|

市场调查报告书

商品编码

1521686

太空低温技术:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Space Cryogenics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

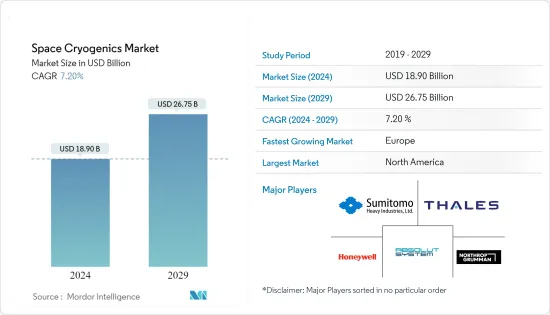

预计到 2024 年,太空低温技术市场规模将达到 189 亿美元,预计到 2029 年将达到 267.5 亿美元,在预测期内(2024-2029 年)复合年增长率为 7.20%。

太空低温技术市场的成长是由太空船上的操作日益简化所推动的。随着太空任务变得越来越复杂,对能够长期提供可靠性能的低温系统的需求不断增长。

低温技术的进步正在导致更强大、更有效率的低温系统的发展,这些系统可以承受恶劣的太空环境。空间应用中感测器和冷电子设备等低温设备的进步和开拓正在推动市场成长。

低温感测器和冷电子设备是受益于材料科学进步的设备。开发、测试和部署低温基础设施需要大量的财务投资,包括储存槽、隔热材料、传输系统和冷却机制。因此,低温设备所需的高营运成本和资本支出是阻碍太空低温市场成长的主要因素。

太空低温市场的趋势

在预测期内,空间科学任务部分将占据最高的市场占有率

由于在太空任务中越来越多地使用低温技术,预计太空科学任务部分将在预测期内占据最大的收益占有率。在全球范围内,航太机构在发射卫星、火箭等方面发挥领导作用。例如,2023年5月,印度太空研究组织(ISRO)使用具有低温上部级的GSLV火箭成功发射了第二代导航卫星。 NVS-01 透过提供准确、即时的导航来补充该国的区域导航系统。

2022年11月,美国太空总署NASA在佛罗里达州甘乃迪太空中心发射了Artemis-1任务。在升空过程中,核心级引擎在升空八分钟后关闭并与火箭的其余部分分离。此后,中低温推进级(ICPS)被用来推进猎户座太空船。猎户座太空船的四块太阳能板由美国太空总署部署。 Orion与ICPS分离并完成了「transluner注射」。目前它正在前往月球轨道的途中。预计此类发展将在可预见的几年内引领该领域。

欧洲将在预测期内经历最高的成长

在太空低温技术市场中,由于正在进行和计划中的太空倡议,预计欧洲在预测期内将呈现最高成长。例如,英国政府宣布2022年投资3,105万美元,由英国主导打造太空望远镜,用于研究系外行星。透过这笔资金,该国预计将接收 Ariel 的有效载荷模组、低温冷却器和光学地面支援设备,同时继续主导该任务的科学操作和资料处理。

2023年7月,法国议会核准了2024年至2030年的七年军费开支计画。该计划包括 67 亿美元的太空支出,比上一季成长 45%。 2023年9月,德国政府宣布了新的太空策略,制定了2030年太空旅行的目标和机会。

2023年10月,英国航太局和美国航太服务公司Axiom Space签署了初步协议,旨在将英国太空人送入轨道为期两週。英国的这项任务将得到欧洲太空总署的商业赞助和支持。因此,该地区太空产业活动的增加导致了对太空低温技术的需求增加,预计这将推动市场收益成长。

空间低温产业概况

太空低温技术市场整合,龙头企业市场占有率最高。主要市场参与企业包括泰雷兹、诺斯罗普·格鲁曼公司、Absolut System、住友重工有限公司和霍尼韦尔国际公司。

这些公司是低温技术的领导者和低温冷却器的供应商。公司正在投资研发低温系统,提供自动控制、远端监控和维护功能,帮助简化太空船操作并降低人为错误的风险。降低低温系统的复杂性并提高其易用性使太空船操作员能够专注于任务目标而不是复杂的系统管理。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行概述

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 按冷却方式分

- 高温冷却器

- 低温冷却器

- 按用途

- 地球观测

- 通讯应用

- 技术示范任务

- 低温电子学应用

- 按温度分类

- 120K以下

- 120 K

- 150K以上

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 俄罗斯

- 法国

- 欧洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 拉丁美洲

- 巴西

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 以色列

- 其他中东/非洲

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- THALES

- Absolut System

- Sumitomo Heavy Industries Ltd

- Air Liquide

- Oxford Instruments

- Parker Hannifin Corporation

- Honeywell International Inc.

- RICOR

- Creare

- Northrop Grumman Corporation

第七章 市场机会及未来趋势

The Space Cryogenics Market size is estimated at USD 18.90 billion in 2024, and is expected to reach USD 26.75 billion by 2029, growing at a CAGR of 7.20% during the forecast period (2024-2029).

The space cryogenics market growth can be attributed to the increasing simplicity of operations in onboard spacecraft. With space missions becoming more complex, the demand for cryogenic systems that can deliver reliable performance over extended periods is growing.

Advancements in cryogenic technologies are leading to the development of more robust and efficient cryogenic systems to withstand harsh space conditions. Advancements and developments in cryogenic devices, such as sensors and cold electronics in space-based applications, are driving market growth.

Cryogenic sensors and cold electronics are devices that benefit from the development of materials science. Substantial financial investments are required for the development, testing, and deployment of cryogenic infrastructure, which includes storage tanks, insulation, transfer systems, and cooling mechanisms. Hence, high operating expenses and capital expenditures required for cryogenic setups are major factors hindering the growth of the space cryogenics market.

Space Cryogenics Market Trends

The Space Science Missions Segment will Account for the Highest Market Share During the Forecast Period

The space science missions segment is expected to account for the largest share of revenue over the forecast period, owing to the increasing use of cryogenics in space missions. Globally, space organizations have been taking the initiative to launch satellites, rockets, and others. For instance, in May 2023, a second-generation navigation satellite that utilizes a GSLV rocket with a cryogenic upper stage was successfully launched by the Indian Space Research Organization (ISRO). The NVS-01 will supplement the country's regional navigation system by delivering precise and real-time navigation.

In November 2022, the American space agency, NASA, launched the Artemis-1 mission at Florida's Kennedy Space Center. During the launch, the core stage engines shut down eight minutes after liftoff and separated from the rest of the rocket. After this, the Interim Cryogenic Propulsion Stage (ICPS) was used to propel the Orion spacecraft. The four solar panels of the Orion spacecraft were deployed by NASA. Orion decoupled from the ICPS and completed 'translunar injection.' It is now traveling toward the lunar orbit. Such developments are expected to lead the segment during the forecasted years.

Europe will Witness the Highest Growth During the Forecast Period

In the space cryogenics market, Europe is projected to witness the highest growth as a result of the ongoing and planned space initiatives during the forecast period. For instance, to ensure that the United Kingdom leads the creation of a space telescope to study exoplanets, in 2022, the UK government announced an investment of USD 31.05 million. With this funding, the country is envisioned to continue leading the mission's scientific operations and data processing while also receiving the payload module, cryogenic cooler, and optical ground support equipment for Ariel.

In July 2023, the French parliament approved a seven-year military spending program for 2024-2030 that includes USD 6.7 billion for space programs, which is a 45% increase from the previous period. In September 2023, the German government presented a new Space Strategy and laid its goals and opportunities for space travel until 2030.

In October 2023, the UK Space Agency and a US spaceflight services company, Axiom Space, signed an initial agreement as they bid to send British astronauts into orbit for two weeks. The mission with the UK would be commercially sponsored and supported by the European Space Agency. Hence, increasing activities in the space industry in this region are leading to a rise in demand for space cryogenics, which is expected to drive growth in market revenue.

Space Cryogenics Industry Overview

The space cryogenics market is consolidated, with leading players having the highest market share. Some of the key market players include THALES, Northrop Grumman Corporation, Absolut System, Sumitomo Heavy Industries Ltd, and Honeywell International Inc.

These companies are leaders in cryogenic technology and suppliers of cryogenic coolers. Companies are investing in the R&D of cryogenic systems that offer automated controls, remote monitoring, and maintenance capabilities to help streamline spacecraft operations and reduce the risk of human error. By reducing the complexity of cryogenic systems and enhancing their ease of use, spacecraft operators can focus on mission objectives rather than intricate system management.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Cooling Type

- 5.1.1 High-Temperature Coolers

- 5.1.2 Low-Temperature Coolers

- 5.2 By Application

- 5.2.1 Earth Observation

- 5.2.2 Telecom Applications

- 5.2.3 Technology Demonstration Missions

- 5.2.4 Cryo-Electronics Applications

- 5.3 By Temperature

- 5.3.1 Less Than 120 K

- 5.3.2 120 K

- 5.3.3 More Than 150K

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Russia

- 5.4.2.4 France

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Israel

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 THALES

- 6.2.2 Absolut System

- 6.2.3 Sumitomo Heavy Industries Ltd

- 6.2.4 Air Liquide

- 6.2.5 Oxford Instruments

- 6.2.6 Parker Hannifin Corporation

- 6.2.7 Honeywell International Inc.

- 6.2.8 RICOR

- 6.2.9 Creare

- 6.2.10 Northrop Grumman Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

低温设备市场规模、份额、趋势分析报告:按产品、低温材料、应用、最终用途、地区和细分市场预测,2025 年至 2030 年

低温设备市场规模、份额、趋势分析报告:按产品、低温材料、应用、最终用途、地区和细分市场预测,2025 年至 2030 年 2032年低温气体市场预测:全球产品、应用与地区分析

2032年低温气体市场预测:全球产品、应用与地区分析 日本低温设备市场报告(按设备、冷媒、应用、最终用途产业和地区)2025-2033

日本低温设备市场报告(按设备、冷媒、应用、最终用途产业和地区)2025-2033 低温产品市场:按低温设备、低温气体、应用和最终用户划分-2025-2030 年全球预测低温气体市场规模、份额、趋势分析报告:产品、应用、地区、细分市场预测,2025-2030

低温产品市场:按低温设备、低温气体、应用和最终用户划分-2025-2030 年全球预测低温气体市场规模、份额、趋势分析报告:产品、应用、地区、细分市场预测,2025-2030 宇宙用极低温市场:现状分析与未来预测 (2024年~2032年)

宇宙用极低温市场:现状分析与未来预测 (2024年~2032年) 2025 年低温设备全球市场报告

2025 年低温设备全球市场报告 极低温设备的全球市场:产品类型 (阀门·坦克·汽化器·帮浦·其他)·不同地区的预测 (~2032年)极低温设备的全球市场的评估:不同设备,冷却剂,各用途,各系统,各最终用途产业,各地区,机会,预测(2018年~2032年)太空低温技术市场机会、成长驱动因素、产业趋势分析及 2025 年至 2034 年预测

极低温设备的全球市场:产品类型 (阀门·坦克·汽化器·帮浦·其他)·不同地区的预测 (~2032年)极低温设备的全球市场的评估:不同设备,冷却剂,各用途,各系统,各最终用途产业,各地区,机会,预测(2018年~2032年)太空低温技术市场机会、成长驱动因素、产业趋势分析及 2025 年至 2034 年预测