|

市场调查报告书

商品编码

1444353

平板玻璃 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029 年)Flat Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

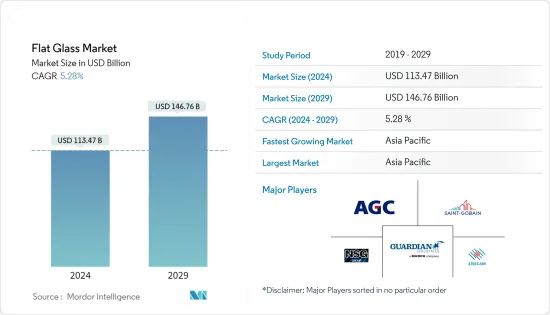

平板玻璃市场规模预计到2024年为1134.7亿美元,预计到2029年将达到1467.6亿美元,在预测期内(2024-2029年)CAGR为5.28%。

受疫情影响,大部分生产设施停工,汽车生产受到严重影响,生产设施因停工而受到影响达数月之久。全世界的供应链都断裂了。由于债务增加,疫情爆发造成的经济不稳定也使得公共和私营部门的开发商重新考虑他们的项目。这造成了建筑业的衰退。

主要亮点

- 短期内,电子显示器需求的成长和建筑业需求的成长是推动所研究市场成长的主要因素。

- 然而,全球经济衰退的影响和中国 COVID-19 的復苏可能会抑制所研究市场的成长。

- 儘管如此,汽车行业的进步和太阳能行业的不断涌现可能很快就会为全球市场创造利润丰厚的成长机会。

- 亚太地区主导平板玻璃市场,最大消费来自中国、日本、东协国家等国家。

平板玻璃市场趋势

建筑业将拉动平板玻璃的需求

- 平板玻璃因其广泛的功能而在建筑行业中广泛应用,从隔热到隔音,从安全应用到遮阳。

- 平板玻璃的最新进展使该材料表现出自清洁能力。有机污垢会被阳光中的紫外线分解。下雨时,破碎的污垢被简单地从窗户上冲走,几乎不留下任何痕迹;水不会像在传统玻璃上那样形成水滴,而是形成一层覆盖玻璃整个表面的薄膜,并在流走时带走污垢。因此,在下雨时,自清洁玻璃比传统玻璃具有更好的可视性。

- 建筑和基础设施发展的成长与平板玻璃的需求直接相关,从而推动了市场的成长。最近的趋势显示建筑结构正在迅速变化,在外墙和屋顶上使用平板玻璃,优化自然采光。

- 在北美,美国在该地区整体住宅建筑业中占有重要份额。根据美国人口普查局的数据,2021 年美国住宅建设年价值为 8,029.33 亿美元,而 2020 年为 6,442.57 亿美元。

- 从2021年开始,亚太地区的一些地区的建筑业预计将成为该国成长最快的产业之一。建筑业预计将从 2020 年收缩 18.7% 反弹至 2021 年成长 13.9%。

- 根据普华永道的数据; Urban Land Institute认为,2022年工业不动产是亚太地区商业不动产中前景最好的,指数得分为6.99(分数范围为1-9)。

- 根据土木工程师学会预测,未来十年,全球建筑产量预计将成长 85%,收入将达到 15.5 兆美元,其中印度、中国等新兴国家和美国等已开发国家领先。

- 由于印度和东协国家等发展中国家住房建设市场的不断扩大,亚太地区预计将见证新住宅建设项目的最高成长。

- 在印度,建筑业贡献了该国GDP的约9%。允许在自动路线下对印度建筑业进行 100% 外国直接投资,用于城镇、商场/购物中心和商业建筑运营和管理的已竣工项目。预计这些因素将有助于所研究市场的成长。

- 据 IBEF 称,政府在 2022-23 年联邦预算中拨款 10 亿印度卢比(1,305.7 亿美元)来加强基础设施部门,大力推动基础设施部门的发展。

中国将主导亚太地区

- 中国是全球最大的平板玻璃生产国,在该地区占有重要的市场份额。中国的许多製造商一直致力于创造符合西方生产水准和环境标准的产品。

- 能源产业对太阳能应用中平板玻璃的需求不断增长。中国拥有比世界上任何其他国家都多的太阳能发电能力。它是腾格里沙漠世界上最大的太阳能发电场之一的所在地。在可预见的未来,预计该国仍将是再生能源的最大投资者。

- 亚太地区在全球汽车市场的产量份额最高,2021年产量为46,732,785辆。2021年,中国约占全球汽车产量的32.5%。在乘用车市场,中国乘用车年产量超过日本、德国、印度、韩国的总和。 2021年中国也是全球最大的汽车销售市场。

- 根据OICA的数据,汽车总产量从2020年的25,225,242辆增加到2021年的26,082,220辆。

- 根据CEC;中国能源入口网站数据显示,截至2021年,我国太阳能发电装置容量已超过300吉瓦。预测期内,中国在增加太阳能发电容量方面取得了长足进步,累计容量从2017年的125.79吉瓦增加到2021年的306.56吉瓦。

平板玻璃产业概况

平板玻璃市场本质上是整合的。主要参与者包括 Saint-Gobain、AGC Inc.、Guardian Industries、Nippon Sheet Glass 和 Sisecam 等(排名不分先后)。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 司机

- 对电子显示器不断增长的需求

- 建筑业需求不断增加

- 限制

- 即将到来的全球经济衰退的影响以及 COVID-19 在中国的死灰復燃

- 其他限制

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第 5 章:市场区隔(市场价值规模)

- 产品类别

- 退火玻璃(包括有色玻璃)

- 镀膜玻璃

- 反光玻璃

- 加工玻璃

- 镜子

- 最终用户产业

- 建筑与施工

- 汽车

- 太阳能玻璃

- 其他最终用户产业

- 地理

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 东协国家

- 亚太其他地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 中东和非洲其他地区

- 亚太

第 6 章:竞争格局

- 併购、合资、合作与协议

- 市场排名分析

- 领先企业采取的策略

- 公司简介

- AGC Inc.

- Asahi India Glass Limited

- Cardinal Glass Industries Inc.

- China Glass Holdings Limited

- Fuyao Glass Industry Group Co., Ltd.

- Guardian Industries

- Nippon Sheet Glass Co. Ltd

- Phoenicia

- Saint-Gobain

- SCHOTT

- Sisecam

- Taiwan Glass Industry Corporation

- Vitro

第 7 章:市场机会与未来趋势

- 汽车工业的进步

- 太阳能产业不断涌现的倡议

The Flat Glass Market size is estimated at USD 113.47 billion in 2024, and is expected to reach USD 146.76 billion by 2029, growing at a CAGR of 5.28% during the forecast period (2024-2029).

Most manufacturing facilities were shut down due to the pandemic, and automotive production was affected severely, which impacted production facilities for several months due to the lockdown. The supply chain throughout the world was fractured. The economic instability due to the pandemic outbreak has also made developers, in both public and private sectors, rethink their projects as debts mount. This has created a downfall in the construction sector.

Key Highlights

- Over the short term, the growing demand for electronic displays and increasing demand from the construction industry are major factors driving the growth of the market studied.

- However, the impact of the global recession and the resurgence of COVID-19 in China are likely to restrain the growth of the studied market.

- Nevertheless, advancements in the automotive industry and rising initiatives in the solar industry are likely to create lucrative growth opportunities for the global market soon.

- The Asia-Pacific region dominates the flat glass market, with the largest consumption coming from countries such as China, Japan, ASEAN countries, etc.

Flat Glass Market Trends

Construction Industry to Drive the Demand for Flat Glass

- Flat glass is used significantly in the construction industry owing to its wide range of functions, from heat insulation to soundproofing and from safety applications to solar protection.

- Recent advancements in flat glass have enabled the material to exhibit self-cleaning abilities. Organic dirt is broken down by ultraviolet light in sunlight. When it rains, the broken-down dirt is simply washed off the windows, leaving almost no streaks; instead of forming droplets as it would on conventional glass, the water forms a film that covers the entire surface of the glass and takes the dirt with it as it runs off. Thus, self-cleaning glass offers better visibility than conventional glass when it rains.

- The growth of construction and infrastructure development directly links to the demand for flat glass, which drives the market's growth. The recent trend suggests a rapid change in building architecture, with the use of flat glass in facades and roofs, optimizing natural daylight.

- In North America, the United States has a significant share of the overall residential construction sector in the region. According to the United States Census Bureau, the annual value of residential construction put in place in the United States was USD 802,933 million in 2021, compared to USD 644,257 million in 2020.

- From 2021, a few regions of Asia-Pacific in the construction sector are expected to be one of the fastest-growing sectors in the country. The construction sector is projected to rebound to a growth of 13.9% in 2021, from an 18.7% contraction in 2020.

- According to PwC; Urban Land Institute, industrial real estate had the best prospects among commercial properties in the Asia-Pacific region in 2022 with an index score of 6.99 on a scale of 1-9.

- According to the Institution of Civil Engineers, the volume of construction output is forecasted to grow by 85%, with a revenue of USD 15.5 trillion worldwide in the upcoming decade, led by emerging countries such as India and China and developed countries like the United States.

- The Asia-Pacific is expected to witness the highest growth in new residential construction projects due to the expanding housing construction market in developing countries, like India, and ASEAN countries.

- In India, the construction industry contributes to about 9% of the country's GDP. 100% Foreign direct investment in the construction industry in India under automatic route is permitted in completed projects for operations and management of townships, malls/shopping complexes, and business constructions. These factors are expected to contribute towards the growth of the market studied.

- According to IBEF, the government has given a massive push to the infrastructure sector by allocating INR 10 lakh crore (USD 130.57 billion) to enhance the infrastructure sector in the Union Budget 2022-23.

China to Dominate the Asia-Pacific Region

- China is the largest producer of flat glass in the world, holding a significant market share in the region. Many manufacturers in China have been geared to create products that meet Western production levels and environmental standards.

- The energy sector is witnessing rising demand for flat glass in solar power applications. China has more solar capacity than any other country in the world. It is home to one of the biggest solar farms in the world in the Tengger Desert. The nation is expected to remain the largest investor in renewable energy for the foreseeable future.

- The Asia-Pacific region holds the highest production share in the global automotive market, with 46,732,785 units in 2021. In 2021, China accounted for about 32.5% of global car production. In the passenger car market, China's annual production for passenger cars exceeded that of Japan, Germany, India, and South Korea combined. China was also the world's largest automobile sales market in 2021.

- According to OICA, the total number of vehicle production increased from 25,225,242 units in 2020 to 26,082,220 units in 2021.

- According to CEC; China Energy Portal, as of 2021, China has installed more than 300 gigawatts of solar power capacity. China made great strides in increasing solar power capacity during the forecast period, increasing cumulative capacity from just 125.79 GW in 2017 to 306.56 GW in 2021.

Flat Glass Industry Overview

The flat glass market is consolidated in nature. The major players include Saint-Gobain, AGC Inc., Guardian Industries, Nippon Sheet Glass Co., Ltd, and Sisecam, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Electronic Displays

- 4.1.2 Increasing Demand from the Construction Industry

- 4.2 Restraints

- 4.2.1 Impact of the Upcoming Recession Across the Globe and the Resurgence of COVID-19 in China

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Annealed Glass (Including Tinted Glass)

- 5.1.2 Coater Glass

- 5.1.3 Reflective Glass

- 5.1.4 Processed Glass

- 5.1.5 Mirrors

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Solar Glass

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 Asahi India Glass Limited

- 6.4.3 Cardinal Glass Industries Inc.

- 6.4.4 China Glass Holdings Limited

- 6.4.5 Fuyao Glass Industry Group Co., Ltd.

- 6.4.6 Guardian Industries

- 6.4.7 Nippon Sheet Glass Co. Ltd

- 6.4.8 Phoenicia

- 6.4.9 Saint-Gobain

- 6.4.10 SCHOTT

- 6.4.11 Sisecam

- 6.4.12 Taiwan Glass Industry Corporation

- 6.4.13 Vitro

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancement in the Automotive Industry

- 7.2 Rising Initiatives in the Solar Industry

中东和非洲平板玻璃:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年)

中东和非洲平板玻璃:市场占有率分析、行业趋势、统计数据和成长预测(2025-2030 年) 亚太平板玻璃:市场占有率分析、产业趋势与成长预测(2025-2030 年)

亚太平板玻璃:市场占有率分析、产业趋势与成长预测(2025-2030 年) 北美平板玻璃:市场占有率分析、产业趋势、成长预测(2025-2030)

北美平板玻璃:市场占有率分析、产业趋势、成长预测(2025-2030) 拉丁美洲平板玻璃:市场占有率分析、产业趋势、成长预测(2025-2030)

拉丁美洲平板玻璃:市场占有率分析、产业趋势、成长预测(2025-2030) 欧洲平板玻璃:市场占有率分析、行业趋势和成长预测(2025-2030 年)

欧洲平板玻璃:市场占有率分析、行业趋势和成长预测(2025-2030 年) 平板玻璃市场:按类型、治疗玻璃、应用划分 - 2025-2030 年全球预测

平板玻璃市场:按类型、治疗玻璃、应用划分 - 2025-2030 年全球预测 全球平板玻璃市场预测(2025-2030年)

全球平板玻璃市场预测(2025-2030年) 平板玻璃市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年

平板玻璃市场规模、份额、趋势分析报告:按产品、最终用途、地区、细分市场预测,2025-2030 年 建筑平板玻璃市场机会、成长动力、产业趋势分析及 2024 年至 2032 年预测

建筑平板玻璃市场机会、成长动力、产业趋势分析及 2024 年至 2032 年预测 冷藏玻璃门市场:全球产业分析,规模,占有率,成长,趋势,预测,2024年~2033年

冷藏玻璃门市场:全球产业分析,规模,占有率,成长,趋势,预测,2024年~2033年