|

市场调查报告书

商品编码

1445968

紧急与灾难应变 - 市场占有率分析、产业趋势与统计、成长预测(2024 - 2029)Emergency And Disaster Response - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

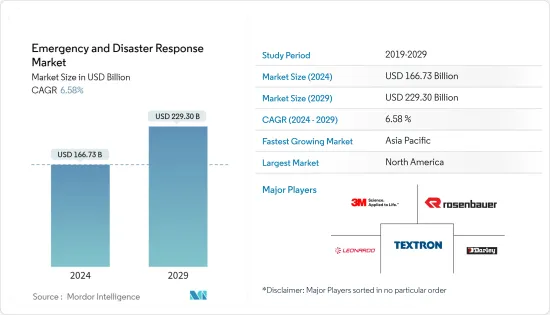

2024年紧急应变和灾难应变市场规模预计为1,667.3亿美元,预计到2029年将达到2,293亿美元,在预测期内(2024-2029年)CAGR为6.58%。

主要亮点

- COVID-19 大流行对紧急和灾难应变市场产生了重大影响。随着病例史无前例的激增,对医疗设备、个人防护装备和紧急物资的需求激增,对产业产能带来巨大压力。此外,疫情凸显了增强数位解决方案和资料分析的必要性,以改善危机时期的反应协调和资源分配,从而导致市场转向更多技术驱动的方法。

- 在一个不断变化的世界中,自然灾害、技术事故和不可预见的流行病的威胁不断存在,迅速有效地应对紧急情况和灾难的能力已成为政府、组织和个人最关心的问题。对准备和復原力的关注得到加强,推动了对创新解决方案的研发投资,以有效应对未来的紧急情况。全球自然和人为灾害事件的增加导致相关政府机构采购必要设备和响应车辆的数量增加。随着紧急情况变得更加复杂和多样化,传统方法可能不够用,需要不断适应和创新。这种不确定性可能使利害关係人难以预测并为所有潜在情况做好准备,从而进一步增加了市场有效应对能力的压力。

紧急和灾难应变市场趋势

预测期间内复合CAGR最高的土地板块

- 预测期内,土地市场的CAGR最高。各种公共和私人组织增加对陆地车辆的采购是市场的主要驱动力。陆地车辆可以就地驻扎,并且可以轻鬆、迅速地部署用于紧急减轻损失。为了增加陆上紧急应变车辆的可用性,当地灾害管理和紧急应变团队可以随时使用这些车辆。

- 因此,与飞行器相比,它们的采购量更高,而飞行器的总机队较少,因为它们只驻扎在拥有维护飞机所需基础设施的大城市。然而,随着大规模灾害的不断增多,用于消防和救灾物流等用途的飞行器的部署正在增加。

- 例如,2022 年 5 月,美国医疗响应公司获得了一份价值 12 亿美元的五年期新合同,为应对国家灾难和紧急情况提供医疗运输和支持。 AMR 是美国最大的地面医疗运输供应商,也是 FEMA 的主要 EMS 提供者。

北美在预测期内将主导市场份额

- 北美由于政府的高支出以及各种公共和私人灾难救援队不断采购相关设备和车辆而占据了市场份额。最近,严重的飓风和洪水袭击了美国,该国和加拿大在过去五年中发生了多起森林火灾。为了应对所有这些事件,该地区增加了救灾设备和车辆的采购。预计这些因素将在预测期内推动该地区的市场。

- 例如,1 月份,ICF 获得波多黎各住房部 (PRDOH) 授予的一份价值 5100 万美元的新合同,以支持该联邦的单户灾后恢復和减灾计划。合约为期三年,可选择再延长 24 个月。 ICF 将扩大对PRDOH 灾后恢復社区发展整笔拨款(CDBG-DR) 和减灾社区发展整笔拨款(CDBG-MIT) 赠款计划的实施支持,以修復和重建遭受飓风艾尔玛和玛丽亚损坏的房屋,并建造根据合约条款,抵御未来自然灾害的能力。

- 然而,作为世界上最大的灾害多发区之一的亚太地区预计将经历最高的市场成长率。世界上一些人口最多的国家的存在,紧急情况和灾害应变的延迟可能会急剧增加死亡率,迫使该地区政府透过采购必要的设备来为灾害和其他紧急情况做好准备。例如,菲律宾八打雁省政府宣布采购186辆全新日野200系列救援卡车,以增强紧急应变能力。同样,威廉森县正在寻求与 FloodMapp 签订新合同,彻底改变其洪水灾害准备、响应和恢復工作。 FloodMapp 是一家澳洲科技公司,为紧急管理人员提供即时洪水测绘,以减少对社区的影响。

紧急与灾难应变产业概述

市场是分散的,市场上的不同参与者将其产品提供给属于整体紧急和灾难应变市场的各种应用。 Rosenbauer International AG、Darley、Textron Inc.、3M 和 Leonardo SpA 是该市场的主要参与者。此外,每个国家都有许多本地企业,其产品组合各不相同,这加剧了市场的分散化。

因此,参与者的竞争仅限于他们提供的产品组合,且参与者不存在跨行业的竞争对手。在这种情况下,与面对大量提供不同产品的多行业参与者相比,参与者与相对较少的直接竞争对手池进行竞争。市场上的老牌企业可以透过合作或收购进入其他相关产业,从而灵活地扩大其产品范围。

例如,Rosenbauer 的 ET 系列如今在德国非常成功。目前,联邦内政部代表联邦民防和救灾办公室于 2021 年底订购的救灾集体消防车 (LF 20 KatS) 正在交付中。

额外的好处:

- Excel 格式的市场估算 (ME) 表

- 3 个月的分析师支持

目录

第 1 章:简介

- 研究假设

- 研究范围

第 2 章:研究方法

第 3 章:执行摘要

第 4 章:市场动态

- 市场概况

- 市场驱动因素

- 市场限制

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代产品的威胁

- 竞争激烈程度

第 5 章:市场细分

- 装置

- 威胁侦测设备

- 个人防护装备

- 医用器材

- 临时避难设备

- 登山装备

- 消防设备

- 其他设备

- 车载平台

- 土地

- 海洋

- 空降兵

- 地理

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 俄罗斯

- 欧洲其他地区

- 亚太

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 埃及

- 南非

- 中东和非洲其他地区

- 北美洲

第 6 章:竞争格局

- 供应商市占率

- 公司简介

- Rosenbauer International AG

- Darley

- Ziegler GmbH

- Magirus GmbH

- Emergency One Group

- Viking Air Ltd.

- Textron Inc.

- Leonardo SpA

- 3M

- Emergency Medical International

- Smiths Group plc

- REV Group, Inc.

- Honeywell International, Inc.

- Juvare, LLC

- Esri, Inc.

- Everbridge, Inc.

- Hexagon AB

第 7 章:市场机会与未来趋势

The Emergency And Disaster Response Market size is estimated at USD 166.73 billion in 2024, and is expected to reach USD 229.30 billion by 2029, growing at a CAGR of 6.58% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic had a significant impact on the emergence and disaster response market. With the unprecedented surge in cases, the demand for medical equipment, personal protective gear, and emergency supplies skyrocketed, putting immense pressure on the industry's capacity. Additionally, the pandemic highlighted the need for enhanced digital solutions and data analytics to improve response coordination and resource allocation in times of crisis, leading to a shift towards more technology-driven approaches in the market.

- In an ever-changing world, marked by the constant threat of natural calamities, technological mishaps, and unforeseen pandemics, the ability to respond swiftly and effectively to emergencies and disasters has become a paramount concern for governments, organizations, and individuals alike. The focus on preparedness and resilience has intensified, driving investment in research and development of innovative solutions to tackle future emergenies effectively. Increasing incidents of natural and anthropogenic hazards globally have led to a rise in the procurement of necessary equipment and response vehicles by the concerned government agencies. As emergencies become more complex and diverse, traditional approaches might prove insufficient, neccessitating continous adaptiona and innovation. This uncertainity can make it difficult for stakeholders to anticipate and prepare for all potential scenerios, adding further strain on the market's ability to respond effectively.

Emergency and Disaster Response Market Trends

Land Segment to Register the Highest CAGR during the Forecast Period

- The land segment recorded the highest CAGR in the market in the forecast period. Increasing procurement of land vehicles by various public and private organizations is acting as the main driver for the market. Land vehicles can be locally stationed and can be easily and promptly deployed for emergency damage alleviation purposes. To increase the availability of land-based emergency response vehicles, local disaster management and emergency response teams keep these vehicles at their disposal.

- Thus, their procurement volumes are higher compared to the aerial vehicles, whose overall fleet is less, as they are stationed only in bigger cities that possess the necessary infrastructure to maintain the aircraft. However, with the growing number of large-scale disasters, the deployment of aerial vehicles for purposes like firefighting and disaster relief logistics is increasing.

- For instance, in May 2022, American Medical Response was awarded a new USD 1.2 billion five-year contract to provide medical transport and support in response to national disasters and emergencies. AMR is the biggest provider of ground medical transportation in the US and FEMA's prime EMS provider.

North America to Dominate Market Share During the Forecast Period

- North America dominates the market share due to high spending from the government, in addition to the continual procurement of related equipment and vehicles by various public and private disaster rescue teams. Severe hurricanes and floods have hit the US in the recent past, and the country, along with Canada, has seen several forest fires in the past five years. In response to all these occurrences, the procurement of disaster response equipment and vehicles has increased in the region. These factors are expected to drive the market in the region during the forecast period.

- For instance, in January, ICF was awarded a new USD 51 million contract by the Puerto Rico Department of Housing (PRDOH) to support the commonwealth's single-family disaster recovery and mitigation programs. The contract is for three years with an option to extend for another 24 months. ICF will expand its implementation support of PRDOH's Community Development Block Grant for Disaster Recovery (CDBG-DR) and Community Development Block Grant for Mitigation (CDBG-MIT) grant programs to repair and rebuild homes damaged by hurricanes Irma and Maria, as well as build resilience against future natural disasters, under the terms of the contract.

- However, the Asia-Pacific region, which is one of the largest disaster-prone zones in the world, is projected to experience the highest growth rates in the market. The presence of some of the largest populated countries in the world, where a delay in emergency and disaster response can increase fatality rates drastically, is compelling the governments in the region to stay prepared for disasters and other emergencies by procuring the necessary equipment. For instance, the Provincial Government of Batangas (Philippines) has announced their purchase of 186 brand new Hino 200 Series Rescue trucks to enhance emergency response capabilities. Likewise, Williamson County is looking to revolutionize its flood disaster preparation, response and recovery with a new contract with FloodMapp. FloodMapp is an Australian technology company that provides real-time flood mapping for emergency managers to reduce the impacts on their communities.

Emergency and Disaster Response Industry Overview

The market is fragmented, with various players in the market supplying their products to various applications that fall under the overall emergency and disaster response market. Rosenbauer International AG, Darley, Textron Inc., 3M, and Leonardo S.p.A. are some of the major players in the market. In addition, the presence of many local players in each country with varying product portfolios is enhancing market fragmentation.

Thus, the competition for the players is restricted to the product portfolios they offer, and there are no cross-industry competitors for the players. In such cases, players compete with a relatively lower direct-competitor pool than facing a larger set of multi-industry players having different product offerings. Established players in the market gain the flexibility to expand their product reach by entering other related industries either by partnerships or acquisitions.

For instance, Rosenbauer is very successful in Germany with its ET series these days. Currently, the group firefighting vehicles for disaster relief (LF 20 KatS) are being delivered, which the Federal Ministry of the Interior ordered at the end of 2021, on behalf of the Federal Office of Civil Protection and Disaster Assistance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Equipment

- 5.1.1 Threat Detection Equipment

- 5.1.2 Personal Protection Gear

- 5.1.3 Medical Equipment

- 5.1.4 Temporary Shelter Equipment

- 5.1.5 Mountaineering Equipment

- 5.1.6 Fire Fighting Equipment

- 5.1.7 Other Equipment

- 5.2 Vehicle Platform

- 5.2.1 Land

- 5.2.2 Marine

- 5.2.3 Airborne

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rosenbauer International AG

- 6.2.2 Darley

- 6.2.3 Ziegler GmbH

- 6.2.4 Magirus GmbH

- 6.2.5 Emergency One Group

- 6.2.6 Viking Air Ltd.

- 6.2.7 Textron Inc.

- 6.2.8 Leonardo S.p.A

- 6.2.9 3M

- 6.2.10 Emergency Medical International

- 6.2.11 Smiths Group plc

- 6.2.12 REV Group, Inc.

- 6.2.13 Honeywell International, Inc.

- 6.2.14 Juvare, LLC

- 6.2.15 Esri, Inc.

- 6.2.16 Everbridge, Inc.

- 6.2.17 Hexagon AB

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

危机管理软体市场规模、份额和成长分析(按解决方案类型、部署类型、组织、产业垂直领域和地区划分)-2026-2033年产业预测

危机管理软体市场规模、份额和成长分析(按解决方案类型、部署类型、组织、产业垂直领域和地区划分)-2026-2033年产业预测 智慧疏散系统市场-2025-2030年预测

智慧疏散系统市场-2025-2030年预测 灾害復原服务:全球市场占有率和排名、总收入和需求预测(2025-2031年)

灾害復原服务:全球市场占有率和排名、总收入和需求预测(2025-2031年) 2025年全球商业復苏服务市场报告2025年全球危机管理软体市场报告2025年全球灾害应变与紧急管理人工智慧市场报告2025年全球灾害復原软体市场报告2025年全球灾害防备系统市场报告

2025年全球商业復苏服务市场报告2025年全球危机管理软体市场报告2025年全球灾害应变与紧急管理人工智慧市场报告2025年全球灾害復原软体市场报告2025年全球灾害防备系统市场报告 灾害准备系统市场(按类型、组件、应用、最终用户和部署)—2025-2030 年全球预测

灾害准备系统市场(按类型、组件、应用、最终用户和部署)—2025-2030 年全球预测 全球灾害防备系统市场

全球灾害防备系统市场