|

市场调查报告书

商品编码

1536826

端点安全:市场占有率分析、产业趋势与统计、成长预测(2024-2029)Endpoint Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

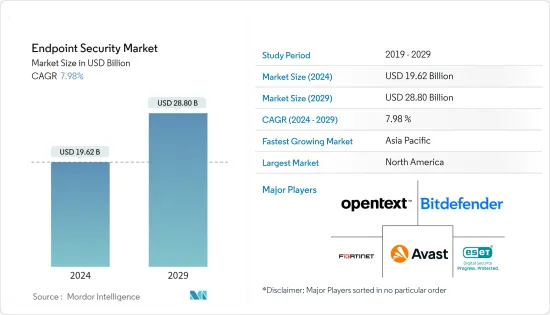

端点安全市场规模预计到 2024 年为 196.2 亿美元,预计到 2029 年将达到 288 亿美元,在预测期内(2024-2029 年)复合年增长率为 7.98%。

主要亮点

- 由于透过互联连网型设备在商业生态系统中越来越多地采用资料集中方法和决策,因此随着数位化的发展,全球网路攻击的数量也在增加。全球资料外洩事件的增加正在推动企业采用更加分散和基于边缘的安全技术,从而推动市场对端点安全解决方案的需求。

- 市场上端点设备的使用量正在强劲增长,这使得它们更容易受到端点攻击和破坏的持续增加和复杂性的影响,并且对高安全性解决方案来应对端点攻击的需求也在成比例地增加。 。此外,物联网、人工智慧、机器学习和巨量资料等创新技术的出现等因素也支持了市场的成长。在日益复杂的法规环境中,快速变化的法律体制和 IT 风险的缓解预计将在预测期内支持市场成长。

- 2023 年 3 月,GSMA 报告称,继 2020 年以来的成长趋势之后,全球企业的物联网 (IoT) 连接正在显着增加。到 2030 年,连线数量预计将达到 440 亿,物联网易受网路攻击的脆弱性将增加企业资料外洩的风险。

- 由于缺乏对网路攻击的认识,市场成长受到限制。然而,由于采取正确的措施几乎所有网路攻击都可以显着减少,因此许多公司正计划增加整体支出。今年预计将有超过 1 兆美元用于网路安全,并且这一数字预计会随着时间的推移而改善。

- COVID-19 大流行增加了对端点安全解决方案的需求,主要是端点侦测和回应解决方案,以及在数位化。

- 国际付款银行表示,在新冠肺炎 (COVID-19) 疫情期间,金融机构面临的网路攻击风险增加,而远距工作条件又加剧了这种风险。大流行后,线上和资料主导的业务趋势增加了对网路安全的需求,并刺激了世界各地的企业和政府机构采用端点安全。

端点安全市场趋势

消费领域预计将显着成长

- 提高消费者端点安全性的主要驱动力是网路连线的改善和网路普及率的上升。对于家庭用户来说,网路和电子邮件是恶意软体可能进入的区域。因此,端点安全解决方案针对消费者群体的这些攻击点。此外,越来越多的消费者将智慧型手机、平板电脑和笔记型电脑等设备用于个人和业务目的,这使得端点安全解决方案成为保护资料的重要工具。

- 智慧建筑和智慧家庭产品的出现增加了住宅中物联网的数量,增加了全球端点安全攻击的风险,增加了消费者领域对端点安全解决方案的需求并增加了市场份额。

- 爱立信表示,预计 2022 年至 2028 年全球物联网连线数量将增加一倍。预计2022年广域物联网连线数将达到29亿个,到2028年将达到60亿个。

- 美国政府计划于 2023 年 7 月实施措施,提高人们对智慧家庭设备的安全意识。政府推出了「美国网路信任标誌」倡议,对物联网设备进行认证,以保护用户免受网路攻击。

- 智慧型手錶的普及增加了从健康和位置资讯到银行帐户详细资讯等大量个人资料的储存和传输,使智慧型手錶用户容易受到网路攻击。

- 因此,在智慧家庭的成长支持下,消费者领域中智慧型装置、笔记型电脑和智慧型手机的使用不断增加,以提高能源管理和生产力,从而增加了消费者领域的网路攻击风险,预计将推动这一趋势。

亚太地区成长强劲

- 由于智慧型手机普及率高、勒索软体和恶意软体攻击增加、终端用户行业数位化不断提高、连接设备数量不断增加以及网路攻击的演变,亚太地区的端点安全市场正在经历显着增长。这些因素不仅推动了消费者,也推动了该地区企业对端点安全的需求。

- 随着各行业组织的发展,该地区的端点也显着增加。因此,组织拥有更广泛的攻击面,攻击者拥有更多进入其係统的入口点,从而增加了对端点安全的需求。

- 亚太地区提供端点安全解决方案的端点安全解决方案供应商显着扩张,显示该地区存在成长机会。例如,2024 年 1 月,着名端点安全公司 ESET 宣布在新加坡开设新的亚太 (APAC) 总部。透过此次扩张,该公司旨在为亚太地区的消费者和合作伙伴提供更有效的服务。

- 2023 年 11 月,网路安全解决方案供应商兼 Percept 端点侦测与回应云端安全平台开发商 Sequretek 从 Omidyar Network India 获得 800 万美元资金,用于扩大其在印度的业务。

- 端点网路攻击的增加、企业数位化趋势的策略发展以提高业务效率、数位经济的成长、不断变化的网路环境以及跨行业端点设备的激增正在推动对点安全解决方案的需求不断增加。

端点安全产业概述

由于跨国公司和中小企业的存在,全球端点安全市场高度分散。市场上的主要企业永续Open Text Corporation、Bitdefender LLC、Avast Software SRO、Fortinet Inc. 和 ESET Spol。

- 2023 年 12 月,商业软体和服务评论提供者 G2 在 2024 年冬季报告中将 Sophos 评为端点保护、EDR、XDR、防火墙和 MDR 领域的关键参与者。

- 2023 年 11 月,SentinelOne 宣布与 Pax8 建立合作伙伴关係,Pax8 是一流技术解决方案的市场。此次合作将提供下一代网路安全解决方案,可端到端地保护公司最关键的基础设施和资产。这种合作关係为两家公司提供了更先进的端点、身分和云端安全产品。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 评估 COVID-19 对产业的影响

第五章市场动态

- 市场驱动因素

- 智慧型设备的成长

- 资料外洩增加

- 市场挑战

- 对网路攻击缺乏认识

第六章 市场细分

- 按最终用户

- 消费者

- 商业

- BFSI

- 政府机构

- 製造业

- 卫生保健

- 能源/电力

- 零售

- 其他业务

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Open Text Corporation

- Bitdefender LLC

- Avast Software SRO

- Fortinet Inc.

- Eset Spol. S RO

- Watchguard Technologies Inc.

- Kaspersky Lab Inc.

- Microsoft Corporation

- Sophos Ltd

- Cisco Systems Inc.

- Sentinelone Inc.

- Musarubra Us LLC(Trellix)

- Deep Instinct Ltd

- Palo Alto Networks Inc.

- Broadcom Inc.

- Trend Micro Inc.

- Crowdstrike Holdings Inc.

- Cybereason Inc.

- Blackberry Limited

第八章投资分析

第九章 市场机会及未来趋势

The Endpoint Security Market size is estimated at USD 19.62 billion in 2024, and is expected to reach USD 28.80 billion by 2029, growing at a CAGR of 7.98% during the forecast period (2024-2029).

Key Highlights

- The increased adoption of data-intensive approaches and decisions in the business ecosystems through connected devices has raised the number of cyber-attacks globally in line with the growing digitalization. Enterprises are increasingly adopting more decentralized and edge-based security techniques due to increasing data breaches worldwide, driving the demand for endpoint security solutions in the market.

- The market has been registering significant growth in the usage of endpoint devices, which are becoming vulnerable to a continuously increasing and sophisticated nature of endpoint attacks and breaches and a proportionally increasing demand for high-security solutions to combat endpoint attacks. The growth of the market is also supported by factors such as the advent of innovative technologies like IoT, AI, ML, and big data, among others. IT risk mitigation in an increasingly complex regulatory environment with fast-changing legal frameworks is expected to support the market's growth during the forecast period.

- In March 2023, GSMA reported that Worldwide Internet of Things (IoT) connections in Enterprises are increasing significantly, following a growing trend from 2020. It is expected to reach 44 billion connection numbers by 2030, which would raise the risk of data breaches in enterprises due to the vulnerability of IoT to cyber attacks.

- The market's growth is restrained by the lack of awareness about cyberattacks. However, since almost all cyberattacks can be reduced significantly by taking appropriate actions, many companies are planning to raise their overall spending. With over a trillion dollars anticipated to be spent on cyber security this year, these figures are anticipated to improve in the future.

- The COVID-19 pandemic raised the demand for endpoint security solutions, majorly endpoint detection and response solutions and services to protect businesses and countries from malicious cyber attacks supported by increasing digitalization.

- The Bank for International Settlements stated that, during the COVID-19 pandemic, financial institutions faced an increasing risk of cyber attacks, which were accelerated by remote working conditions. The need for cyber security majors in enterprises and government entities of various countries worldwide increased after the pandemic due to the trend of online and data-driven businesses, fueling the implementation of endpoint security.

Endpoint Security Market Trends

Consumer Segment is Expected to Witness Significant Growth

- The primary driving force for increased consumer endpoint security is improved internet connectivity and growing internet penetration. For household users, the web and e-mail are potential areas for malware penetration. Thus, endpoint security solutions are aimed at these attack points for the consumer segment. Moreover, consumers are increasingly adopting devices such as smartphones, tablets, and laptops for personal and professional purposes, making endpoint security solutions an essential tool for securing data.

- The emergence of intelligent buildings and smart home products has raised the number of IoTs in residential premises, which is increasing the risk of endpoint security attacks worldwide, driving the demand for endpoint security solutions in the consumer segment and supporting the market's growth.

- According to Ericsson, the number of global IoT connections is expected to double from 2022 to 2028. The number of wide-area IoT connections in 2022 was 2.9 billion, and it is expected to be 6 billion by 2028.

- In July 2023, the US government planned to implement measures to enhance awareness of the safety of smart home devices. The administration introduced the "US Cyber Trust Mark" initiative, which seeks to authorize IoT devices to protect users from cyberattacks.

- The growth of smartwatches has raised the storage and transmission of large amounts of personal data, from health and location information to banking details, making smartwatch users vulnerable to cyberattacks.

- Therefore, the increasing usage of smart devices, laptops, and smartphones in the consumer segments, supported by the growth of smart homes for better energy management and productivity, has raised the risk of cyber attacks in the consumer segment, which is expected to fuel the growth of endpoint security solutions during the forecast period.

Asia-Pacific to Register Major Growth

- The endpoint security market in Asia-Pacific is experiencing significant growth owing to the region's high smartphone penetration, rising ransomware and malware attacks, growing digitization in end-user industries, rising number of connected devices, and evolving cyberattacks. These have necessitated the demand for endpoint security for consumers as well as businesses across the region.

- As organizations across verticals grow in the region, there is significant growth in endpoints. As a result, it expands the attack surface of an organization while offering attackers increasing entry points to a system, necessitating the demand for endpoint security.

- Asia-Pacific has been witnessing significant expansion of endpoint security solution providers to offer their endpoint security solutions, pointing toward growth opportunities in the region. For instance, in January 2024, ESET, a prominent player in endpoint security, announced the inauguration of its new Asia-Pacific (APAC) Headquarters in Singapore. With this expansion, the company aims to more effectively serve its consumers and partners in the APAC region.

- In November 2023, cybersecurity solutions provider and the developer of Percept Cloud Security Platform for Endpoint Detection & Response, Sequretek, secured USD 8 million from Omidyar Network India to expand its business in India, which shows the increasing demand for endpoint security solutions in the region.

- The growth of endpoint cyberattacks, strategic development of digitalization trends in enterprises for business efficiencies, the growing digital economy, the evolving cyber landscape, and the proliferation of endpoint devices across verticals have raised the demand for endpoint security solutions in the region.

Endpoint Security Industry Overview

The global endpoint security market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Open Text Corporation, Bitdefender LLC, Avast Software SRO, Fortinet Inc., and ESET Spol. S.R.O. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- In December 2023, G2, a business software and service review provider, named Sophos a significant player for Endpoint Protection, EDR, XDR, Firewall, and MDR in their Winter 2024 Reports, which would fuel the company's brand positioning to support its market growth in the future.

- In November 2023, SentinelOne announced that the company is partnering with Pax8, which is a marketplace for best-in-class technology solutions. The partnership provides next-generation cybersecurity solutions that enable the protection of the company's most critical infrastructure and assets from end to end. This partnership will allow both companies to get more advanced endpoint, identity, and cloud security offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Smart Devices

- 5.1.2 Increasing Number of Data Breaches

- 5.2 Market Challenges

- 5.2.1 Lack of Awareness about Cyberattacks

6 MARKET SEGMENTATION

- 6.1 By End User

- 6.1.1 Consumer

- 6.1.2 Business

- 6.1.2.1 BFSI

- 6.1.2.2 Government

- 6.1.2.3 Manufacturing

- 6.1.2.4 Healthcare

- 6.1.2.5 Energy and Power

- 6.1.2.6 Retail

- 6.1.2.7 Other Businesses

- 6.2 By Geography***

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Open Text Corporation

- 7.1.2 Bitdefender LLC

- 7.1.3 Avast Software SRO

- 7.1.4 Fortinet Inc.

- 7.1.5 Eset Spol. S R. O.

- 7.1.6 Watchguard Technologies Inc.

- 7.1.7 Kaspersky Lab Inc.

- 7.1.8 Microsoft Corporation

- 7.1.9 Sophos Ltd

- 7.1.10 Cisco Systems Inc.

- 7.1.11 Sentinelone Inc.

- 7.1.12 Musarubra Us LLC (Trellix)

- 7.1.13 Deep Instinct Ltd

- 7.1.14 Palo Alto Networks Inc.

- 7.1.15 Broadcom Inc.

- 7.1.16 Trend Micro Inc.

- 7.1.17 Crowdstrike Holdings Inc.

- 7.1.18 Cybereason Inc.

- 7.1.19 Blackberry Limited

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025 年端点安全全球市场报告

2025 年端点安全全球市场报告 端点安全市场:组件、执行点、解决方案、服务、部署,按产业划分 - 2025-2030 年全球预测

端点安全市场:组件、执行点、解决方案、服务、部署,按产业划分 - 2025-2030 年全球预测 2024-2032 年端点安全市场报告(按组件、部署模式、组织规模、垂直产业和区域)

2024-2032 年端点安全市场报告(按组件、部署模式、组织规模、垂直产业和区域) 全球端点安全市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测

全球端点安全市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势与预测 端点安全市场规模、份额、成长分析、按组件、按执行点、按企业规模、按最终用户、按部署、按地区 - 行业预测,2024-2031 年

端点安全市场规模、份额、成长分析、按组件、按执行点、按企业规模、按最终用户、按部署、按地区 - 行业预测,2024-2031 年 端点备用软体的全球市场:2024年

端点备用软体的全球市场:2024年 2024-2028 年全球端点安全市场

2024-2028 年全球端点安全市场 端点安全市场:2023 年至 2028 年预测

端点安全市场:2023 年至 2028 年预测 端点安全市场规模、份额、趋势分析报告:按组件、按部署、按组织、按用途、按地区、细分趋势,2023-2030 年

端点安全市场规模、份额、趋势分析报告:按组件、按部署、按组织、按用途、按地区、细分趋势,2023-2030 年 全球端点安全成长机会

全球端点安全成长机会