|

市场调查报告书

商品编码

1536928

浮体式海上风力发电 -市场占有率分析、产业趋势/统计、成长预测(2024-2029)Floating Offshore Wind Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

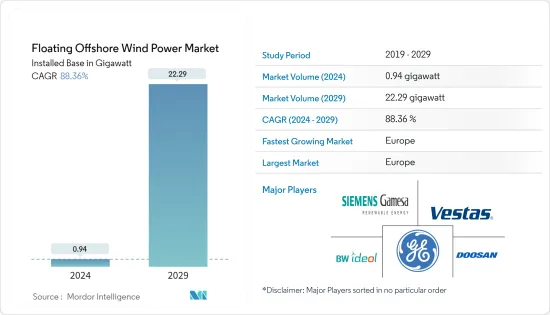

浮体式海上风电市场装置规模预计将从2024年的0.94吉瓦扩大到2029年的22.29吉瓦,预测期间(2024-2029年)复合年增长率为88.36%。

主要亮点

- 从中期来看,对海上可再生风力发电计划的投资增加以及先进且易于使用的海上风力发电技术预计将成为预测期内浮体式海上风电市场的主要驱动力。

- 另一方面,来自替代可再生能源市场的激烈竞争将成为预测期内浮体式海上风电市场的限制因素。

- 儘管如此,由于开拓了有利于浮体式结构的开拓的深海市场,浮体式海上风力发电越来越受欢迎,为市场参与者提供了充足的机会。

- 预计欧洲将在预测期内主导浮体式海上风电市场。

浮体式海上风力发电市场趋势

过渡水深(水深30m至60m)段预计将成长

- 由于水深较深且计划经济性良好,浮体式海上风电(FOWT)技术在过渡水深(30-60 m 深度)较为发达。驳船类型是浅水中最具商业性可行性的浮体式风力发电机设计。此型号适用于30公尺(m)以上的活动,是所有浮体式基础中吃水最浅的。

- 驳船浮体式风力发电机的占地面积为方形,而其他设计则采用月池来减少波浪载荷引起的应力。据GWEC称,典型的6兆瓦驳船浮体式风力发电机重量在2000吨至8000吨之间。然而,BW Ideol 凭藉其阻尼池驳船浮动下部结构技术,是唯一部署兆瓦级驳船型 FOWT 的公司。

- 由于水深较浅,与固定基地技术相比,FOWT技术从商业角度来看实用性较差。在预测期内,驳船技术预计将占 FOWT 市场的一小部分。根据美国环保署统计,截至2021年,全球运作中的驳船式FOWT容量仅5兆瓦。基于驳船的 FOWT 容量约为 1,932 MW,占全球未来计划宣布的离岸风力发电技术的 2.1%。

- 大多数公司都试图将可用于更深水域的 FOWT 设计推向市场。然而,一些半潜式技术也可以在瞬时深度使用。几种基于半潜式设计的商业性FOWT 模型使其即使在瞬态水深下也能发挥作用。其中一些模型最初用于实验计划,而其他模型则经过改进以用于商业企业。

- 2024 年 4 月 24 日,美国能源局风力发电技术办公室 (WETO) 宣布拨款 4800 万美元,用于资助地区和国家海上风电技术的研发,其中包括宣布的浮体式海上风电平台的研发。机会的意向通知。这预示着市场未来的成长潜力。

- 根据国际可再生能源机构(IEA)《2024年可再生能源容量报告》,2023-24年全球离岸风力发电将成长17.26%,2023年新增10,696MW,而2022年为61,967MW。做到了。这样的市场开拓预示着市场参与者在不久的将来前景光明。

- 大多数转型中的 FOWT计划似乎都在欧洲,特别是在英国、斯堪地那维亚和法国,这些国家的大型计划正处于规划阶段。在预测期内,该领域的大部分部署预计将在这些地区进行。

- 因此,瞬态深度(30m至60m深度)部分预计在预测期内将显着成长。

预计欧洲将主导市场

- 欧洲拥有全球最大份额的离岸风力发电能力。据欧盟称,欧洲占全球离岸风力发电装置容量的四分之一。该国(主要是北海国家)可能主导离岸风力发电市场。

- 全球整体约85%的离岸风力发电设施位于欧洲水域。各国政府,特别是北海地区的政府,有着在其领海内建立离岸风力发电的雄心勃勃的目标。

- EolMed计划是法国第一个位于地中海的浮体式试验风力发电厂。 2022年5月,道达尔能源宣布该计划开工建设,预计2024年投入运作。该计划由三台 10MW浮体式涡轮机组成,锚定在 62 公尺深的海底。涡轮机采用带有阻尼池的驳船设计。

- 根据国际可再生能源机构《2024年再生能源容量》显示,2023-24年欧洲离岸风力发电装置容量将成长9.58%,从2022年的29,539MW增加到2023年的2,830MW。这些新兴市场的开拓为市场相关人员带来了美好的未来前景。

- 2023年8月,全球最大的浮体式风力发电厂Hywind Tampen计划在距离挪威海岸约140公里、水深270至310公尺处开始运作。 Highwind Tampen 使用 11 台浮体式风力发电机,系统容量为 88MW。它有助于为海上石油和天然气平台供电。

- 这些趋势将使欧洲成为预测期内参与浮体式海上风电的主要业务地点。

浮体式海上风电产业概况

浮体式海上风电市场较为分散。市场的主要企业包括 GE、Doosan Energy、Siemens Gamesa Renewable Energy、BW Ideaol SA 和 Vestas Wind Systems AS。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章 简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年浮体式海上风力发电的潜在装置容量产能预测

- 主要计划资讯

- 现有主要计划

- 即将进行的计划

- 最新趋势和发展

- 政府法规政策

- 市场动态

- 促进因素

- 加大海上可再生风力发电计划投资

- 先进且易于使用的海上风力发电技术

- 抑制因素

- 替代可再生能源市场的激烈竞争

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 按水深(仅限定性分析)

- 浅水(水深小于30m)

- 瞬态水深(水深30m至60m)

- 深海(深度超过60m)

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 日本

- 印尼

- 马来西亚

- 越南

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 南非

- 奈及利亚

- 其他中东/非洲

- 北美洲

第六章 竞争状况

- 合併、收购、联盟和合资企业

- 主要企业策略

- 公司简介

- Vestas Wind Systems AS

- General Electric Company

- Siemens Gamesa Renewable Energy SA

- BW Ideol AS

- Equinor ASA

- Marubeni Corporation

- Macquarie Group Limited

- Doosan Enerbility Co. Ltd

- 市场排名分析

第七章 市场机会及未来趋势

- 开拓的深海水域浮体式海上风力发电工程的开发

简介目录

Product Code: 62712

The Floating Offshore Wind Power Market size in terms of installed base is expected to grow from 0.94 gigawatt in 2024 to 22.29 gigawatt by 2029, at a CAGR of 88.36% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, rising investments in offshore renewable wind energy projects, coupled with advanced and readily accessible offshore wind turbine technologies, are expected to be major drivers of the floating offshore wind market during the forecast period.

- On the other hand, tough competition from alternate renewable energy markets will restrain the floating offshore wind market during the forecast period.

- Nevertheless, floating offshore wind energy is becoming more popular in developing untapped deep-water prospects favorable for floating structures, providing ample opportunities for the market players.

- Europe is expected to dominate the floating offshore wind market during the forecast period.

Floating Offshore Wind Power Market Trends

The Transitional Water (30 m to 60 m depth) Segment is Expected to Grow

- Due to the greater water depth and favorable project economics, floating offshore wind turbine (FOWT) technology is more developed in transitional water depths (30-60 meters). The barge variant is the most commercially viable floating wind turbine design at shallow depths. This model is appropriate for activities higher than 30 meters (m) and has the shallowest draft of any floating foundation.

- Barge-style floating wind turbines have a square footprint, while other designs incorporate a moonpool to lessen stresses brought on by wave-induced loads. According to GWEC, a typical 6-megawatt floating barge wind turbine weighs between 2,000 and 8,000 tons. However, BW Ideol, with its Damping Pool Barge Floating Substructure Technology, is the only company that has deployed barge-type FOWT at the MW scale.

- Since the water depth is shallower, FOWT technology is less practical from a business point of view than fixed-base technology. During the forecast period, barge technology is expected to make up a small part of the FOWT market. According to the US EPA, only 5 MW of barge FOWT capacity operated globally as of 2021. Around 1,932 MW of FOWT capacity on barges, or 2.1% of all announced offshore wind substructure technologies for future projects worldwide, was announced.

- Most companies attempt to market FOWT designs that can be used in deeper waters. However, some semi-submersible technologies can also be used at transitional water depths. They can function at transitional depths due to several commercial FOWT models that are built on the semi-submersible design. A few of these models were initially used in experimental projects, while others were modified for use in ventures for profit.

- The US Department of Energy's Wind Energy Technologies Office (WETO) announced on April 24, 2024, that it intended to issue a Notice of Intent involving a USD 48 million funding opportunity for regional and national research and development of offshore wind technologies, including floating offshore wind platform research and development. This promises future growth potential for the market.

- According to the International Renewable Energy Agency RE Capacity 2024, the global installed offshore wind energy capacity increased by 17.26% in FY 2023-24, adding 10,696 MW in 2023 to the earlier installed capacity of 61,967 MW in 2022. Such developments show promising outlooks for the market players in the near future.

- Most of the FOWT projects in transitional depths are likely to be in Europe, especially in the United Kingdom, Scandinavia, and France, where large projects are in the planning stages. During the forecast period, most of the deployments in this segment are likely to happen in these regions.

- Thus, the transitional water (30 m to 60 m depth) segment is expected to grow significantly during the forecast period.

Europe is Expected to Dominate the Market

- Europe holds the largest share of offshore wind energy installations globally. According to the European Union, Europe represents a quarter of global offshore wind installations. The country (primarily North Sea countries) is likely to be at the helm of the offshore wind market.

- Around 85% of offshore wind installations are globally in European waters. The governments, particularly in the North Sea area, have set an ambitious target for installing offshore wind farms in their territorial waters.

- The EolMed project is France's first floating pilot wind farm in the Mediterranean Sea. In May 2022, TotalEnergies announced the start of the project's construction, which is expected to be operational by 2024. The project consists of three 10 MW floating turbines on the bathymetry of the 62-meter depth and anchored to the seabed. The turbines will use a barge design with a damping pool.

- According to the International Renewable Energy Agency RE Capacity 2024, the installed offshore wind energy capacity in Europe increased by 9.58% in FY 2023-24, adding 2,830 MW in 2023 to the earlier installed capacity of 29,539 MW in 2022. Such developments show promising outlooks for the market players in the near future.

- In August 2023, the world's largest floating wind farm, the Hywind Tampen Project, started operating around 140 kilometers off the coast of Norway in depths ranging from 270 to 310 meters. Hywind Tampen uses 11 floating wind turbines and has a system capacity of 88 MW. It helps power operations at offshore oil and gas platforms.

- During the forecast period, these trends should make Europe a great place to do business for players involved in floating offshore wind farms.

Floating Offshore Wind Power Industry Overview

The floating offshore wind power market is moderately fragmented. Some major players in the market include General Electric Company, Doosan Energy, Siemens Gamesa Renewable Energy, BW Ideaol SA, and Vestas Wind Systems AS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Floating Offshore Wind Power Potential Installed Capacity Forecast in GW, till 2029

- 4.3 Key Projects Information

- 4.3.1 Major Existing Projects

- 4.3.2 Upcoming Projects

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Rising investments in offshore renewable wind energy projects

- 4.6.1.2 Advanced and readily accessible offshore wind turbine technologies

- 4.6.2 Restraint

- 4.6.2.1 Tough competition from alternate renewable energy markets

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Water Depth (Qualitative Analysis Only)

- 5.1.1 Shallow Water (less than 30 m depth)

- 5.1.2 Transitional Water (30 m to 60 m depth)

- 5.1.3 Deep Water (higher than 60 m depth)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Nordic Countries

- 5.2.2.7 Russia

- 5.2.2.8 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Indonesia

- 5.2.3.5 Malaysia

- 5.2.3.6 Vietnam

- 5.2.3.7 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 South Africa

- 5.2.5.5 Nigeria

- 5.2.5.6 Rest of the Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems AS

- 6.3.2 General Electric Company

- 6.3.3 Siemens Gamesa Renewable Energy SA

- 6.3.4 BW Ideol AS

- 6.3.5 Equinor ASA

- 6.3.6 Marubeni Corporation

- 6.3.7 Macquarie Group Limited

- 6.3.8 Doosan Enerbility Co. Ltd

- 6.4 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developing Floating Offshore Wind Projects in untapped offshore deep-water prospects

02-2729-4219

+886-2-2729-4219

亚太地区浮体式海上风电:市场占有率分析、产业趋势与成长预测(2025-2030)

亚太地区浮体式海上风电:市场占有率分析、产业趋势与成长预测(2025-2030) 浮体式海上风电市场:按组件、类型、水深、涡轮机容量、应用划分 - 2025-2030 年全球预测

浮体式海上风电市场:按组件、类型、水深、涡轮机容量、应用划分 - 2025-2030 年全球预测 离岸风电市场规模、份额、成长分析,按组件、按安装、按深度、按容量、按地区 - 产业预测,2024-2031 年

离岸风电市场规模、份额、成长分析,按组件、按安装、按深度、按容量、按地区 - 产业预测,2024-2031 年 海上平台电气化市场 - 按技术、应用、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029F

海上平台电气化市场 - 按技术、应用、地区和竞争细分的全球产业规模、份额、趋势、机会和预测,2019-2029F 离岸风力发电市场:按组成部分和位置- 2025 年至 2030 年全球预测

离岸风力发电市场:按组成部分和位置- 2025 年至 2030 年全球预测 Equinor 收购 Orsted 9.8% 股份:下一步是什么?

Equinor 收购 Orsted 9.8% 股份:下一步是什么? 全球离岸风力发电市场,2024-2028

全球离岸风力发电市场,2024-2028 全球离岸风电电缆市场

全球离岸风电电缆市场 浮式离岸风能市场、机会、成长动力、产业趋势分析与预测,2024-2032

浮式离岸风能市场、机会、成长动力、产业趋势分析与预测,2024-2032 离岸风电市场、机会、成长动力、产业趋势分析与预测,2024-2032

离岸风电市场、机会、成长动力、产业趋势分析与预测,2024-2032

▼