|

市场调查报告书

商品编码

1630294

半导体电池-市场占有率分析、产业趋势/统计、成长预测(2025-2030)Batteries For Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

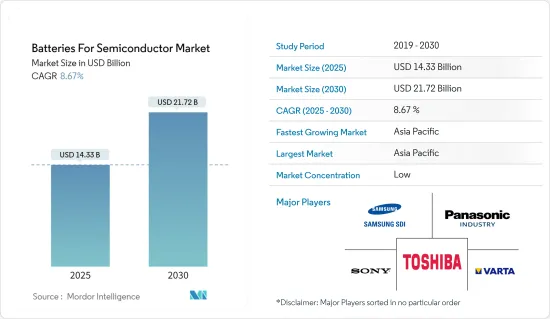

预计2025年半导体电池市场规模为143.3亿美元,预计2030年将达217.2亿美元,预测期内(2025-2030年)复合年增长率为8.67%。

从长远来看,电动车的普及和行动电话需求的增加预计将在预测期内推动市场发展。

另一方面,电池的技术挑战,如能量密度低、寿命短和充电能力慢等,预计将阻碍预测期内的市场成长。

由于能源储存系统日益普及,预计半导体电池市场将创造重大的机会。

由于亚太地区拥有大规模电池製造基础设施,预计亚太地区将成为消费电池市场的主导地区。

半导体电池市场趋势

电动车领域预计将获得巨大需求

- 电动车(EV)细分市场近年来经历了显着成长,这对半导体市场的电池需求产生了重大影响。随着电动车因其环境效益和技术进步而不断受到欢迎,对高效、可靠电池的需求变得至关重要。需求激增正在整个半导体市场产生连锁反应,为产业相关人员创造新的机会和挑战。

- 根据国际能源总署(IEA)预计,2022年全球电动车保有量将呈上升趋势,全球插电式轻型电动车累积销量约1,020万辆,成长率为2021年至2022年成长56.9%,2018年至2022年成长五倍。

- 支持电动车细分市场成长的关键因素之一是全球对环境问题的意识不断增强。政府和消费者正在倡导更清洁、更永续的交通,而电动车正成为可行的解决方案。因此,政府实施了各种激励措施、税收减免和法规来鼓励电动车的采用。因此,汽车製造商正在将重点转向电动车生产,从而推动半导体市场对先进电池技术的需求。

- 例如,2023年1月,加拿大政府宣布,从2026年起,该国销售的汽车中至少20%将是电动车。该公告旨在加速该国电动车的普及,以实现加拿大设定的碳排放目标。政府也宣布将为全国电动车电池製造企业提供生产诱因。

- 电动车细分市场的成长轨迹对半导体产业产生连锁影响,为市场相关人员创造各种机会。半导体製造商将有机会开发和供应电动车电池、电池管理系统和电力电子所需的尖端组件和晶片。这会增加收益潜力,并有机会在不断扩大的电动车市场中获得股权。

- 随着电动车销量的增加和政府措施的支持,半导体电池的研发活动预计将变得更加活性化。

亚太地区市场成长显着

- 亚太半导体电池市场是一个充满活力、充满活力的地区,对全球半导体产业影响重大。这个广阔而多样化的地区包括许多国家,每个国家都有自己的经济和技术前景。受快速工业化、家用电子电器产品使用量增加以及电动车市场快速成长等因素影响,亚太半导体市场的电池需求稳定成长。

- 亚太地区半导体电池需求的主要驱动力之一是家用电子电器产品的快速成长。这种增长是由可支配收入的增加和中产阶级人口的迅速增长所推动的,特别是在中国和印度等国家。这些消费者越来越多地采用智慧型手机、笔记型电脑和其他个人电子设备,导致对先进半导体电池为这些设备供电的需求不断增加。随着家用电子电器成为日常生活中不可或缺的一部分,亚太地区的半导体製造商准备从这个不断增长的市场领域中获利。

- 此外,亚太地区电动车的采用率正在显着增加。随着对环境永续性的日益关注以及政府对推广电动车的奖励,中国等国家正在成为电动车市场的重要参与企业。

- 例如,根据中国工业协会(AMMA)的数据,截至2023年5月,中国是最大的电动车(EV)市场,拥有79.3万辆插电式混合动力汽车(PHEV)和79.3万辆纯电动车(BEV)。 2022年,该国纯电动车销量将达545万辆,位居世界第一。预计在预测期内仍将是全球最大的电动车市场。

- 因为电动车需要高效可靠的半导体元件来管理电源和电池性能。因此,电动车市场的成长为亚太地区的半导体电池製造商提供了重大机会。

- 总之,亚太半导体市场的电池细分市场充满活力且快速发展。在家用电子电器和电动车的推动下,该地区对半导体电池的需求不断增长,为製造商带来了巨大的商机。因此,鑑于上述几点,亚太地区将在预测期内主导半导体电池市场。

半导体电池产业概况

半导体电池市场高度细分和整合。主要企业(排名不分先后)包括三星 SDI、索尼公司、松下公司、Varta AG 和东芝公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 对行动装置的需求增加

- 电动车的普及

- 抑制因素

- 存在技术问题

- 促进因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 种类

- 锂离子

- 镍金属氢化物

- 锂离子聚合物

- 钠离子电池

- 目的

- 家用电子电器产品

- 电动车

- 能源储存系统

- 其他最终用户用途

- 市场分析:按地区(2028 年之前的市场规模和需求预测)

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 欧洲其他地区

- 南美洲

- 智利

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 其他中东/非洲

- 北美洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- Samsung SDI Co Ltd.

- Sony Corporation

- Panasonic Corporation

- Varta AG

- Toshiba Corporation

- EnerSys

- GS Yuasa Corporation

- Faradion Limited

- Routejade

- TianJin Lishen Battery Joint-Stock Co. Ltd.

- Market Ranking/Share Analysis

第七章 市场机会及未来趋势

- 能源储存系统创新

The Batteries For Semiconductor Market size is estimated at USD 14.33 billion in 2025, and is expected to reach USD 21.72 billion by 2030, at a CAGR of 8.67% during the forecast period (2025-2030).

Over the long term, the increasing adoption of electric vehicles and demand for mobile phones are expected to drive the market during the forecasted period.

On the other hand, technological challenges of batteries, like low energy density, lower lifespan, and slower charging capacity, are expected to hinder the growth of the market during the forecasted period.

Nevertheless, the increasing adoption of energy storage systems is expected to create huge opportunities for the Batteries for Semiconductor Market.

Asia-Pacific is expected to be a dominant region for the Consumer Battery Market due to the presence of a large battery manufacturing infrastructure in the region.

Semiconductor Battery Market Trends

The Electric Vehicle Segment is Expected to Witness Significant Demand

- The electric vehicle (EV) market segment has witnessed substantial growth in recent years, and this has had a significant impact on the demand for batteries in the semiconductor market. As EVs continue to gain popularity due to their environmental benefits and technological advancements, the need for efficient and reliable batteries has become paramount. This surge in demand has generated a ripple effect throughout the semiconductor market, creating new opportunities and challenges for stakeholders in the industry.

- According to the International Energy Agency, global electric vehicles are on the rise in 2022; the cumulative plug-in light electric vehicle sales globally were around 10.2 million units, recording a growth rate of 56.9% between 2021 and 2022 and a fivefold increase between 2018 and 2022.

- One of the key drivers behind the growth of the EV market segment is the increasing global awareness of environmental concerns. Governments and consumers are advocating for cleaner and more sustainable modes of transportation, and EVs have emerged as a viable solution. This has led to various incentives, tax breaks, and regulations promoting the adoption of electric vehicles. As a result, automakers are shifting their focus towards EV production, thus bolstering the demand for advanced battery technologies within the semiconductor market.

- For instance, in January 2023, the Government of Canada announced that at least 20% of the vehicles sold in the country will be electric vehicles from 2026, and it will gradually increase to 60% in 2030 and reach 100% by the end of 2035. This announcement was made to increase the adoption of electric vehicles in the country to meet the carbon emission targets set by Canada. The government has also announced offering production incentives to companies manufacturing electric vehicle batteries nationwide.

- The electric vehicle market segment's growth trajectory has a cascading effect on the semiconductor industry, creating a range of opportunities for market players. Semiconductor manufacturers have a chance to develop and supply the cutting-edge components and chips required for EV batteries, battery management systems, and power electronics. This translates to increased revenue potential and the chance to capitalize on the expanding EV market.

- With the increasing sales of electric vehicles and the supportive government policies, the segment is expected to increase further, increasing the research and development activities in the battery for semiconductor segment.

Asia-Pacific Account for Significant Market Growth

- The Asia-Pacific market segment for batteries in the semiconductor market is a pivotal and dynamic region with significant implications for the global semiconductor industry. This vast and diverse region encompasses many countries, each with its unique economic and technological landscape. The demand for batteries in the semiconductor market within the Asia Pacific region has been steadily rising, driven by factors that include rapid industrialization, increasing consumer electronics usage, and the burgeoning electric vehicle market.

- One of the critical drivers for the demand for semiconductor batteries in the Asia-Pacific region is the exponential growth in consumer electronics. This growth is driven by rising disposable incomes and a surging middle-class population, especially in countries like China and India. These consumers are increasingly adopting smartphones, laptops, and other personal electronic devices, which, in turn, fuels the need for advanced semiconductor batteries to power these gadgets. As consumer electronics become an integral part of everyday life, semiconductor manufacturers in the Asia-Pacific region are poised to benefit from this growing market segment.

- Additionally, the Asia-Pacific region has witnessed a substantial uptick in electric vehicle adoption. With an increasing focus on environmental sustainability and government incentives to promote electric vehicles, countries like China have become significant players in the electric vehicle market.

- For instance, according to the China Association of Automobile Manufacturers (AMMA), as of May 2023, China is the largest market for electric vehicles (EV), with an estimated 0.793 million plug-in hybrid Electric vehicles (PHEVs) and 2.146 million battery electric vehicles (BEVs) being sold. In 2022, the country recorded the highest sales of battery electric vehicles, with 5.45 million. It is expected to remain the world's largest electric car market during the forecast period.

- This, in turn, has led to soaring demand for advanced batteries in the semiconductor market, as EVs require efficient and reliable semiconductor components to manage power and battery performance. The growth of the electric vehicle market, therefore, offers substantial opportunities for semiconductor battery manufacturers in the Asia-Pacific region.

- In conclusion, the Asia-Pacific market segment for batteries in the semiconductor market is a dynamic and rapidly evolving landscape. The region's growing demand for semiconductor batteries, driven by consumer electronics and electric vehicles, offers significant opportunities for manufacturers. Therefore, per the above points, the Asia-Pacific region will dominate the battery for semiconductor market during the forecasted period.

Semiconductor Battery Industry Overview

The batteries for semiconductor market are highly fragmented and consolidated. The major companies (in no particular order) include Samsung SDI Co Ltd, Sony Corporation, Panasonic Corporation, Varta AG, and Toshiba Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand for Mobile Devices

- 4.5.1.2 Rising Adaption of Electric Vehicles

- 4.5.2 Restraints

- 4.5.2.1 Availability of Technical Challenges

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Lithium-Ion

- 5.1.2 Nickel-Metal Hydride

- 5.1.3 Lithium-Ion Polymer

- 5.1.4 Sodium-Ion Battery

- 5.2 End-User Application

- 5.2.1 Consumer Electronics

- 5.2.2 Electric Vehicles

- 5.2.3 Energy Storage System

- 5.2.4 Other End-User Applications

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 India

- 5.3.2.3 Japan

- 5.3.2.4 South Korea

- 5.3.2.5 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Chile

- 5.3.4.2 Brazil

- 5.3.4.3 Argentina

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Samsung SDI Co Ltd.

- 6.3.2 Sony Corporation

- 6.3.3 Panasonic Corporation

- 6.3.4 Varta AG

- 6.3.5 Toshiba Corporation

- 6.3.6 EnerSys

- 6.3.7 GS Yuasa Corporation

- 6.3.8 Faradion Limited

- 6.3.9 Routejade

- 6.3.10 TianJin Lishen Battery Joint-Stock Co. Ltd.

- 6.4 Market Ranking/Share Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation in Energy Storage System

电池物联网市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、形式、材料类型、最终用户和功能

电池物联网市场分析及预测(至 2034 年):类型、产品、服务、技术、组件、应用、形式、材料类型、最终用户和功能 全球启动照明点火器电池市场(按电池化学成分、应用、最终用户和销售管道)预测 2025-2032

全球启动照明点火器电池市场(按电池化学成分、应用、最终用户和销售管道)预测 2025-2032 木质电池市场-全球产业规模、份额、趋势、机会和预测,按类型、材料来源、应用、地区和竞争细分,2020-2030 年电池市场按电池技术、应用、外形规格和容量范围划分-2025-2032年全球预测电池结构件市场-全球产业规模、份额、趋势、机会与预测(细分、按类型、按应用、按电池类型、按地区、按竞争,2020-2030 年预测)矿山机械电池市场-全球产业规模、份额、趋势、机会及预测(按类型、产能、应用、地区和竞争,2020-2030 年)

木质电池市场-全球产业规模、份额、趋势、机会和预测,按类型、材料来源、应用、地区和竞争细分,2020-2030 年电池市场按电池技术、应用、外形规格和容量范围划分-2025-2032年全球预测电池结构件市场-全球产业规模、份额、趋势、机会与预测(细分、按类型、按应用、按电池类型、按地区、按竞争,2020-2030 年预测)矿山机械电池市场-全球产业规模、份额、趋势、机会及预测(按类型、产能、应用、地区和竞争,2020-2030 年) 2025年无钴电池全球市场报告2025年全球盐水电池市场报告氧化银电池市场类型、电压、容量、电池尺寸、销售管道和应用—2025-2030 年全球预测全球电子设备电池市场

2025年无钴电池全球市场报告2025年全球盐水电池市场报告氧化银电池市场类型、电压、容量、电池尺寸、销售管道和应用—2025-2030 年全球预测全球电子设备电池市场