|

市场调查报告书

商品编码

1549842

补充装和可重复使用包装:市场占有率分析、行业趋势和成长预测(2024-2029)Refillable And Reusable Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

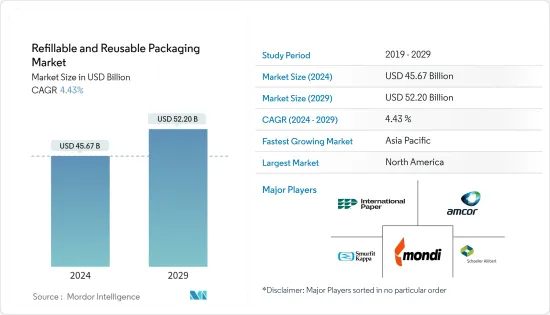

可再填充和可重复使用包装市场规模预计到 2024 年将达到 456.7 亿美元,到 2029 年将达到 522 亿美元,在市场预测期间(2024-2029 年)复合年增长率为 4.43%。

在全球转向永续性和环保意识不断增强的推动下,再填充和可重复使用包装市场正在经历显着的快速成长。世界各国政府正在推出更严格的法规,国际贸易不断增长,进一步增加了可再填充和可重复使用包装的需求。减少一次性包装废弃物、提高经济效益和确保包装安全等因素正在促进市场成长。

主要亮点

- 可再填充包装是一种永续的解决方案,允许产品多次再填充,与一次性替代品相比,可显着减少废弃物。这种趋势在食品和饮料、家庭清洁、个人卫生和其他消耗品领域尤其明显。

- 补充包装的主要目的是为客户提供延长容器使用寿命的选择,从而解决普遍存在的塑胶污染问题。补充包装提供的不仅是初始成本,更强调这项初始成本的长期回报,使经营模式更具永续性。透过强调补充包装的环境效益,公司可以提高品牌忠诚度并吸引特定的细分市场。

- 全球对永续性的关注正在增加对可重复使用包装解决方案的需求。这些选择不仅限制废弃物,而且支持循环经济。汽车和製药等不同行业正在转向可重复使用的包装选项。物流和运输业也透过使用可重复使用的托盘和板条箱来运输货物来减少包装废弃物。

- 可重复使用的产品可大幅减少生态废弃物并提供永续的解决方案。在食品和饮料行业,它可确保更安全的运输,有助于减少固态废弃物并增强产品保护。可重复使用的包装系统在保护自然资源方面发挥着至关重要的作用。透过选择重复利用而不是不断生产新材料,公司不仅可以延长包装的使用寿命,还可以减少对木材、油和水等新鲜原料的需求。

- 塑胶面临着日益严峻的环境挑战,但其弹性和多功能性巩固了其在严重依赖塑胶容器和托盘的零售、物流和汽车行业中作为可重复使用包装材料的作用。

补充装和可重复使用包装市场趋势

托盘和木箱的预期成长

- 托盘具有刚性形状,可在处理散装货物时提供机械稳定性并保持品质。搬运是指与起重、堆放、储存产品以及透过陆地或海上运输产品相关的所有活动。塑胶托盘被开发用于透过堆高机、托盘搬运车和前置装载机等设备移动,以方便货物的移动。塑胶托盘具有许多优点,包括重量轻、卫生且经济高效。企业可以根据自己的需求从多种塑胶托盘设计中进行选择。塑胶托盘常见于仓库、工厂、商店、运输公司等。

- 电子商务的日益普及导致物流活动的扩大,导致全球托盘的需求急剧增加。此外,有组织的零售业的日益渗透预计也将推动托盘需求,因为托盘被广泛用于零售空间中的重型货物装卸。

- 该行业的各种公司都致力于透过收购和合作来扩大业务。例如,Hine Group 于 2024 年 4 月宣布,将透过收购位于布里斯班附近纳兰巴的 Express Pallets and Crate (Express) 来拓展新的业务部门。 Hein此次收购涉及Express Pallets & Crates的资产和贸易业务。 Express 拥有庞大的基本客群,在各个细分市场中建立了重要的长期合作关係。

- 塑胶托盘和板条箱具有许多优点,包括比木材优越的强度和耐用性。它在高重复、封闭式场景中表现出色,并具有木栈板无法比拟的坚固性。与木材不同,塑胶托盘和塑胶盒没有钉子或锋利的边缘,并且在手动搬运过程中不存在碎裂或鬆动的风险。

- 根据Modern 物料输送统计,2023年托盘市场收入为906.1亿美元,预计2024年将达到952.3亿美元。电子商务的爆炸式增长推动了对托盘和板条箱的需求增加,这对于运输从消费品到工业零件的各种产品至关重要。这种成长迫使零售商和製造商扩大仓库并加强库存。产品製造商通常购买或租赁托盘并将其计入运输包装成本。相反,当零售商面临托盘短缺时,回收商就会介入,维修并转售这些关键的运输资产。

亚太地区预计将推动市场

- 亚太地区由于重视环境因素和对永续实践的承诺,成为包装产业的成熟地区之一。人们对生态保育的认识和兴趣的提高正在增加补充装和可重复使用包装在该地区的主导地位。

- 政府的措施和立法主要透过颁布环境法规和鼓励公司使用永续包装技术,使该地区的再填充和可重复使用包装产业得以扩大。根据环境、森林和气候变迁部 2023 年 7 月发布的塑胶包装生产者延伸责任 (EPR) 指南,要求重复使用硬质塑胶包装,并遵守印度食品安全和标准局针对食品接触制定的法规这是强制性的。 EPR 指南还鼓励永续塑胶包装并减少塑胶足迹。

- 与印度和中国等国家的全球贸易增加也可能推动可重复使用包装市场的发展。根据国际贸易管理局(ITA)预测,到2024年3月,印度将成为世界上成长最快的重要经济体之一。美国和印度之间的关係依然牢固,商品和服务贸易总额到 2022 年迅速增至 1,910 亿美元,约为 2014 年的两倍。 2022年4月1日至2023年3月31日的财政年度,印度经济成长7.2%。特别是特伦甘纳邦、安得拉邦、泰米尔纳德邦、卡纳塔克邦和喀拉拉邦的成长率明显高于全国平均水平,达到8%至9%。

- 据印度品牌股权基金会(IBEF)称,印度的化学工业高度多元化,大致分为散装、特殊、农业化学品、石化产品、聚合物和化肥。印度是世界第六大化学品生产国、亚洲第三大化学品生产国,占GDP的7%。

- 此外,根据印度经济顾问办公室(OEA)的数据,印度化学品和化学产品批发价格指数为133.5。 2023年将达145.4。在全球范围内,印度是继美国、日本和中国之后的第四大农药生产国。 2023年4月至2023年12月印度农药出口额估计为31.2亿美元。印度在化学品出口和进口方面均处于强势地位,出口排名第 14 位,进口排名第 8 位(不包括药品)。

补充和可重复使用包装行业概述

补充装和可重复使用包装市场较为分散,公司众多,包括: Schoeller Allibert Services BV、International Paper、Mondi PLC、Amcor PLC、Berry Global Inc. 和 Smurfit Kappa Group。

- 2024 年 2 月 欧洲领先的玻璃包装製造商之一 Brau Union Osterreich 和 Vetropack Group 推出了一款新型可重复使用的 0.33 公升可回收瓶。它作为啤酒行业的标准解决方案投放市场。

- 2023 年 9 月 Mondi PLC 和 Veete 在英国推出首款纸质干冰包装。 Veetee 的新型大米包装采用 Mondi 的功能屏障纸製成,为标准塑胶包装提供安全、可靠且坚固的包装替代品。 Veetee 和 Mondi 在英国推出了首款纸质干冰替代品,专门针对消费者对更永续包装的需求而量身定制。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

第五章市场动态

- 市场驱动因素

- 对永续和可回收再填充包装的需求不断增长

- 对智慧、可追溯和可重复使用的包装解决方案的需求不断增长

- 市场限制因素

- 供应链中断和监管变化可能会限制市场成长

第六章 市场细分

- 按材质

- 塑胶

- 纸板

- 金属

- 玻璃

- 副产品

- 瓶子/容器

- 托盘/木框架

- IBC

- 鼓桶

- 盒子/纸箱

- 罐/桶

- 其他产品(管、袋、袋子、麻袋等)

- 按最终用户产业

- 饮食

- 化妆品/个人护理

- 家居用品

- 化学/石化

- 建筑/施工

- 运输/运输

- 其他最终用户产业(汽车、製药等)

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Schoeller Allibert Services BV

- International Paper

- Nefab Group

- IPL Inc.

- Vetropack Holding Ltd

- Mondi PLC

- Greif Inc.

- Berry Global Inc.

- IFCO Systems

- Smurfit Kappa Group

- GWP Group

- Orbis Corporation

- Petainer Ltd

- Refillism

- Amcor PLC

- Bormioli Luigi Corporation

- Jiangmen UA Packaging Co. Ltd

第八章投资分析

第九章 市场未来展望

The Refillable And Reusable Packaging Market size is estimated at USD 45.67 billion in 2024, and is expected to reach USD 52.20 billion by 2029, growing at a CAGR of 4.43% during the forecast period (2024-2029).

The refillable and reusable packaging market is witnessing a notable surge, propelled by a global shift towards sustainability and heightened environmental consciousness. Governments worldwide are rolling out stringent regulations, and with international trade on the rise, the demand for refillable and reusable packaging is being further catalyzed. Factors such as curbing single-use packaging waste, enhancing economic efficiency, and ensuring packaging safety contribute to the market's growth.

Key Highlights

- The refillable packaging is a sustainable solution that allows multiple product refills, significantly reducing waste compared to single-use items. This trend is particularly prominent in food and beverage, household cleaning, personal hygiene, and other consumables.

- The main goal of refillable packaging is to provide customers with the choice to prolong the life of their containers, therefore tackling the widespread problem of plastic pollution. Refillable packaging offers more than an initial cost, and emphasizing the long-term returns on this upfront cost enhances the business model's sustainability. By highlighting the environmental benefits of refillable packaging, businesses can boost brand loyalty and draw a specific market segment.

- The global emphasis on sustainability has propelled the demand for reusable packaging solutions. These alternatives not only curb waste but also support a circular economy. Various industries, such as automotive and pharmaceutical, have started opting for reusable packing options. The logistics and transportation industry also reduced their packing waste by using pallets and crates to transport goods, which can be reused.

- Reusable products have significantly curbed ecosystem waste, offering a sustainable solution. In the food and beverage sector, they ensure safer transportation, aid in solid waste reduction, and enhance product protection. Reusable packaging systems play a pivotal role in conserving the natural resources. By opting for reuse over the constant production of new materials, businesses not only extend the life of their packaging but also curb the need for fresh raw materials like timber, petroleum, or water.

- While plastic faces mounting environmental concerns, its resiliency and versatility have cemented its role in reusable packaging in retail, logistics, and automotive industries, which lean heavily on plastic containers and pallets.

Refillable And Reusable Packaging Market Trends

Pallets and Crates are Expected to Witness Growth

- Pallets are rigid forms that provide mechanical stability to bulk goods during handling to preserve quality. Handling comprises all activities related to lifting, stacking, product storage, and transportation by land or sea. Plastic pallets are developed to be moveable by equipment such as forklifts, pallet jacks, and front loaders to facilitate the mobility of goods. Plastic pallets have many advantages, such as being lightweight, hygienic, and cost-effective. A business may choose from several plastic pallet designs depending on their needs. Plastic pallets can be noticed in warehouses, factories, stores, and shipping companies.

- The increasing popularity of e-commerce resulted in the expansion of logistics activities, which, in turn, surged the demand for pallets worldwide. Furthermore, the rising penetration of organized retail is anticipated to drive the demand for pallets, as these are widely used in retail spaces for the loading and unloading of heavy merchandise.

- Various companies operating in the industry are focused on expanding their business through acquisitions, collaborations, and more. For instance, in April 2024, Hyne Group announced the expansion of its new operating division with the acquisition of Express Pallets and Crates (Express), based at Narangba near Brisbane. Hyne's acquisition involves the assets and trading business of Express Pallets & Crates. Express has a vast client base with significant long-term relationships across various market segments.

- Plastic pallets and crates have many benefits, such as outshining wood in strength and durability. They excel in high-repeat, closed-loop scenarios, offering robustness that wooden counterparts struggle to match. Unlike their wooden counterparts, plastic pallets and boxes are crafted without nails or sharp edges, eliminating the risk of splinters or loose parts during manual handling.

- According to Modern Materials Handling, the revenue of the pallet market in 2023 was USD 90.61 billion, and it is expected to reach USD 95.23 billion in 2024. The surge in e-commerce is fueling a rising demand for pallets and crates, essential for transporting diverse products, from consumer goods to industrial components. This uptick is prompting retailers and manufacturers to enlarge their warehouses and bolster their inventory. Generally, product manufacturers purchase or lease pallets, factoring them into transportation packaging costs. Conversely, when retailers face a shortage of pallets, recycling firms step in, refurbishing and reselling these essential transport assets.

Asia-Pacific is Expected to Drive the Market

- Asia-Pacific is one of the established regions in the packaging industry due to reasons highlighting environmental care and commitment to sustainable practices. Growing awareness and concern for ecological conservation drive the region's refillable and reusable packaging dominance.

- Government initiatives and legislation have primarily enabled the expansion of the region's refillable and reusable packaging industry by enacting environmental regulations and encouraging companies to use sustainable packaging techniques. According to the Ministry of Environment, Forest and Climate Change in July 2023, the Extended Producer's Responsibility (EPR) guidelines on plastic packaging mandate the reuse of rigid plastic packaging, subject to the regulations specified by the Food Safety and Standards Authority of India for food contact applications. The EPR guidelines also encourage sustainable plastic packaging, thus reducing the plastic footprint.

- Increasing trade with countries such as India and China globally will also push the market for reusable packaging. According to the International Trade Administration (ITA), in March 2024, India stood out as one of the swiftest expanding significant economies worldwide. The US-India ties, robust as ever, saw their combined trade in goods and services soar to a noteworthy USD 191 billion in 2022, nearly doubling the figures from 2014. For the fiscal year spanning April 1, 2022, to March 31, 2023, the Indian economy surged by 7.2%. Notably, Telangana, Andhra Pradesh, Tamil Nadu, Karnataka, and Kerala outshone the national average, boasting a remarkable growth rate of 8% to 9%.

- According to the India Brand Equity Foundation (IBEF), covering more than 80,000 commercial products, India's chemical industry is highly diversified and can be broadly categorized into bulk, specialty, agrochemicals, petrochemicals, polymers, and fertilizers. India is the sixth largest producer of chemicals globally and third in Asia, contributing 7% to its GDP.

- Further, according to the Office of Economic Advisor (OEA) India, the wholesale price index of chemicals and chemical products in India was 133.5. It reached 145.4 in 2023. Globally, India is the fourth-largest producer of agrochemicals after the United States, Japan, and China. From April 2023 to December 2023, India's agrochemicals exports were estimated at USD 3.12 billion. India holds a strong position in chemical exports and imports and ranks 14th in exports and 8th in imports (excluding pharmaceuticals).

Refillable And Reusable Packaging Industry Overview

The refillable and reusable packaging market is fragmented, with various players such as Schoeller Allibert Services BV, International Paper, Mondi PLC, Amcor PLC, Berry Global Inc., and Smurfit Kappa Group. The players are focused on expanding their business in the region through acquisitions, collaborations, mergers, and more.

- February 2024: Brau Union Osterreich and Vetropack Group, one of Europe's manufacturers of glass packaging, launched a new 0.33-liter returnable bottle that can be reused. It was launched on the market as a standard solution for the brewing industry.

- September 2023: Mondi PLC and Veete launched the first paper-based packaging for dry ice in the United Kingdom. Veetee's new rice packaging has been created using Mondi's FunctionalBarrier Paper, providing a safe, secure, and robust alternative to standard plastic packs. Veetee and Mondi were the first in the United Kingdom to launch a paper-based alternative for dry rice, customized in direct response to consumer demands for more sustainable packaging.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Sustainable and Recyclable Refillable Packaging

- 5.1.2 Increasing Need for Smart and Trackable Reusable Packaging Solutions

- 5.2 Market Restraints

- 5.2.1 Supply Chain Disruptions and Regulatory Changes Might Limit the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.2 Paper and Paperboard

- 6.1.3 Metal

- 6.1.4 Glass

- 6.2 By Product

- 6.2.1 Bottles and Containers

- 6.2.2 Pallets and Crates

- 6.2.3 IBCs

- 6.2.4 Drums and Barrels

- 6.2.5 Boxes and Cartons

- 6.2.6 Cans and Pails

- 6.2.7 Others Products (Tubes, Pouches, Bags and Sacks, Etc.)

- 6.3 By End-user Industry

- 6.3.1 Food and Beverage

- 6.3.2 Cosmetics and Personal Care

- 6.3.3 Household Care

- 6.3.4 Chemicals and Petrochemicals

- 6.3.5 Building and Construction

- 6.3.6 Shipping and Transportation

- 6.3.7 Other End-user Industries (Automotive, Pharmaceuticals, Etc.)

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schoeller Allibert Services BV

- 7.1.2 International Paper

- 7.1.3 Nefab Group

- 7.1.4 IPL Inc.

- 7.1.5 Vetropack Holding Ltd

- 7.1.6 Mondi PLC

- 7.1.7 Greif Inc.

- 7.1.8 Berry Global Inc.

- 7.1.9 IFCO Systems

- 7.1.10 Smurfit Kappa Group

- 7.1.11 GWP Group

- 7.1.12 Orbis Corporation

- 7.1.13 Petainer Ltd

- 7.1.14 Refillism

- 7.1.15 Amcor PLC

- 7.1.16 Bormioli Luigi Corporation

- 7.1.17 Jiangmen UA Packaging Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

全球可填充和可重复使用包装市场:预测至 2032 年—按产品、材料、分销管道、最终用户和地区分類的分析可重复填充和可重复使用包装解决方案市场预测至2032年:按产品、材料、分销管道、最终用户和地区分類的全球分析

全球可填充和可重复使用包装市场:预测至 2032 年—按产品、材料、分销管道、最终用户和地区分類的分析可重复填充和可重复使用包装解决方案市场预测至2032年:按产品、材料、分销管道、最终用户和地区分類的全球分析 可重复使用包装市场规模、份额、趋势分析报告:按材料、产品类型、最终用途、地区和细分市场预测,2025-2030 年

可重复使用包装市场规模、份额、趋势分析报告:按材料、产品类型、最终用途、地区和细分市场预测,2025-2030 年 可重复使用的电子商务包装市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

可重复使用的电子商务包装市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 速食可重复使用包装市场 - 全球产业分析、规模、占有率、成长、趋势及2032年预测可重复使用包装市场机会、成长动力、产业趋势分析与预测 2024 - 2032

速食可重复使用包装市场 - 全球产业分析、规模、占有率、成长、趋势及2032年预测可重复使用包装市场机会、成长动力、产业趋势分析与预测 2024 - 2032 再填充和可重复使用包装的全球市场的未来(~2029年)

再填充和可重复使用包装的全球市场的未来(~2029年) 速食可重复使用包装市场:依产品类型、最终用户、地区(北美、欧洲、亚太地区、拉丁美洲、中东非洲):全球产业分析、规模、占有率、成长、趋势,2023-2030 年预测

速食可重复使用包装市场:依产品类型、最终用户、地区(北美、欧洲、亚太地区、拉丁美洲、中东非洲):全球产业分析、规模、占有率、成长、趋势,2023-2030 年预测