|

市场调查报告书

商品编码

1445674

持续整合工具 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Continuous Integration Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

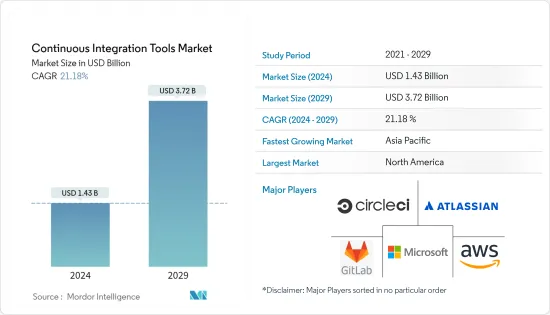

持续整合工具市场规模预计到 2024 年为 14.3 亿美元,预计到 2029 年将达到 37.2 亿美元,在预测期内(2024-2029 年)CAGR为 21.18%。

持续整合是一种用于製作软体的 DevOps 方法,开发人员定期将其程式码变更合併到共用储存库中。之后,对程式码运行自动建置和测试。

主要亮点

- 持续整合 (CI) 可协助开发人员在程式码中发现任何缺陷时立即提供报告,以便立即采取纠正措施。它是 DevOps 的重要组成部分,整合了众多 DevOps 阶段。测试阶段也是自动化的,并立即报告给使用者。

- 在持续整合中,软体在程式码提交后立即建置和测试。在拥有许多开发人员的大型专案中,提交是在一天中的不同时间进行的。每次提交都会建置并测试程式码。如果测试用例通过,则对建置进行部署测试。如果部署成功,程式码将被推送到生产环境。此提交、建置、测试和部署是一个连续的过程,因此称为「持续整合」。

- 市面上有各种 CI 工具,提供独特的功能。它们有开源版本和付费版本,根据用户的需求,可以选择最喜欢的版本。

- 儘管所有 CI 工具都旨在执行相同的基本功能,但从长远来看,选择最佳的 CI 工具变得至关重要。还可以选择多种工具来满足不同的需求,这取决于功能、使用的难易度和成本等因素。

- 根据JetBrains(软体公司)的调查,43%的软体开发人员将在2021年采用持续整合工具。由于CI工具很有用,预计未来几年市场将出现积极成长。

由于 COVID-19 大流行,一些企业的员工在家工作,开发人员采用 CI 工具的需求大幅增加。公司越来越多地将其应用程式转移到云端或基于云端的平台。此类事件需要及时使用 CI 工具。

持续整合工具市场趋势

零售及电商产业预计将呈现显着成长

- 数位转型使零售商能够为其消费者开闢多通路和全通路体验。数位化展示使客户可以根据自己的方便在各种平台上购物。

- COVID-19 大流行影响了零售和电子商务行业的消费者行为。零售商需要调整其实体业务以与数位系统整合。零售商需要提供从浏览到研究、选择、购买、退货和换货的简单、无缝的电子商务体验。疫情过后,消费者倾向于获得更好的数位购物体验。零售商需要确保其网站具有行动响应能力,提供整合解决方案,例如「线上购买、店内取货」(BOPIS),并跨装置和管道提供可靠、一致的数位体验。

- 这种消费者行为的变化迫使零售商将数位通路和电子商务纳入其营运中,随着数位资料在这种转变中大幅增加,对持续整合工具的需求也随之增加。

- 在零售业中,透过高效的供应链加快采用新技术变得更加复杂。持续整合预计将成为这些零售业务的接触点。持续整合有助于满足下一代客户日益增长的需求。随着版本的不断增加,它可以提高程式码品质、持续交付速度并降低 IT 成本。

- 持续整合模型旨在确保零售业的最终用户可以测试尽可能多的程式码类型,并将其整合到现有产品中,而不会出现任何重大效能问题。这使得电子商务网站有很好的机会透过比以往更快、更顺畅地推送更新和新功能来即时回应用户的需求和愿望。

北美预计将主导市场

- 北美是一个相当发达的市场,因为有几家新创公司致力于缓解机构的持续整合能力。目前,批量资料整合技术和工具在关键最终用户(例如 BFSI 或政府计划)中最有效地实施,以识别资料同步模式。

- 整体趋势有利于采用 CI 基础设施来推进 DevOps 和简化流程。对于早期采用者来说,一个特别的考虑因素是,如果任务是由公共基础设施驱动的,那么程式码必须公开可用,并在整个开发和部署过程中定期部署,确保公众可以存取程式码以进行品质保证和安全审计。其他相关第三方,并允许快速开发和修復流程。

- 一般来说,API 是现代数位生态系统的基础。该地区的团队旨在采用由自动化工具和整合安全测试功能支援的持续整合实践,从而显着促进 DevOps 的采用。本地供应商也一直在透过将 API 应用到他们的 CI 产品中来慢慢地最大化功能。此外,合作伙伴关係正在吸引市场上的重要供应商,这些供应商有能力进一步获取客户。

- 去年 2 月,美国 CI/CD 管线供应商 CircleCI 宣布与 AWS GovCloud 合作,利用 AWS 政府平台协助美国政府平台增强应用程式开发工作流程,实现应用程式开发工作流程现代化。此合作伙伴关係涉及与独立联邦机构(例如小型企业管理局 (SBA))或系统整合商(例如 AWS)的合作。

此外,该公司的成长势头良好,宣布完成 F 轮融资,融资 1 亿美元,使公司估值达到 17 亿美元。这取代了他们最近计划收购的荷兰发布编排平台 Vamp,从而使该公司能够最大限度地发挥其产品的潜力。

持续整合工具产业概述

由于新市场参与者的出现和现有市场参与者的扩张,持续整合工具市场的竞争格局预计在预测期内将出现碎片化。中小型解决方案提供商越来越多地筹集资金并试图顺利进入市场。

2022 年 11 月,Arista Networks 宣布推出具有 Arista 持续整合 (CI) 管道的全面网路自动化解决方案。 Arista CI 管道基于 Arista 的 EOS 网路资料湖 (NetDL),可协助企业客户实施现代网路操作范例。此策略可以减少营运时间和资金,为网路提供灵活的、数据驱动的流程来管理变更,从而使部署更快、更可靠。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设和市场定义

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争激烈程度

- 评估 COVID-19 对市场的影响

第 5 章:市场动态

- 市场驱动因素

- 越来越多地采用基于软体的业务流程

- 降低软体开发和成本优化复杂性的需求不断增加

- 市场挑战

- 缺乏部署 CI 工具的专业知识,尤其是中小型企业

第 6 章:市场细分

- 部署

- 本地部署

- 云

- 最终用户产业

- 资讯科技和电信

- 零售及电子商务

- 医疗保健和生命科学

- BFSI

- 媒体和娱乐

- 其他最终用户产业(教育、製造业)

- 地理

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第 7 章:竞争格局

- 公司简介

- Atlassian Corporation PLC

- Amazon Web Services Inc.

- Microsoft Corporation

- Circle Internet Services Inc.

- GitLab Inc.

- Buddy (BDY Sp zoo Sp K)

- Micro Focus International PLC

- JetBrains SRO

- CodeShip Inc.

- Thoughtworks Inc.

- IBM Corporation

- Travis CI GmbH

第 8 章:投资分析

第 9 章:市场的未来

The Continuous Integration Tools Market size is estimated at USD 1.43 billion in 2024, and is expected to reach USD 3.72 billion by 2029, growing at a CAGR of 21.18% during the forecast period (2024-2029).

Continuous integration is a DevOps method for making software in which developers regularly merge their code changes into a shared repository. After that, automated builds and tests are run on the code.

Key Highlights

- Continuous integration (CI) helps developers provide immediate reporting whenever any defect is identified in the code, so immediate corrective action is taken. It is an essential part of DevOps that integrates numerous DevOps stages. The testing phase is also automated and is instantly reported to the user.

- In continuous integration, the software is built and tested immediately after the code commit. In a larger project with many developers, commits are made at various times during the day. With each commit, code is built and tested. If the test case is passed, the build is tested for deployment. If the deployment is a success, the code is pushed to production. This commit, build, test, and deploy is a continuous process, hence the name "continuous integration."

- Various CI tools are available on the market, offering access to unique features. These have open-source and paid versions, and depending on the user's needs, the most preferred can be selected.

- Although all the CI tools are designed to perform the same basic functions, choosing the best CI tool becomes vital in the long run. Multiple tools may also be chosen to meet different needs, depending on things like features, how easy they are to use, and cost, among other things.

- According to a survey by JetBrains (a software company), 43% of software developers will employ continuous integration tools in 2021. Because CI tools are useful, the market is expected to grow positively over the next few years.

Due to the COVID-19 pandemic, several businesses had employees working from home, and the need to adopt CI tools for developers increased substantially. Companies increasingly moved their apps to the cloud or cloud-based platforms. Such incidents necessitated the use of CI tools in a timely manner.

Continuous Integration Tools Market Trends

Retail and E-commerce Industry Expected to Exhibit Significant Growth

- Digital transformation allows retailers to open up multi-channel and omnichannel experiences for their consumers. A digital presence allows customers to shop across various platforms according to their convenience.

- The COVID-19 pandemic impacted consumer behaviour in the retail and e-commerce industries. Retailers are required to adapt their brick-and-mortar operations to integrate with digital systems. Retailers need to deliver a simple and seamless e-commerce experience from browsing to researching, selecting, purchasing, returning and exchanging. Customers are inclined toward better digital shopping experiences after the pandemic. Retailers are required to ensure their sites are mobile-responsive, provide integrated solutions, such as "buy online, pick up in-store" (BOPIS), and deliver a reliable, consistent digital experience across devices and channels.

- This changed consumer behaviour is forcing retailers to incorporate digital channels and e-commerce into their operations, increasing the demand for continuous integration tools as digital data largely increases in this shift.

- Adopting new technologies at an increased rate with efficient supply chains becomes more complicated in the retail industry. Continuous integration is expected to become the touchpoint for these retail businesses. Continuous integration helps meet the requirements of increasing demands from next-generation customers. It offers improved code quality, continuous delivery speed, and IT cost reduction with the constant increase in releases.

- The continuous integration model is primed to ensure that retail sector end users can test as many types of codes as they want and integrate them within their existing product without any major performance issues. This gives e-commerce sites a great chance to respond to users' needs and wants in real time by pushing updates and new features more quickly and smoothly than ever before.

North America Expected to Dominate the Market

- North America is a considerably developed market, owing to the presence of several startups working toward easing the continuous integration capabilities of institutions. Bulk data integration techniques and tools are currently most efficiently implemented in critical end-users such as BFSI or government initiatives to identify data synchronization patterns.

- The general trend has been favourable toward the adoption of CI infrastructure to advance DevOps and streamline processes. A special consideration for early adopters has been that if a task is driven by public infrastructure, the code must consequently be publicly available and deployed periodically throughout the development and deployment process, ensuring access to the code for quality assurance and security audits by the public and other relevant third parties and allowing for rapid development and fixing processes.

- Generally, APIs are foundational for a modern digital ecosystem. The region's teams aim to adopt continuous integration practices buttressed by automation tools and integrated security testing capabilities, significantly boosting DevOps adoption. Local vendors have also been slowly maximizing capabilities by applying APIs to their CI offerings. Moreover, partnerships are engaging significant vendors in the market who are well-placed for further customer acquisition.

- In February last year, CircleCI, a CI/CD pipeline provider based in the USA, announced a collaboration with AWS GovCloud to assist in the augmentation of application development workflows for United States government platforms utilizing AWS's government platform to modernize their application development workflows. The partnership involves collaborating with an independent federal agency, such as the Small Business Administration (SBA), or systems integrators, such as AWS.

Moreover, the company's growth has been well placed with the announcement of a Series F funding round, raising USD 100 million and bringing the company's valuation to USD 1.7 billion. This was in lieu of their recently planned acquisition of Vamp, a Dutch release orchestration platform, allowing the company to maximize the potential of their offering.

Continuous Integration Tools Industry Overview

Because of the emergence of new market players and the expansion of existing market players, the competitive landscape of the Continuous Integration Tools Market is expected to fragment over the forecast period. Small and medium-sized solution providers are increasingly raising capital and attempting to enter the market smoothly.

In November 2022, Arista Networks announced a comprehensive network automation solution with the Arista Continuous Integration (CI) Pipeline. The Arista CI Pipeline, based on Arista's EOS Network Data Lake (NetDL), aids enterprise customers in implementing a contemporary network operating paradigm. With less operational time and money, this strategy gives the network a flexible, data-driven process for managing changes that makes deployment faster and more reliable.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Software-based Business Processes

- 5.1.2 Increasing Demand for Reduced Complexities in Software Development and Cost Optimization

- 5.2 Market Challenges

- 5.2.1 Lack of Expertise in Deployment of CI Tools Especially in the Small and Medium Enterprises

6 MARKET SEGMENTATION

- 6.1 Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 End-User Industry

- 6.2.1 IT and Telecom

- 6.2.2 Retail and E-commerce

- 6.2.3 Healthcare and Life Sciences

- 6.2.4 BFSI

- 6.2.5 Media and Entertainment

- 6.2.6 Other End-User Industries (Education, Manufacturing)

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Atlassian Corporation PLC

- 7.1.2 Amazon Web Services Inc.

- 7.1.3 Microsoft Corporation

- 7.1.4 Circle Internet Services Inc.

- 7.1.5 GitLab Inc.

- 7.1.6 Buddy (BDY Sp zoo Sp K)

- 7.1.7 Micro Focus International PLC

- 7.1.8 JetBrains SRO

- 7.1.9 CodeShip Inc.

- 7.1.10 Thoughtworks Inc.

- 7.1.11 IBM Corporation

- 7.1.12 Travis CI GmbH

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

持续交付:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

持续交付:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 持续交付市场:按产品、部署、组织规模和最终用户产业划分 - 2025-2030 年全球预测

持续交付市场:按产品、部署、组织规模和最终用户产业划分 - 2025-2030 年全球预测 持续整合工具市场:组件、部署类型、组织规模、最终用户产业 - 2025-2030 年全球预测

持续整合工具市场:组件、部署类型、组织规模、最终用户产业 - 2025-2030 年全球预测 持续交付市场、规模、占有率、趋势、行业分析报告:按部署、公司规模、最终用途、地区 - 市场预测,2024-2032 年

持续交付市场、规模、占有率、趋势、行业分析报告:按部署、公司规模、最终用途、地区 - 市场预测,2024-2032 年 持续交付市场规模、份额、趋势分析报告:按配置、按最终用途、按企业规模、按地区、细分市场预测,2024-2030 年

持续交付市场规模、份额、趋势分析报告:按配置、按最终用途、按企业规模、按地区、细分市场预测,2024-2030 年 2024 年至 2031 年持续整合工具市场类型、部署模式、组织规模与地区分布

2024 年至 2031 年持续整合工具市场类型、部署模式、组织规模与地区分布 持续整合 (CI) 工具市场报告:2030 年趋势、预测与竞争分析

持续整合 (CI) 工具市场报告:2030 年趋势、预测与竞争分析 2024 年持续整合工俱全球市场报告

2024 年持续整合工俱全球市场报告 持续交付 -市场占有率分析、产业趋势与统计、2024-2029 年成长预测

持续交付 -市场占有率分析、产业趋势与统计、2024-2029 年成长预测 2024 年持续交付全球市场报告

2024 年持续交付全球市场报告