|

市场调查报告书

商品编码

1521428

5G 国防:市场占有率分析、产业趋势与统计、成长预测(2024-2029 年)5G In Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

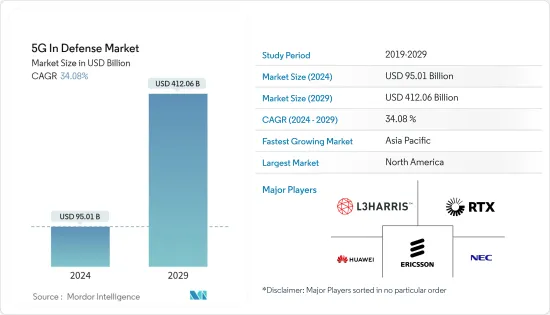

5G国防市场规模预计到2024年将达到950.1亿美元,预计到2029年将达到4120.6亿美元,在预测期内(2024-2029年)复合年增长率为34.08%。

主要亮点

- 对巨量资料的日益依赖预计将推动国防设备对 5G 网路的需求不断增长。越来越多地使用即时资料进行决策,提出了重要的资料收集要求。凭藉更快、更彻底的通讯,5G 网路能够更快地获取大量资料。透过5G网络,这种新的无线网路将实现从无人机和无人侦察机到指挥中心的即时资料传输,从而增强情境察觉和战术侦察能力。

- 国防计划的需求可能会推动国防市场的互通性。可以透过 5G 网路执行针对独特最终用户的端对端切片。切片可以定制,以提供自动驾驶汽车和卡车以及自动化处理技术等项目所需的系统性能。

- 然而,建造 5G 基础设施的高昂成本可能会阻碍预测期内的市场成长。

5G国防市场趋势

预测期内航空市场复合年增长率最高

- 由于无人机(UAV)和军用飞机采购的增加,机载领域预计将以最高的复合年增长率成长。 5G 与机载在国防市场的整合有可能显着增强能力并改变军事空中作战。

- 结合5G可以大大增强无人机和无人机的操作。高速资料传输可实现监视、侦察和战斗行动所需的即时视讯和感测器资料流。 2023年12月,《国防授权法案》(NDAA)宣布国防支出为8,860亿美元。它也呼吁美国国防部向军事基地部署5G开放RAN专用无线网路。

- 5G 的超低延迟还可以在每一毫秒都至关重要的环境中更好地远端控制无人机。 5G可以确保飞机资产与地面或海军部队之间的无缝资料集成,创建统一的作战图景并提高联合作战的效率。 5G 将促进多架无人机之间的通讯,并实现无人机集群作战。成群的此类无人机可以联合执行监视、电子战或攻击行动等任务。

亚太地区将在预测期内经历最高的成长

- 随着中国、韩国、日本等国家在部署5G网路方面取得重大进展,亚太地区5G技术正经历显着成长,导致对5G技术解决方案的需求激增。中国在无线网路市场的竞争中正在超越美国,特别是在 5G 技术方面。这些国家和其他国家5G网路的广泛建立正在推动5G测试市场的扩大。

- 例如,印度陆军希望沿其边境建设5G网络,以改善通讯,并拥有满足作战需求的高速资料网路。中国已经开始在实际控制线(LAC)沿线建造5G网络,以改善通讯。

- 印度陆军正在努力利用5G来支援战术性战场区域的行动。在此背景下,陆军通讯工程学院与印度理工学院马德拉斯分校于2022年4月签署了一份关于建立5G测试平台的谅解备忘录(MoU)。这些新兴市场的开拓将确保亚太地区国防5G市场的快速成长。

国防领域5G产业概况

国防领域的 5G 市场是半固定的,每个市场参与者都透过有吸引力的产品和有竞争力的定价策略来争取主导市场占有率。国防 5G 市场的主要市场参与企业包括 Telefonaktiebolaget LM Ericsson、华为技术公司、NEC 公司、L3Harris Technologies, Inc. 和 RTX Corporation。这些在该市场运营的领先公司正在采取各种策略,例如併购、研发投资、联盟、合作伙伴关係、区域扩张和新产品推出。

例如,2022 年 4 月,洛克希德马丁公司和英特尔公司签署了一份谅解备忘录,利用两家公司在技术和通讯方面的专业知识来提供创新的 5G 解决方案。该谅解备忘录扩大了两家公司之间的战略关係,使它们能够为美国国防部提供支援 5G 的硬体和软体解决方案。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 透过通讯基础设施

- 小型基地台

- 大型基地台

- 无线接取网路

- 透过核心网路技术

- 软体定义网路 (SDN)

- 雾计算(FC)

- 行动边缘运算(MEC)

- 网路功能虚拟(NFV)

- 按平台

- 土地

- 海军

- 空中的

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 拉丁美洲

- 巴西

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 以色列

- 其他中东和非洲

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- Huawei Technologies Co., Ltd.

- L3Harris Technologies, Inc.

- NEC Corporation

- Nokia Networks(Nokia Corporation)

- Qualcomm Technologies, Inc.

- RTX Corporation

- Samsung Electronics Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- THALES

- Wind River Systems, Inc.

第七章市场机会与未来趋势

The 5G In Defense Market size is estimated at USD 95.01 billion in 2024, and is expected to reach USD 412.06 billion by 2029, growing at a CAGR of 34.08% during the forecast period (2024-2029).

Key Highlights

- The growing dependence on big data is projected to drive the increased need for 5G networks of defense equipment. The increased use of real-time data for decisive decision-making has raised substantial data collections. With faster and more thorough communication, the 5G network will establish the capacity to take huge amounts of data more swiftly. Through its 5G network, this new wireless network would allow for real-time data transfer from unmanned aerial vehicles and surveillance drones to command centers, boosting situational awareness and tactical reconnaissance.

- Defense program demand will propel interoperability forward in the defense market. End-to-end slicing for unique end users can be carried out via 5G networks. Slices can be tailor-made to offer system performance needed by programs such as autonomous cars and trucks and automated process technology.

- However, the high costs involved in setting up 5G infrastructure might hinder the market growth during the forecast period.

5G In Defense Market Trends

Airborne Segment to Register the Highest CAGR During the Forecast Period

- The airborne segment is expected to grow with the highest CAGR owing to the rising procurement of unmanned aerial vehicles (UAVs) and military aircraft. 5G integration with airborne in the defense market has the potential to significantly enhance capabilities and transform military aerial operations.

- Incorporating 5G can greatly enhance UAV and drone operations. High-speed data transmission will allow real-time video and sensor data streaming, crucial for surveillance, reconnaissance, and combat operations. In December 2023, the National Defense Authorization Act (NDAA) announced that it would allocate USD 886 billion in defense spending. It also asked the US Defense Department to deploy 5G open RAN private wireless networks on military bases.

- The ultra-low latency of 5G can also support better remote control of UAVs in environments where every millisecond counts. 5G can ensure seamless data integration between airborne assets and ground or naval forces, creating a unified combat picture and improving joint operations' efficiency. 5G can facilitate communication between multiple drones, enabling swarm drone operations. Such drone swarms can collaboratively undertake tasks, be it for surveillance, electronic warfare, or even offensive operations.

Asia-Pacific to Witness the Highest Growth During the Forecast Period

- 5G technology in the Asia-Pacific region is experiencing significant growth due to countries such as China, South Korea, and Japan, which have advanced considerably in rolling out 5G networks, leading to a surge in demand for 5G technology solutions. China is outcompeting the US in the wireless network market, specifically with 5G technology. The widespread establishment of 5G networks in these and other countries in the area has propelled the expansion of the 5G testing market.

- For instance, the Indian Army wants to establish a 5G network along the border to improve communication and get a high-speed data network for operational requirements. China has already begun the operation of setting up a 5G network along the Line of Actual Control (LAC) for better communication.

- The Indian Army has been endeavoring to exploit 5G for supporting operations in the tactical battlefield area. In this context, in April 2022, a Memorandum of Understanding (MoU) for the establishment of a 5G testbed was signed between the Military College of Telecommunication Engineering and IIT Madras. Such developments will ensure speedy growth of the 5G defense market in Asia Pacific.

5G In Defense Industry Overview

The 5G in Defense Market is semi-consolidated, with the market players vying for a dominant market share through attractive offerings and competitive pricing strategies. Some of the key market participants in the 5G defense market include Telefonaktiebolaget LM Ericsson, Huawei Technologies Co., Ltd., NEC Corporation, L3Harris Technologies, Inc., and RTX Corporation. These major players operating in this market have adopted various strategies comprising M&A, investment in R&D, collaborations, partnerships, regional business expansion, and new product launches.

For instance, in April 2022, Lockheed Martin and Intel Corporation signed a memorandum of understanding to leverage their expertise in technology and communications to bring together innovative 5G-capable solutions. The memorandum of understanding (MoU) will expand the strategic relationship between the two companies to align 5G-enabled hardware and software solutions for the US Department of Defense.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Communication Infrastructure

- 5.1.1 Small Cell

- 5.1.2 Macro Cell

- 5.1.3 Radio Access Network

- 5.2 By Core Network Technology

- 5.2.1 Software-Defined Networking (SDN)

- 5.2.2 Fog Computing (FC)

- 5.2.3 Mobile Edge Computing (MEC)

- 5.2.4 Network Functions virtualization (NFV)

- 5.3 By Platform

- 5.3.1 Land

- 5.3.2 Naval

- 5.3.3 Airborne

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Israel

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Huawei Technologies Co., Ltd.

- 6.2.2 L3Harris Technologies, Inc.

- 6.2.3 NEC Corporation

- 6.2.4 Nokia Networks (Nokia Corporation)

- 6.2.5 Qualcomm Technologies, Inc.

- 6.2.6 RTX Corporation

- 6.2.7 Samsung Electronics Co., Ltd.

- 6.2.8 Telefonaktiebolaget LM Ericsson

- 6.2.9 THALES

- 6.2.10 Wind River Systems, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

欧洲的智慧型手机费用:追踪与分析 2025年

欧洲的智慧型手机费用:追踪与分析 2025年 非洲的智慧型手机费用:追踪与分析 2025年

非洲的智慧型手机费用:追踪与分析 2025年 5G Red Cap 技术市场规模、份额、成长分析(按组件、应用、部署模式、企业规模、最终用户和地区)-2025 年至 2032 年产业预测

5G Red Cap 技术市场规模、份额、成长分析(按组件、应用、部署模式、企业规模、最终用户和地区)-2025 年至 2032 年产业预测 5G的最佳化:网路切片和智慧天线的策略性协同效应

5G的最佳化:网路切片和智慧天线的策略性协同效应 2032 年自动化製造中的 5G 和连接:按组件、部署类型、公司规模、连接类型、技术整合、最终用户和地区进行的全球分析

2032 年自动化製造中的 5G 和连接:按组件、部署类型、公司规模、连接类型、技术整合、最终用户和地区进行的全球分析 4G 和 5G 市场按组件、网路技术、频谱频宽、频谱所有权、网路架构、部署类型、部署模式和最终用户划分 - 2025-2030 年全球预测5G地面电波非联网市场(按产品、位置、频宽、最终用户和应用)—2025-2030 年全球预测全端开发服务市场按服务类型、部署模式、技术堆迭、参与模式、组织规模和最终用户行业划分 - 全球预测,2025 年至 2030 年卫星地面电波网路市场(按组件、轨道、技术、频宽和最终用户划分)—2025-2030 年全球预测

4G 和 5G 市场按组件、网路技术、频谱频宽、频谱所有权、网路架构、部署类型、部署模式和最终用户划分 - 2025-2030 年全球预测5G地面电波非联网市场(按产品、位置、频宽、最终用户和应用)—2025-2030 年全球预测全端开发服务市场按服务类型、部署模式、技术堆迭、参与模式、组织规模和最终用户行业划分 - 全球预测,2025 年至 2030 年卫星地面电波网路市场(按组件、轨道、技术、频宽和最终用户划分)—2025-2030 年全球预测 全球石油和天然气领域的5G市场

全球石油和天然气领域的5G市场