|

市场调查报告书

商品编码

1444512

柠檬酸:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Citric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

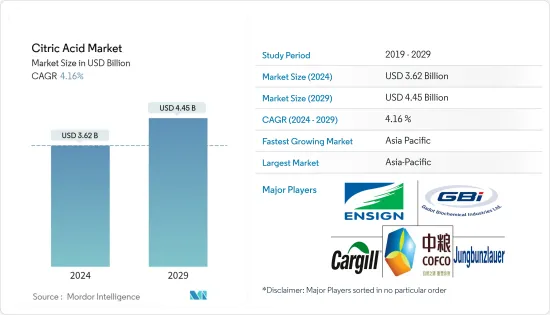

2024年柠檬酸市场规模预计为36.2亿美元,预计到2029年将达到44.5亿美元,在预测期内(2024-2029年)复合年增长率为4.16%增长。

主要亮点

- 柠檬酸的多功能特性使其成为多种行业(包括食品和非食品行业)的宝贵成分。它用作酸味剂、防腐剂、抗氧化剂、缓衝剂和粘合剂。液体和型态柠檬酸的应用涵盖食品和饮料、製药和个人护理等多个领域。在食品中,柠檬酸作为添加剂添加以增强酸度、酸味和风味。此外,柠檬酸的存在抑制微生物的生长,延长食品的保质期并增加对柠檬酸的需求。

- 柠檬酸在药品和营养补充中的受欢迎程度在全球食品增加。它可用于帮助保存和稳定药物中的活性成分,还可以增强咀嚼片和糖浆药物的味道。柠檬酸还可以增加镁和钙等矿物质补充品的吸收。

- 此外,消费者越来越要求从天然来源提取柠檬酸,因为他们更喜欢产品中的纯素来源。这一趋势促使市场相关人员专注于不断推出具有改进的应用功能和高品质标准的新产品。因此,柠檬酸市场预计在未来几年将显着成长。

柠檬酸市场趋势

对洁净标示和天然/有机成分的需求增加

- 随着政府和各种研究计划的禁令和限制的出台,消费者越来越意识到合成食品添加剂对健康的负面影响。这些添加剂可能会导致健康问题,例如运动过度、肿瘤、皮疹、肾臟损伤、偏头痛、睡眠障碍、气喘和肠道健康状况不佳。因此,我们看到消费者转向天然添加剂,青睐清洁标籤和天然成分。

- 世界卫生组织 (WHO)、食品药物管理局(FDA)、欧洲食品安全局和印度食品安全和标准局 (FSSAI) 等政府机构已认识到合成成分的有害影响,并制定了安全指南..它在食品中的使用需要食品和饮料製造商的合规性。此外,为了解决食品安全问题,各个组织推出了意识计划和研究计划,以促进从植物源中提取的有机成分在食品和饮料产品中的使用。

- 例如,2022年,有机印度在印度发起了一项名为「#TowardsHealthyEating」的新宣传活动,旨在促进儿童健康的用餐习惯。因此,全球食品产业透过在食品开发过程中更加重视这些方面来满足消费者的高需求。

2022年亚太地区将获得最大份额

- 中国是亚洲国家中最大的食品添加剂生产国和出口国之一,在食品和饮料行业使用的大多数原材料类别中占据全球原材料市场的近四分之三。中国是柠檬酸的重要出口国,因为其原料生产规模大,且供应成本低于其他地区。

- 此外,中国也是全球主要原料消费国之一,不断扩大的医药产业正在为中国柠檬酸市场创造成长机会。例如,2021年中国医药业务营业收益为3.3兆元(5,156亿美元),较去年与前一年同期比较成长近20%。此外,以柠檬酸为成分的清洁剂、餐具清洁剂和除锈产品等家庭清洁剂产品的需求不断增长,进一步推动了中国市场的成长。

- 同样,在日本,本土的酸柑是继盐之后必不可少的调味料之一,在日本料理中常用作香料。由于日本对保健食品的需求量很大,製造商将天然柠檬酸添加到食品中,以安全、不含防腐剂和天然的方式销售其产品,从而增加了日本市场对保健食品的需求。我们正在因应日益增长的需求需求

- 日本是亚洲最富裕、最有文化的消费市场之一,青睐易于理解的标籤检视,以更好地了解产品配方中使用的成分,而日本食品製造商可以使用天然来源的柠檬酸,是日本食品製造商的理想选择。

柠檬酸产业概况

全球柠檬酸市场竞争激烈且分散,主要企业包括阿彻丹尼尔斯米德兰(ADM)、嘉吉公司、Jungbunzlauer公司、中粮生化和加多生化工业有限公司。由于持续的市场力量和其他因素,这些公司在市场上占据主导地位。为了获得竞争优势,该品牌专注于推出高品质和多功能性的新产品,在口味和高溶解度方面使产品与众不同。

公司也在研发(R&D)和行销方面进行投资,同时扩大分销管道以维持其市场地位。此外,我们还采取了竞争策略,投资开发生产柠檬酸原料的新一代技术,这使我们能够降低成本并提高产品的永续性。整体而言,市场参与者的定位取决于他们的创新能力和提供满足客户各种需求的优质产品的能力。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买方议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争公司之间敌对的强度

第五章市场区隔

- 形状

- 液体

- 无水的

- 目的

- 食品和饮料

- 麵包店

- 糖果零食

- 乳製品

- 饮料

- 其他食品和饮料

- 药品

- 个人护理

- 其他用途

- 食品和饮料

- 地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 西班牙

- 义大利

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲

- 北美洲

第六章 竞争形势

- 最采用的策略

- 市场占有率分析

- 公司简介

- Jungbunzlauer Suisse AG

- Cargill Incorporated

- Merck KGaA

- Gadot Biochemical Industries

- Archer Daniels Midland Company

- Foodchem International Corporation

- Cofco Biochemical

- Posy Pharmachem Pvt Ltd

- Hawkins Pharmaceutical Group

- Saudi Bio-Acids Company

第七章市场机会与未来趋势

The Citric Acid Market size is estimated at USD 3.62 billion in 2024, and is expected to reach USD 4.45 billion by 2029, growing at a CAGR of 4.16% during the forecast period (2024-2029).

Key Highlights

- The versatile nature of citric acid makes it a valuable component in various industries, including food and non-food sectors. It is utilized as an acidulant, preservative, antioxidant, buffering, and binding agent. The applications of citric acid, in both liquid and anhydrous forms, span across different domains, such as food and beverages, pharmaceuticals, personal care, and more. In food products, citric acid is added as an additive to intensify sourness, tartness, and flavor. Moreover, its inclusion suppresses microbial growth, thereby increasing the shelf life of food products and driving the demand for citric acid.

- The popularity of citric acid in medicines and dietary supplements is on the rise globally. Its use helps preserve and stabilize the active ingredients in medicines and can also enhance the taste of chewable and syrup-based medications. Citric acid is also known to boost the absorption of mineral supplements like magnesium and calcium.

- Moreover, consumers are increasingly demanding citric acid extraction from natural sources as they prefer vegan sources for their products. This trend has led market players to focus on continuously launching new products with improved application capabilities and high-quality standards. As a result, the market for citric acid is expected to grow significantly in the coming years.

Citric Acid Market Trends

Increasing Demand for Clean-Label and Natural/Organic Ingredients

- With the introduction of bans and limits by governments and various research projects, consumers are increasingly becoming aware of the adverse health effects of synthetic food additives. These additives can lead to health issues such as hyperkinesia, tumors, skin rashes, kidney damage, migraine, sleep disturbance, asthma, and ill-gut health. As a result, there has been a shift towards natural additives and a preference for clean labels and natural ingredients among consumers.

- Government authorities such as the World Health Organization (WHO), Food and Drug Administration (FDA), European Food Safety Authority, and Food Safety and Standards Authority of India (FSSAI) have recognized the hazardous effects of synthetic ingredients and have laid down guidelines for their use in food products, which food and beverage manufacturers must comply with. Furthermore, various organizations have launched awareness programs and research projects promoting the use of organic ingredients extracted from plant sources in food and beverage products to address concerns regarding food safety.

- For instance, Organic India launched a new campaign in India in 2022 called '#TowardsHealthyEating,' with the aim of promoting healthy eating practices among children. As a result, the global food industry is responding to the high consumer demand by placing additional emphasis on these aspects during the food product development process.

Asia-Pacific Holds the Largest Share For the Year 2022

- China is one of the largest producers and exporters of food additives among Asian countries, accounting for nearly three-quarters of the global ingredients market in most ingredient categories used in the food and beverage industry. China produces ingredients on a large scale and supplies them at a lower cost than other regions, making it a significant exporter of citric acid.

- Moreover, China is also one of the major consumers of ingredients globally, and the expanding pharmaceutical industry is creating growth opportunities for the citric acid market in China. For instance, in 2021, the Chinese pharmaceutical business generated operating revenue of CNY 3.3 trillion (USD 515.6 billion), representing a growth of nearly 20% from the previous year. Additionally, the growing demand for household cleaners, including detergents, dish soaps, and rust remover products, that use citric acid as an ingredient is further driving the market growth in China.

- Similarly, in Japan, the native tart citrus is one of the country's most essential seasonings after salt and is commonly used as a flavoring agent in Japanese cuisine. With the high demand for healthy products in the country, manufacturers are incorporating naturally sourced citric acid in food items to sell their products as safe, preservative-free, and natural, meeting the increasing demand for healthy foods in the Japanese market.

- Japan is one of the most affluent and cultured consumer markets in Asia, with a preference for descriptive labeling that provides a better understanding of the ingredients used in the product formulation, making naturally sourced citric acid an ideal choice for food manufacturers in Japan.

Citric Acid Industry Overview

The global citric acid market is highly competitive and fragmented, with key players such as Archer Daniels Midland (ADM), Cargill Incorporated, Jungbunzlauer Company, Cofco Biochemical, and Gadot Biochemical Industries Ltd. These players dominate the market owing to factors such as the continuous launch of new products with high-quality and versatile applications. To gain a competitive advantage, brands are focusing on differentiating their products in terms of taste and high solubility.

Companies are also investing in research and development (R&D) and marketing while expanding their distribution channels to maintain their position in the market. Furthermore, they are adopting competitive strategies by investing in developing new-generation technologies to produce citric acid ingredients, which can help reduce costs and improve the product's sustainability. Overall, the market players' positioning is determined by their ability to innovate and provide high-quality products that cater to the varying demands of the customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Form

- 5.1.1 Liquid

- 5.1.2 Anhydrous

- 5.2 Application

- 5.2.1 Food and Beverage

- 5.2.1.1 Bakery

- 5.2.1.2 Confectionery

- 5.2.1.3 Dairy

- 5.2.1.4 Beverages

- 5.2.1.5 Other Foods and Beverages

- 5.2.2 Pharmaceutical

- 5.2.3 Personal Care

- 5.2.4 Other Applications

- 5.2.1 Food and Beverage

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Jungbunzlauer Suisse AG

- 6.3.2 Cargill Incorporated

- 6.3.3 Merck KGaA

- 6.3.4 Gadot Biochemical Industries

- 6.3.5 Archer Daniels Midland Company

- 6.3.6 Foodchem International Corporation

- 6.3.7 Cofco Biochemical

- 6.3.8 Posy Pharmachem Pvt Ltd

- 6.3.9 Hawkins Pharmaceutical Group

- 6.3.10 Saudi Bio-Acids Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

柠檬酸酯市场:按等级、按应用、按地区

柠檬酸酯市场:按等级、按应用、按地区 柠檬酸盐市场:按类型、形式、分销管道、应用分类 - 2025-2030 年全球预测

柠檬酸盐市场:按类型、形式、分销管道、应用分类 - 2025-2030 年全球预测 柠檬酸的全球市场机会与策略(至2033年)

柠檬酸的全球市场机会与策略(至2033年) 伊康酸市场:依衍生物、依应用分类 - 全球预测 2025-2030

伊康酸市场:依衍生物、依应用分类 - 全球预测 2025-2030 柠檬酸市场:按形式、应用和最终用户划分 - 2025-2030 年全球预测

柠檬酸市场:按形式、应用和最终用户划分 - 2025-2030 年全球预测 全球衣康酸市场规模(按衍生物、应用、地区、范围和预测)

全球衣康酸市场规模(按衍生物、应用、地区、范围和预测) 无水柠檬酸的全球市场,实际成果与预测(2019年~2030年)

无水柠檬酸的全球市场,实际成果与预测(2019年~2030年) 柠檬酸市场:依等级、依应用、依最终用途、按地区

柠檬酸市场:依等级、依应用、依最终用途、按地区 2024-2032 年柠檬酸市场报告(按应用(食品和饮料、家用洗涤剂和清洁剂、药品等)、形式(无水、液体)和地区)

2024-2032 年柠檬酸市场报告(按应用(食品和饮料、家用洗涤剂和清洁剂、药品等)、形式(无水、液体)和地区) 柠檬酸全球市场规模、份额和趋势分析报告:2023-2030 年按最终用途、产品和地区分類的展望和预测

柠檬酸全球市场规模、份额和趋势分析报告:2023-2030 年按最终用途、产品和地区分類的展望和预测