|

市场调查报告书

商品编码

1630287

阀门和致动器:市场占有率分析、行业趋势和统计、成长预测(2025-2030)Valves And Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

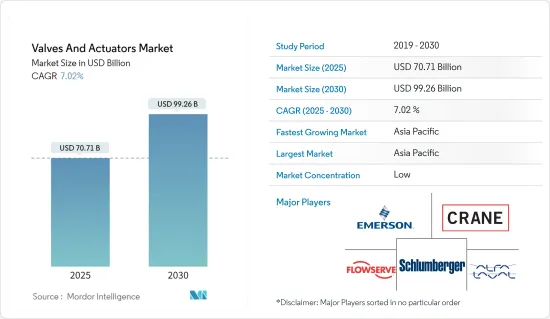

阀门和致动器市场规模预计到 2025 年为 707.1 亿美元,预计到 2030 年将达到 992.6 亿美元,预测期内(2025-2030 年)复合年增长率为 7.02%。

阀门和致动器市场包括供应商为石油、天然气和发电行业提供的各种阀门和致动器。市场规模由每个行业供应商产生的收益决定。

石油和天然气探勘计划、运输管道计划和持续维护活动对控制阀的需求量很大。在先进技术进步的推动下,该市场正在快速成长,为智慧致动器的发展铺平了道路。这些智慧致动器无缝整合感测器、马达、通讯模组和控制器。它的适应性使其易于调整、安装和拆卸,使其成为各种工业领域机器人的主要产品。

随着阀门和致动器技术的进步,工程师正在优先考虑能够提供准确性能、减少功耗并最大限度减少环境碳排放的解决方案。解决传统阀门技术的这些挑战正在推动市场成长。

海水淡化可以去除海水中的盐和矿物质,对于多种产业至关重要。製造业、食品加工和农业等行业越来越依赖清洁水,推动了对海水淡化的需求,将其作为解决日益严重的水资源短缺的关键解决方案。

阀门和致动器在水处理厂、发电、炼油厂、采矿和食品生产中至关重要。然而,由于工业成长疲软,特别是在已开发国家,对这些零件的需求停滞不前。

总体而言,由于电力和化学行业需求的增加、海水淡化活动的需求以及先进技术的采用,对许多行业至关重要的阀门和致动器市场正在成长。

阀门和致动器市场趋势

石油和天然气领域占主要市场占有率

- 石油和天然气领域是致动器市场的重要组成部分,因为致动器对于调节管道中的石油和天然气流量、维护安全系统以及自动化上游和下游的许多任务至关重要。由于需要可靠、持久且准确的控制系统,致动器已在工业中广泛应用。在日益复杂的采矿和精製过程中尤其如此。为了确保石油和天然气设施的安全有效运行,此类致动器用于控制阀门自动化和防喷器以及其他关键设备等应用。

- 在石油和天然气领域,深海探勘和生产活动的增加大大增加了对海底致动器的需求。恶劣的水下环境需要海底致动器来操作设备。最近的进展旨在使这些致动器更加可靠和耐用,使其能够承受腐蚀环境、高压和低温。例如,致动器製造商Rotork开发了一种先进的海底电动致动器,其性能和寿命已提高,以满足深海计划的要求。

- 石油和天然气产业正在加速采用数位和致动器致动器,以提高营运效率和安全性。这些智慧致动器的传感器和通讯功能可实现即时监控、诊断和控制。 Bettis RTS 智慧电动致动器由业界领导者艾默生电气製造,具有先进的诊断和远端控制功能。这使您能够更有效地管理石油和天然气营运。

- 工业阀门有多种形状和尺寸,每种都有不同的功能,包括闸阀、截止阀、球阀、蝶阀、止回阀、压力阀和隔膜阀。随着商业建筑和自动化计划越来越依赖阀门,预计未来几年对工业燃气阀门的需求将会增加。这一激增将受到技术进步、工业化和都市化程度的提高以及现有设施的扩建的推动。

- 2024 年 2 月,塞勒姆市有 3,000 个家庭在城市燃气发行(CGD) 网路下註册使用家用管道天然气 (D-PNG)。印度石油公司 (IOCL) 已为 1,550 个家庭安装了电錶。

- 据贝克休斯称,北美是世界上最大的石油和天然气钻机所在地。截至2024年5月,该地区有700个陆上钻机和22个海上钻机。到2023年,全球石油钻机平均数量将超过1,800个。

- 探勘和生产作业中对可靠控制系统的需求、不断增长的液化天然气基础设施以及全球能源需求都促使石油和天然气行业成为致动器。海底致动器和智慧致动器的最新技术趋势,以及对环境合规性和安全性的重视,使该行业在充满挑战的市场中更具弹性。

亚太地区成长强劲

- 中国正在大力投资工业自动化,以提高製造效率并降低人事费用。随着工厂转向高度自动化流程,对作为这些系统重要组成部分的致动器的需求不断增加。

- 《中国製造2025》等中国政府倡议强调对自动化、技术研发和投资的关注。鑑于该国依赖从德国和日本进口的自动化设备,「中国製造」计画旨在加强国内生产并促进市场成长。

- 印度製定了一项国家製造业政策,旨在2025年将製造业占GDP的比重提高到25%,并透过印度政府等倡议,于2022年推出发展核心製造业以达到全球製造业标准的製造业政策。印度製造业正在逐步转向更自动化和流程主导的製造,这有望提高製造效率并增加产量,从而推动市场成长。

- 此外,国际贸易和工业部和能源部正在加强支持中小企业引进和推广智慧工厂技术。透过韩国技术资讯振兴院成立了智慧製造创新办公室。它还计划到2025年在10个重点产业拥有4500个智慧工厂。政府的此类积极措施有望刺激市场成长。

- 为了满足不断增长的需求,东南亚的天然气探勘活动不断增加,预计该地区石油和天然气公司对各种类型阀门的需求将会增加。马来西亚和印尼报告了上游的成功发现,其中包括穆巴达拉能源公司在南安达曼区块的重大发现。

阀门和致动器行业概述

阀门和致动器市场适度分散,国内外供应商都拥有数十年的经验。供应商采取了强有力的市场竞争策略,并大力投资广告以维持其在市场上的地位。

各大厂商都在积极引进创新技术。市场上的其他领导者正在专注于整合解决方案以吸引消费者。相较之下,小型和新兴供应商则优先考虑成本效益,从而扩大竞争格局。现在公共部门已接近成熟,重点正在转向私营部门。

品质认证、多样化的产品供应、有竞争力的价格和技术专长等关键因素对于赢得新契约至关重要。竞争公司之间的敌意仍然很高,并且预计在预测期内将持续下去。

市场主要参与者包括艾默生电气公司、斯伦贝谢有限公司、阿法拉伐公司、福斯公司、克瑞公司等。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

第五章市场动态

- 市场驱动因素

- 技术进步促进智慧阀门和致动器的应用

- 海水淡化需求增加

- 市场限制因素

- 已开发国家工业成长停滞

第六章市场细分:致动器

- 按类型

- 油压

- 气动

- 电动式

- 机械的

- 其他类型

- 按行业分类

- 石油和天然气

- 发电

- 化学

- 用水和污水

- 矿业

- 其他最终用户产业

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 亚洲

- 中国

- 日本

- 印度

- 韩国

- 澳洲/纽西兰

- 拉丁美洲

- 中东 非洲

- 北美洲

第七章市场细分:阀门

- 按类型

- 球

- 蝴蝶

- 门/手套/检查

- 插头

- 控制

- 其他类型

- 按行业分类

- 石油和天然气

- 发电

- 化学

- 用水和污水

- 矿业

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

第八章 竞争格局

- 公司简介

- Emerson Electric Co.

- Schlumberger Limited

- Alfa Laval Corporate AB

- Flowserve Corporation

- Crane Co.

- Rotork PLC

- Metso Oyj

- KITZ Corporation

- IMI Critical Engineering

- Samson Controls Inc.

第九章投资分析

第十章市场机会与未来趋势

The Valves And Actuators Market size is estimated at USD 70.71 billion in 2025, and is expected to reach USD 99.26 billion by 2030, at a CAGR of 7.02% during the forecast period (2025-2030).

The valves and actuators market encompasses various valves and actuators supplied by vendors catering to oil and gas and power generation industries. Market size is determined by the revenue generated by these vendors across industries.

Control valves see heightened demand from oil and gas exploration projects, transportation pipeline initiatives, and ongoing maintenance activities. The market is witnessing a surge, fueled by the push for advanced technologies, paving the way for the development of smart actuators. These smart actuators integrate sensors, motors, communication modules, and controllers seamlessly. Their adaptability allows for easy adjustments, setups, or dismantling, making them a staple in robots across various industries.

As valve and actuator technology advances, engineers prioritize solutions that deliver precise performance, consume less power, and minimize the environmental carbon footprint. This commitment to address the challenges of traditional valve technologies is fueling market growth.

Desalination, which is the process of removing salts and minerals from salty water, is essential for various industries. Industries such as manufacturing, food processing, and agriculture rely more on clean water, leading to a growing demand for desalination as a key solution to increasing water scarcity.

Valves and actuators are pivotal in water treatment plants, power generation, refineries, mining, and food production. Yet, demand for these components has stagnated, particularly in developed nations, due to sluggish industrial growth.

Overall, the valve and actuators market, integral to many industries, is growing, owing to rising demand from the power and chemical industries, the need for desalination activities, and the adoption of advanced technologies.

Valves And Actuators Market Trends

The Oil and Gas Segment Holds Major Market Share

- The oil and gas segment is an important contributor to the actuators market because actuators are essential for regulating the flow of gas and oil through pipelines, maintaining safety systems, and automating a number of tasks in both upstream and downstream operations. Actuators have become widely used in the industry due to the necessity for dependable, long-lasting, and accurate control systems. This is especially true in the increasingly complicated extraction and refining processes. To ensure the safe and effective functioning of oil and gas facilities, actuators in this category are utilized in applications such as valve automation blowout preventers and control of other essential equipment.

- The oil and gas segment increased exploration and production activities in deeper oceans, which has resulted in a major increase in demand for subsea actuators. Extreme underwater environments require subsea actuators to operate equipment. Recent advancements aim to make these actuators more dependable and durable, allowing them to resist corrosive environments, high pressures, and low temperatures. For example, in order to meet the requirements of deep-water projects, Rotork, an actuator manufacturer, has developed advanced subsea electric actuators that offer improved performance and longevity.

- To improve operational efficiency and safety, the oil and gas segment is embracing digital and smart actuation systems at an increasing rate. These smart actuators' sensors and communication capabilities enable real-time monitoring, diagnostics, and control. The Bettis RTS intelligent electric actuators, manufactured by the major industry player Emerson Electric, offer advanced diagnostic features and remote-control capabilities. This allows for more effective administration of oil and gas operations.

- Industrial valves are available in numerous shapes and sizes, including gate, globe, ball, butterfly, check, pressure, and diaphragm valves, each serving distinct functions. As commercial construction and automation projects increasingly rely on them, the demand for industrial gas valves is projected to rise in the coming years. This surge is fueled by technological advancements, heightened industrialization and urbanization, and the expansion of existing facilities.

- In February 2024, 3,000 households in Salem City were registered for domestic piped natural gas (D-PNG) under the city gas distribution (CGD) network. Indian Oil Corporation Limited (IOCL) has installed meters at 1,550 households.

- According to Baker Hughes, North America hosts oil and gas rigs globally. As of May 2024, the region boasted 700 land and 22 offshore rigs. In 2023, the global count of oil rigs surpassed 1,800 units on average.

- The necessity for dependable control systems in exploration and production activities, the growing LNG infrastructure, and the world's need for energy all contribute to the oil and gas segment's continued growth as a key growth area for actuators. Recent subsea and smart actuator technology developments and a strong emphasis on environmental compliance and safety have strengthened the segment's resilience in a challenging market.

Asia-Pacific to Register Major Growth

- China is investing significantly in industrial automation to enhance manufacturing efficiency and reduce labor costs. As factories transition to advanced automated processes, there is an increasing need for actuators, which are essential components in these systems.

- China's government initiatives, like the "Made in China 2025" plan, underscore its focus on automation, technology R&D, and investment. Given the reliance on imports from Germany and Japan for automation equipment, the "Made in China" initiative aims to strengthen domestic production and boost the market's growth.

- India is gradually progressing on the road to Industry 4.0 through the Government of India's initiatives like the National Manufacturing Policy, which aims to increase the share of manufacturing in GDP to 25% by 2025, and the PLI scheme for manufacturing, which was launched in 2022 to develop the core manufacturing industry at par with global manufacturing standards. The manufacturing industry in India is gradually shifting to more automated and process-driven manufacturing, which is expected to increase efficiency and boost production in the manufacturing industry, thereby driving market growth.

- Moreover, the Ministry of Trade, Industry, and Energy is strengthening its efforts by supporting SMEs in adopting and expanding smart factory technologies. They have established the Smart Manufacturing Innovation Office through the Korea Technology and Information Promotion Agency. Also, 10 significant industries are targeted to boast 4,500 smart factories by 2025. Such proactive government measures are poised to stimulate the market's growth.

- The increase in gas exploration activities in Southeast Asia to meet rising demand is expected to drive the need for various types of valves among oil and gas companies in the region. Malaysia and Indonesia have reported successful upstream discoveries, including a significant find by Mubadala Energy in the South Andaman Block.

Valves And Actuators Industry Overview

The valves and actuators market is moderately fragmented, featuring local and international vendors with decades of experience. Vendors are adopting robust competitive strategies, heavily investing in advertising to maintain their market presence.

Leading vendors are actively introducing innovative technologies. Other prominent players in the market are emphasizing integrated solutions to captivate consumers. In contrast, smaller and emerging vendors prioritize cost-benefit advantages, heightening the competitive landscape. With the public sector nearing maturity, a substantial focus is shifting toward the private sector.

Key factors like quality certification, diverse product offerings, competitive pricing, and technical expertise are pivotal in securing new contracts. The competitive rivalry remains high and is projected to persist during the forecast period.

Some of the major players in the market are Emerson Electric Co., Schlumberger Limited, Alfa Laval Corporate AB, Flowserve Corporation, and Crane Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Force Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technological Advancements Propelling Application of Smart Valves and Actuators

- 5.1.2 Increase in Demand for Desalination Activities

- 5.2 Market Restraints

- 5.2.1 Stagnant Industrial Growth in Developed Countries

6 MARKET SEGMENTATION - ACTUATORS

- 6.1 By Type

- 6.1.1 Hydraulic

- 6.1.2 Pneumatic

- 6.1.3 Electric

- 6.1.4 Mechanical

- 6.1.5 Other Types

- 6.2 By End-user Vertical

- 6.2.1 Oil and Gas

- 6.2.2 Power Generation

- 6.2.3 Chemical

- 6.2.4 Water and Wastewater

- 6.2.5 Mining

- 6.2.6 Other End User Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East Africa

- 6.3.1 North America

7 MARKET SEGMENTATION - VALVES

- 7.1 By Type

- 7.1.1 Ball

- 7.1.2 Butterfly

- 7.1.3 Gate/Globe/Check

- 7.1.4 Plug

- 7.1.5 Control

- 7.1.6 Other Types

- 7.2 By End-user Vertical

- 7.2.1 Oil and Gas

- 7.2.2 Power Generation

- 7.2.3 Chemical

- 7.2.4 Water and Wastewater

- 7.2.5 Mining

- 7.2.6 Other End User Verticals

- 7.3 By Geography

- 7.3.1 North America

- 7.3.2 Europe

- 7.3.3 Asia

- 7.3.4 Australia and New Zealand

- 7.3.5 Latin America

- 7.3.6 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Emerson Electric Co.

- 8.1.2 Schlumberger Limited

- 8.1.3 Alfa Laval Corporate AB

- 8.1.4 Flowserve Corporation

- 8.1.5 Crane Co.

- 8.1.6 Rotork PLC

- 8.1.7 Metso Oyj

- 8.1.8 KITZ Corporation

- 8.1.9 IMI Critical Engineering

- 8.1.10 Samson Controls Inc.

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

工业阀门致动器市场:动力来源、阀门类型、运作模式、材质、尺寸、压力等级和最终用户产业划分-2026-2032年全球市场预测电动阀门致动器市场:依产品、阀门类型、类型、电压、致动器尺寸、安装方式、最终用途产业划分,全球预测(2026-2032年)

工业阀门致动器市场:动力来源、阀门类型、运作模式、材质、尺寸、压力等级和最终用户产业划分-2026-2032年全球市场预测电动阀门致动器市场:依产品、阀门类型、类型、电压、致动器尺寸、安装方式、最终用途产业划分,全球预测(2026-2032年) 工业阀门及致动器市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、材质、最终用户、功能、安装类型划分阀门致动器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能和安装类型划分

工业阀门及致动器市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、材质、最终用户、功能、安装类型划分阀门致动器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能和安装类型划分 全球致动器和阀门市场规模、份额、趋势和成长分析报告(2026-2034)阀门致动器市场(依阀门类型、执行介质、致动器类型和最终用户产业划分)-2026-2032年全球预测

全球致动器和阀门市场规模、份额、趋势和成长分析报告(2026-2034)阀门致动器市场(依阀门类型、执行介质、致动器类型和最终用户产业划分)-2026-2032年全球预测 亚太地区阀门执行器市场预测至 2031 年 - 区域分析 - 按最终用户(采矿、液化天然气、化学、石油和天然气、水和废水处理等)和产品类型(电动、手动、液压和气动)

亚太地区阀门执行器市场预测至 2031 年 - 区域分析 - 按最终用户(采矿、液化天然气、化学、石油和天然气、水和废水处理等)和产品类型(电动、手动、液压和气动) 北美阀门执行器市场预测至 2031 年 - 区域分析 - 按最终用户(采矿、液化天然气、化学、石油和天然气、水和废水处理等)和产品类型(电动、手动、液压和气动)

北美阀门执行器市场预测至 2031 年 - 区域分析 - 按最终用户(采矿、液化天然气、化学、石油和天然气、水和废水处理等)和产品类型(电动、手动、液压和气动) 欧洲阀门执行器市场预测至 2031 年 - 区域分析 - 按最终用户(采矿、液化天然气、化学、石油和天然气、水和废水处理等)和产品类型(电动、手动、液压和气动)

欧洲阀门执行器市场预测至 2031 年 - 区域分析 - 按最终用户(采矿、液化天然气、化学、石油和天然气、水和废水处理等)和产品类型(电动、手动、液压和气动) 电动阀门致动器的全球市场:2024年

电动阀门致动器的全球市场:2024年