|

市场调查报告书

商品编码

1549891

全球工业自动化市场:市场占有率分析、产业趋势/统计、成长预测(2024-2029)Industrial Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

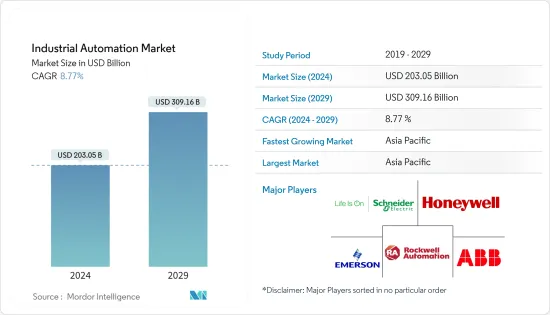

根据预测,2024年全球工业自动化市场规模预估为2,030.5亿美元,2029年达3,091.6亿美元,预测期间(2024-2029年)复合年增长率为8.77%。

主要亮点

- 工业自动化有潜力提高开发中国家的出口竞争力。透过自动化製造流程,这些国家可以更快、更有效、更便宜地生产商品,在全球市场上更具竞争力。因此,新兴经济体的工业自动化市场将受到刺激,出口水准提高,外汇收入改善,新兴经济体或将改善。

- 工业自动化对开发中国家的中小企业有重大影响。自动化有潜力使这些公司更具竞争力并实现永续成长。它使中小型企业能够提高生产力、简化业务并满足大客户和供应链的需求。例如,工业自动化可以优化资源并减少生产时间,从而腾出人员来执行策略业务。根据国际机器人联合会 (IFR) 的数据,製造公司可以透过自动化多个流程将生产力提高高达 30%。

- 根据国际货币基金组织 (IMF) 的数据,新兴市场和经济体 2024 年和 2025 年的成长预计为 4.2%,而 2023 年为 4.3%。在印度等许多新兴国家,印度政府的多项倡议,如印度市场的报废政策、2026年汽车使命计划以及与生产连结奖励计画计划,使印度成为两轮和四轮车市场的重要参与者。 。这些政策包括采用自动化技术和创造有利于市场研究的环境。

- 自动化设备需要智慧製造的高资本投资(自动化系统的安装、设计和製造可能花费数百万美元)。购买机器人系统、输送机、感测器和控制系统等设备的成本可能很高。工厂自动化设备还需要客製化并整合到现有生产系统中。该过程涉及设备的设计、工程和编程,以满足特定的製造要求。这是所研究市场成长的主要障碍。

- 除了对工业自动化解决方案的供应链和生产的直接影响外,疫情的后遗症也影响了所研究市场的成长。例如,包括北美在内的各个地区迫在眉睫的景气衰退威胁正在对所研究市场的成长产生负面影响,因为经济不确定性阻碍了消费者和企业增加汽车等大件产品的支出,而扩建计划可能会受到影响。

工业自动化市场趋势

石油和天然气产业预计将显着成长

- 石油和天然气产业是迄今为止实施工业自动化解决方案的领域。然而,与其他发展中产业相比,该产业的工业自动化成长前景有限,因此预计该产业的成长速度将放缓。

- 石油和天然气自动化(也称为油田自动化)是一组由数位技术驱动的流程,旨在提高能源生产商在全球市场的竞争力。虽然产业内的某些部门将实现更大程度的自动化,但关键领域包括钻井、生产业务、物流、安全和零售业务。石油和天然气自动化主要依靠基于物联网的感测器、预测系统和人工智慧专家系统来提高生产力并缩小劳动力短缺造成的技能差距。

- 石油和天然气产业的危险环境日益透过自动化得到改善。机器人和自动化系统处理挖掘、检查和维护等任务,大大减少了人类面临的风险。

- 该行业正在透过紧急关闭系统等自动化功能来增强安全性,并确保对困难情况做出快速反应。透过部署感测器和自动化工具,公司可以确保合规性并减少对环境的影响。

- 石油和天然气工业是全球经济的重要组成部分。 IEA 预计,2024 年全球液体燃料产量将放缓至80 万桶/日,较2023 年180 万桶/日的增幅有所放缓,因为OPEC+ 自愿减产被非OPEC+ 供应增量超过100 万桶/日所抵销。儘管2024年OPEC+原油产量预计将年减90万桶/与前一年同期比较,但非OPEC+产量预计将增加180万桶/日,其中以美国、圭亚那、巴西和加拿大为首。随着石油产量的大幅增加数位化的提高,石油和燃气公司越来越依赖数位技术和自动化。

亚太地区预计将录得最快成长

- 亚太地区是世界上最大的製造业经济体的所在地,包括中国、日本、韩国和台湾。汽车、电子、航太、医疗设备等製造业的持续扩张正在创造对工业自动化的巨大需求。

- 印度等新兴国家扩大製造业和实现自力更生的努力进一步推动了市场成长。製造业已成为印度高成长产业之一。 「印度製造」计画使印度成为世界地图上的製造中心,并让印度经济获得全球认可。 IBEF 预计,到 2030 年,印度将出口价值 1 兆美元的商品,预计将成为世界主要製造中心。

- 印度政府的目标是到2025年经济规模达到5兆美元,其中製造业价值1兆美元。为了实现这一目标,印度製造、印度技能和数位印度等旗舰计画的整合至关重要,这将推动该地区的市场成长。

- 为加速电动车的采用而建造电池製造厂的持续倡议进一步支持了市场成长。例如,Recharge Industries于2023年8月宣布,计划兴建一座年产能30吉瓦时的工厂,为约30万辆电动车供应电池。建设计划于 2024 年 5 月左右开始,生产计划于 2025 年开始。

- 由于台积电等公司的存在,该地区是最大的半导体和电子产品製造商。台湾生产全球60%以上的半导体,以及90%以上最先进的半导体。大部分半导体由台积电生产。

工业自动化产业概况

由于中小企业和跨国公司的存在,工业自动化市场高度分散。该市场的主要企业包括Schneider Electric、罗克韦尔自动化、Honeywell国际、艾默生电气和 ABB 有限公司。市场上的主要企业正在采取收购和合作等策略来加强其产品范围并获得永续的竞争优势。

- 2024 年 6 月 - 罗克韦尔自动化宣布与 NVIDIA 合作,加速开发更安全、更智慧的工业 AI 移动机器人。此次合作预计将加速人工智慧在自主移动机器人(AMR)的应用,并提高其效能和效率。

- 2024 年 2 月 -Schneider Electric与科技巨头英特尔和红帽公司合作,宣布推出新的软体框架:分散式控制节点 (DCN)。此创新框架基于Schneider Electric的 EcoStruxure Automation Expert 构建,可帮助工业公司转向软体定义的即插即用模型。这种转变提高了业务效率和质量,并简化了流程,最终节省了成本。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 技术趋势/进展

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

- 产业价值链分析

- 市场宏观趋势分析

第五章市场动态

- 市场驱动因素

- 新兴经济体工业活动的成长

- 人们对能源效率和降低成本的兴趣日益浓厚

- 市场限制

- 安装/改造成本高

第六章 市场细分

- 按解决方案

- 工业控制系统

- 集散控制系统(DCS)

- 监控/资料采集 (SCADA)

- 可程式逻辑控制器(PLC)

- 人机介面 (HMI)

- 其他控制系统

- 现场设备

- 感测器和发射器

- 阀门和致动器

- 马达和驱动器

- 机器人

- 其他现场设备

- 软体

- 产品生命週期管理 (PLM)

- 企业资源规划(ERP)

- 製造执行系统(MES)

- 其他软体

- 工业控制系统

- 按最终用户产业

- 石油和天然气

- 製药

- 汽车/交通

- 饮食

- 电力/公共产业

- 化工/石化

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Schneider Electric SE

- Rockwell Automation Inc.

- Honeywell International Inc.

- Emerson Electric Co.

- ABB Limited

- Mitsubishi Electric Corporation

- Siemens AG

- Omron Corporation

- Yokogawa Electric Corporation

- Yaskawa Electric Corporation

- Kuka Aktiengesellschaft

- Fanuc Corporation

- Regal Rexnord Corporation

- Nidec Corporation

- Basler AG

第八章投资分析

第9章市场的未来

The Industrial Automation Market size is estimated at USD 203.05 billion in 2024, and is expected to reach USD 309.16 billion by 2029, growing at a CAGR of 8.77% during the forecast period (2024-2029).

Key Highlights

- Industrial automation may potentially and considerably increase export competitiveness in developing nations. By automating their manufacturing processes, these nations can create items more quickly, effectively, and affordably, which boosts their ability to compete in the global market. This may result in higher levels of exports, better foreign currency revenues, and an improvement in the emerging economy, hence driving the market for industrial automation in developing countries.

- Industrial automation significantly impacts small and medium-sized firms (SMEs) in developing nations. Automation may boost these companies' competitiveness and achieve sustained growth. It enables SMEs to improve productivity, streamline operations, and satisfy the needs of larger customers and supply chains. For instance, Industrial automation optimizes resources and reduces production times, freeing personnel for strategic tasks. According to the International Federation of Robotics (IFR), productivity increases by up to 30% in manufacturing with automation in multiple processes.

- According to the International Monetary Fund (IMF), growth rates for emerging markets and developing economies are projected to be 4.2% in 2024 and 2025 compared to 4.3% in 2023. In many developing countries such as India, several initiatives by the Government of India, like the scrappage policy, Automotive Mission Plan 2026, and production-linked incentive scheme in the Indian market, are expected to make India a significant player in the two-wheeler and four-wheeler market. Such policies include adopting automation technologies and fostering a favorable environment for the market studied.

- Automation equipment mandates high capital investment to fund smart manufacturing (an automated system may cost millions of dollars to install, design, and fabricate). The cost of purchasing the equipment, including robotic systems, conveyor belts, sensors, and control systems, can be substantial. The factory automation equipment also necessitates the customization and integration into existing production systems. This process involves designing, engineering, and programming the equipment to meet specific manufacturing requirements. This poses a significant hindrance to the growth of the market studied.

- Apart from the direct impact evident in the supply chains and production of industrial automation solutions, the aftereffects of the pandemic are also impacting the growth of the studied market. For instance, the ongoing threat of recession looming over various regions, including North America, may negatively influence the studied market's growth as the economic uncertainty will prevent consumers and businesses from spending more on high-value products such as automobiles and expansion projects, which may impact the growth of the market studied.

Industrial Automation Market Trends

Oil and Gas Industry to Witness Significant Growth

- The oil and gas industry has been a dominating segment in adopting industrial automation solutions. However, the growth prospects for industrial automation in this industry are limited compared to other developing industries, and therefore, the growth rate is expected to slow in this industry.

- Oil and gas automation, also known as oilfield automation, is a set of processes, many leveraging digital technologies, aimed at enhancing the competitiveness of energy producers in global markets. While certain sectors within the industry are more primed for automation, key areas include drilling, production operations, logistics, safety, and retail operations. Oil and gas automation predominantly relies on IoT-based sensors, predictive systems, and AI-driven expert systems to boost productivity and bridge skill gaps arising from labor shortages.

- The oil and gas industry's hazardous environments are increasingly being navigated through automation. Robots and automated systems handle tasks like drilling, inspection, and maintenance, significantly reducing human exposure to risks.

- The industry is bolstering safety with automated features like emergency shutdown systems, guaranteeing swift responses to difficult situations. By deploying sensors and automated tools, companies are ensuring compliance with regulations and curbing their environmental footprint.

- The oil and gas industry is a vital component of the global economy. As per IEA, global production of liquid fuels will increase by more than 0.8 million b/d in 2024, slowing from the 1.8 million b/d increase in 2023, as OPEC+ voluntary production cuts are offset by supply growth outside of OPEC+. Although OPEC+ crude oil production in 2024 decreases by 0.9 million b/d compared with last year, forecast production outside of OPEC+ increased by 1.8 million b/d, led by the United States, Guyana, Brazil, and Canada. With significant surge in oil production and surging digitization, oil and gas companies have increasingly relied on digital technology and automation.

Asia-Pacific is Expected to Register the Fastest Growth

- Asia-Pacific is home to some of the world's largest manufacturing economies, including China, Japan, South Korea, and Taiwan. The ongoing expansion of manufacturing industries in automotive, electronics, aerospace, and medical devices creates a significant demand for industrial automation.

- Initiatives by emerging countries like India to expand their manufacturing footprint and become self-reliant further propel the market growth. Manufacturing emerged as one of the high-growth sectors in India. The 'Make in India' program places India on the global map as a manufacturing hub and globally recognizes the Indian economy. According to IBEF, India can export goods worth USD 1 trillion by 2030 and is on the road to becoming a significant global manufacturing hub.

- The government of India aims for a USD 5 trillion economy by 2025, of which manufacturing would be worth USD 1 trillion. The convergence of flagship programs, such as Make in India with Skill India and Digital India, would be vital to achieving this goal, thereby driving the region's market growth.

- The ongoing initiatives to build a battery manufacturing plant for faster adoption of electric vehicles are further driving the market growth. For instance, in August 2023, Recharge Industries announced its plans to build a factory with an annual capacity of 30 gigawatt-hours to supply batteries for roughly 300,000 EVs. Construction is expected to begin around May 2024, with production slated to start in 2025.

- The region is the biggest semiconductor and electronics product manufacturer due to the presence of companies like Taiwan Semiconductor Manufacturing Company. Taiwan produces over 60% of the world's semiconductors and over 90% of the most advanced ones. Most of the semiconductors are manufactured by TSMC.

Industrial Automation Industry Overview

The industrial automation market is highly fragmented due to the presence of small and medium-sized enterprises and global players. Some of the major players in the market are Schneider Electric SE, Rockwell Automation Inc., Honeywell International Inc., Emerson Electric Co., and ABB Limited. Key players in the market are adopting strategies such as acquisitions and partnerships to enhance their product offerings and gain sustainable competitive advantage.

- June 2024 - Rockwell Automation announced a partnership with NVIDIA to expedite the development of safer and smarter industrial AI mobile robots. The collaboration is anticipated to drive the use of AI in autonomous mobile robots (AMRs), improving their performance and efficiency.

- February 2024 - Schneider Electric, in partnership with tech giants Intel and Red Hat, unveiled a new software framework, the Distributed Control Node (DCN). Building upon Schneider Electric's EcoStruxure Automation Expert, this innovative framework empowers industrial firms to transition to a software-defined, plug-and-play model. This shift boosts operational efficiency and quality and streamlines processes, ultimately leading to cost savings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends/Advancements

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Degree of Competition

- 4.4 Industry Value Chain Analysis

- 4.5 Analysis of the Macro Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth of Industrial Activities in Developing Economies

- 5.1.2 Growing Emphasis on Energy Efficiency and Cost Reduction

- 5.2 Market Restrains

- 5.2.1 High Cost of Installation and Re-building

6 MARKET SEGMENTATION

- 6.1 By Solution

- 6.1.1 Industrial Control Systems

- 6.1.1.1 Distributed Control System (DCS)

- 6.1.1.2 Supervisory Control and Data Acquisition (SCADA)

- 6.1.1.3 Programmable Logic Controller (PLC)

- 6.1.1.4 Human-machine Interface (HMI)

- 6.1.1.5 Other Control Systems

- 6.1.2 Field Devices

- 6.1.2.1 Sensors and Transmitters

- 6.1.2.2 Valves and Actuators

- 6.1.2.3 Motors and Drives

- 6.1.2.4 Robotics

- 6.1.2.5 Other Field Devices

- 6.1.3 Software

- 6.1.3.1 Product Lifecycle Management (PLM)

- 6.1.3.2 Enterprise Resource and Planning (ERP)

- 6.1.3.3 Manufacturing Execution System (MES)

- 6.1.3.4 Other Software

- 6.1.1 Industrial Control Systems

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Pharmaceuticals

- 6.2.3 Automotive and Transportation

- 6.2.4 Food and Beverage

- 6.2.5 Power and Utilities

- 6.2.6 Chemical and Petrochemical

- 6.2.7 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Rockwell Automation Inc.

- 7.1.3 Honeywell International Inc.

- 7.1.4 Emerson Electric Co.

- 7.1.5 ABB Limited

- 7.1.6 Mitsubishi Electric Corporation

- 7.1.7 Siemens AG

- 7.1.8 Omron Corporation

- 7.1.9 Yokogawa Electric Corporation

- 7.1.10 Yaskawa Electric Corporation

- 7.1.11 Kuka Aktiengesellschaft

- 7.1.12 Fanuc Corporation

- 7.1.13 Regal Rexnord Corporation

- 7.1.14 Nidec Corporation

- 7.1.15 Basler AG

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球自动化与控制市场报告

2026年全球自动化与控制市场报告 办公室寻呼系统市场按技术、组件类型、最终用户和部署模式划分,全球预测(2026-2032年)静电纺丝喷嘴市场按类型、技术、材料、应用和最终用途划分,全球预测(2026-2032年)全球钻屑管理系统市场依技术、钻井液类型、应用、服务模式及最终用途划分,2026-2032年预测工业声光讯号元件市场(按元件类型、技术、安装方式、额定电压、终端用户产业和应用划分),全球预测(2026-2032年)批量流处理器市场按应用、技术、终端用户产业、反应器类型、容量、操作模式和物料相划分,全球预测,2026-2032年

办公室寻呼系统市场按技术、组件类型、最终用户和部署模式划分,全球预测(2026-2032年)静电纺丝喷嘴市场按类型、技术、材料、应用和最终用途划分,全球预测(2026-2032年)全球钻屑管理系统市场依技术、钻井液类型、应用、服务模式及最终用途划分,2026-2032年预测工业声光讯号元件市场(按元件类型、技术、安装方式、额定电压、终端用户产业和应用划分),全球预测(2026-2032年)批量流处理器市场按应用、技术、终端用户产业、反应器类型、容量、操作模式和物料相划分,全球预测,2026-2032年 雷射清洗设备市场规模、份额及成长分析(依产品类型、技术类型、额定功率、应用、终端用户产业及地区划分)-2026-2033年产业预测全球工业自动化市场:机会与策略展望(至2034年)

雷射清洗设备市场规模、份额及成长分析(依产品类型、技术类型、额定功率、应用、终端用户产业及地区划分)-2026-2033年产业预测全球工业自动化市场:机会与策略展望(至2034年) 工业自动化市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和模式划分

工业自动化市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和模式划分 日本工业机器人软体市场规模、份额、趋势及预测(依软体类型、实施类型、功能、用途、最终用户产业及地区划分),2026-2034年

日本工业机器人软体市场规模、份额、趋势及预测(依软体类型、实施类型、功能、用途、最终用户产业及地区划分),2026-2034年