|

市场调查报告书

商品编码

1444828

网路安全保险 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Cybersecurity Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

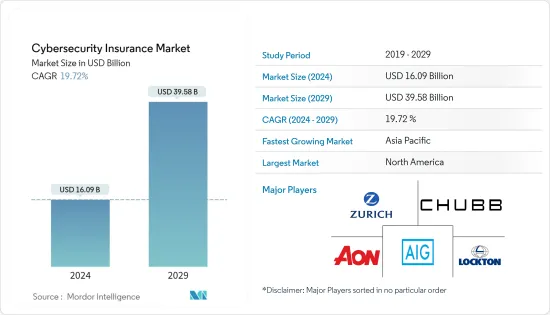

网路安全保险市场规模预计到 2024 年为 160.9 亿美元,预计到 2029 年将达到 395.8 亿美元,在预测期内(2024-2029 年)CAGR为 19.72%。

商业和社会中的数位化程度不断提高,云端、大数据、物联网和人工智慧 (AI) 的快速发展,以及万物互联的不断增强,增加了本已紧张的 IT 团队的工作量。

主要亮点

- IT 进步、通讯技术和智慧能源网格正在改变每个国家关键基础设施和商业网路的格局。然而,随着科技的快速发展,威胁也随之迅速发展。个人资料很有价值,这会促使网路犯罪分子实施犯罪,个人资讯将在暗网上出售,例如信用卡号码、身分、医疗记录等。这是导致对个人资料的需求增加的少数因素之一。网路安全。

- 云端运算是发展最快的最新技术之一,它消除了 IT 的传统界限,创造了新的市场,刺激了行动趋势,并推动了统一通讯的进步。各种技术利害关係人和组织正在转向新的保险模式,以减轻在现代网路安全环境中储存敏感资料的风险。

- 随着网路安全保险领域的不断成熟,保险公司将在评估中考虑更广泛的安全控制和技术。因此,组织资料的敏感度及其充分掩盖资料的能力将在确定整体风险方面发挥关键作用,从而推动微着色等新技术的采用。微分片技术将资料分解成小至个位数字节的碎片,然后将碎片分布到多个位置,以减少攻击面并消除资料敏感性。

- 网路保险保单和业务涵盖广泛的风险,保险公司并不总是就承保哪些损失事件达成一致。网路事件具有一些特征,使得编写全面的策略变得具有挑战性,例如有限的损失历史、预测未来事件时过去的资料不可靠,以及发生大规模攻击且跨公司和行业损失高度相关的可能性。此外,保险公司仍在研究网路攻击和物联网等新技术影响的精确标准。如果在没有明确定义危险以及不了解这些攻击如何影响保险公司的情况下发生大规模网路攻击,网路保险承保范围可能会无效,并使公司遭受相当大的损失。

- 这场大流行加速了数位工具的采用,这推动了对网路安全保险的更大需求。许多公司一直期待将保险与网路安全工具结合,以帮助企业减轻和管理网路风险。 2020 年,网路保险公司 Coalition 收购了 BinaryEdge,这是一个类似于 BitSight 和 Security Scorecard 的平台,用于搜寻网路并绘製组织的攻击面。该联盟已将来自 BinaryEdge 的数 TB资料与索赔和其他网路安全资料来源合併,以透过机器学习和自然语言处理来实现其风险评估流程。此外,由于新冠肺炎 (COVID-19) 疫情持续蔓延,世界各国已采取预防措施。随着学校关闭和社区被要求留在家里,多个组织找到了让员工在家工作的方法。这导致视讯通讯平台的采用率上升。过去6-8个月,包括Zoom在内的这些视讯通讯平台的新网域註册量迅速增加。

网路安全保险市场趋势

BFSI 细分市场预计将占有重要份额

- BFSI 产业是面临多次资料外洩和网路攻击的关键基础设施领域之一,因为该产业服务的客户群庞大且财务资讯受到威胁。网路犯罪分子正在优化无数邪恶的网路攻击,以瘫痪金融业,因为这是一种利润丰厚的营运模式,利润惊人,而且风险和可检测性相对较小。木马、ATM、勒索软体、资料外洩、机构入侵、资料窃取、财务外洩和其他威胁都是这些攻击的威胁环境的一部分,这进一步增加了 BFSI 领域对网路安全保险的需求。

- 例如,根据 Orange 的资料,该恶意软体是 2021 年 10 月至 2022 年 9 月期间金融和保险组织最常见的网路攻击形式。该攻击向量针对全球超过 40% 的组织。网路和应用程式异常位居第二,有 23% 的组织报告了此类网路攻击,其次是系统异常,占 20%。

- 网路安全保险日益成为银行和金融机构的重要组成部分。预计该行业在预测期内将占据重要的全球市场份额。它是受到高度监管和监管的行业之一,也容易发生身份欺诈,从而增加需求,从而进一步增加 BFSI 行业网路安全保险市场的需求。

- 例如,2021 年 10 月,联邦贸易委员会发布了一项修订后的规则,增加了金融机构为保护客户财务资料而必须实施的资料安全预防措施。近年来,由于大规模资料外洩和网路攻击,消费者遭受了巨大的痛苦,包括金钱损失、身分盗窃和其他形式的财务困境。联邦贸易委员会修订后的保障规则要求抵押贷款经纪人、汽车经销商和发薪日贷款机构等非银行金融公司建立、实施和维护强大的安全系统,以保护其客户资讯。政府政策将大大推动市场。

- 随着安全漏洞的增加,银行和金融机构应采用网路安全保险来保护客户的资料并防止经济损失。例如,2021 年 12 月,加密货币交易平台 Bitmart 发生巨大安全漏洞,导致骇客窃取约 2 亿美元资产。私钥被盗是安全漏洞的主要来源,影响了其以太坊和币安的两个创新链热钱包。

美国可望占据北美地区主要份额

- 美国被认为是世界上最重要的网路安全保险市场。该国还拥有大量在市场上运营的主要参与者,这是该国高份额的另一个原因。

- 美国的网路攻击正在迅速增加,并达到历史最高水平,这主要是由于该地区连网设备数量的迅速增加。在美国,消费者正在使用公有云,他们的许多行动应用程式都预先安装了他们的个人讯息,以方便银行、购物、通讯等。

- 据白宫经济顾问委员会称,有害网路活动每年给美国经济造成约 570 亿至 1,090 亿美元的损失。为了最大限度地减少网路攻击造成的损失,网路安全保险提供者提供的解决方案至关重要,并且该地区对网路安全保险的需求正在增加。

- 多年来,该地区发生了大量资料外洩事件。根据身分盗窃资源中心 2022 年发布的报告,已记录了 1,789 起资料外洩事件。大量的资料外洩事件鼓励各行业的组织选择网路安全保险,从而推动市场的成长。

- 美国政府签署法律成立网路安全和基础设施安全局(CISA),以加强对网路攻击的防御。它与联邦政府合作提供网路安全工具、事件回应服务和评估能力,以保护支援合作伙伴部门和机构基本运作的政府网路。因此,它将为新公司和现有公司投资专为该行业设计的合适网路安全套件开闢新途径。

网路安全保险产业概况

网路安全保险市场得到适度整合,重要参与者提供卓越的技术并透过现有的分销管道促进成长。这些技术领导者正在投资创新、合併、收购和合作伙伴关係活动,以保持市场竞争优势。

- 2023 年 2 月 - CloudCover Re 与保险经纪公司 Hylant Global Captive Solutions (Hylant) 合作推出 CloudCover CyberCell,这是一项网路安全「租用自保」保险计划。该计划可供协会、亲和团体和大型企业使用,允许用户以可管理的成本为自我保险的网路风险提供资金。这减少了网路攻击的潜在责任,并有助于为公司创造更可观的收入,因为他们可以以更低的成本和更广泛的覆盖范围提供网路保险。

- 2022 年 11 月 - 网路安全公司 Agilicus 与领先的普通保险管理机构之一 Ridge Canada Cyber Solutions Inc.(RCCS) 合作,协助加拿大中小企业 (SMB) 获得网路安全保险资格。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争激烈程度

- 行业指南和政策

- 评估 COVID-19 对市场的影响

第 5 章:市场动态

- 市场驱动因素

- 越来越多地采用基于云端的服务

- 资料安全漏洞不断增加

- 市场限制

- 网路保险实施难度高、成本高

第 6 章:市场细分

- 组织规模

- 中小企业 (SME)

- 大型企业

- 最终用户产业

- 卫生保健

- 零售

- BFSI

- 资讯科技和电信

- 製造业

- 其他最终用户产业

- 地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 欧洲其他地区

- 亚太

- 印度

- 中国

- 日本

- 新加坡

- 亚太其他地区

- 世界其他地区

- 北美洲

第 7 章:竞争格局

- 公司简介

- American International Group Inc.

- Zurich Insurance Co. Ltd

- Aon PLC

- Lockton Companies Inc.

- The Chubb Corporation

- AXA XL

- Berkshire Hathaway Inc.

- Insureon

- Security Scorecard Inc.

- Allianz Global Corporate & Specialty (AGCS)

- Munich Re Group

第 8 章:投资分析

第 9 章:市场机会与未来趋势

The Cybersecurity Insurance Market size is estimated at USD 16.09 billion in 2024, and is expected to reach USD 39.58 billion by 2029, growing at a CAGR of 19.72% during the forecast period (2024-2029).

Increasing digitalization and rapid development in the cloud, Big Data, IoT, and artificial intelligence (AI) in business and society and the growing connectivity of everything have increased the workload of already strained IT teams.

Key Highlights

- IT advances, communication technologies, and the smart energy grid are changing the landscape of all every country's critical infrastructure and business networks. However, with rapidly evolving technology comes rapidly advancing threats. Personal data is valuable, which prompts cybercriminals to commit crimes, where personal information will be sold on the dark web, like a credit card number, identity, medical records, etc. It is among the few factors that have led to an increased demand for cybersecurity.

- Cloud computing is one of the most rapidly growing recent technologies, eliminating the traditional boundaries of IT, creating new markets, spurring the mobility trend, and enabling advances in unified communications. Various tech stakeholders and organizations are turning to new insurance models to mitigate the risks of storing sensitive data in the modern cybersecurity landscape.

- As the cybersecurity insurance space continues to mature, insurers will consider a broader range of security controls and technologies in their assessments. Hence, the sensitivity level of an organization's data and its ability to adequately obscure it will play a key role in determining the overall risk, which is driving the adoption of new technologies like micro shading. Microsharding technology breaks data into fragments that can be as small as single-digit bytes before polluting and distributing shards to multiple locations to reduce the attack surface and eliminate data sensitivity.

- Cyber insurance policies and businesses cover a wide range of risks, and insurers do not always agree on which loss events are covered. Cyber events have characteristics that make it challenging to write comprehensive policies, such as limited loss history, the unreliability of past data when predicting future events, and the possibility of a large-scale attack with highly correlated losses across companies and industries. Furthermore, insurers are still working on precise and accurate criteria for cyberattacks and the impact of new technologies like the Internet of Things. Cyber insurance coverage could be ineffective and expose firms to considerable damage if big cyberattacks occur without well-defined dangers and an understanding of how they affect insurers.

- The pandemic accelerated the adoption of digital tools, which has driven a greater need for cybersecurity insurance coverage. Various companies have been looking forward to combining insurance with cybersecurity tools to help businesses mitigate and manage cyber risk. In 2020, Coalition, a cyber insurance company, acquired BinaryEdge, a platform akin to BitSight and Security Scorecard that searches the internet and maps an organization's attack surface. The Coalition has merged terabytes of data from BinaryEdge with claims and other cybersecurity data sources to enable its risk evaluation process with machine learning and natural language processing. Further, due to the ongoing COVID-19 pandemic, countries worldwide have implemented preventive measures. With schools being closed and communities being asked to stay at home, multiple organizations found a way to enable employees to work from their homes. This resulted in a rise in the adoption of video communication platforms. In the past 6-8 months, the new domain registration on these video communication platforms, including Zoom, rapidly increased.

Cybersecurity Insurance Market Trends

The BFSI Segment is Estimated to Hold a Significant Share

- The BFSI industry is one of the critical infrastructure segments facing multiple data breaches and cyberattacks, owing to the massive client base that the sector serves and the financial information at stake. Cybercriminals are optimizing myriad diabolical cyberattacks to immobilize the financial industry since it is a highly lucrative operating model with amazing profits and the bonus of relatively little risk and detectability. Trojans, ATMs, ransomware, data breaches, institutional invasion, data thefts, fiscal breaches, and other threats are all part of the threat environment for these attacks, which further necessitated the demand for cybersecurity insurance in the BFSI sector.

- For instance, according to the data from Orange, the malware was the most frequent form of cyber attack in financial and insurance organizations between October 2021 and September 2022. The attack vector targeted over 40% of the world's organizations. Network and application anomalies came in second, with 23% of organizations reporting such cyberattacks, followed by System anomalies with 20%.

- Cybersecurity Insurance is increasingly becoming a vital part of banking and financial institutions. The industry is expected to command a significant global market share during the forecast period. It is one of the highly regulated, governed industries and is also prone to identity frauds that augment demand, thus further proliferating the demand for the cybersecurity insurance market in the BFSI sector.

- For instance, in October 2021, the Federal Trade Commission issued an amended rule that increases the data security precautions financial institutions must implement to secure their clients' financial data. In recent years, consumers have suffered enormous suffering due to massive data breaches and cyberattacks, including monetary loss, identity theft, and other forms of financial misery. The revised Safeguards Rule from the Federal Trade Commission requires non-banking financial firms, such as mortgage brokers, car dealers, and payday lenders, to establish, implement, and maintain a robust security system to protect their clients' information. Government policies will significantly drive the market.

- With increased security breaches, banks and financial institutes should adopt cybersecurity insurance to safeguard their customers' data and prevent economic losses. For instance, in December 2021, a huge security breach at Bitmart, a crypto trading platform, resulted in hackers removing about USD 200 million in assets. A stolen private key was the primary source of the security compromise, which affected two of its Ethereum and Binance innovative chain hot wallets.

The United States is Expected to Hold the Major Share in the North American Region

- The United States is considered the world's most prominent cybersecurity insurance market. The country is also home to a significant number of key players operating in the market, which is another reason for the country's high share.

- Cyberattacks in the United States are rising rapidly and have reached an all-time high, primarily owing to the rapidly increasing number of connected devices in the region. In the United States, consumers are using public clouds, and many of their mobile applications are preloaded with their personal information for the convenience of banking, shopping, communication, etc.

- According to the White House Council of Economic Advisers, the US economy loses approximately USD 57 billion to USD 109 billion per year to harmful cyber activity. To minimize this loss due to cyber attacks, the solutions offered by cyber security insurance providers are essential, and the demand for cyber security insurance is increasing in the region.

- The region has been witnessing a significant number of data breaches over the years. According to the report published in 2022 by the Identity Theft Resource Center, 1,789 data breach incidents have been recorded. The high number of data breaches encourages organizations across various industries to opt for cybersecurity insurance, driving the market's growth.

- The United States government signed the law to establish Cybersecurity and Infrastructure Security Agency (CISA) to enhance the defense against cyber attacks. It works with the federal government to provide cybersecurity tools, incident response services, and assessment capabilities to safeguard the governmental networks that support essential operations of the partner departments and agencies. As a result, it will open new avenues for the new and existing companies to invest in suitable cyber security suite designed for this industry.

Cybersecurity Insurance Industry Overview

The cybersecurity insurance market is moderately consolidated, with significant players offering superior technology and fostering growth through their existing distribution channels. These technology leaders are investing in innovations, mergers, acquisitions, and partnership activities to maintain a competitive edge in the market.

- February 2023 - CloudCover Re collaborated with insurance brokerage Hylant Global Captive Solutions (Hylant) to launch CloudCover CyberCell, a cybersecurity 'rent-a-captive' insurance program. Available to associations, affinity groups, and large enterprises, the program allows users to finance self-insured cyber risks at a manageable cost. This reduces the potential liability of cyber attacks and facilitates more significant revenue generation for companies, as they can provide cyber insurance at a lower cost and broader coverage.

- November 2022 - Agilicus, a cybersecurity firm, and Ridge Canada Cyber Solutions Inc.(RCCS), one of the leading managing general insurance agencies, collaborated to assist Canadian small to midsize businesses (SMBs) qualify for and obtain cybersecurity insurance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Guidelines and Policies

- 4.5 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Cloud-based Services

- 5.1.2 Rising Data Security Breaches

- 5.2 Market Restraints

- 5.2.1 Difficulties in Implementing Cyber Insurance and High Costs

6 MARKET SEGMENTATION

- 6.1 Organization Size

- 6.1.1 Small and Medium Enterprises (SMEs)

- 6.1.2 Large Enterprises

- 6.2 End-user Industry

- 6.2.1 Healthcare

- 6.2.2 Retail

- 6.2.3 BFSI

- 6.2.4 IT and Telecom

- 6.2.5 Manufacturing

- 6.2.6 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 Germany

- 6.3.2.2 United Kingdom

- 6.3.2.3 France

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 India

- 6.3.3.2 China

- 6.3.3.3 Japan

- 6.3.3.4 Singapore

- 6.3.3.5 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 American International Group Inc.

- 7.1.2 Zurich Insurance Co. Ltd

- 7.1.3 Aon PLC

- 7.1.4 Lockton Companies Inc.

- 7.1.5 The Chubb Corporation

- 7.1.6 AXA XL

- 7.1.7 Berkshire Hathaway Inc.

- 7.1.8 Insureon

- 7.1.9 Security Scorecard Inc.

- 7.1.10 Allianz Global Corporate & Specialty (AGCS)

- 7.1.11 Munich Re Group

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

网路安全保险市场:保险风险范围、产品、合规要求、保险类型、组织规模和最终用户 - 2025-2030 年全球预测

网路安全保险市场:保险风险范围、产品、合规要求、保险类型、组织规模和最终用户 - 2025-2030 年全球预测 全球网路安全保险市场(按组成部分、覆盖范围、公司规模、产业、地区(北美、欧洲、亚太地区、拉丁美洲、中东/非洲)):趋势分析、竞争格局、未来预测(2019年~2030年)

全球网路安全保险市场(按组成部分、覆盖范围、公司规模、产业、地区(北美、欧洲、亚太地区、拉丁美洲、中东/非洲)):趋势分析、竞争格局、未来预测(2019年~2030年) 网路安全保险市场规模、份额和成长分析:按产品、按承保范围、按保险类型、按合规要求、按最终用户、按地区 - 行业预测,2024-2031 年

网路安全保险市场规模、份额和成长分析:按产品、按承保范围、按保险类型、按合规要求、按最终用户、按地区 - 行业预测,2024-2031 年 全球安全保障市场规模、份额、成长分析,按组件(软体、服务(咨询))、部署模式(本地、基于云端)、应用程式(网路安全、应用程式安全)- 2024-2031 年产业预测

全球安全保障市场规模、份额、成长分析,按组件(软体、服务(咨询))、部署模式(本地、基于云端)、应用程式(网路安全、应用程式安全)- 2024-2031 年产业预测 网路安全保险市场,按保险类型,按承保类型,按企业规模,按最终用户,按地理位置

网路安全保险市场,按保险类型,按承保类型,按企业规模,按最终用户,按地理位置 网路安全保险市场报告:2030 年趋势、预测与竞争分析

网路安全保险市场报告:2030 年趋势、预测与竞争分析 2024 年网路安全保险全球市场报告

2024 年网路安全保险全球市场报告 全球网路安全保险市场报告

全球网路安全保险市场报告 网路安全保险市场规模- 按组成部分(解决方案、服务)、按企业规模(大型企业、中小企业)、按保险类型(打包、独立)、按承保类型(第一方、责任险)、最终用途和2023 年预测- 2032

网路安全保险市场规模- 按组成部分(解决方案、服务)、按企业规模(大型企业、中小企业)、按保险类型(打包、独立)、按承保类型(第一方、责任险)、最终用途和2023 年预测- 2032 全球网络安全保险市场(~2028):按组件(解决方案/服务)、类型(独立/套餐)、承保范围(数据洩露/网络责任)、合规性要求、最终用户(技术/保险)、地区

全球网络安全保险市场(~2028):按组件(解决方案/服务)、类型(独立/套餐)、承保范围(数据洩露/网络责任)、合规性要求、最终用户(技术/保险)、地区