|

市场调查报告书

商品编码

1628851

亚太地区自动化物料输送和储存系统:市场占有率分析、产业趋势和成长预测(2025-2030)Asia Pacific Automated Material Handling And Storage Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

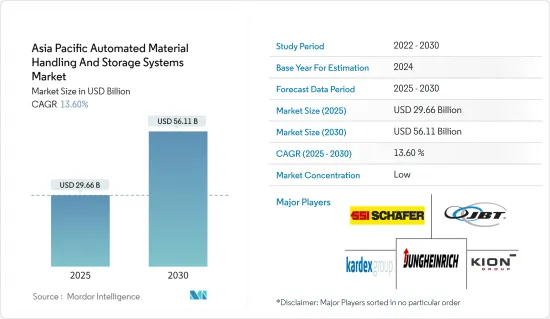

预计2025年亚太地区自动化物料输送与储存系统市场规模为296.6亿美元,2030年达561.1亿美元,预测期间(2025-2030年)复合年增长率为13.6%。

库存单位 (SKU) 的快速成长使得批发商和经销商难以做出明智的业务决策。这种困境凸显了迫切需要更有效地利用劳动力、设备和技术。推动自动化物料输送系统需求的关键因素包括降低成本、提高劳动效率和空间最佳化。

市场格局见证了产品类型的激增以及对更频繁和更小交付的需求。自动化交付操作可以显着提高组织的订单准确性,通常可以提高几个百分点。都市化、电子商务的激增以及技术提供者的出现正在推动亚太市场的成长。这些供应商正在加强研发力度,以提供尖端的解决方案并保持竞争力。

亚太地区正在巩固其作为全球电子商务强国的地位。该地区零售电子商务的扩张,加上中国、印度和印尼等国家中产阶级的快速成长以及对行动装置的偏好,进一步巩固了这一地位。尤其是中国,其零售额占全球零售电子商务销售额的 40%,令人震惊。亚太地区多个国家的仓库可用土地正在减少,促使人们转向多层设施和更高、更窄的通道。这些调整将推动对先进物料输送系统的需求。

过去 70 年来,物料输送发生了重大演变,机器和机器人越来越多地取代个别工人。这种转变不仅重塑了产业,也刺激了企业的成长,特别是汽车产业,规模扩大了10倍。据威斯康辛州经济发展公司称,印度等国家在物料输送设备方面投入了大量资金,MHE市场约占该国施工机械产业的13%。泰国、菲律宾、越南等东南亚国家製造业快速成长,就业扩大,可支配所得增加。收入的成长,加上国际品牌意识的提高,正在推动对当地仓储的需求。

印尼是一个正在迅速拥抱自动化的国家,机器人在工业应用中的使用显着增加。由于日本扮演供应商和消费者的双重角色,印尼可以从贸易活动的活性化中受益,进一步推动该地区的自动化需求。

由于 COVID-19 大流行以及由此导致的停工,全球工业格局面临重大破坏。这些中断包括供应链挑战、原材料短缺、劳动力短缺、价格波动和运输瓶颈,所有这些都增加了生产成本并可能超出预算。

亚太地区自动化物料输送和储存系统市场趋势

组装领域证实了显着的市场成长

- 组装AGV 主要应用于汽车製造、车厢製造、航太和铁路等产业。电动和混合动力汽车产量的增加将在未来几年推动这些 AGV 的需求。这种转变不仅提高了製造商的灵活性,还使他们能够快速回应市场变化,同时确保安全且经济高效的营运。

- 过去十年,随着电动车和混合动力汽车的采用,汽车产业发生了一场革命。这种转变显着增加了汽车生产的复杂性。加上不断发展的安全法规和行业标准,汽车行业对自动化的需求不断增加。关键优先事项包括减少运输过程中人为错误造成的产品损坏、加快工作站之间的底盘搬运速度以及促进与组装工人的互动。有效满足这些要求的组装AGV已成为汽车产业自动化的基石。

- 此外,汽车业依靠自动化组装来製造各种零件,从引擎和变速箱到燃油系统和泵浦。透过利用机器人技术和视觉技术,製造商可以建造符合人体工学的高效产品线,确保快速组装,同时保护员工免受危险情况的影响。因此,安全问题正在推动整个汽车产业的自动化。

- 根据汽车技能发展委员会 (ASDC) 的报告《汽车产业的人力资源和技能要求 (2026)》,预计到 2026 年,印度汽车产业将僱用 4,508 万人。这种劳动力爆炸需要重新评估目前的技能组合,并强调汽车设计、机器人、物联网和人工智慧等领域技能提升的必要性。随着传统角色的发展,工业自动化的推动力不断增强

- 为了满足这种不断增长的需求,许多市场参与企业正在扩大製造能力并引入新的产品线。例如,北美着名自动化工程公司Applied Manufacturing Technologies (AMT)于2024年3月宣布了其最新创新产品ROBiN。 ROBiN,名为机器人引导系统,旨在彻底改变仓库的物料输送,并有望提高效率和吞吐量。 AMT 的 ROBiN 因先进的物料输送和最先进的自主移动机器人 (AMR) 而享有盛誉,有望对该行业产生重大影响。

工业 4.0 投资推动自动化和物料输送的需求

- 世界各地都重视机场投资,因为各国都了解创造舒适的环境让旅客可以花时间和金钱的价值。从办理登机手续到登机,输送机和分类系统在各种规模的机场中都很常见,可有效简化流程并改善整体客户体验。许多机场现在正在与供应商合作部署自主机器人,此举不仅提高了行李运输效率,还降低了营运成本。例如,物流自动化专家 Vanderlande Dutch 最近与香港机场合作,开始测试自动行李车。

- 在国内航空连结性增加和人均 GDP 上升的推动下,印度和中国成为支线航空格局的关键参与企业。国际民航组织指出,光是亚太地区就占国内航线的70%。

- 预测预计未来几年中国航空市场将呈现强劲成长轨迹。特别是,中国三大航空公司——国航、南航和东航——为提升全球排名而製定了雄心勃勃的机队扩张目标。此外,上海和北京的主要机场正积极推行重大扩建计画。

- 根据中国旅游出境研究院预测,到2030年,中国出境旅游人数将达到约4亿人次,占全球出境旅游人数的四分之一。为了应对这一激增,机场将必须实施先进的系统,这项倡议预计将在整个预测期内推动市场的积极成长。

- 相反,疫情促使许多机场部署机器人进行乘客筛检和病毒遏制。例如,韩国仁川机场的智慧机场团队正在利用机器人技术和自动驾驶车辆来改善行动不便乘客 (PRM) 的体验。

亚太地区自动化物料输送与储存系统产业概况

亚太地区自动化物料输送和储存系统市场竞争激烈,主要是由于大量参与企业进入该领域。形成这种竞争的关键因素包括高进入障碍、企业集中度的提高以及市场渗透率的提高。市场上的一些主要参与企业包括卡迪斯集团、凯傲集团、JBT Corporation、Jungheinrich AG、Daifuku、BEUMER Group GmbH &Co.KG。

- 2024 年 2 月,全球着名鞋类和服装品牌 Skechers USA 与主要企业的自动化仓储和搜寻系统 (ASRS) 公司 Hi-Robotics 合作,在港区开设了一个最先进的物流中心,东京我们已经开业了。透过利用 Hy Robotics 的尖端自动化仓库技术,Skechers 正在增强其仓库业务、加快履约并确保准确的订单处理。

- 2024 年 1 月,富士通有限公司和 YE DIGITAL CORPORATION 宣布开展合作,旨在解决日本物流业的劳动力短缺问题并加强永续供应链。此次伙伴关係将重点利用以简化物流中心而闻名的富士通 WMS 服务,以及旨在实现仓库业务自动化的 YE DIGITAL 的 WES MMLogiStation。除了提供WMS服务外,富士通还为新物流中心的建设和现有物流中心的业务改革提供规划支持,并推动自动化设备的引进。透过简化设施管理,我们的目标是促进营运自动化并提高整个物流中心的绩效。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 竞争公司之间的敌对关係

- 替代品的威胁

- COVID-19 对工业生态系的影响

- 市场驱动因素

- 技术进步不断推动市场成长

- 工业 4.0 投资推动自动化和物料输送的需求

- 电子商务快速成长

- 市场限制因素

- 初始成本高

- 缺乏技术纯熟劳工

第五章市场区隔

- 产品类型

- 硬体

- 软体

- 服务

- 设备类型

- 移动机器人

- 自动导引运输车(AGV)

- 自动堆高机

- 自动拖车/拖拉机/标籤

- 单元货载

- 组装

- 特殊用途

- 自主移动机器人(AMR)

- 自动储存和搜寻系统(ASRS)

- 固定通道

- 旋转木马

- 垂直升降模组

- 自动输送机

- 腰带

- 滚筒

- 调色盘

- 开卖

- 堆垛机

- 传统的

- 机器人

- 分类系统

- 移动机器人

- 最终用户产业

- 飞机场

- 车

- 饮食

- 零售/仓库/配送中心/物流中心

- 一般製造业

- 药品

- 小包裹

- 电子/半导体製造

- 其他的

- 国家名称

- 中国

- 日本

- 印尼

- 印度

- 澳洲

- 泰国

- 韩国

- 新加坡

- 马来西亚

- 台湾

- 其他亚太地区

第六章 竞争状况

- 公司简介

- Daifuku Co. Ltd

- Kardex Group

- KION Group

- JBT Corporation

- Jungheinrich AG

- SSI Schaefer AG

- VisionNav Robotics

- System Logistics

- BEUMER Group GmbH & Co. KG

- Interroll Group

- Witron Logistik

- Kuka AG

- Honeywell Intelligrated Inc.

- Murata Machinery Ltd

- Toyota Industries Corporation

第七章 投资分析

第八章 市场机会及未来趋势

The Asia Pacific Automated Material Handling And Storage Systems Market size is estimated at USD 29.66 billion in 2025, and is expected to reach USD 56.11 billion by 2030, at a CAGR of 13.6% during the forecast period (2025-2030).

With the rapid growth in stock-keeping units (SKUs), wholesalers and distributors are finding it difficult to make informed decisions about operations. This dilemma underscores the pressing need for more efficient labor, equipment, and technology utilization. Key factors driving the need for automated material-handling systems include cost savings, enhanced labor efficiency, and space optimization.

The market landscape is witnessing a surge in product variety and a demand for more frequent, smaller deliveries. Automated distribution operations can significantly boost an organization's order accuracy, often by several percentage points. The Asia-Pacific market's growth is propelled by urbanization, surging e-commerce sales, and a robust technology provider presence. These providers are intensifying their R&D efforts to offer cutting-edge solutions and maintain a competitive edge.

Asia-Pacific has cemented its position as a global e-commerce powerhouse. This status has been bolstered by the region's expanding retail e-commerce, driven by a burgeoning middle-income group in countries like China, India, and Indonesia, coupled with a fondness for mobile devices. Notably, China commands a staggering 40% share of global retail e-commerce sales. In several Asia-Pacific nations, the availability of warehouse land is dwindling, prompting a shift toward multi-story facilities and taller, narrower aisles. These adaptations are poised to fuel the demand for advanced material handling systems.

Material handling has witnessed a profound evolution over the past seven decades, with machines and robots increasingly replacing individual workers. This transformation has not only reshaped the industry but also fueled the growth of enterprises, notably in the automotive industry, which has seen a tenfold expansion. Countries like India are significantly investing in material handling equipment, with the MHE market, as per the Wisconsin Economic Development Corporation, capturing around 13% of the country's construction equipment industry. Southeast Asian nations, including Thailand, the Philippines, and Vietnam, are witnessing a surge in manufacturing establishments, bolstering employment and, subsequently, disposable incomes. This rise in income, coupled with a growing awareness of international brands, is spurring demand for local warehouses.

Indonesia stands out as a nation swiftly embracing automation, with a notable uptick in robotic usage for industrial applications. Given Japan's dual role as both a supplier and a consumer, Indonesia stands to benefit from heightened trade activities, further propelling the region's automation demand.

The global industrial landscape faced significant disruptions due to the COVID-19 pandemic and ensuing lockdowns. These disruptions spanned supply chain challenges, raw material shortages, labor scarcities, fluctuating prices, and shipping bottlenecks, all of which threatened to inflate production costs and exceed budgets.

APAC Automated Material Handling & Storage Systems Market Trends

Assembly Line Segment to Witness Significant Growth in the Market

- Assembly-line AGVs find their primary application in industries like automobile manufacturing, coach-building, aerospace, and railways. The rising production of electric and hybrid vehicles is set to drive the demand for these AGVs in the coming years. This shift not only enhances manufacturers' flexibility but also enables them to swiftly adapt to market changes, all while ensuring safe and cost-effective operations.

- The automotive industry witnessed a revolution in the past decade with the introduction of electric and hybrid vehicles. This transformation has significantly increased the complexity of automobile production. Coupled with evolving safety regulations and industry standards, there is a growing need for automation in the automotive industry. Key priorities include reducing product damage, often caused by human error during transit, improving the speed of chassis handling between workstations, and facilitating interaction with assembly-line workers. Assembly line AGVs, meeting these requirements effectively, have become the cornerstone of automation in the automotive industry.

- Furthermore, in the automotive industry, automated assembly lines are utilized to craft various parts, ranging from engines and gearboxes to fuel systems and pumps. Leveraging robotics and vision technology, manufacturers can create ergonomic and efficient product lines, safeguarding their workforce from hazardous conditions while ensuring swift assembly. Consequently, safety concerns are propelling automation across the automotive landscape.

- According to a report by the Automotive Skill Development Council (ASDC), titled 'Human Resource and Skills Requirements in the Automotive Sector (2026),' India is projected to employ 45.08 million individuals in the automobile industry by 2026. This surge in the workforce demands a reevaluation of the current skill set, emphasizing the need for upskilling in areas like automotive design, robotics, IoT, and AI. As traditional roles evolve, the industry is witnessing a heightened push toward automation.

- To cater to this escalating demand, numerous market players are not only expanding their manufacturing capacities but also introducing new product lines. For instance, in March 2024, Applied Manufacturing Technologies (AMT), a prominent name in North America's automation engineering, unveiled its latest innovation, ROBiN. Termed the Robotic Induction System, ROBiN aims to revolutionize material handling in warehousing, promising heightened efficiency and throughput. With a strong reputation in advanced material handling and cutting-edge autonomous mobile robots (AMRs), AMT's ROBiN is poised to make a significant impact in the industry.

Industry 4.0 Investments Driving Demand for Automation and Material Handling

- Airport investments are gaining global recognition as nations understand the value of creating welcoming environments that encourage travelers to spend both time and money. From check-in to boarding, conveyors and sortation systems, prevalent in airports of all sizes, effectively streamline the process, enhancing the overall customer experience. Many airports are now collaborating with vendors to introduce autonomous robots, a move that not only boosts luggage transfer efficiency but also trims operational costs. For example, Vanderlande Dutch, a logistics automation specialist, recently partnered with Hong Kong Airport to trial autonomous baggage handling vehicles.

- India and China, driven by increasing domestic air connectivity and rising per capita GDP, stand out as pivotal players in the regional aviation landscape. Highlighting this, the ICAO notes that the Asia-Pacific region alone accounted for 70% of domestic air travel.

- Projections indicate a robust growth trajectory for the Chinese aviation market in the coming years. Notably, China's top three airlines-Air China, China Southern, and China Eastern-have set ambitious fleet expansion goals, aiming to elevate their global rankings. Furthermore, major airports in Shanghai and Beijing are actively pursuing extensive expansion initiatives.

- According to the Chinese Tourism Outbound Research Institute, Chinese outbound visits are set to reach around 400 million by 2030, potentially constituting a quarter of all global outbound travelers. To accommodate this surge, airports must deploy advanced systems, a move that is expected to drive market growth positively throughout the forecast period.

- Conversely, the pandemic prompted many airports to deploy robots for passenger screening and virus containment. For instance, South Korea's Incheon Airport's Smart Airport team has been leveraging robotics and automated vehicles to enhance the experience for passengers with reduced mobility (PRMs).

APAC Automated Material Handling & Storage Systems Industry Overview

The Asia-Pacific market for automated material handling and storage systems is fiercely competitive, primarily due to the significant number of players in the arena. Key factors shaping this competition include high exit barriers, increasing firm concentration, and rising market penetration rates. Some of the key players operating in the market are Kardex Group, KION Group, JBT Corporation, Jungheinrich AG, Daifuku Co. Ltd, and BEUMER Group GmbH & Co. KG.

- In February 2024, Skechers USA, a prominent global footwear and apparel brand, partnered with Hai Robotics, a top player in automated storage and retrieval systems (ASRS), to inaugurate its latest distribution hub in Minato City, Tokyo, Japan. By leveraging Hai's cutting-edge automated goods-to-person technology, Skechers is enhancing its warehouse operations, accelerating fulfillment, and ensuring precise order processing.

- In January 2024, Fujitsu Limited and YE DIGITAL CORPORATION announced a collaboration aimed at tackling labor shortages and bolstering sustainable supply chains in Japan's logistics industry. The partnership focuses on leveraging Fujitsu's WMS services, known for enhancing distribution center efficiency, alongside YE DIGITAL's WES MMLogiStation, which is designed to automate warehouse operations. Fujitsu will not only provide its WMS services but also offer planning support for constructing new distribution centers and transforming operations at existing ones, aiming to ease the adoption of automated facilities. By streamlining facility management, the companies aim to drive operational automation and enhance overall distribution center performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of COVID-19 on the Industry Ecosystem

- 4.5 Market Drivers

- 4.5.1 Increasing Technological Advancements Aiding Market Growth

- 4.5.2 Industry 4.0 Investments Driving Demand for Automation and Material Handling

- 4.5.3 Rapid Growth of E-commerce

- 4.6 Market Restraints

- 4.6.1 High Initial Costs

- 4.6.2 Unavailability of Skilled Workforce

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 Equipment Type

- 5.2.1 Mobile Robots

- 5.2.1.1 Automated Guided Vehicle (AGV)

- 5.2.1.1.1 Automated Forklift

- 5.2.1.1.2 Automated Tow/Tractor/Tug

- 5.2.1.1.3 Unit Load

- 5.2.1.1.4 Assembly Line

- 5.2.1.1.5 Special Purpose

- 5.2.1.2 Autonomous Mobile Robots (AMR)

- 5.2.2 Automated Storage and Retrieval System (ASRS)

- 5.2.2.1 Fixed Aisle

- 5.2.2.2 Carousel

- 5.2.2.3 Vertical Lift Module

- 5.2.3 Automated Conveyor

- 5.2.3.1 Belt

- 5.2.3.2 Roller

- 5.2.3.3 Pallet

- 5.2.3.4 Overhead

- 5.2.4 Palletizer

- 5.2.4.1 Conventional

- 5.2.4.2 Robotic

- 5.2.5 Sortation System

- 5.2.1 Mobile Robots

- 5.3 End-user Industry

- 5.3.1 Airport

- 5.3.2 Automotive

- 5.3.3 Food and Beverage

- 5.3.4 Retail/Warehousing/Distribution Centers/Logistic Centers

- 5.3.5 General Manufacturing

- 5.3.6 Pharmaceuticals

- 5.3.7 Post and Parcel

- 5.3.8 Electronics and Semiconductor Manufacturing

- 5.3.9 Other End-user Industries

- 5.4 Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 Indonesia

- 5.4.4 India

- 5.4.5 Australia

- 5.4.6 Thailand

- 5.4.7 South Korea

- 5.4.8 Singapore

- 5.4.9 Malaysia

- 5.4.10 Taiwan

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Daifuku Co. Ltd

- 6.1.2 Kardex Group

- 6.1.3 KION Group

- 6.1.4 JBT Corporation

- 6.1.5 Jungheinrich AG

- 6.1.6 SSI Schaefer AG

- 6.1.7 VisionNav Robotics

- 6.1.8 System Logistics

- 6.1.9 BEUMER Group GmbH & Co. KG

- 6.1.10 Interroll Group

- 6.1.11 Witron Logistik

- 6.1.12 Kuka AG

- 6.1.13 Honeywell Intelligrated Inc.

- 6.1.14 Murata Machinery Ltd

- 6.1.15 Toyota Industries Corporation

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

对自动化物料输送设备市场进行分析和预测,直至 2035 年:按类型、产品、服务、技术、组件、应用、最终用户、功能、安装配置和解决方案进行分析和预测。

对自动化物料输送设备市场进行分析和预测,直至 2035 年:按类型、产品、服务、技术、组件、应用、最终用户、功能、安装配置和解决方案进行分析和预测。 包装物料收集台市场:材料类型、产品类型、应用和分销管道划分,全球预测,2026-2032年在线连续雷射拼板机市场:按雷射类型、功率范围、自动化程度、分销管道、应用和最终用户行业划分,全球预测,2026-2032年移动式卡车清洗系统市场:按服务类型、卡车类型、清洗技术、最终用户和应用划分,全球预测,2026-2032年自动装袋机市场:依机器类型、包装材料、袋型、自动化程度、技术、封口类型、速度、产能、最终用途和销售管道,全球预测,2026-2032年邮件包装机市场:按机器类型、技术、分销管道、应用和最终用户划分,全球预测,2026-2032年人工智慧驱动的回收机器人市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署模式、最终用户和功能划分电动标籤列车市场:按动力源配置、运行模式、电池类型、牵引能力和最终用户划分-全球预测,2026-2032年葡萄籽收穫机市场:按类型、技术、应用、最终用户和分销管道划分,全球预测,2026-2032年餐厅传菜梯市场按类型、安装类型、载重能力、速度和应用划分,全球预测(2026-2032)

包装物料收集台市场:材料类型、产品类型、应用和分销管道划分,全球预测,2026-2032年在线连续雷射拼板机市场:按雷射类型、功率范围、自动化程度、分销管道、应用和最终用户行业划分,全球预测,2026-2032年移动式卡车清洗系统市场:按服务类型、卡车类型、清洗技术、最终用户和应用划分,全球预测,2026-2032年自动装袋机市场:依机器类型、包装材料、袋型、自动化程度、技术、封口类型、速度、产能、最终用途和销售管道,全球预测,2026-2032年邮件包装机市场:按机器类型、技术、分销管道、应用和最终用户划分,全球预测,2026-2032年人工智慧驱动的回收机器人市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、流程、部署模式、最终用户和功能划分电动标籤列车市场:按动力源配置、运行模式、电池类型、牵引能力和最终用户划分-全球预测,2026-2032年葡萄籽收穫机市场:按类型、技术、应用、最终用户和分销管道划分,全球预测,2026-2032年餐厅传菜梯市场按类型、安装类型、载重能力、速度和应用划分,全球预测(2026-2032)