|

市场调查报告书

商品编码

1549825

全球单纸箱市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Mono Cartons - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

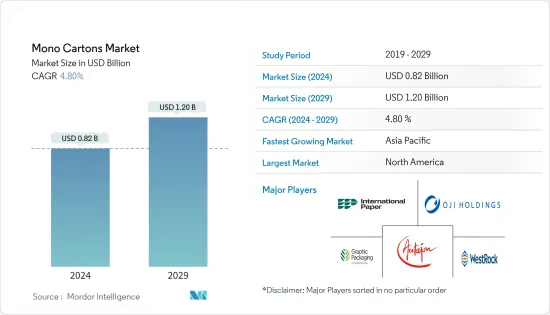

全球单纸箱市场规模预计到 2024 年为 8.2 亿美元,预计到 2029 年将达到 12 亿美元,在预测期内(2024-2029 年)复合年增长率为 4.80%。

单纸箱是一种轻质且美观的包装解决方案。 Monocarton 是一种可折迭纸盒,可提供保护并允许根据各种最终用户应用的要求定製纸盒。

主要亮点

- 单纸箱用于紧凑地包装产品,并且高度可定制,促进了各种最终用户行业的许多应用。对永续包装的需求不断增长正在推动市场成长。涂层和非涂层单纸盒有多种设计、形状和尺寸,这增加了对有吸引力的设计的需求,并为纸盒创造了成长机会。

- 单纸盒便于储存和使用。这些纸箱由于其轻质结构有助于减轻包装重量,并提供适度的强度以确保包装产品的安全。它还可折迭,提供充足的存储空间并易于运输。它的需求量很大,因为它在生产、分销和消费方面具有成本效益。

- 由于牙膏、肥皂、饼干和乳霜等小产品的持续储存和运输,快速消费品 (FMCG) 产业对单箱的消费至关重要。快速消费品产业也使用印有产品规格标籤的印刷纸盒作为主要包装材料。由于开发中国家零售店数量的增加和个人可支配收入的增加,预计快速消费品行业的成长将在预测期内推动对单纸盒的需求。

- 电子商务单纸盒作为电子商务包装的替代品正在引起人们的注意。随着越来越多的人在网上购买并希望他们的产品安全且状况良好,单箱已成为重要的选择。此外,企业可以利用单纸盒的大表面积进行品牌推广和行销,增加曝光度并创造更强大的品牌形象。

- 市场正在见证塑胶等替代包装材料的挑战。儘管永续包装越来越受欢迎,但塑胶包装仍然是市场的关键成长要素之一。许多顾客仍然青睐塑胶包装的舒适度和成本,这使得单纸盒难以普及。要说服消费者和企业放弃塑胶包装,需要有效的教育和宣导活动,宣传使用单纸箱的环境效益。

单箱市场趋势

食品和饮料行业预计将显着成长

- 食品饮料包装是食品工业的重要组成部分,对于确保食品饮料安全至关重要。保护食品免受污染和损坏,延长保质期,并方便运输和储存。

- 用于食品包装的单纸盒由单层纸板製成。单纸盒可回收、耐用且用途广泛,可用于包装各种食品,包括生鲜食品、冷冻食品、零嘴零食和烘焙点心。单纸箱包装可确保食品保持新鲜、受保护且具有视觉吸引力。

- 全球对纸板的需求正在成长。根据Suzano Papel e Celulose预测,2022年纸板消费量预计将达到5,400万吨,2024年将达到5,600万吨。全球纸箱消费量的增加预计将在预测期内推动市场成长。此外,根据 Frozen & Refrigerated Buyer 和 Circnca 的数据,2023 年,披萨在美国冷冻食品销售额中位居榜首,达 15,640.4 亿美元,其次是冰淇淋,达 1,463.49 亿美元。

- 纸箱包装可以防止产品受潮,并且可以承受较长的运输时间,因此越来越多的品牌采用它来为消费者提供更好的效果,主要作为二级和三级包装的手段。麵包、蛋糕和生鲜产品等加工食品需要使用此类包装材料,并且正在推动需求。

- 各国加工食品、生鲜食品和肉类的消费量正在增加。食品消费的成长持续受到健康和保健趋势以及消费者日益增长的道德关注的推动。此外,人口成长预计将成为预测期内支持生鲜食品需求的主要驱动力。有机生产食品的趋势预计将增加现代杂货零售店中价格分布永续生鲜食品的数量。

亚太地区预计将经历最快的成长

- 亚太地区是全球最大的折迭纸盒包装市场之一,其中包括单纸盒,其巨大的发展潜力很可能会增加需求。亚洲一些新兴国家的需求预计将强劲。由于中国和印度等国家对家常小菜的需求不断增长,亚太地区主导了全球纸盒包装市场。

- 随着消费者关注环保和永续实践的变化,食品和饮料、医疗保健、个人护理和零售等多个区域行业对单纸盒的需求不断增长。消费者对永续包装选择的认识、原材料的可用性、纸张的轻质和可回收特性以及森林砍伐都促进了该地区对纸盒包装的需求。

- Packman团队于2023年6月进行的一项研究对印度的单箱公司集团进行了财务分析,排名前五的公司营业额超过20亿印度卢比,排名最后五的公司营业额在4.5亿印度卢比之间。许多公司向食品、酒类和药品等各个快速消费品领域供应单纸盒。

- 根据日本经济产业省及废纸回收促进中心(PRPC)统计,2023年日本纸张产量约1,160万吨,纸板产量约1,040万吨。纸和纸板产量增加约2200万吨。

- 2023 年 5 月,Omya International AG 宣布投资纸和纸板产业。我们在中国和印尼的纸板厂建造了七座现场粉碎和沈淀碳酸钙工厂。中国的新工厂包括位于广西、广东和山东省的三座研磨碳酸钙(GCC)工厂,位于山东省的两座沉淀碳酸钙(PCC)工厂以及位于福建省的另一座PCC工厂。这些用于造纸的原料可改善纸张性能,如印刷适性、光泽度和平滑度。该地区造纸公司的此类扩张预计将在预测期内推动市场成长。

单箱产业概况

单纸箱市场分散,包括各种公司,包括: Graphic Packaging International LLC、Oji Holdings Corporation、Westrock Company 和 International Paper 等营运公司致力于透过投资、合作、併购等方式创新新的解决方案,以扩大其在该地区的业务。

- 2024 年 2 月:王子控股与利乐日本有限公司合作开发日本首个专用无菌包装的回收系统。此回收系统从各种来源收集无菌包装包装,包括零售店、市政收集以及包装製造商的废纸。

- 2023 年 9 月:Graphic Packaging International 以 2.625 亿美元收购 Bell。贝尔经营三个加工工厂,两个位于南达科他州,一个位于俄亥俄州。 Graphic先前预计,收购贝尔将增加2亿美元的收入和1,000万美元的利润。贝尔公司每年在这些工厂消耗 95,000 吨纸板,并将其转化为折迭纸盒和相关产品。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 对永续包装解决方案的需求

- 电子商务正在推动市场成长

- 市场限制因素

- 与替代包装解决方案的竞争

第六章 市场细分

- 透过涂层

- 搭配外套

- 没有外套

- 按最终用户产业

- 饮食

- 药品

- 个人护理

- 电子产品

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Graphic Packaging International LLC

- Oji Holdings Corporation

- Westrock Company

- International Paper Company

- Stora Enso

- Georgia-Pacific LLC

- Autajon Group

- Parksons Packaging Ltd

- Packman Packaging Private Limited

- Packtek

第八章投资分析

第九章 市场机会及未来趋势

The Mono Cartons Market size is estimated at USD 0.82 billion in 2024, and is expected to reach USD 1.20 billion by 2029, growing at a CAGR of 4.80% during the forecast period (2024-2029).

Mono cartons are lightweight, esthetically appealing packaging solutions. Mono cartons are a type of folding carton that provides protection, and the cartons can be customized based on the requirements of various end-user applications.

Key Highlights

- Mono cartons are used for compact packaging of products, are highly customizable, and facilitate many applications across various end-user industries. An increase in demand for sustainable packaging is driving the market growth. Coated and uncoated mono cartons are produced in multiple designs, shapes, and sizes, increasing the demand for appealing designs and creating growth opportunities for the cartons.

- Mono cartons facilitate convenience for their storage and usage. These cartons help reduce the weight of the package due to their lightweight structure and offer a reasonable amount of strength to ensure the security of the packaged products. It also comes foldable, providing ample storage and shipment easement. It is cost-effective in production, distribution, and consumption, thus, is in high demand.

- The fast-moving consumable goods (FMCG) industry is critical to the consumption of mono cartons due to the continuous storage and shipment of small-sized products such as toothpaste, soap, biscuits, and face cream. The FMCG industry also uses printed cartons labeled with product specifications as the primary packaging material. Due to the increasing number of retail stores, coupled with rising individual disposable income in developing countries, the growing FMCG industry is anticipated to fuel the demand for mono cartons over the forecast period.

- E-commerce mono cartons have emerged as a favored alternative for e-commerce packaging. Mono cartons are a significant choice as more individuals buy online and want their products to arrive securely and in shape. Furthermore, companies can use the large surface area of mono cartons for branding and marketing, increasing exposure and creating a stronger brand identity.

- The market witnesses challenges due to alternate packaging materials such as plastic. Despite the rising popularity of sustainable packaging, plastic packaging remains one of the market's leading growth drivers. Many customers still favor the comfort and cost of plastic packaging, which makes the widespread adoption of mono cartons difficult. Persuading consumers and businesses to abandon plastic packaging necessitates effective educational and awareness initiatives on the environmental benefits of utilizing mono cartons.

Mono Cartons Market Trends

The Food and Beverage Industry is Expected To Witness Significant Growth

- Food and beverage packaging is a critical part of the industry and essential in ensuring the food or beverage is safe. It protects food from contamination and damage, helps extend its shelf life, and makes it easier to transport and store.

- Mono cartons used for food packaging are made from a single layer of cardboard. Mono cartons are recyclable, durable, and versatile and can package various food products, including fresh and frozen food products, snacks, and baked goods. Mono-carton packaging guarantees the food stays fresh, protected, and visually appealing.

- The demand for carton boards globally is witnessing growth. According to Suzano Papel e Celulose, cartonboard consumption was 54 million tons in 2022 and is expected to reach 56 million tons by 2024. The increase in the worldwide consumption of cartons is expected to drive the market growth over the forecast period. Also, according to Frozen & Refrigerated Buyer and Cirnca, the frozen food sales in the United States in 2023 were topped by pizza at USD 1,564.04 million, followed by ice cream at USD 1,463.49 million.

- As carton packaging keeps moisture away from products and resists long shipping times, it is increasingly being adopted by various brands to offer better results to their consumers, mainly as a means to secondary or tertiary packaging. Processed foods, such as bread, cakes, and perishable items, need such packaging materials to be used, thereby driving the demand.

- Various countries are witnessing a rise in the consumption of processed food, fresh produce, and meat sectors. Food consumption growth continues to be fueled by health and wellness trends and the increase in consumers' ethical concerns. Additionally, population growth is expected to be the key driver behind the demand for fresh food during the forecast period. A trend for organically produced foods is expected to increase the presence of sustainable fresh food at premium price points in modern grocery retailers.

The Asia-Pacific Region is Expected to Witness the Fastest Growth

- The Asia-Pacific region is one of the largest global folding carton packaging markets, including mono cartons, and demand is likely to grow due to its significant potential evolution. Demand in some emerging Asian countries is anticipated to be strong. The Asia-Pacific region dominates the global folding carton packaging market due to the rising demand for ready-to-eat meals in China, India, etc.

- As consumers focus on changes to eco-friendly and sustainable practices, mono-carton demand is growing across several regional industries, including food and beverage, healthcare, personal care, retail, etc. Consumer awareness of sustainable packaging choices, raw material availability, paper's lightweight and recyclable characteristics, and deforestation have all contributed to the region's demand for folding carton packaging.

- A survey conducted by the Packman team in June 2023 showed a financial analysis of a group of Indian mono-carton companies; the top five companies had turnovers exceeding INR 200 crore, while the bottom five had turnovers ranging from INR 45 crore to INR 90 crore. Many companies supplied mono cartons for various FMCG segments, including food, alcohol, and pharma products.

- According to METI (Japan) and the Paper Recycling Promotion Center (PRPC), in 2023, the paper production volume in Japan amounted to approximately 11.6 million metric tons, and the production volume for paperboard stood at around 10.4 million metric tons. The paper and paperboard production volume increased to around 22 million metric tons.

- In May 2023, Omya International AG announced investments in its paper and board industry. The company invested in seven onsite plants for ground and precipitated calcium carbonate at paperboard mill locations in China and Indonesia. The new plants in China include three ground calcium carbonate (GCC) plants in Guangxi, Guangdong, and Shandong, two precipitated calcium carbonate (PCC) plants in Shandong, and one more PCC plant in Fujian. These raw materials used for paper manufacturing will improve the paper's properties, such as printability, gloss, smoothness, etc. Such expansions by paper manufacturing companies in the region are expected to drive the market growth over the forecast period.

Mono Cartons Industry Overview

The market is fragmented with the presence of various players such as Graphic Packaging International LLC, Oji Holdings Corporation, Westrock Company, and International Paper. The companies operating are focused on innovating new solutions through investments, collaborations, mergers and acquisitions, etc., to expand their business in the region.

- February 2024: Oji Holdings and Nihon Tetra Pak K.K. partnered to pioneer Japan's first recycling system specifically for aseptic carton packages, a significant step toward gaining a circular economy for paper resources in the country. The recycling system collects aseptic carton packages from various sources, including retail and municipal collections and waste paper from packaging manufacturers.

- September 2023: Graphic Packaging International acquired Bell Inc. for USD 262.5 million. Bell operates three converting facilities: two in South Dakota and one in Ohio. Graphic previously estimated the Bell acquisition would add USD 200 million in sales and yield USD 10 million. Bell consumes an estimated 95,000 tons of paperboard annually at those facilities to convert into folding cartons and related products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Demand for Sustainable Packaging Solutions

- 5.1.2 E-commerce to Drive the Market Growth

- 5.2 Market Restraints

- 5.2.1 Competition from Alternative Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Coating

- 6.1.1 Coated

- 6.1.2 Uncoated

- 6.2 By End-User Industry

- 6.2.1 Food & Beverage

- 6.2.2 Pharmaceuticals

- 6.2.3 Personal Care & Comsetics

- 6.2.4 Electronics

- 6.2.5 Other End-User Industries

- 6.3 By Region

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Graphic Packaging International LLC

- 7.1.2 Oji Holdings Corporation

- 7.1.3 Westrock Company

- 7.1.4 International Paper Company

- 7.1.5 Stora Enso

- 7.1.6 Georgia-Pacific LLC

- 7.1.7 Autajon Group

- 7.1.8 Parksons Packaging Ltd

- 7.1.9 Packman Packaging Private Limited

- 7.1.10 Packtek

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

瓦楞纸包装市场:按材料类型、瓦楞纸板类型、印刷技术、最终用户和销售管道-全球预测,2026-2032年

瓦楞纸包装市场:按材料类型、瓦楞纸板类型、印刷技术、最终用户和销售管道-全球预测,2026-2032年 东南亚瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东南亚瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 单层纸匣全球市场规模、份额、趋势和成长分析报告(2026-2034年)

单层纸匣全球市场规模、份额、趋势和成长分析报告(2026-2034年) 日本纸盒包装市场规模、份额、趋势及预测(按材料类型、产品类型、最终用户和地区划分,2026-2034年)

日本纸盒包装市场规模、份额、趋势及预测(按材料类型、产品类型、最终用户和地区划分,2026-2034年) 2026年全球瓦楞纸包装市场报告中东和非洲瓦楞纸包装市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)北美瓦楞纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球瓦楞纸包装市场报告中东和非洲瓦楞纸包装市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)北美瓦楞纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 瓦楞纸包装市场规模、份额和成长分析:按壁型、箱型、瓦楞数、印刷技术、最终用户、通路和地区划分-2026-2033年产业预测

瓦楞纸包装市场规模、份额和成长分析:按壁型、箱型、瓦楞数、印刷技术、最终用户、通路和地区划分-2026-2033年产业预测 快速折迭门市场按类型、操作方式、最终用途领域和区域划分

快速折迭门市场按类型、操作方式、最终用途领域和区域划分 瓦楞包装市场-全球产业规模、份额、趋势、机会和预测,按产品类型、包装类型、最终用途、地区和竞争细分,2020-2030 年预测

瓦楞包装市场-全球产业规模、份额、趋势、机会和预测,按产品类型、包装类型、最终用途、地区和竞争细分,2020-2030 年预测