|

市场调查报告书

商品编码

1640682

企业伺服器 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Enterprise Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

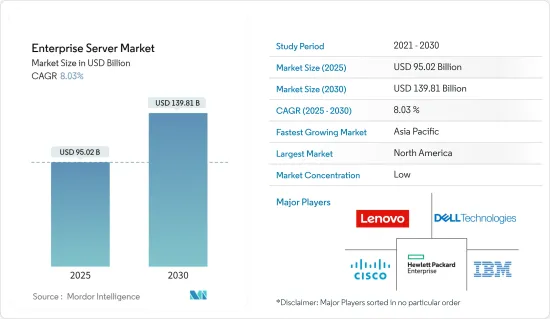

预计 2025 年企业伺服器市场规模为 950.2 亿美元,到 2030 年将达到 1,398.1 亿美元,预测期内(2025-2030 年)的复合年增长率为 8.03%。

预计市场将出现强大的创新,以提高效能、速度和内存,以支援巨量资料、高效能运算和商业智慧应用的普及。

关键亮点

- 企业伺服器是一种电脑伺服器,它包含满足公司(而不是单一单位、使用者或特定应用程式)需求所需的程式。企业伺服器提供连线整合、广播、TCP/IP、多播选择以及使用者定义的衝突和休眠工具,以提高网路和桌面效能。

- 企业伺服器市场主要受到超大规模资料中心容量投资增加的推动,从而重塑了核心伺服器市场。此外,伺服器市场预计将经历伺服器更新周期,这可能会对未来几年的市场成长产生积极影响。

- 此外,快闪记忆体、虚拟和先进管理等新技术可能为市场成长提供新的途径。为满足企业和最终用户的特定运算需求而开发的新应用程式也有望为企业伺服器市场的成长做出重大贡献。

- 目前的伺服器数量无法在管理资料流量、工作负载和运算的同时跟上不断增长的资料中心流量。不断提高的伺服器运算能力和虚拟、多重工作负载以及每个实体伺服器更多的运算实例都要求有更多资料中心来处理这些负载。这是推动全球资料中心基础设施投资的主要因素,为企业伺服器市场的成长做出了重大贡献。

- 然而,使用企业伺服器的高昂前期和安装成本是阻碍其广泛采用的主要问题之一。高阶企业伺服器对市场构成了障碍,因为它们的安装和维护需要大量的技术技能。

企业伺服器市场趋势

机架优化伺服器类型高速成长

- 机架伺服器比塔式伺服器相对较小,安装在机架内。它旨在容纳各种电子设备,包括冷却系统、储存单元、网路周边设备、电池和 SAN 设备,这些设备垂直堆迭在伺服器旁边。

- 使用机架伺服器的主要优点是使用者可以将所需的电子设备与伺服器堆迭在一起,一个机架可以存储多台伺服器,占用更少的空间,对全球许多人来说更实惠。爱。

- 预计预测期内,云端服务供应商采用超大规模资料中心将大幅推动市场发展。此外,对机架优化伺服器的需求正在快速成长,迫使工业公司对这项技术进行投资。

- Supermicro 是解决方案供应商,该公司今天宣布,正在其核心 Supermicro 伺服器产品组合中扩大对领先开放硬体和开放原始码技术的采用。此外,新发布的 8U 8-GPU 机架优化系统为大规模 AI 训练提供了卓越的功率和热性能,并包含一系列开放技术。

亚太地区成长率最高

- 据估计,由于人工智慧、物联网和巨量资料等技术在各个终端用户产业中的应用日益广泛,对企业伺服器的需求也随之增加,因此亚太地区预计将实现最高的成长率。

- 此外,随着跨国和国内公司越来越多地转向云端服务供应商,资料中心服务的成长也推动了亚太地区企业伺服器的需求。

- 此外,印度政府的云端运算政策规定,印度境内产生的资料可以储存在印度境内,这可能导致印度境内资料储存中心的数量和规模增加,从而有望振兴企业伺服器市场。

- 此外,Google、苹果等大公司也计划在中国建立资料中心,为其不断成长的业务寻求更好的连接和可扩展的解决方案。

企业伺服器产业概览

企业伺服器市场竞争激烈,许多国内外参与企业进入该市场。目前,市场正在整合,少数参与企业占据市场主导地位。主要企业采取的关键策略包括产品创新和併购。市场的主要企业包括惠普企业、戴尔科技公司、IBM 和思科系统公司。

- 2022 年 11 月,联想将推出搭载第四代 AMD EPYC 处理器的 ThinkSystem 伺服器和 ThinkAgile 超融合 (HCI) 解决方案,包括 ThinkAgile VX 和 ThinkAgile HX,以加速混合多重云端部署并简化基础架构管理。

- 2022 年 5 月,IBM 宣布将把 ESS 3500 添加到其 Spectrum Scale 企业储存伺服器 (ESS) 产品组合中,具有更快的控制器 CPU 和更高的吞吐量。它旨在与 Nvidia 的 DGX 密集计算伺服器配合进行 AI 训练。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查结果和先决条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 云端迁移的兴起

- 巨量资料的成长

- 市场限制

- 采用伺服器虚拟

第六章 市场细分

- 按作业系统

- Linux

- Windows

- UNIX

- 其他作业系统(i5/OS、z/OS 等)

- 按伺服器类别

- 高阶伺服器

- 中阶伺服器

- 低负载伺服器

- 按伺服器类型

- 刀刃

- 多节点

- 塔型

- 机架优化

- 按行业

- 资讯科技/通讯

- BFSI

- 製造业

- 零售

- 医疗

- 媒体娱乐

- 其他行业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Hewlett Packard Enterprise Co.

- Dell Technologies Inc.

- IBM Corporation

- Cisco Systems Inc.

- Lenovo Group Ltd

- Oracle Corporation

- NEC corporation

- Unisys Corporation

- Fujitsu Ltd

- Hitachi Ltd

- Toshiba Corporation

第八章投资分析

第九章:市场的未来

The Enterprise Server Market size is estimated at USD 95.02 billion in 2025, and is expected to reach USD 139.81 billion by 2030, at a CAGR of 8.03% during the forecast period (2025-2030).

The market landscape is expected to witness strong innovations to enhance performance, speed, and memory to support the surge of Big Data, high-performance computing, and business intelligence applications.

Key Highlights

- An enterprise server is a computer server that includes programs required to collectively serve the requirements of an enterprise instead of an individual unit, user, or specific application. An enterprise server provides consolidated connections, a choice of broadcast, TCP/IP, or multicast, as well as user-defined tools for conflation and hibernation, resulting in improved network and desktop performance.

- The market for enterprise servers is majorly driven by the increased investments in the capacity of hyperscale data centers to reshape the core server market. The server market is also expected to witness a server-refresh cycle, which may favorably impact market growth over the next few years.

- Furthermore, emerging technologies, such as flash storage, virtualization, and advanced management, may offer new avenues for market growth. New applications (developed to meet specific computing requirements of the enterprises and end users) are also expected to contribute significantly to the growth of the enterprise server market.

- With the current number of servers, managing data traffic, workload, and computing have been unable to keep up with the snowballing growth in data center traffic. With the increasing server computing capacity and virtualization, multiple workloads, and compute instances per physical server, there is a demand for more data centers to handle this load. This has been a significant factor driving investments in data center infrastructure across the world, significantly contributing to the growth of the enterprise server market.

- However, the high initial and installation costs related to using enterprise servers are one of the main concerns preventing their wider adoption. High-end corporate servers demand a significant level of technical skill to install and maintain, which is a barrier for the studied market.

Enterprise Server Market Trends

Rack Optimized Server Type to Witness High Growth

- A rack server is comparatively smaller and mounted within a rack compared to a tower server. It is designed to be positioned vertically, stacking various electronic devices, such as cooling systems, storage units, network peripherals, batteries, and SAN devices, with servers one over the other.

- The primary advantage of using a rack server is that a user can stack any required electronic devices with the server, wherein a single rack can contain multiple servers, hence, consuming lesser space, due to which it is now mostly preferred by many organizations across the world.

- Hyperscale data center adoption by cloud service providers is expected to drive the market considerably over the forecast period. Moreover, the demand for rack-optimized servers is rapidly increasing, compelling the industry players to invest in this technology.

- Supermicro, an IT solution provider for cloud, AI/ML, storage, and 5G/Edge, announced the expanded adoption of key open hardware and open source technologies into the core Supermicro server portfolio. Moreover, the newly launched 8U 8-GPU Rack Optimized Systems delivers superior power and thermal capabilities for large-scale AI Training and includes a host of open technologies.

Asia-Pacific to Witness Highest Growth Rate

- The Asia-Pacific region is estimated to register the highest growth rate, due to the increasing adoption of technologies, such as artificial intelligence, the Internet of Things, and Big Data, in various end-user industries, thus, increasing the demand for enterprise servers in this region.

- The increasing data center services in the Asia-Pacific region, owing to the growing number of multinational and domestic enterprises turning toward cloud service providers, are also driving the need for enterprise servers.

- Moreover, the Indian government's cloud computing policy, which says that the data generated in India may be stored within the country, may ramp up the number and size of data storage centers in India, thus, boosting the enterprise server market.

- Furthermore, major firms, such as Google and Apple, are also planning to open their data centers in China to seek enhanced connectivity and scalable solutions for their growing businesses.

Enterprise Server Industry Overview

The enterprise server market is competitive, owing to the presence of many players in the market in the market, both domestic and international. The market is consolidated as some players currently occupy most of the market. Some of the key strategies adopted by the major players are product innovation and mergers and acquisitions. Some major players in the market are Hewlett Packard Enterprise Co., Dell Technologies Inc., IBM Corporation, and Cisco Systems Inc., among others.

- On November 2022, Lenovo announced the launch of ThinkSystem servers and ThinkAgile hyper-converged (HCI) solutions, powered by 4th Gen AMD EPYC processors, including ThinkAgile VX and ThinkAgile HX, to enable faster hybrid multi-cloud deployment and simplify infrastructure management.

- On May 2022, IBM announced the launch of ESS 3500 to its Spectrum Scale Enterprise Storage Server (ESS) portfolio featuring a faster controller CPU and more throughput. It is designed to work with Nvidia's DGX-dense compute servers for AI training.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables and Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Migration to the Cloud

- 5.1.2 Growth of Big Data

- 5.2 Market Restraints

- 5.2.1 Adoption of Server Virtualization

6 MARKET SEGMENTATION

- 6.1 By Operating System

- 6.1.1 Linux

- 6.1.2 Windows

- 6.1.3 UNIX

- 6.1.4 Other Operating Systems (i5/OS, z/OS, etc.)

- 6.2 By Server Class

- 6.2.1 High-end Server

- 6.2.2 Mid-range Server

- 6.2.3 Volume Server

- 6.3 By Server Type

- 6.3.1 Blade

- 6.3.2 Multi-node

- 6.3.3 Tower

- 6.3.4 Rack Optimized

- 6.4 By End-user Vertical

- 6.4.1 IT and Telecommunication

- 6.4.2 BFSI

- 6.4.3 Manufacturing

- 6.4.4 Retail

- 6.4.5 Healthcare

- 6.4.6 Media and Entertainment

- 6.4.7 Other End-user Verticals

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia-Pacific

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Hewlett Packard Enterprise Co.

- 7.1.2 Dell Technologies Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Cisco Systems Inc.

- 7.1.5 Lenovo Group Ltd

- 7.1.6 Oracle Corporation

- 7.1.7 NEC corporation

- 7.1.8 Unisys Corporation

- 7.1.9 Fujitsu Ltd

- 7.1.10 Hitachi Ltd

- 7.1.11 Toshiba Corporation