|

市场调查报告书

商品编码

1627130

奈米管:市场占有率分析、产业趋势、成长预测(2025-2030)Nanotubes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

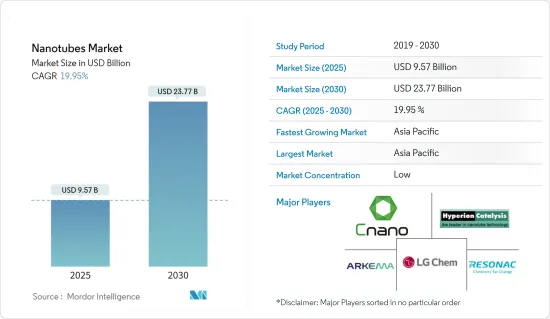

奈米管市场规模预计到2025年为95.7亿美元,预计到2030年将达到237.7亿美元,预测期内(2025-2030年)复合年增长率为19.95%。

奈米管市场 COVID-19大流行减缓了生产和运输,导致半导体短缺,这对奈米管市场产生了负面影响。由于遏制措施和经济中断,电子、能源和航太等产业也被迫放慢生产速度。目前市场正从疫情中恢復。预计2022年市场将达到疫情前水准并持续稳定成长。

推动所研究市场成长的主要因素是奈米管技术的进步和奈米碳管的日益普及。

另一方面,高昂的製造成本和研发成本是所研究市场成长的主要障碍。

在预测期内,电子设备和储存设备中潜在应用的增加可能会为所研究的市场提供机会。

亚太地区在全球市场中占据主导地位,电子、能源、航太和国防等产业不断增长的应用和需求在很大程度上推动了对奈米管的需求。

奈米管市场趋势

电子和半导体领域主导市场需求

- 奈米管已广泛应用于电子产业,用于开发更快、更有效率、更耐用的电子设备。

- 在所有类型的奈米管中,奈米碳管由于其在电子工业中的应用而引领市场需求。除奈米碳管外,硅奈米管和无机奈米管也用于电子工业。

- 奈米碳管用于显示器、大面积表面导电、彩色电致发光显示器、感测器、显示器背光源、行波管、电晶体、光伏、非显示应用的导电添加剂、光电、射频识别(应用于RFID)标籤、中子源、伽玛射线源、照明设备等

- 硅奈米管含有氢分子,起到金属燃料的作用。因此,它被广泛用于电子工业的半导体应用。

- 无机奈米管也用于电子工业中的半导体装置、感测器、生物感测器、马达和平板显示器。因此,由于奈米管在多种电子元件中的广泛应用,预计对奈米管的需求将会增加。

- 电气和电子行业使用量的增加和应用领域的扩大预计将推动市场成长。

- 例如,根据日本电子情报技术产业协会(JEITA)的数据,2022年全球电子资讯科技产业产值预计为34,368亿美元,而2021与前一年同期比较。此外,预计2023年将达35,266亿美元,与前一年同期比较成长3%。

- 根据半导体产业协会(SIA)的数据,2022年全球半导体产业销售额为5,741亿美元,较2021年的5,559亿美元成长3.3%。

- 此外,依地区划分,美洲市场2022年销售额增幅最大(16.2%)。中国仍是最大的半导体市场,2022年销售额较2021年下降6.2%至1804亿美元。此外,欧洲(12.8%)和日本(10.2%)2022年的年销售额也有所成长。

- 预计这种增长将增加预测期内该地区电子应用对奈米管的需求。

亚太地区主导市场

- 由于电子、能源、医疗保健、航太和国防以及汽车等行业的需求不断增长,亚太地区在全球市场占有率中占据主导地位。

- 根据日本电子情报技术产业协会(JEITA)预测,2022年日本电子产业国内产值预估与前一年同期比较111,243亿日圆(851.9亿美元),年成长率为2%。 2023年,日本电子业的国内产值与前一年同期比较将达到114,029亿日圆(873.2亿美元),年成长率为3%。

- 此外,根据电子与资讯科技部的数据,2022 财年印度消费性电子产品(电视、配件、音讯)产值将超过 7,450 亿印度卢比(94.6 亿美元)。这就是我们支持市场成长的方式。

- 此外,中国民用航空局(CAAC)预计,国内航空运输量将恢復至疫情前水准的85%左右。根据波音《2023-2042年商业展望》,到2042年,中国将交付约8,560架新飞机,到2042年,市场服务价值将达到6,750亿美元。这些新的交付预计将增加飞机领域对奈米管的需求。

- 此外,亚太地区汽车工业的成长进一步推动了市场成长。中国、印度、日本、韩国等新兴国家正专注于加强製造基础、发展高效供应链,以提高汽车製造的盈利。

- 中国政府的政策发展包括限制对新内燃机汽车製造厂的投资,以及 2025 年收紧轻型乘用车平均燃油经济性的提案。

- 此外,根据印度汽车工业商协会(SIAM)的数据,2022年印度乘用车销量为379万辆,较2021年销量成长约23%。

- 此外,中国民航局预计国内航空运输量将恢復至疫情前85%左右的水准。根据波音《2023-2042年商业展望》,到2042年,中国将交付约8,560架新飞机,到2042年,市场服务价值将达到6,750亿美元。

- 因此,预计上述趋势将在预测期内推动该地区的奈米管需求。

奈米管产业概况

奈米管市场是分散的。研究市场的主要企业包括(排名不分先后)阿科玛、Hyperion Catalysis International、江苏纳诺科技、Resonac Holdings Corporation、LG Chem等。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 促进因素

- 奈米管技术的进步

- 扩大奈米碳管的采用

- 其他司机

- 抑制因素

- 製造和研发成本高

- 其他阻碍因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争程度

第五章市场区隔(以金额为准的市场规模)

- 按类型

- 奈米碳管

- 硅奈米管

- 无机奈米管

- 其他类型(例如膜奈米管)

- 依结构类型分

- 非聚合有机奈米材料

- 高分子奈米材料

- 按用途

- 储氢装置

- 感应器

- 高分子生物材料

- 锂离子电池

- 发光显示装置

- 生物感测器

- 奈米电极

- 水质净化过滤器

- 半导体装置

- 导电塑料

- 按最终用户产业

- 卫生保健

- 电子产品

- 活力

- 车

- 航太/国防

- 纤维

- 其他最终用户产业(例如化学材料)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲国家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲

- 亚太地区

第六章 竞争状况

- 併购、合资、联盟、协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Arkema

- Carbon Solutions Inc.

- Cheap Tubes

- Hyperion Catalysis International

- Jiangsu Cnano Technology Co., Ltd.

- Nano-C

- Nanocyl SA(Birla Carbon)

- NanoIntegris Inc.

- Nanoshel LLC

- Resonac Holdings Corporation

- Thomas Swan & Co. Ltd

- LG Chem

第七章 市场机会及未来趋势

- 增加电子和储存设备中的潜在应用

- 其他机会

The Nanotubes Market size is estimated at USD 9.57 billion in 2025, and is expected to reach USD 23.77 billion by 2030, at a CAGR of 19.95% during the forecast period (2025-2030).

The nanotubes market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility, which caused a shortage of semiconductors, which negatively impacted the market for nanotubes. Also, industries such as electronics, energy, and aerospace were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

The major factors driving the growth of the market studied are an advancement in nanotube technologies and the growing adoption of carbon nanotubes.

On the flip side, high manufacturing and R&D costs serve as one of the major stumbling blocks in the growth of the market studied.

Rising potential uses in electronic and storage devices are likely to provide opportunities for the market studied during the forecast period.

Asia-Pacific dominated the global market, as the increasing application and demand from industries such as electronics, energy, aerospace, and defense majorly drive the demand for nanotubes.

Nanotubes Market Trends

Electronics and Semiconductor Segment to Dominate the Market Demand

- Nanotubes find extensive application in the electronics industry, for the development of faster, more efficient, and more durable electronic devices.

- Among all the types of nanotubes, carbon nanotubes lead the market demand due to their applications in the electronics industry. Apart from carbon nanotubes, silicon nanotubes, and inorganic nanotubes are also used in the electronics industry.

- Carbon nanotubes find application in displays, large area surface conduction, color field emission displays, sensors, backlights for displays, traveling wave tubes, transistors, photovoltaics, conductive additives for non-display applications, photonics, radio-frequency identification (RFID) tags, neutron, and gamma-ray sources, and lighting devices.

- Silicon nanotubes contain hydrogen molecules and act like metal fuels. Thus, they are widely used for semiconductor applications in the electronics industry.

- Inorganic nanotubes are also used in the electronics industry for application in semiconductor devices, sensors, biosensors, nano-motors, and flat panel displays. Hence, owing to the diversified application of nanotubes in several electronic components, the demand for nanotubes is expected to increase.

- The increasing usage and widening arena of application in the electrical and electronics industry is expected to drive market growth.

- For instance, according to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year on year, compared to USD 3,415.9 billion in 2021. Moreover, the industry is expected to reach USD 3,526.6 billion, with a growth rate of 3% year on year in 2023.

- According to the Semiconductor Industry Association (SIA), the global semiconductor industry sales totaled USD 574.1 billion in 2022, registering an increase of 3.3% compared to 2021 with USD 555.9 billion.

- Furthermore, on a regional basis, sales into the Americas market saw the largest increase (16.2%) in 2022. China remained the largest individual market for semiconductors, with sales there totaling USD 180.4 billion in 2022, a decrease of 6.2% compared to 2021. Moreover, annual sales also increased in 2022 in Europe (12.8%) and Japan (10.2%).

- This growth is expected to increase the demand for nanotubes for electronic applications in the region during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region dominated the global market share due to the increasing demand from industries such as electronics, energy, healthcare, aerospace and defense, and automotive.

- Japan is one of the largest producers of electronics; as per the Japan Electronics and Information Technology Industries Association (JEITA), the domestic production by the Japanese electronics industry was estimated at JPY 11,124.3 billion (USD 85.19 billion) in 2022, witnessing a growth rate of 2% compared to the previous year. The domestic production by the Japanese electronics industry is likely to reach JPY 11,402.9 billion (USD 87.32 billion) by 2023, registering a growth rate of 3% year-on-year.

- Moreover, according to the Ministry of Electronics and Information Technology, the production value of consumer electronics (TV, accessories, and audio) across India was above INR 745 billion (USD 9.46 billion) in fiscal year 2022. Thus supporting the growth of the market.

- Additionally, The Civil Aviation Administration of China (CAAC) has estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels. According to the Boeing Commercial Outlook 2023-2042, in China, around 8,560 new deliveries will be made by 2042, and the market service value will account for USD 675 billion by 2042. Owing to such new deliveries in the country, the demand for nanotubes in the aircraft sector will likely rise.

- Moreover, the market growth is further boosted by the growing automotive industry in the Asia-Pacific region. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability in vehicle manufacturing.

- The Chinese government policy developments include the restriction of investments in new ICE-vehicle manufacturing plants and a proposal to tighten the average fuel economy of its light-duty passenger vehicle fleet by 2025.

- In addition, according to the Society of Indian Automobile Manufacturers (SIAM), a total of 3.79 million passenger vehicles were sold in India in 2022, witnessing a growth rate of around 23% compared to the passenger vehicles sold in the year 2021.

- Additionally, The Civil Aviation Administration of China (CAAC) has estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels. According to the Boeing Commercial Outlook 2023-2042, in China, around 8,560 new deliveries will be made by 2042, and the market service value will account for USD 675 billion by 2042.

- Hence, the trends above are expected to drive the demand for nanotubes in the region during the forecast period.

Nanotubes Industry Overview

The nanotubes market is fragmented in nature. The major players in the studied market (not in any particular order) include Arkema, Hyperion Catalysis International, Jiangsu Cnano Technology Co., Ltd, Resonac Holdings Corporation, and LG Chem, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Advancement in Nanotubes Technologies

- 4.1.2 Growing Adoption of Carbon Nanotubes

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Manufacturing and R&D Cost

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of Substitute Products and Services

- 4.4.4 Threat of New Entrants

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Carbon Nanotubes

- 5.1.2 Silicon Nanotubes

- 5.1.3 Inorganic Nanotubes

- 5.1.4 Other Types (Membrane Nanotubes, Etc.)

- 5.2 Structure Type

- 5.2.1 Non-polymer Organic Nanomaterials

- 5.2.2 Polymeric Nanomaterials

- 5.3 Application

- 5.3.1 Hydrogen Storage Devices

- 5.3.2 Sensors

- 5.3.3 Polymeric Biomaterials

- 5.3.4 Li-ion Batteries

- 5.3.5 Luminescent Display Devices

- 5.3.6 Biosensors

- 5.3.7 Nanoelectrodes

- 5.3.8 Water Purification Filters

- 5.3.9 Semiconductor Devices

- 5.3.10 Conductive Plastics

- 5.4 End-user Industry

- 5.4.1 Healthcare

- 5.4.2 Electronics

- 5.4.3 Energy

- 5.4.4 Automotive

- 5.4.5 Aerospace and Defense

- 5.4.6 Textile

- 5.4.7 Other End-user Industries (Chemical Materials, Etc.)

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Arkema

- 6.4.2 Carbon Solutions Inc.

- 6.4.3 Cheap Tubes

- 6.4.4 Hyperion Catalysis International

- 6.4.5 Jiangsu Cnano Technology Co., Ltd.

- 6.4.6 Nano-C

- 6.4.7 Nanocyl SA (Birla Carbon)

- 6.4.8 NanoIntegris Inc.

- 6.4.9 Nanoshel LLC

- 6.4.10 Resonac Holdings Corporation

- 6.4.11 Thomas Swan & Co. Ltd

- 6.4.12 LG Chem

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Potential Uses in Electronic and Storage Devices

- 7.2 Other Opportunities

石墨烯增强混凝土市场分析与预测(至2035年):类型、产品类型、技术、应用、形式、材料类型、最终用户、功能、安装类型、解决方案

石墨烯增强混凝土市场分析与预测(至2035年):类型、产品类型、技术、应用、形式、材料类型、最终用户、功能、安装类型、解决方案 奈米碳管薄膜市场按类型、终端用途产业、合成技术、材料形态、基板类型和应用划分,全球预测(2026-2032年)石墨化高纯度多壁奈米碳管市场:依应用、形貌、功能化、纯度等级及最终用途划分,全球预测(2026-2032年)

奈米碳管薄膜市场按类型、终端用途产业、合成技术、材料形态、基板类型和应用划分,全球预测(2026-2032年)石墨化高纯度多壁奈米碳管市场:依应用、形貌、功能化、纯度等级及最终用途划分,全球预测(2026-2032年) 全球奈米碳管市场规模、份额、趋势和成长分析报告(2026-2034年)

全球奈米碳管市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球奈米碳管市场报告

2026年全球奈米碳管市场报告 碳奈米材料市场按类型、应用、终端用户产业和地区划分军用碳材料市场:依产品类型、製造流程、材料等级、形态、最终用途和销售管道,全球预测,2026-2032年奈米碳管导电液体市场(按奈米管类型、导电等级、分散介质、应用和最终用途产业划分)-2026年至2032年全球预测奈米碳管水性涂料市场按类型、产品类型、应用和最终用途产业划分-2026年至2032年全球预测锂离子电池用奈米碳管市场:按类型、形貌、纯度、功能化、应用和终端用户行业划分 - 全球预测(2026-2032 年)

碳奈米材料市场按类型、应用、终端用户产业和地区划分军用碳材料市场:依产品类型、製造流程、材料等级、形态、最终用途和销售管道,全球预测,2026-2032年奈米碳管导电液体市场(按奈米管类型、导电等级、分散介质、应用和最终用途产业划分)-2026年至2032年全球预测奈米碳管水性涂料市场按类型、产品类型、应用和最终用途产业划分-2026年至2032年全球预测锂离子电池用奈米碳管市场:按类型、形貌、纯度、功能化、应用和终端用户行业划分 - 全球预测(2026-2032 年)