|

市场调查报告书

商品编码

1444435

全球网路自动化市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Network Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

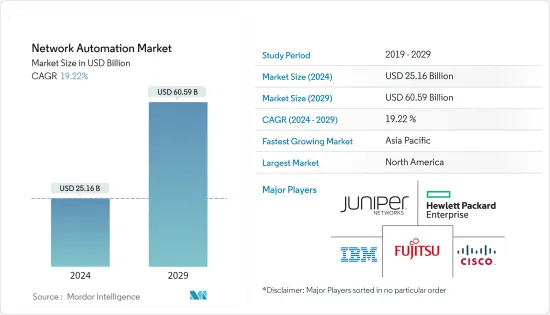

全球网路自动化市场规模预计在 2024 年将达到 251.6 亿美元,并在 2024-2029 年预测期内以 19.22% 的复合年增长率增长,到 2029 年将达到 605.9 亿美元。

公营和私人公司以及政府机构强制员工在家工作(WFH),这给网路技术带来了不可预见的压力,并增加了网路流量,造成了全球范围内蔓延的频宽和安全问题。正在引领中国的网路自动化市场。

主要亮点

- 随着越来越多的用户、装置和应用程式依赖企业网路来实现与各种端点的关键连接,企业网路面临压力。组织对新的网路架构和先进的管理工具越来越感兴趣,这些工具利用机器学习和人工智慧来创建自动驾驶或自主网路。这些进步也显着改变了企业依赖合作伙伴和供应商服务的方式。

- 网路自动化最重要的好处之一是降低营运成本。透过使用自动化且协调的基础架构消除繁琐的手动流程,您不仅可以扩展网路的功能,还可以更快地实现投资回报。

- 自动化还可以减少错误并提高弹性。除了自动化手动任务和最大限度地减少网路错误之外,许多解决方案还可以在无需干预的情况下自动回应网路错误,从而提高业务弹性并确保员工在需要时始终可以存取应用程式和资料。提高网路自动化水平有助于降低复杂性,对于企业跟上数位世界的步伐至关重要。

- 限制市场成长的主要因素之一是某些公司担心自动化解决方案可能会忽略安全问题或施加许多网路限制。此外,实施自动化系统和解决方案需要组织聘请专家或培训其目前的网路团队,最终增加开展业务的成本。

- 在 COVID-19感染疾病期间,自动化在维持 IT 营运方面发挥关键作用。根据 4 月 22 日 Verizon 网路报告,该公司网路的资料量与感染疾病 19 之前的水平相比增加了 19%。儘管资料使用仍在增加,但人们使用网路的方式的变化是稳定的。 Verizon 预计其用户将继续保持高水准。

网路自动化市场趋势

虚拟网路领域预计将占据主要市场占有率

- 网路功能虚拟(NFV) 和软体定义网路 (SDN) 抽象化了新网路功能的实现,并将它们与硬体基础设施和相关拓扑约束解耦。这使得通讯网路可程式设计,从而更加灵活和敏捷。

- SDN和NFV都被视为通讯服务供应商转型的关键使能技术,提供了满足市场需求的低成本手段。推动该市场的主要最终用户是需要减少资本支出、提高效率和提供新服务的通讯业者。 NFV 始终透过虚拟在 DPI、防火墙、负载平衡器和会话边界控制器 (SBC) 等专用设备上执行的网路服务来补充 SDN。这允许这些服务在单一电脑池上运行。减少硬体并节省资本支出和营运支出。

- 网路虚拟和自动化在遇到意外使用高峰的环境中非常有用。自动化网路可以透过自动将网路流量重新导向到网路影响较小区域的伺服器来处理这些峰值。

- 企业开始将其虚拟环境扩展到简单的虚拟伺服器部署之外。我们目前正在为动态工作负载和私有云端基础架构实施虚拟灾害復原和虚拟支援。在这个过程中,他们遇到了物理和逻辑网路前所未有的变化速度和复杂性的增加。

- 多个开放原始码计划致力于透过虚拟建立网路自动化标准。例如,欧洲电讯标准协会 (ETSI) 的 NFV 管理和编配(MANO) 行业规范组 (ISG) 重点关注云端基础的资料中心中网路资源的管理和编配。这些标准可实现 SDN 和 NFV 平台之间更好、更有效率的通讯。

- Microsoft 的 Azure 虚拟网路 (VNet) 是 Azure 专用网路的基本建置区块。 VNet 允许不同类型的 Azure 资源(例如 Azure 虚拟机器 (VM))安全地相互通讯、与 Internet 和本机网路通讯。 VNet 与资料中心中运行的传统网路相当,但为 Azure 基础架构带来了额外的好处,例如规模、可用性和隔离。

欧洲占主要市场占有率

- 由于欧洲地区的快速扩张以及 Microfocus International PLC、诺基亚通讯、爱立信和 Entity Network Management 等市场参与者的存在,欧洲地区在网路自动化领域占据了主要份额。

- 在欧洲,软体定义网路(SDN)和网路功能虚拟(NFV)技术的采用日益增加。这些因素正在迅速改变大型企业建立广域网路以满足其不断增长的网路需求的方式。此外,在组织中部署多种技术会增加其IT基础设施的复杂性,从而进一步增加对网路自动化解决方案的需求。

- 5G技术将进一步增加技术和网路架构的复杂性。通讯服务供应商越来越需要智慧管理系统来处理数量迅速增加的实体和虚拟网路事件,这些事件可能会给网路营运中心带来巨大压力。思科与 Telefonica 合作实施网路自动化,以简化西班牙服务供应商的业务,为 5G 时代做好准备。这个新的自动化网路由思科的 Crosswork 网路自动化套件提供支持,可以为 Telefonica 提供更好的营运洞察力和网路健康状况。

- 此外,三星电子和沃达丰英国也宣布推出英国首个 5G Open RAN 站点,目前正在处理活跃的客户流量。位于英国巴斯的站点是沃达丰在欧洲第一个可扩展的开放式 RAN 网路设计,另外还有 2,500 多个站点。两家公司完成了由三星 5G虚拟无线接取网路(vRAN) 提供支援的 5G 即时视讯对话,以纪念首次站点部署。这是英国于 2022 年 1 月首次征集商用 5G Open RAN。

网路自动化产业概况

网路自动化市场正逐渐成为一个碎片化的市场。各个最终用户行业的云端趋势和不断增长的网路流量预计很快就会显着增长。为了在网路自动化形势保持立足点,当前市场领导的竞争策略非常强大,主要是透过收购各种新兴企业和解决方案供应商来推动的。该市场的主要企业是思科系统公司、瞻博网路公司和IBM公司。

2022年12月,T-Mobile和思科宣布推出弹性的分散式全球云端原生融合核心闸道。 Un-Carrier已将所有5G和4G流量迁移到新的云端原生核心闸道。这使我们的客户在频宽和延迟方面的效能提高了 10% 以上。 T-Mobile 可透过全自动融合核心闸道简化跨云端、边缘和资料中心的网路任务,从而显着减少营运生命週期管理。

2022 年 1 月,慧与与日本电讯供应商 OPTAGE 合作,后者选择 HPE 5G 核心堆迭作为其本地 5G 网路测试台。 OPTAGE已经测试了本地5G网路的可行性,以满足各种最终用户商业客户的需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 工业吸引力 - 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌意强度

- 产业价值链分析

- 技术简介

- 评估 COVID-19 对市场的影响

- 市场驱动因素

- 资料中心网路需求不断增长

- 连网型设备的成长趋势

- 市场限制因素

- 各行各业都缺乏熟练的专业人员。

第五章市场区隔

- 网路类型

- 身体的

- 虚拟的

- 混合

- 解决方案类型

- 网路自动化工具

- SD-WAN/网路虚拟

- 意图式网路

- 服务类型

- 管理服务

- 专业服务

- 介绍

- 云

- 本地

- 混合

- 最终用户产业

- 资讯科技/通讯

- 製造业

- 能源/公共事业

- 银行/金融服务

- 教育

- 其他最终用户产业

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第六章 竞争形势

- 公司简介

- Cisco Systems Inc.

- Juniper Networks Inc.

- IBM Corporation

- Hewlett Packard Enterprise Development LP

- SolarWinds Inc.

- Network Automation Inc.

- Micro Focus International PLC

- NetBrain Technologies Inc.

- Arista Networks Inc.

- Extreme Networks Inc.

- BMC Software Inc.

- Fujitsu Limited

- VMware Inc.+Saltstack

- Nuage Networks(NOKIA CORPORATION)

- Forward Networks Inc.

- AppViewX Inc.

第七章 投资分析

第八章市场的未来

The Network Automation Market size is estimated at USD 25.16 billion in 2024, and is expected to reach USD 60.59 billion by 2029, growing at a CAGR of 19.22% during the forecast period (2024-2029).

Public and private companies and government entities are requiring employees to work from home (WFH), putting an unforeseen strain on networking technologies and causing bandwidth and security concerns because of increased internet traffic, which is driving the Network Automation Market across the globe.

Key Highlights

- Enterprise networks are under pressure, with more users, devices, and applications relying on the network for essential connectivity to a broad range of endpoints. Organizations are increasingly interested in new network architectures and advanced management tools that leverage machine learning and artificial intelligence to create self-driving or autonomous networks. These advancements are also significantly changing the way enterprises rely on services from their partners and vendors.

- One of the most significant benefits of network automation is a lower operational expense. By eliminating tedious and manual processes through automated and orchestrated infrastructures, one not only extends the network's capabilities but also achieves a faster ROI.

- Automation also reduces errors and builds resiliency. In addition to automating manual tasks to minimize network errors, many solutions automatically respond to network errors without intervention, enhancing business resiliency and ensuring employees have access to the applications and data they need whenever they need it. Increased network automation levels help reduce complexity and are essential for businesses to keep up in the digital world.

- One of the main factors constraining the market's growth is certain firms' concern that automated solutions can overlook security issues or impose many network restrictions. Additionally, implementing automated systems or solutions forces an organization to hire professionals or train its current network teams, ultimately raising costs for the business.

- Automation plays an essential role in maintaining IT operations during the COVID-19 pandemic. According to the Verizon Network Report, April 22, the overall data volume across its networks increased by 19% compared to pre-COVID levels. While data usage remains elevated, the changes in how people use the network have stabilized. Verizon expects the user to continue at sustained higher levels in the future.

Network Automation Market Trends

The Virtual Network Segment is Expected to Hold a Major Market Share

- Network functions virtualization (NFV) and Software-defined networking (SDN) abstract the implementation of new network functions and decouple them from the hardware infrastructure and associated topological constraints, thus, making communications networks programmable and, as a result, much more flexible and agile.

- SDN and NFV are together seen as key technologies enabling the transformation of communication service providers to provide a lower-cost means to address market demands. The primary end users driving this market are telecom operators who need to achieve CAPEX reduction, improve efficiency, and offer new services. NFV has constantly been complementing SDN by virtualizing network services that run in dedicated appliances, such as deep packet inspection (DPI), firewalls, load balancers, and session border controllers (SBCs), so that these services can run on a single pool of computer hardware, yielding CAPEX and OPEX savings.

- Network virtualization and automation are beneficial for environments that experience unexpected usage surges. The automated network can accommodate these surges by automatically redirecting network traffic to servers in less impacted areas of the network.

- Companies are resuming to scale their virtualized environments past simple virtual server deployment. They are now deploying virtual disaster recovery and virtual support for dynamic workloads and private cloud infrastructure. In doing so, they encounter unprecedented rates of change and growing complexity in the physical and logical network.

- Several open-source projects are dedicated to establishing network automation standards through virtualization. For instance, the European Telecommunications Standards Institute (ETSI) Industry Specification Group (ISG) for NFV Management and Orchestration (MANO) is focused on the management and orchestration of network resources in cloud-based data centers. These standards will enable better and more efficient communication between SDN and NFV platforms.

- Microsoft's Azure Virtual Network (VNet) is the fundamental building block for Azure's private network. VNet permits many types of Azure resources, such as Azure Virtual Machines (VM), to interact with each other securely, the internet, and on-premises networks. VNet is comparable to a traditional network that would work in the data center but brings additional benefits to Azure's infrastructure, such as scale, availability, and isolation.

Europe to Account for a Significant Market Share

- The European region holds a significant share in network automation due to the rapid expansion of the area and the presence of market players such as Microfocus International PLC, Nokia Communications, Ericsson, and Entuity Network Management.

- In Europe, the adoption of software-defined networking (SDN) and network function virtualization (NFV) technologies is increasing daily. These factors rapidly change how large enterprises build their wide area networks to meet these growing network requirements. Also, deploying several technologies in organizations is increasing the complexity of the IT infrastructure in these organizations, further increasing the demand for network automation solutions.

- 5G technology adds layers of technical and network architecture complexities. CSPs increasingly demand intelligent management systems to deal with the fast-increasing number of physical and virtual network events that may place heavy workloads on network operation centers. Cisco collaborated with Telefonica to implement network automation to simplify the service provider's operations in Spain in preparation for the 5G era. With this newly automated network powered by Cisco's Crosswork Network Automation suite, Telefonica may be able to provide improved operational insight and network health.

- In addition, Samsung Electronics and Vodafone UK announced the launch of the UK's first 5G Open RAN site, which is now handling active customer traffic. In Bath, the UK, this site is the first of Vodafone's scalable Open RAN network design in Europe, with over 2,500 more locations. The firms completed a 5G live video conversation utilizing Samsung's 5G virtualized Radio Access Network (vRAN) to commemorate the deployment of their first site, which was the UK's first call on a commercial 5G Open RAN in January 2022.

Network Automation Industry Overview

The network automation market is slowly turning into a fragmented market. It is expected to witness a robust increase shortly, strongly driven by cloud trends and growing network traffic across various end-user industries. To maintain their foothold in the network automation landscape, the competitive strategy has been quite strong from the current market leaders, mainly driven by their acquisitions of various startups and solution vendors. Key players in the market are Cisco System Inc., Juniper Networks Inc., and IBM Corporation.

In December 2022, T-Mobile and Cisco announced introducing the highly flexible and distributed global cloud-native converged core gateway. The Un-carrier migrated all of its 5G and 4G traffic to the newly cloud-native core gateway, which immediately improved customer performance by more than 10% in both bandwidth and latency. T-Mobile can dramatically decrease operational life cycle management by using a fully automated convergent core gateway to streamline network tasks throughout the cloud, edge, and data centers.

In January 2022, Hewlett Packard Enterprise partnered with OPTAGE, a Japanese telecommunications provider that selected HPE 5G Core Stack for its testbed Local 5G network. OPTAGE has tested the viability of Local 5G networks to meet the business customer demands of various end-users.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Assessment of the Impact of COVID-19 on the Market

- 4.6 Market Drivers

- 4.6.1 Increasing Demand for Data Center Network

- 4.6.2 Rising Trend of Connected Devices

- 4.7 Market Restraints

- 4.7.1 Lack of Skilled Professional Across Industries

5 MARKET SEGMENTATION

- 5.1 Network Type

- 5.1.1 Physical

- 5.1.2 Virtual

- 5.1.3 Hybrid

- 5.2 Solution Type

- 5.2.1 Network Automation Tools

- 5.2.2 SD-WAN and Network Virtualization

- 5.2.3 Intent-based Networking

- 5.3 Service Type

- 5.3.1 Managed Service

- 5.3.2 Professional Service

- 5.4 Deployment

- 5.4.1 Cloud

- 5.4.2 On-premise

- 5.4.3 Hybrid

- 5.5 End-user Industry

- 5.5.1 IT and Telecom

- 5.5.2 Manufacturing

- 5.5.3 Energy and Utility

- 5.5.4 Banking and Financial Services

- 5.5.5 Education

- 5.5.6 Other End-user Industries

- 5.6 Geography

- 5.6.1 North America

- 5.6.2 Europe

- 5.6.3 Asia-Pacific

- 5.6.4 Latin America

- 5.6.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cisco Systems Inc.

- 6.1.2 Juniper Networks Inc.

- 6.1.3 IBM Corporation

- 6.1.4 Hewlett Packard Enterprise Development LP

- 6.1.5 SolarWinds Inc.

- 6.1.6 Network Automation Inc.

- 6.1.7 Micro Focus International PLC

- 6.1.8 NetBrain Technologies Inc.

- 6.1.9 Arista Networks Inc.

- 6.1.10 Extreme Networks Inc.

- 6.1.11 BMC Software Inc.

- 6.1.12 Fujitsu Limited

- 6.1.13 VMware Inc. + Saltstack

- 6.1.14 Nuage Networks (NOKIA CORPORATION)

- 6.1.15 Forward Networks Inc.

- 6.1.16 AppViewX Inc.

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

2024 年意图式网路(IBN) 全球市场报告

2024 年意图式网路(IBN) 全球市场报告 2024 网路自动化全球市场报告

2024 网路自动化全球市场报告 5G端到端核心网路的自动化和编配

5G端到端核心网路的自动化和编配 网路自动化:SON、RIC、SMO(2023 年 10 月)

网路自动化:SON、RIC、SMO(2023 年 10 月) 中低压电网自动化市场:按组件、应用和最终用户划分 - 2023-2030 年全球预测

中低压电网自动化市场:按组件、应用和最终用户划分 - 2023-2030 年全球预测 IBN(基于意图的网路)市场规模、份额和趋势分析报告:2023-2030 年按组件、功能、部署、公司规模、行业、地区和细分市场进行的预测

IBN(基于意图的网路)市场规模、份额和趋势分析报告:2023-2030 年按组件、功能、部署、公司规模、行业、地区和细分市场进行的预测 全球网路自动化市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势和预测

全球网路自动化市场研究报告 - 2023 年至 2030 年产业分析、规模、份额、成长、趋势和预测 意图式网路市场:提供服务类别,各引进形态,各组织规模,各用途(网路自动化&编配,政策实施&保全,网路监视&分析),各终端用户,各地区-2030年前的世界预测

意图式网路市场:提供服务类别,各引进形态,各组织规模,各用途(网路自动化&编配,政策实施&保全,网路监视&分析),各终端用户,各地区-2030年前的世界预测 网路·自动化的全球市场

网路·自动化的全球市场 到 2030 年基于意图的网路市场预测 - 按产品、部署类型、组织规模、最终用户和区域进行的全球分析

到 2030 年基于意图的网路市场预测 - 按产品、部署类型、组织规模、最终用户和区域进行的全球分析