油基

- 紫外线

- 紫外线LED

- 其他类型

- 过程

- 平版印刷

- 柔版印刷

- 凹版印刷

- 数位印刷

- 其他流程

- 应用

- 包装

- 硬质包装

- 纸板容器

- 瓦楞纸箱

- 硬质塑胶容器

- 金属罐

- 其他硬质包装

- 软包装

- 标籤

- 其他包装

- 商业及出版

- 纺织品

- 其他应用

- 包装

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 东协国家

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 西班牙

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 领先企业采取的策略

- 公司简介

- ALTANA

- Dainichiseika Color & Chemicals Mfg. Co. Ltd

- Dow

- Epple Druckfarben AG

- Flint Group

- FUJIFILM Corporation

- Hubergroup Deutschland GmbH

- SAKATA INX CORPORATION

- Sanchez SA de CV

- SICPA HOLDING SA

- Siegwerk Druckfarben AG & Co. KGaA

- Sun Chemical

- T&K TOKA Corporation

- Tokyo Printing Ink Mfg Co. Ltd

- Toyo Ink SC Holdings Co. Ltd

- Wikoff Color Corporation

- Yip's Chemical Holdings Limited

- Zeller+Gmelin

第 7 章:市场机会与未来趋势

- 生物基和紫外线固化油墨的出现

- 其他机会

The Printing Inks Market size is estimated at USD 18.04 billion in 2024, and is expected to reach USD 20.60 billion by 2029, growing at a CAGR of 2.69% during the forecast period (2024-2029).

Due to the COVID-19 impact in 2020, various manufacturing plants were shut down, and the demand for packaging has declined. Thus, this affected the consumption of printing inks in the packaging sector. However, the food and beverage industry started recovering and has shown a positive impact. In 2021 the industry was in the recovery process, and the manufacturers overcame many challenges that the pandemic created.

Key Highlights

- In the short term, the major factors such as growing demand from the digital printing industry and the rising demand from the packaging and labels sector are expected to drive the market's growth.

- On the flip side, a decline in the conventional commercial printing industry, and stringent regulations regarding disposal are expected to hinder the growth of the market studied.

- Nevertheless, the emergence of bio-based and UV-curable Inks is likely to create lucrative growth opportunities for the global market soon.

- Asia-Pacific dominated the market across the world, with the largest consumption from China.

Printing Inks Market Trends

Increasing Demand from the Packaging Segment

- According to a report published by PMMI, the Association for Packaging and Processing Technologies, growth in the global packaging industry is anticipated to reach USD 42.2 billion by 2021 from USD 36.8 billion in 2016. This is due to the increasing population, growing sustainability concerns, and more spending power in developing regions are expected to increase the demand for packaging.

- Digital printing is rapidly expanding into label production and electrophotography. The packaging industry is expected to experience a significant revolution over the next decade due to the increasing application of digital printing.

- Due to the quick turnaround capability that digital printing offers, it has been very popular among various brand owners. Recent developments in digital printing, such as digital carton cutting, creasing, and other completion technologies, have increased the potential for more applications in flexible packaging, corrugated packaging, and folding cartons.

- With the advantages of the inkjet process, such as being non-contact and low cost, this process is extensively used for printing large formats on a wide range of substrates, making it suitable for packaging. It can be integrated into existing conversion lines more efficiently than toner systems.

- With the developments in the food industry and the growing population in countries like China, India, and the United States, rigid packaging has been increasing over the past few years.

- Flexible packaging is the largest packaging application segment of the overall packaging market, owing to its various advantages, such as requiring 91% lesser material than rigid packaging, and about 96% of space saving. Moreover, with an increasing focus on sustainability, traditional rigid packaging solutions are being replaced by innovative and flexible packaging solutions.

- In the food industry, flexible packaging is preferred due to its moisture absorption properties, product freshness, and temperature control, while being able to maintain the shelf life of the product. Cigarettes and associated tobacco products are the major products for the flexible packaging industry, among other products, such as bottled water.

- In the food industry, flexible packaging is preferred due to its moisture absorption properties, product freshness, and temperature control, while being able to maintain the shelf life of the product. Cigarettes and associated tobacco products are the major products for the flexible packaging industry, among other products, such as bottled water.

- Hence, the demand for printing inks from the packaging industry is expected to grow at a rapid rate during the forecast period.

China to Dominate the Asia-Pacific Market

- The Asia-Pacific region dominated the global market share. With growing construction activities and the increasing demand for furniture

- China stands to be the world's largest manufacturing economy and exporter, due to which its packaging requirement is huge. The packaging industry in China produced 11.6 million metric tons million metric ton of packaging paper and paperboard in September 2022 and was the largest producer worldwide that year. China sees a growing trend in the use of flexible, rigid, and paper and board packaging materials. This positive momentum in the packaging industry is expected to boost the market demand for printing inks.

- Additionally, the packaging industry witnessed noticeable growth, with the increasing trend of express deliveries. the total volume of express delivery in China amounted to about 108 billion pieces in 2021.

- The textile industry in China employs millions of people and contributes significantly to the country's exports and economy. Chinese apparel cloth businesses are profitable and expanding, with the export sector experiencing day-to-day growth.

- In both the domestic and global consumer markets, the Chinese garment cloth industry is progressing in many areas, including raw material quality, industrial structure, modern high-tech machinery, label development, and the work process.

- Additionally, printing ink demand has also been increasing from the textile industry in the country. The country stands to be the largest clothing exporter in the world, holding massive production capacity, although the textile industry witnessed a slow growth in the past few years.

- Owing to all the above-mentioned factors, the market for printing inks in the region is projected to increase during the forecast period.

Printing Inks Industry Overview

The global printing inks market is partially consolidated, the top five players dominated the global market share. Some of the Major players include Sun Chemicals, Flint Group, Sakata Inx Corporation, Toyo Ink SC Holdings Co. Ltd, and Siegwerk Druckfarben AG & Co, among others

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Digital Printing Industry

- 4.1.2 Rising Demand from the Packaging and Labels Sector

- 4.2 Restraints

- 4.2.1 Decline in the Conventional Commercial Printing Industry

- 4.2.2 Stringent Regulations Regarding Disposal

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Solvent-based

- 5.1.2 Water-based

- 5.1.3 Oil-based

- 5.1.4 UV

- 5.1.5 UV-LED

- 5.1.6 Other Types

- 5.2 Process

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Gravure Printing

- 5.2.4 Digital Printing

- 5.2.5 Other Processes

- 5.3 Application

- 5.3.1 Packaging

- 5.3.1.1 Rigid Packaging

- 5.3.1.1.1 Paperboard Containers

- 5.3.1.1.2 Corrugated Boxes

- 5.3.1.1.3 Rigid Plastic Containers

- 5.3.1.1.4 Metal Cans

- 5.3.1.1.5 Other Rigid Packaging

- 5.3.1.2 Flexible Packaging

- 5.3.1.3 Labels

- 5.3.1.4 Other Packaging

- 5.3.2 Commercial and Publication

- 5.3.3 Textiles

- 5.3.4 Other Applications

- 5.3.1 Packaging

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Australia & New Zealand

- 5.4.1.6 ASEAN Countries

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.2.4 Rest of North America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Spain

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East & Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East & Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ALTANA

- 6.4.2 Dainichiseika Color & Chemicals Mfg. Co. Ltd

- 6.4.3 Dow

- 6.4.4 Epple Druckfarben AG

- 6.4.5 Flint Group

- 6.4.6 FUJIFILM Corporation

- 6.4.7 Hubergroup Deutschland GmbH

- 6.4.8 SAKATA INX CORPORATION

- 6.4.9 Sanchez SA de CV

- 6.4.10 SICPA HOLDING SA

- 6.4.11 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.12 Sun Chemical

- 6.4.13 T&K TOKA Corporation

- 6.4.14 Tokyo Printing Ink Mfg Co. Ltd

- 6.4.15 Toyo Ink SC Holdings Co. Ltd

- 6.4.16 Wikoff Color Corporation

- 6.4.17 Yip's Chemical Holdings Limited

- 6.4.18 Zeller+Gmelin

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence of Bio-based and UV-curable Inks

- 7.2 Other Opportunities

凹版印刷油墨市场 - 全球产业规模、份额、趋势、机会和预测,按技术、树脂类型、着色剂、油墨黏度、应用、地区和竞争细分,2019-2029F

凹版印刷油墨市场 - 全球产业规模、份额、趋势、机会和预测,按技术、树脂类型、着色剂、油墨黏度、应用、地区和竞争细分,2019-2029F 中国的印刷油墨市场

中国的印刷油墨市场 2024 年印刷油墨世界市场报告

2024 年印刷油墨世界市场报告 全球油性印刷油墨市场 - 2023-2030

全球油性印刷油墨市场 - 2023-2030 全球 UV 固化印刷油墨市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球 UV 固化印刷油墨市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 凹版印刷油墨2024年世界市场报告

凹版印刷油墨2024年世界市场报告 UV 固化印刷油墨市场(类型:电弧固化和 LED 固化;油墨类型:自由基和阳离子)- 2023-2031 年全球产业分析、规模、份额、成长、趋势和预测

UV 固化印刷油墨市场(类型:电弧固化和 LED 固化;油墨类型:自由基和阳离子)- 2023-2031 年全球产业分析、规模、份额、成长、趋势和预测 柔性印刷油墨市场报告:2030 年趋势、预测与竞争分析

柔性印刷油墨市场报告:2030 年趋势、预测与竞争分析 2024年油性印刷油墨全球市场报告

2024年油性印刷油墨全球市场报告 印刷油墨市场:按类型、工艺、应用分类 - 2023-2030 年全球预测

印刷油墨市场:按类型、工艺、应用分类 - 2023-2030 年全球预测