|

市场调查报告书

商品编码

1630301

收缩和弹力套筒标籤:市场占有率分析、行业趋势和成长预测(2025-2030)Shrink And Stretch Sleeve Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

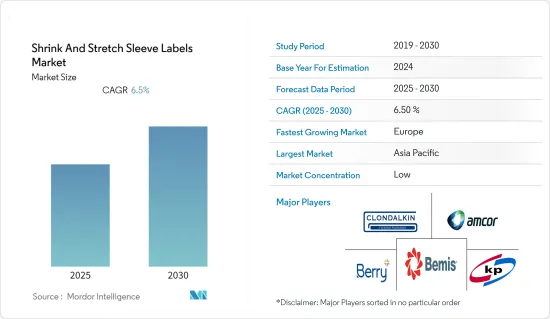

收缩和弹力套筒标籤市场预计在预测期内复合年增长率为 6.5%。

主要亮点

- 这些标籤是一种先进的标籤解决方案,与传统的不干胶标籤相比具有显着的优势。广泛应用于食品饮料、家居用品、化工包装等各行业。

- 由于对创新且具有视觉吸引力的包装解决方案的需求不断增加,收缩和弹力套筒标籤市场在过去十年中经历了显着增长。这种成长是由印刷技术的进步以及竞争市场中对产品差异化日益增长的需求所推动的。

- 这些标籤由 PVC、PETG 和 OPS 等聚合材料製成,可包装您的产品并提供无缝的 360 度品牌宣传机会。与传统标籤相比,这种全身标籤具有显着优势,允许品牌利用整个表面区域进行行销和资讯宣传。在这些标籤上列印高解析度图形和鲜艳色彩的能力提高了品牌知名度和消费者兴趣。

- 这种趋势在食品和饮料产业尤其明显,视觉吸引力直接影响消费者的购买决策。此外,製药和个人护理行业依赖这些标籤来符合复杂的几何形状、提供防篡改功能并增强整体产品吸引力。收缩和弹力套筒标籤用途广泛,足以适应各种容器形状和尺寸,使其成为希望提高货架展示度和品牌认知度的製造商的首选。

- 全球收缩和弹力套筒标籤市场主要由亚太地区主导,地区差异较大。该地区的成长是由强大的製造业、不断增长的中等收入人口以及对包装商品不断增长的需求所推动的。中国、印度、日本等重点市场以先进技术和大规模产能领先。

- 儘管收缩和弹力套筒标籤市场有着光明的成长轨迹,但它也面临重大挑战。其中最主要的是塑胶材料对环境的影响,监管机构和具有环保意识的消费者对塑胶材料的审查越来越严格。

收缩和弹力套筒标籤市场趋势

增加各种产品货架吸引力的需求预计将推动市场

- 收缩和弹力套筒标籤市场的主要成长要素是增强产品商店吸引力的需求不断增长。消费品产业的竞争日益激烈,促使品牌采取创新策略来脱颖而出。收缩和弹力套筒标籤以其全身覆盖和高品质印刷而闻名,是一种有吸引力的解决方案。

- 360度品牌可以比传统标籤进行更精緻的设计,大大增加了货架上产品的视觉衝击力。这种知名度的提高吸引了消费者的注意力并导致销量增加。此外,包装饮料消费量的增加进一步加速了收缩和弹力套筒标籤市场的发展。

- 收缩和弹力套筒标籤越来越受欢迎,主要是因为它们的设计多功能性。它可以无缝地装入容器中,无论是瓶子、罐子还是不规则形状的容器,使其成为各种产品的完美选择。这种适应性使品牌能够创造出传统标籤无法实现的创新设计。

- 该公司现在正在整合雾面饰面、金属效果和触觉元素,以增强消费者的视觉和触觉体验。这些先进的包装能力对于希望在竞争激烈的市场中脱颖而出的品牌至关重要。

亚太地区在收缩和弹力套筒标籤市场中占据主要份额

- 亚太地区的收缩和弹力套筒标籤市场主要由中国和印度推动,但其成长背后有多个因素。这些包括都市化进程的加速、包装食品消费的增加、聚合物薄膜的可用性的提高以及更具成本效益的劳动力。都市化推动了消费品需求的增加,并增加了对高效包装解决方案的需求。

- 同时,由于生活方式的不断变化和可支配收入的增加,包装食品的消费量增加,使方便食品成为主流。製造此类套管所必需的聚合物薄膜的易得性确保了原料的稳定供应。此外,该地区具有竞争力的人事费用有助于降低生产成本,使这些标籤解决方案对製造商来说具有成本效益。

- 东南亚被称为对价格敏感的市场,随着收缩和拉伸套的推出,该市场有望显着成长。这些套筒以具有复杂设计的经济高效的装饰容器而闻名,并且在该地区的市场上越来越受欢迎。聚合物薄膜的现成供应和可承受的人事费用进一步增强了市场动力。鑑于该地区的价格敏感性,收缩和拉伸套已成为寻求平衡成本效率与优质包装的製造商的一个有吸引力的选择。此外,这些套筒可实现复杂的设计,使品牌能够在拥挤的货架上脱颖而出,增加对消费者的吸引力。

- 儘管中国和印度引领亚太市场,但该地区每个国家对 COVID-19 疫情都有自己独特的应对措施。值得注意的是,包装和标籤产业的製造和生产在包装对 GDP 贡献显着的国家中持续存在。这次疫情凸显了包装在保护产品安全和完整性、支持这些产业需求方面发挥的关键作用。包装工业强大的国家不仅保持了经济稳定,而且透过持续生产和创新标籤解决方案增强了国内生产总值。

- 每个地区的国家对加工食品的需求正在显着增加。由于拉伸和收缩薄膜的多功能性、耐用性和成本效益,製造商对它们越来越感兴趣。这种采用率的增加不仅帮助食品製造商提供更安全、更高品质的产品,而且还刺激了对拉伸套和收缩标籤的需求。

- 该薄膜的适应性使其能够适应各种容器形状和尺寸,满足各种包装需求。其耐用性使标籤在整个产品生命週期中保持完整和清晰,其成本效益吸引了寻求优化包装预算的製造商。因此,对这些标籤解决方案的需求只会不断增加,支持整个亚太市场的扩张。

收缩和弹力套筒标籤行业概述

收缩和弹力套筒标籤市场呈现出高度分散的竞争格局,以大量区域性中小企业为特征。不断增长的客製化需求正在推动这些中小企业的崛起,每家企业都针对客户需求量身定制特定细分市场。

主要企业正在采取策略性收购和伙伴关係关係,为市场带来创新解决方案。收缩和弹力套筒标籤市场的主要企业正在策略性地收购其他公司并与其他公司合作,以加强产品系列併推出创新解决方案。这些策略旨在加强我们的市场地位并满足消费者不断变化的需求。

- 2024 年 6 月,全球永续包装解决方案领导者 Amcor 与知名零嘴零食製造商 Lorenz Snacks 合作,为其扁豆涂层花生产品推出可回收包装。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家/消费者的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

- 宏观经济因素对市场的影响

- 标籤产业整体主要趋势分析(收缩标籤与套筒标籤份额比较)

第五章市场动态

- 市场概况

- 市场驱动因素

- 能够适合任何尺寸和形状并提供您所需的保护

- 提高商店各种产品吸引力的需求

- 防篡改的需求推动了收缩套管市场

- 市场挑战

- 饮料业对立式袋的需求不断增长以及整个回收过程的复杂性

- 市场机会

第六章 市场细分

- 按类型

- 收缩套管

- 拉伸套

- 按材质

- PVC

- PET

- PE

- OPP &OPS

- 其他材料(PO、PLA等)

- 按最终用户

- 食物

- 软性饮料

- 酒精饮料

- 化妆品/家居用品

- 药品

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 亚洲

- 中国

- 印度

- 日本

- 澳洲/纽西兰

- 拉丁美洲

- 中东/非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Bemis Company

- Berry Plastic Group Inc.

- Klockner Pentaplast Group

- Amcor PLC

- Clondalkin Group Holdings BZ

- Huhtamaki Oyj

- Schur Flexibles

- Cenveo Group

- Taghleef Industries

第八章 收缩标籤和套筒标籤主要树脂供应商

- Exxon Mobil Corporation

- Eastman Chemicals

- Lyondell Basell

- The Dow Chemical Company

- Celanese Corporation

- Indorama Group

- LG Chem Limited

- Carmel Olefins Limited

- Borealis Group

- Nova Chemicals

- SABIC Group

第九章投资分析

第十章市场展望

The Shrink And Stretch Sleeve Labels Market is expected to register a CAGR of 6.5% during the forecast period.

Key Highlights

- These labels represent advanced labeling solutions that offer significant advantages over traditional adhesive labels. They are extensively utilized across various industries, including food and beverage, household products, and chemical packaging.

- The shrink and stretch sleeve labels market has experienced significant growth over the past decade, driven by the increasing demand for innovative and visually appealing packaging solutions. This growth is attributed to advancements in printing technologies and the rising need for product differentiation in a competitive market.

- These labels, made from polymer materials such as PVC, PETG, and OPS, encase products, providing a seamless 360-degree branding opportunity. This full-body coverage offers substantial advantages over traditional labels, allowing brands to utilize the entire surface area for marketing and information purposes. The ability to print high-resolution graphics and vibrant colors on these labels enhances brand visibility and consumer engagement.

- This trend is particularly prevalent in the food and beverage industry, where visual appeal directly influences consumer purchasing decisions. Additionally, the pharmaceutical and personal care industries have adopted these labels for their ability to conform to complex shapes, provide tamper evidence, and enhance the product's overall appeal. The versatility of shrink and stretch sleeve labels in accommodating various container shapes and sizes makes them a preferred choice for manufacturers aiming to improve shelf presence and brand recognition.

- Asia-Pacific dominates the global shrink and stretch sleeve labels market, exhibiting significant regional disparities. The region's growth is driven by a robust manufacturing industry, a growing middle-income group, and increasing demand for packaged goods. Key markets such as China, India, and Japan lead the way, capitalizing on their advanced technology and large-scale production capabilities.

- Although the shrink and stretch sleeve labels market demonstrates a promising growth trajectory, it faces significant challenges. Chief among these is the environmental impact of plastic-based materials, which has attracted increased scrutiny from regulators and environmentally conscious consumers.

Shrink And Stretch Sleeve Labels Market Trends

Demand to Increase On-shelf Appeal of Various Products Expected to Drive the Market

- The rising demand for enhancing product shelf appeal is a primary growth driver for the shrink and stretch sleeve labels market. As competition intensifies in the consumer goods industry, brands are increasingly adopting innovative strategies for differentiation. Shrink and stretch sleeve labels, known for their full-body coverage and high-quality prints, present a compelling solution.

- Their 360-degree branding capability allows for more elaborate designs than conventional labels, significantly boosting a product's visual impact on the shelf. This increased visibility attracts more consumer attention and drives higher sales. Moreover, the growing consumption of packaged beverages is further accelerating the shrink and stretch sleeve labels market.

- Shrink and stretch sleeve labels are gaining traction primarily due to their design versatility. They conform seamlessly to containers, whether bottles, jars, or irregular shapes, making them an optimal choice for diverse products. This adaptability enables brands to implement innovative designs that traditional labels cannot achieve.

- Companies now incorporate matte finishes, metallic effects, and tactile elements, enhancing the consumer's visual and tactile experience. Such advanced packaging capabilities are essential for brands aiming to differentiate themselves in a competitive market.

Asia-Pacific Holds a Significant Share of the Shrink and Stretch Sleeve Labels Market

- The Asia-Pacific shrink and stretch sleeve labels market, primarily driven by China and India, owes its growth to several factors. These include increased urbanization, increased packaged food consumption, the ready availability of polymer films, and a cost-effective labor force. Urbanization has spurred greater demand for consumer goods, subsequently driving the need for efficient packaging solutions.

- Meanwhile, the uptick in packaged food consumption, attributed to evolving lifestyles and rising disposable incomes, has made convenience foods more mainstream. The easy accessibility of polymer films, crucial for crafting these sleeves, ensures a consistent raw material supply. Furthermore, the region's competitive labor costs help curb production expenses, rendering these labeling solutions more cost-effective for manufacturers.

- Southeast Asia, known for its price-sensitive market, is poised for significant growth in introducing shrink and stretch sleeves. These sleeves, known for their cost-effective embellishment of containers with intricate designs, are gaining favor in the regional market. With polymer films readily available and labor costs affordable, the market's momentum is further bolstered. Given the region's price sensitivity, shrink and stretch sleeves emerge as an appealing choice for manufacturers seeking to balance cost-efficiency with premium packaging. Moreover, the intricate designs achievable with these sleeves enable brands to stand out on crowded shelves, enhancing their appeal to consumers.

- While China and India lead the Asia-Pacific market, each country in the region responded uniquely to the COVID-19 pandemic. Notably, in nations where packaging significantly contributes to the GDP, the manufacturing and production of packaging and labeling industries have persevered. The pandemic underscored packaging's pivotal role in safeguarding product safety and integrity, sustaining demand in these industries. Countries with robust packaging industries have not only maintained economic stability but also bolstered their GDP through continuous production and innovative labeling solutions.

- Across regional countries, there has been a marked uptick in processed food demand. Manufacturers are increasingly turning to stretch and shrink films, drawn by their versatility, durability, and cost-effectiveness. This heightened adoption not only aids food manufacturers in delivering safer, higher-quality products but also fuels the demand for stretch sleeves and shrink labels.

- The films' adaptability allows them to fit various container shapes and sizes, catering to diverse packaging needs. Their durability ensures labels remain intact and legible throughout the product's lifecycle, while their cost-effectiveness appeals to manufacturers aiming to optimize packaging budgets. Consequently, the demand for these labeling solutions continues to rise, bolstering the Asia-Pacific market's overall expansion.

Shrink And Stretch Sleeve Labels Industry Overview

The shrink and stretch sleeve labels market exhibits a highly fragmented competitive landscape characterized by numerous regional small and medium-sized enterprises. The increasing demand for customization is fueling the emergence of these smaller players, each addressing a specific segment of customers' tailored requirements.

Key players are adopting strategic acquisitions and partnerships and bringing innovative solutions to the market. Key players in the shrink and stretch sleeve labels market are strategically acquiring and partnering with other companies to enhance their product portfolios and introduce innovative solutions. These strategies aim to strengthen their market position and meet the evolving demands of consumers.

- In June 2024, Amcor, a global player in sustainable packaging solutions, partnered with Lorenz Snacks, a prominent snack manufacturer, to introduce a recyclable package for its Lentil Coated Peanuts product.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Industry Attractiveness - Porter's Five Forces Analysis

- 4.1.1 Bargaining Power of Suppliers

- 4.1.2 Bargaining Power of Buyers/Consumers

- 4.1.3 Threat of New Entrants

- 4.1.4 Threat of Substitute Products

- 4.1.5 Intensity of Competitive Rivalry

- 4.2 Impact of Macroeconomic Factors on Market

- 4.3 Analysis of Key Trends in the Overall Labeling Industry (Share Comparison of Shrink and Sleeve Labels)

5 MARKET DYNAMICS

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Ability to Conform to any Size and Shape, and Yet Provide the Necessary Protection

- 5.2.2 Demand to Increase On-shelf Appeal of Various Products

- 5.2.3 Need for Tamper-evident Protection Will Drive the Shrink Sleeves Market

- 5.3 Market Challenges

- 5.3.1 Growing Demand for Stand-up Pouches in the Beverage Industry and Elaborate Nature of the Overall Recycling Process

- 5.4 Market Opportunities

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Shrink Sleeve

- 6.1.2 Stretch Sleeve

- 6.2 By Material

- 6.2.1 PVC

- 6.2.2 PET

- 6.2.3 PE

- 6.2.4 OPP & OPS

- 6.2.5 Other Materials (PO, PLA, etc.)

- 6.3 By End User

- 6.3.1 Food

- 6.3.2 Soft Drinks

- 6.3.3 Alcoholic Drinks

- 6.3.4 Cosmetics & Household

- 6.3.5 Pharmaceutical

- 6.3.6 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Japan

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bemis Company

- 7.1.2 Berry Plastic Group Inc.

- 7.1.3 Klockner Pentaplast Group

- 7.1.4 Amcor PLC

- 7.1.5 Clondalkin Group Holdings BZ

- 7.1.6 Huhtamaki Oyj

- 7.1.7 Schur Flexibles

- 7.1.8 Cenveo Group

- 7.1.9 Taghleef Industries

8 KEY RESIN SUPPLIERS OF SHRINK AND SLEEVE LABELS

- 8.1 Exxon Mobil Corporation

- 8.2 Eastman Chemicals

- 8.3 Lyondell Basell

- 8.4 The Dow Chemical Company

- 8.5 Celanese Corporation

- 8.6 Indorama Group

- 8.7 LG Chem Limited

- 8.8 Carmel Olefins Limited

- 8.9 Borealis Group

- 8.10 Nova Chemicals

- 8.11 SABIC Group

9 INVESTMENT ANALYSIS

10 MARKET OUTLOOK

按包装类型、印刷技术、应用和最终用途行业分類的拉伸套和收缩套筒标籤市场—2025-2032年全球预测

按包装类型、印刷技术、应用和最终用途行业分類的拉伸套和收缩套筒标籤市场—2025-2032年全球预测 2025年全球拉伸套和收缩套筒标籤市场报告

2025年全球拉伸套和收缩套筒标籤市场报告 2025-2029年全球收缩套标与弹力套筒标籤

2025-2029年全球收缩套标与弹力套筒标籤 套筒标籤市场:2025-2030 年预测

套筒标籤市场:2025-2030 年预测 欧洲收缩和弹力套筒标籤:市场占有率分析、行业趋势和成长预测(2025-2030)笔记型电脑内胆包市场:按材料、尺寸、保护类型、闭合类型、价格分布、分销管道和最终用户 - 2025-2030 年全球预测

欧洲收缩和弹力套筒标籤:市场占有率分析、行业趋势和成长预测(2025-2030)笔记型电脑内胆包市场:按材料、尺寸、保护类型、闭合类型、价格分布、分销管道和最终用户 - 2025-2030 年全球预测 2025 年至 2033 年套筒标籤市场(按类型、印刷技术、应用、最终用途和地区划分)

2025 年至 2033 年套筒标籤市场(按类型、印刷技术、应用、最终用途和地区划分) 套筒标籤市场:按原料、类型、最终用途行业和地区划分2030 年纸套市场预测:按产品、材料、印刷技术、应用和地区进行的全球分析

套筒标籤市场:按原料、类型、最终用途行业和地区划分2030 年纸套市场预测:按产品、材料、印刷技术、应用和地区进行的全球分析 套筒标籤市场:2024-2033年全球产业分析、规模、占有率、成长、趋势、预测

套筒标籤市场:2024-2033年全球产业分析、规模、占有率、成长、趋势、预测