|

市场调查报告书

商品编码

1630228

企业人工智慧 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)Enterprise AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

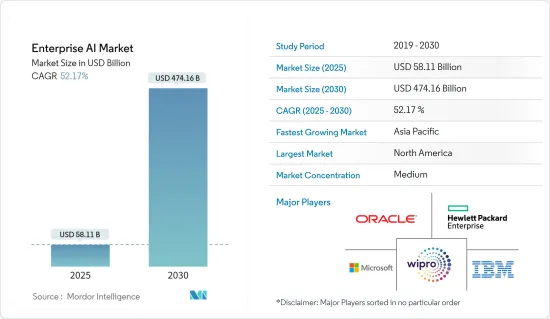

企业人工智慧市场规模预计到2025年为581.1亿美元,预计2030年将达到4,741.6亿美元,预测期内(2025-2030年)复合年增长率为52.17%。

公司正在认识到将人工智慧融入其业务流程、透过流程自动化提高效率并降低成本的价值。最重要的是,它可以帮助公司预测业务成果并提高盈利。

主要亮点

- 企业数位化是市场最主要的趋势。第四次工业革命(工业4.0)以实体和先进数位技术为特征,如物联网、人工智慧、智慧机器人、无所不在的行动超级运算、资讯管理和分析,并对各行业产生重大影响。影响。

- 与工业 4.0 的传播相关的工业自动化热潮正在推动机器人和自动化技术的引入,以提高製造流程的效率。例如,根据美国银行的数据,到 2025 年,机器人和人工智慧工业机器人领域的价值预计将达到约 240 亿美元。这一趋势正在加强企业中人工智慧的一个重要方面,即机器人流程自动化(RPA)。

- 此外,2022 年 6 月,该公司宣布选择专注于工业 4.0 的製造执行系统 (MES) 供应商凯睿德 (Critical Manufacturing) 来优化 SwissSEM 的生产流程。做出这项决定是为了最大限度地降低营运成本并提高公司高度复杂的生产线的营运效率,迈向更高的数位自动化。凯睿德製造的全新製造执行系统 (MES) 可提供有关生产流程的准确、实时信息,为持续流程改进、品质改进和降低成本奠定基础。

- 边缘运算、扩增实境、虚拟实境、工业机器人、自动驾驶汽车、数位製造、工业物联网、数位製造等新技术正在推动各製造业取得显着进步。这些解决方案有潜力提高生产流程的个人化、适应性和敏捷性,进一步推动市场成长。

- 2022 年 2 月,美国钢铁公司与机器人和人工智慧工作室 Carnegie Foundry 宣布建立战略投资和合作关係。这两家总部位于匹兹堡的新兴企业将共同努力,利用尖端的机器人技术和人工智慧来加速和扩大工业自动化。透过这笔资金筹措,Carnegie Foundry 将在先进製造、工业机器人、整合系统、自主移动和语音分析等领域行销和扩展其机器人和人工智慧技术的工业自动化产品组合。

- 据美国钢铁公司称,此次合作将使该公司处于工业机器人和独立解决方案创新的前沿。钢铁製造商表示,需要先进的技术来满足客户对强大且有弹性的供应链的期望。

- 此外,企业人工智慧是数位转型的关键推动者。未来几年内,几乎所有企业软体应用程式都将支援人工智慧。因此,开发大规模建置、部署和营运企业人工智慧应用程式的能力对于企业生存至关重要。

- 根据O'Reilly 的2022 年企业人工智慧采用报告(基于时事通讯收件人对企业人工智慧采用调查的回应),31% 的公司表示他们没有使用人工智慧(高于最近的13%),43%目前正在评估实施情况, 26%的人已经实施了人工智慧应用。在大洋洲,采用人工智慧的製造业受访者数量从 18% 跃升至 31%。大量组织缺乏人工智慧管治。在生产人工智慧产品的 26% 受访者中,只有 49% 制定了监督计划创建、衡量和观察方式的管治计画(51% 的受访者表示没有)。

- 近年来,专注于工业4.0相关解决方案的各种伙伴关係关係进一步加速了研究市场的成长。例如,2022年1月,西班牙电信旗下数位服务部门Telefonica Tech与西班牙工程服务公司Grupo Alava签署协议,为西班牙通讯业者提供私有5G、巨量资料「AI」分析和云端服务。预测分析解决方案,该解决方案也利用了边缘运算。

企业人工智慧软体市场趋势

云端的引入预计将显着成长市场

- 人工智慧云端以前只是一个概念,现在开始被企业采用,将人工智慧与云端运算结合。为云端运算带来新价值的人工智慧工具和软体是一个主要驱动因素。云端是一种经济的资料储存和运算选项,有助于人工智慧的采用。

- Flexera Software 表示,75% 的企业受访者表示,他们将在 2023 年采用 Microsoft Azure 进行公共云端使用。 AWS、Microsoft Azure、Google Cloud 或 Hyperscalar 是世界上最高的云端运算平台供应商之一。

- 人工智慧云端主要由人工智慧使用案例的共用基础设施组成,在任何给定时间在云端基础设施上同时支援多个计划和人工智慧工作负载。 AI Cloud 为组织提供了存取 AI 的机会,并透过结合 AI 硬体和软体并在混合云基础设施上提供 AI 软体即服务,使他们能够更好地利用其 AI 功能。

- 云端中人工智慧最吸引人的好处之一是它能够解决的挑战。它将极大地使人工智慧民主化并使其更容易使用。人工智慧驱动的企业转型是透过降低实施成本和促进共同创造和创新来驱动的。

- 世界各地的组织越来越多地采用云端解决方案。例如,2022 年 7 月,B2B虚拟网路营运商 (VNO) Cloud Connect Communications 获得了电讯部 (DoT) 颁发的在孟买和艾哈默德巴德营运的许可证。 Cloud Connect 描述了一种云端基础的统一通讯解决方案,这是一种透过可程式 API 与 CRM(客户关係管理)和语音通信整合的企业呼叫管理系统,可对国内和国际市场的论坛进行呼叫和管理访问。

- 此外,2022 年 1 月,Oracle 宣布推出适用于电信公司的 Oracle Cloud。 Oracle Cloud for Telcos 是基于 Oracle 云端基础架构建构的一整套云端解决方案。 OCI是一个采用分散式云端架构的云端平台,在全球拥有36个公有云区域。此外,OCI 平台拥有超过 60 个工业应用程式套件,支援第三方、自订和 Oracle Fusion Cloud 应用程式套件工作负载。

欧洲正在经历显着的市场成长

- 在欧洲,由于工业革命和自动化等主流趋势,需求不断增加。该地区的公司正在投资各种自动化技术,包括机器人和人工智慧以及机器学习的发展。

- 大量政府资金也支持该地区製造业采用最新技术。例如,2022 年 10 月,英国研究与发展局 (UKRI) 向 12 个智慧工厂计划提供了 1,370 万英镑的资金,以开发提高能源效率、生产力和製造业成长的技术。资助公司包括使用人工智慧来发现钢铁生产效率低下的公司以及在 3D 列印中使用回收材料的公司。这是政府更广泛的 1.47 亿英镑「变得更聪明的创新挑战」的一部分,该挑战旨在增加英国製造业的技术使用。

- 此外,该地区的主要企业正在投资企业人工智慧市场并扩大其能力。例如,2022年9月,Oracle宣布创建西班牙首个Oracle云端基础设施(OCI)区域,以满足西班牙快速成长的企业云端服务需求。随着马德里新区域的开放, Oracle在西班牙的公共和私营部门客户及合作伙伴现在可以更新应用程式、试验资料和分析,并将关键任务工作负载从其资料中心迁移到 OCI。服务。

- 例如,惠普企业于 2022 年 5 月宣布将在捷克共和国开设新地点,以加强其欧洲超级电脑供应链。新工厂将生产公司自订设计的解决方案,以推进科学研究、成熟 AL/ML 计划并加速创新。

- 此外,2022年5月,欧洲三大壁炉供应商之一的Jotul与商业云端供应商Infor建立了合作关係。 Jotul 透过业内最大的销售组织之一和全球经销商网路行销其产品。 Jotul 将从目前的 ERP 解决方案升级到 Infor M3 CloudSuite 和标准化工业製造解决方案 Infor Consulting Services。

- 认知运算的兴起预计将使在区域企业中复製人类的感官知觉、推理、思考、学习和决策能力成为可能。凭藉着利用巨大运算能力的能力,这种范式在速度和识别模式的能力上都超越了人类复製,并提供了个人可能无法感知的解决方案,有望扩大其对人工智慧解决方案的使用。

- 此外,自动化在製造业中的日益普及、降低製造成本的需求不断增长以及机器对机器(M2M)技术的渗透正在推动该地区自动化的采用,从而导致工业控制的采用增加预计将推动需求。此外,德国是世界第五大数位经济体,已广泛实施工业4.0以实现工业生产数位化(根据GTAI)。此外,根据 Bitkom 数位协会的一项研究,62% 的德国公司正在使用工业 4.0 相关技术和解决方案(软体、IT 服务、硬体)。

企业人工智慧软体产业概况

由于有许多重要的参与企业,企业人工智慧市场上竞争公司之间的竞争非常激烈。 IBM、SAP SE、惠普企业、谷歌公司、微软公司、甲骨文公司等许多公司都试图透过为其用户设计新的创新产品来占领最大的市场占有率。我们透过在研发、併购、策略扩张、资金筹措和策略伙伴关係方面的大量投资获得了竞争优势。

2024 年 8 月 去年刚成立的班加罗尔新兴企业Sarvam AI 推出了一系列由生成式 AI 车型驱动的 B2B 产品。 Sarvam 週二宣布了多元化的产品阵容,瞄准金融服务、法律服务、消费品、科技、媒体和通讯等领域。该系列包括 Sarvam Agents、Sarvam 2B、Shuka 1.0、A1 以及针对各种语言量身定制的多个 Sarvam 模型。

2024年7月,富士通与专门从事安全和资料隐私的企业人工智慧公司Cohere Inc.建立了战略伙伴关係关係。此次伙伴关係旨在透过开发和提供大规模语言模型 (LLM) 来为企业提供先进的日语能力,从而改善客户和员工的体验。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 利用市场促进和市场约束因素

- 市场驱动因素

- 对自动化和基于人工智慧的解决方案的需求不断增长

- 分析指数增长的资料的需求日益增加

- 市场限制因素

- 招聘率低

- 产业吸引力-波特五力分析

- 买方议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 技术简介

- 主要成分分析

- 人工智慧对半导体的影响

- COVID-19 市场影响评估

第五章市场区隔

- 按类型

- 解决方案

- 按服务

- 按发展

- 本地

- 云

- 按最终用户产业

- 製造业

- 车

- BFSI

- 资讯科技/通讯

- 媒体/广告

- 其他的

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第六章 竞争状况

- 公司简介

- IBM Corporation

- Oracle Corporation

- Wipro Limited

- Hewlett Packard Enterprise

- Microsoft Corporation

- Amazon Web Services

- Google Inc.

- Intel Corporation

- SAP SE

- Sentient Technologies

- AiCure LLC

- NEC Corporation

- NVIDIA Corporation

第七章 投资分析

第八章市场的未来

The Enterprise AI Market size is estimated at USD 58.11 billion in 2025, and is expected to reach USD 474.16 billion by 2030, at a CAGR of 52.17% during the forecast period (2025-2030).

Enterprises recognize the value of incorporating artificial intelligence into their business processes, improving efficiency and reducing costs by automating process flows. Most importantly, it has helped enterprises predict business outcomes, driving profitability.

Key Highlights

- The digitalization of enterprises is the most dominant trend in the market. The fourth industrial revolution (Industry 4.0) is characterized by physical and advanced digital technologies, such as the Internet of Things, artificial intelligence, intelligent robots, ubiquitous mobile supercomputing, information management, and analytics, which significantly impact various industries.

- The boom of industrial automation, with the widespread adoption of Industry 4.0, is driving the adoption of robots and automated technologies to enhance the efficiency of manufacturing processes. For instance, according to Bank of America, the industrial robot segment of robotics and AI is expected to be valued at about USD 24 billion by 2025. This trend has augmented robotic process automation (RPA) among enterprises, a significant aspect of AI.

- Additionally, in June 2022, Critical Manufacturing, a provider of an Industry 4.0-focused Manufacturing Execution System (MES), announced that it was selected by SwissSEM to optimize its production processes. This decision is made to move towards greater digital automation based on minimizing operating costs and enhancing operating efficiency for its highly complex production line. The new Manufacturing Execution System (MES) from Critical Manufacturing will facilitate accurate, real-time information about production processes, establishing a basis for continuous process improvement, enhanced quality, and reduced costs.

- Various manufacturing industries have experienced tremendous development due to new technologies, including edge computing, augmented and virtual reality, industrial robots, self-driving cars, digital manufacturing, IIOT, and digital manufacturing. These solutions enhance production processes' personalization, adaptability, and agility, which may further drive market growth.

- In February 2022, United States Steel and Carnegie Foundry, a robotics and AI studio, announced a strategic investment and relationship. The two Pittsburgh-based startups will work together to accelerate and expand industrial automation using cutting-edge robotics and artificial intelligence. Carnegie Foundry will use this funding to market and scale its industrial automation portfolio of robotics and AI technologies in advanced manufacturing, industrial robots, integrated systems, autonomous mobility, speech analytics, and other areas.

- According to US Steel, the collaboration keeps the company at the forefront of growing innovation in robotics and independent solutions for the industry. According to the steelmaker, highly advanced technology will be required to meet its client's expectations for a robust and resilient supply chain.

- Furthermore, Enterprise AI is a significant enabler of digital transformation. Nearly every enterprise software application will be AI-enabled in the years to come. Developing competencies in the capability to build, deploy, and operate enterprise AI applications at scale, therefore, is becoming imperative for business survival.

- According to O'Reilly's 2022 report on enterprise AI adoption (based on the answers given by recipients of its newsletters to a questionnaire on enterprise AI adoption), 31% of companies report not using AI (up from 13% recently), 43% are evaluating adoption, and 26% have implemented AI applications. The immediate increase, from 18% to 31%, in manufacturing respondents with AI was in Oceania. A considerable number of organizations lack AI governance. Of the 26% of respondents with AI products in production, only 49% have a governance plan to oversee how projects are created, measured, and observed (versus 51% for those without).

- In recent years, various partnerships focused on solutions related to Industry 4.0 have further accelerated the studied market's growth. For instance, in January 2022, Telefonica Tech, the digital services arm of Telefonica, signed a deal with Spanish engineering services company Grupo Alava to introduce a predictive analytics solution for the Industry 4.0 market that also leverages private 5G, big-data 'AI' analytics, and cloud and edge computing from the Spanish operator.

Enterprise AI Software Market Trends

Cloud Deployment is Expected to Experience a Significant Market Growth

- The AI cloud, which was previously a concept, has now started to be implemented by enterprises, combining AI with cloud computing. Some significant factors driving it include AI tools and software that deliver new, increased value to cloud computing. It is an economical data storage and computation option and plays a role in AI adoption.

- According to Flexera Software, 75% of enterprise respondents indicated adopting Microsoft Azure for public cloud usage in 2023. AWS, Microsoft Azure, and Google Cloud, or hyper scalers, are among the highest cloud computing platform providers worldwide.

- An AI cloud primarily consists of a shared infrastructure for AI use cases, supporting multiple projects and AI workloads simultaneously on cloud infrastructure at any given time. The AI cloud combines AI hardware and software to deliver AI software-as-a-service on hybrid cloud infrastructure, providing organizations with access to AI and enabling them to harness AI capabilities more.

- One of the most compelling advantages of AI in the cloud is the challenges it addresses. It significantly democratizes AI, making it more accessible. Lowering the adoption costs and facilitating co-creation and innovation drive AI-powered transformation for enterprises.

- Organizations across the world are increasingly adopting cloud solutions. For instance, in July 2022, Cloud Connect Communications, a B2B virtual network operator (VNO), was licensed by the Department of Telecommunications (DoT) to operate in Mumbai and Ahmedabad. CloudConnect would deliver corporate call management systems with Integrated Cloud-based Communication Solutions, CRM (customer relationship management) Integration with telephony through programmable APIs, and calls and administrative access to the forum in local and foreign markets.

- Further, in January 2022, Oracle introduced Oracle Cloud for Telcos. Oracle Cloud for Telcos is a complete suite of cloud solutions built on Oracle Cloud Infrastructure. OCI is a cloud platform that can be utilized in dispersed cloud architecture and has 36 public cloud regions globally. Moreover, with over 60 industry application suites, the OCI platform enables third-party, custom, and Oracle Fusion Cloud Applications Suite workloads.

Europe to Experience Significant Market Growth

- The European region is witnessing increased demand due to mainstream trends, such as the industrial revolution and automation. The regional firms have been identified to invest in various automation technologies, such as robotics, artificial intelligence, etc., with developments in machine learning.

- Many government fundings also aid the adoption of the latest technologies in the manufacturing industry in the region. For Instance, in October 2022, UK Research and Innovation (UKRI) awarded 12 smart factory projects a share of GBP 13.7 million in funding to develop technologies that improve energy efficiency, productivity, and growth in manufacturing. The budget recipients include companies using AI to spot inefficiencies in steel production and using recycled materials in 3D printing. It is a part of the government's broader GBP 147 million Made Smarter Innovation Challenge that seeks to increase the use of technology within UK manufacturing.

- Moreover, major regional players are investing and expanding their capabilities in the Enterprise AI market. For Instance, in September 2022, to address the country's quickly growing demand for enterprise cloud services, Oracle announced the creation of the first Oracle Cloud Infrastructure (OCI) region in Spain. With the opening of the new territory in Madrid, Oracle's public and private sector clients and partners in Spain will have access to various cloud services that will help them update their applications, experiment with data and analytics, and move mission-critical workloads from their data centers to OCI.

- For Instance, in May 2022, Hewlett Packard Enterprise announced the launch of its new site in the Czech Republic to strengthen Europe's Supercomputer Supply Chain. The new factory will likely manufacture the company's custom-designed solutions to advance scientific research, mature AL/ML initiatives, and accelerate innovation.

- Moreover, in May 2022, one of the top three suppliers of fireplaces in Europe, Jotul, and Infor, the business cloud provider, established a partnership. Jotul supplies the markets through one of the largest industry-wide global networks of its sales organizations and distributors. Jotul will upgrade to Infor M3 CloudSuite, a standardized industrial manufacturing solution, and Infor Consulting Services from its present ERP solution.

- This rise in cognitive computing is expected to enable the replication of human sensory perception, deduction, thinking, learning, and decision-making capabilities across regional enterprises. The ability to harness considerable amounts of computing power is poised to take this paradigm beyond human replication, both in terms of speed and capacity, to distinguish patterns and provide potential solutions that individuals may not be equipped to perceive, thus augmenting the use of AI solutions.

- Furthermore, a rise in the penetration of automation in the manufacturing sector, the rising need to mitigate manufacturing costs, and the penetration of machine-to-machine (M2M) technologies are encouraging the adoption of automation in the region, which is anticipated to propel the demand for industrial control systems. In addition, Germany is the fifth largest digital economy in the world, and Industry 4.0 for the digitalization of industrial production is being widely implemented in the country (as per GTAI). Also, 62% of companies utilize Industrie 4.0-related technologies and solutions (software, IT services, and hardware) in Germany, according to a Bitkom digital association study.

Enterprise AI Software Industry Overview

The competitive rivalry in the Enterprise AI Market is high due to many significant players. Players like IBM, SAP SE, Hewlett Packard Enterprise, Google Inc., Microsoft Corporation, Oracle Corporation, and many more are trying to achieve maximum market share by designing new and innovative products for users. Their significant investments in research and Development, mergers & acquisitions, strategic expansion, funding, strategic partnership, etc., have allowed them to gain a competitive advantage.

August 2024: Sarvam AI, a startup based in Bengaluru and established just last year, unveiled a range of B2B products powered by its generative AI models. Targeting sectors such as financial services, legal services, consumer goods, technology, media, and telecom, Sarvam introduced a diverse product lineup on Tuesday. This lineup features Sarvam Agents, Sarvam 2B, Shuka 1.0, A1, and multiple Sarvam models tailored for various Indic languages.

In July 2024, Fujitsu entered into a strategic partnership with Cohere Inc., an enterprise AI company specializing in security and data privacy, with offices in Toronto and San Francisco. This partnership aims to develop and provide a large language model (LLM) that equips enterprises with advanced Japanese language capabilities, thereby enhancing customer and employee experiences.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increasing Demand for Automation and AI-based Solutions

- 4.3.2 Increasing Need to Analyze Exponentially Growing Data Sets

- 4.4 Market Restraints

- 4.4.1 Sluggish Adoption Rates

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technology Snapshot

- 4.6.1 Major Component Analysis

- 4.6.2 Impact of AI on the Semicondu

- 4.7 Assessment of the impact of COVID-19 on the market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Solution

- 5.1.2 Service

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By End-user Industry

- 5.3.1 Manufacturing

- 5.3.2 Automotive

- 5.3.3 BFSI

- 5.3.4 IT and Telecommunication

- 5.3.5 Media and Advertising

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia

- 5.4.4 Australia and New Zealand

- 5.4.5 Latin America

- 5.4.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 Wipro Limited

- 6.1.4 Hewlett Packard Enterprise

- 6.1.5 Microsoft Corporation

- 6.1.6 Amazon Web Services

- 6.1.7 Google Inc.

- 6.1.8 Intel Corporation

- 6.1.9 SAP SE

- 6.1.10 Sentient Technologies

- 6.1.11 AiCure LLC

- 6.1.12 NEC Corporation

- 6.1.13 NVIDIA Corporation

7 INVESTMENT ANALYSIS

8 FUTURE OF THE MARKET

企业人工智慧市场按组件、技术、公司规模、部署类型、应用和产业划分-2025-2032年全球预测

企业人工智慧市场按组件、技术、公司规模、部署类型、应用和产业划分-2025-2032年全球预测 全球企业法学硕士 (LLM) 市场规模、份额和行业分析报告:2025 年至 2032 年按公司规模、模型类型、组件、部署类型、行业垂直和地区分類的展望和预测

全球企业法学硕士 (LLM) 市场规模、份额和行业分析报告:2025 年至 2032 年按公司规模、模型类型、组件、部署类型、行业垂直和地区分類的展望和预测 企业法学硕士市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

企业法学硕士市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 企业AI服务:13通讯业者的案例研究与分析企业法学硕士 (LLM) 市场规模、份额和趋势分析报告:按组件、部署模式、模型类型、公司规模、行业垂直、地区和细分市场预测,2025 年至 2033 年

企业AI服务:13通讯业者的案例研究与分析企业法学硕士 (LLM) 市场规模、份额和趋势分析报告:按组件、部署模式、模型类型、公司规模、行业垂直、地区和细分市场预测,2025 年至 2033 年 全球企业人工智慧市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测企业人工智慧 (AI) 市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户和功能

全球企业人工智慧市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测企业人工智慧 (AI) 市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、部署、最终用户和功能 企业人工智慧市场报告,按组件、部署模式、技术(自然语言处理、机器学习、电脑视觉、语音识别等)、组织规模、产业垂直和地区划分,2025 年至 2033 年

企业人工智慧市场报告,按组件、部署模式、技术(自然语言处理、机器学习、电脑视觉、语音识别等)、组织规模、产业垂直和地区划分,2025 年至 2033 年 企业人工智慧市场:2025-2029 年全球

企业人工智慧市场:2025-2029 年全球 企业人工智慧 (AI) 市场按部署类型、技术、组织规模、垂直领域和地区划分

企业人工智慧 (AI) 市场按部署类型、技术、组织规模、垂直领域和地区划分