|

市场调查报告书

商品编码

1521691

自主潜水器:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Autonomous Underwater Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

根据预测,自主潜水器的市场规模到2024年将达到21.3亿美元,到2029年将达到54.5亿美元,在市场估算和预测期间(2024-2029年)复合年增长率为20.62%。

该市场受到自主水下机器人(AUV)在多个领域的广泛应用的推动,包括探勘和勘探、资源探勘、环境监测、国防和安全、基础设施检查和科学研究。

由于其稳定性、部署成本低、资料品质提高和卓越的导航演算法,AUV 的采用也在增加。这些好处使自主潜水器成为许多人的安全选择。例如,AUV 被部署在石油和天然气行业来绘製海底地图。它也被军方用于检查和识别目的。这为许多国家的商业和安全服务。

潜水技术预计将为製造公司带来有吸引力的商机。开拓具有卓越抗干扰能力的水下航行器的经济有效的通讯技术预计将显着推动市场成长。

然而,营运成本的增加和 AUV 营运绩效的不确定性可能会阻碍市场成长。

自主潜水器市场趋势

军事和国防占据很大的市场占有率

自主水下航行器(AUV)由于能够在水下环境中自主操作并收集有价值的资讯而被用于各种军事和国防应用。这些车辆为军队和国防部队提供了宝贵的水下作战能力,包括监视、侦察、反水雷措施和特种作战,从而增强了复杂和充满挑战的环境中的海上安全和情境察觉。

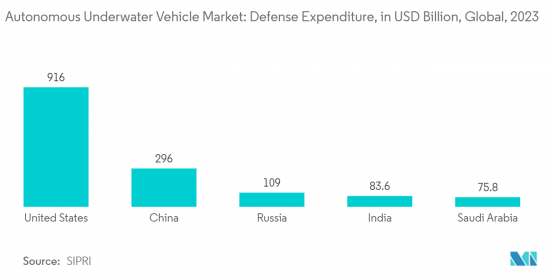

安全问题、对衝突地区的担忧和威胁导致国防支出大幅增加。斯德哥尔摩国际和平研究所(SIPRI)2024年4月发布的全球军费最新资料显示,2022年全球军费总额将实际成长6.8%,达到24,430亿美元。各国正利用尖端技术来保护其边界免受水下威胁。

根据国际商会国际海事局 (IMB) 年度海盗和武装抢劫报告,2023 年报告了 120 起海盗和武装抢劫船舶事件,而 2022 年为 115 起。此类威胁的增加引发了海上边界以外的安全问题。因此,上述因素预计将推动市场成长。

北美地区将在预测期内经历最高的成长

由于新兴市场的存在、美国对 AUV 的需求不断增长以及广泛的研究和开发,预计北美自动驾驶汽车市场将在预测期内呈现最高增长。

2024 年 2 月,美国选择 Anduril 及其 Dive 系列大型自主水下航行器 (AUV) 在竞争环境中进行分散式、远距、持久性水下感测和有效载荷输送原型。 Anduril 提供一系列支援人工智慧的 AUV,旨在执行各种国防和商业任务。

在印度-太平洋地区(特别是海上环境)紧张局势不断升级的情况下,美国国防部(DoD)正在大力投资自主系统的开发,以增强国家安全。例如,波音公司正在美国的资助下开发 Orca XLUUV。 2019年,该公司赢得了一份价值4300万美元的合同,根据波音公司的Echo Voyager设计建造四艘AUV。这些计划将于 2024 年完成。这些因素可能会刺激北美市场的成长。

自动潜水器产业概述

自动潜水器市场较为分散,参与者众多,既有老牌企业,也有新兴新兴企业。主要公司包括康斯伯格集团 ASA、通用动力公司、洛克希德马丁公司、波音公司和萨博公司。

这些参与者正在采取收购、联盟、业务扩张以及产品和技术发布等策略性倡议,以维持其在该市场的地位并获得竞争优势。例如,2022 年 7 月,Kongsberg Gruppen ASA 获得了几份 HUGIN AUV 的重要合约。除了对海洋机器人不断增长的需求外,该公司还宣称其广泛的产品组合使其能够满足新的应用需求。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 市场驱动因素

- 市场限制因素

- 波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 按类型

- 小尺寸

- 中等大小

- 大的

- 按用途

- 军事/国防

- 油和气

- 环保/监测

- 海洋学

- 考古/探勘

- 搜救行动

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 拉丁美洲

- 巴西

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 以色列

- 其他中东和非洲

- 北美洲

第六章 竞争状况

- 供应商市场占有率

- 公司简介

- The Boeing Company

- Kongsberg Gruppen ASA

- L3Harris Technologies Inc.

- Lockheed Martin Corporation

- SAAB AB

- Teledyne Technologies Inc.

- Lockheed Martin Corporation

- General Dynamics Corporation

- BAE Systems plc

- Exail Technologies SA

第七章 市场机会及未来趋势

The Autonomous Underwater Vehicle Market size is estimated at USD 2.13 billion in 2024, and is expected to reach USD 5.45 billion by 2029, growing at a CAGR of 20.62% during the forecast period (2024-2029).

The market is driven by the wide applications of autonomous underwater vehicles (AUVs) in multiple sectors, such as exploration and research, resource exploration, environment monitoring, defense and security, infrastructure inspection, and scientific research.

The adoption of AUVs has also increased due to their stability, low deployment cost, improved data quality, and excellent navigation algorithms. These benefits have made applying autonomous underwater vehicles a safe option for many. For instance, they are deployed in the oil and gas industry to create seafloor maps. The military also uses them for inspection and identification. This has aided commerce and security in many nations.

Underwater vehicle technology is expected to lead to attractive opportunities for manufacturing companies. Developing cost-effective communication technology for underwater vehicles with excellent disturbance tolerance will significantly fuel market growth.

However, increasing operational costs and uncertainty in the operational performance of AUVs are likely to hinder market growth.

Autonomous Underwater Vehicles Market Trends

Military & Defense will a Hold Significant Market Share

Autonomous underwater vehicles (AUVs) are utilized in various military and defense applications due to their ability to operate autonomously and gather valuable information in underwater environments. These vehicles provide military and defense forces with valuable capabilities for underwater operations, including surveillance, reconnaissance, mine countermeasures, and special operations, enhancing maritime security and situational awareness in complex and challenging environments.

Defense spending has significantly increased due to security issues, concerns over contested territories, and threats. According to new data on global military expenditure published by the Stockholm International Peace Research Institute (SIPRI) in April 2024, total global military spending increased by 6.8% in real terms in 2022, reaching USD 2,443 billion. Countries use cutting-edge technologies to protect their borders from underwater threats.

According to the ICC International Maritime Bureau (IMB) 's annual Piracy and Armed Robbery Report, 120 incidents of maritime piracy and armed robbery against ships were reported in 2023 compared to 115 in 2022. This increase in threats creates security issues across marine borders. Thus, the factors mentioned above are expected to drive market growth.

North America will Witness the Highest Growth During the Forecast Period

The autonomous vehicle market in North America is expected to showcase the highest growth during the forecast period, owing to the presence of leading manufacturers, rising demand for AUVs from the US Navy, and extensive research and development.

In February 2024, the US Navy selected Anduril and its Dive family of large autonomous underwater vehicles (AUVs) to prototype distributed, long-range, persistent underwater sensing and payload delivery in contested environments. Anduril provides a family of AI-enabled AUVs that are designed to perform a wide range of defense and commercial missions.

Amid rising tensions in the Indo-Pacific region, particularly in the maritime environment, the US Department of Defense (DoD) is heavily investing in the development of autonomous systems to strengthen national security. For instance, The Boeing Company is developing the Orca XLUUV with funding from the US Navy. In 2019, the company won a USD 43 million contract to build four of the AUVs based on the design of Boeing's Echo Voyager. They are planned to be finished in 2024. Such factors will stimulate the market growth in North America.

Autonomous Underwater Vehicles Industry Overview

The autonomous underwater vehicles market is fragmented, with several players and a mix of established companies and emerging startups. Some of the leading players include Kongsberg Gruppen ASA, General Dynamics Corporation, Lockheed Martin Corporation, The Boeing Company, and SAAB AB.

These players incorporate strategic initiatives such as acquisitions, partnerships, expansions, and product/technology launches to maintain their positions and gain a competitive advantage in this market. For instance, in July 2022, Kongsberg Gruppen ASA secured several significant contracts for HUGIN AUVs. The company declared that, in addition to the increasing demand for marine robots, its broader portfolio allows it to address new applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.2 By Application

- 5.2.1 Military & Defense

- 5.2.2 Oil & Gas

- 5.2.3 Environment Protection & Monitoring

- 5.2.4 Oceanography

- 5.2.5 Archaeology & Exploration

- 5.2.6 Search & Salvage Operations

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 The Boeing Company

- 6.2.2 Kongsberg Gruppen ASA

- 6.2.3 L3Harris Technologies Inc.

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 SAAB AB

- 6.2.6 Teledyne Technologies Inc.

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 General Dynamics Corporation

- 6.2.9 BAE Systems plc

- 6.2.10 Exail Technologies SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年自主水下航行器全球市场报告

2025 年自主水下航行器全球市场报告 海上石油和天然气 IRM 用 AUV 市场规模、份额和成长分析(按类型、水深、推进系统、应用和地区)- 产业预测 2025-2032

海上石油和天然气 IRM 用 AUV 市场规模、份额和成长分析(按类型、水深、推进系统、应用和地区)- 产业预测 2025-2032 亚太地区 AUV -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)南美 AUV -市场占有率分析、行业趋势和成长预测(2025-2030 年)欧洲AUV市场:份额分析、产业趋势/统计、成长预测(2025-2030)

亚太地区 AUV -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)南美 AUV -市场占有率分析、行业趋势和成长预测(2025-2030 年)欧洲AUV市场:份额分析、产业趋势/统计、成长预测(2025-2030) 海上自主水下航行器市场 - 全球产业规模、份额、趋势、机会和预测,按车辆类别、最终用户、活动、地区和竞争细分,2019-2029F

海上自主水下航行器市场 - 全球产业规模、份额、趋势、机会和预测,按车辆类别、最终用户、活动、地区和竞争细分,2019-2029F 自主式无人潜水机 (AUV) 市场评估:类型·形状·用途·各地区的机会及预测 (2017-2031年)

自主式无人潜水机 (AUV) 市场评估:类型·形状·用途·各地区的机会及预测 (2017-2031年) 2030 年亚太海洋监测系统市场预测 - 区域分析 - 按类型(感测器、水下通讯系统和浮标观测监测系统)和应用(陆上和海上)

2030 年亚太海洋监测系统市场预测 - 区域分析 - 按类型(感测器、水下通讯系统和浮标观测监测系统)和应用(陆上和海上) 北美海洋监测系统市场预测至 2030 年 - 区域分析 - 按类型(感测器、水下通讯系统和浮标观测监测系统)和应用(陆上和海上)

北美海洋监测系统市场预测至 2030 年 - 区域分析 - 按类型(感测器、水下通讯系统和浮标观测监测系统)和应用(陆上和海上) 欧洲海洋监测系统市场预测至 2030 年 - 区域分析 - 按类型(感测器、水下通讯系统和浮标观测监测系统)和应用(陆上和海上)

欧洲海洋监测系统市场预测至 2030 年 - 区域分析 - 按类型(感测器、水下通讯系统和浮标观测监测系统)和应用(陆上和海上)