|

市场调查报告书

商品编码

1630444

民航机航空燃油:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Commercial Aircraft Aviation Fuel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

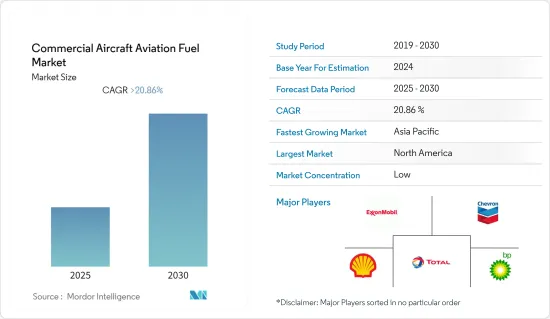

预计民航机航空燃油市场在预测期内复合年增长率将超过20.86%。

由于地区关闭,民航机燃油市场受到了 COVID-19 的负面影响。然而,市场在2021年开始復苏。

主要亮点

- 定期和不定期飞机都是民用航空的一部分。未来几年,市场将受到全球航空旅客数量和机持有数量增加的推动。

- 然而,航空燃油的高成本预计将抑制市场成长。

- 航空业的排放气体日益引起人们的关注,新兴经济体的政府正在采取措施减少航空业的排放气体。未来几年,民航机航空燃油可能会出现许多商机。

- 预计亚太地区将成为预测期内成长最快的市场,大部分需求来自中国、印度和日本等国家。

民航机航空燃油市场趋势

空气涡轮燃料 (ATF) 类型主导市场

- Jet-A 燃油自 20 世纪 50 年代起就在美国使用,但在美国以外以及多伦多和温哥华等加拿大一些机场通常不提供。 Jet-A 与 Jet-A1 具有相同的闪点,但其最高凝固点较高(-40°C)。根据 ASTM D1655 (Jet A) 规格提供。 Jet A1 适用于大多数涡轮发动机飞机。最低闪点为 38 度C(100 °F),最高凝固点为 -47 度C。 Jet A1 在美国以外广泛使用。

- LanzaTech 的乙醇基 ATJ-SPK 现在可作为标准 Jet A 的混合组件,供美国和世界上大多数国家的商业航空公司使用。随着 ASTM D7566 的修订,LanzaTech ATJ-SPK 可以与商业航班的传统喷射机燃料混合高达 50%。

- Jet A燃料见证了大学最近的发展趋势。例如,2021 年 6 月,华盛顿州立大学的研究人员开发了一种将废弃塑胶转化为永续 Jet A 燃料的製程。希望这项製程如果能改进并大规模应用,能够解决温室气体排放和塑胶污染等重大环境问题。

- 一级产业将航线数量和国际旅客数量最多的城市归类为「航空特大城市」(AMC)。据空中巴士称,共有66个AMC,超过60%的航班在这些城市起降,光是AMC之间就有17%的航班。随着世界各地 AMC 的增加,远距航班呈指数级增长,推动了对喷射机燃料的需求,从而推动了商业部门对航空燃油的需求。

- 因此,基于上述因素,航空涡轮燃油(ATF)预计将在预测期内主导民航机航空燃油市场。

亚太地区主导市场

- 亚太地区是民用领域重要的航空燃油市场之一。近年来,印度和东南亚等快速成长的市场对该地区的成长做出了越来越大的贡献,因为这些新兴经济体支持了强劲的客户成长。根据国际航空运输协会 (IATA) 的数据,到 2035 年,中国、印度、印尼和越南等亚太国家的客运量预计将达到最高水准。

- 此外,根据波音2021-2040年商业市场展望(CMO),到2040年,地区间流动的人数将大幅增加。因此,客运量的增加可能会为供应链中的每个人(尤其是新兴地区)带来许多机会来满足未来需求的增加和成长。

- 此外,商业航空公司的机队在过去十年中持续成长,截至 2022 年 1 月,全球共有 22,799 架飞机在使用。乘客数量与营运的商业航班数量直接相关,波音和空中巴士都在稳步增加订单和交付。

- 中国是世界上最大的航空燃油市场之一,也是航空客运量最大的市场之一。截至2021年,中国国内客运量已成为仅次于美国的第二大航空市场。

- 日本航空 (JAL) 和全日空航空 (ANA) 是日本的两大航空公司。然而,乐桃航空、捷星日本航空和香草航空等廉价航空公司(LCC) 正在增加市场占有率,并推动日本航空市场的发展。

- 由于所有这些因素,预计亚太地区将在预测期内引领民航机燃油市场。

民航机航空燃油产业概况

民航机燃油市场是细分的。主要参与企业(排名不分先后)包括埃克森美孚公司、雪佛龙公司、壳牌公司、TotalEnergies SE 和英国石油公司。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第二章调查方法

第三章执行摘要

第四章市场概况

- 介绍

- 至2028年市场规模及需求预测(单位:十亿美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 抑制因素

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔

- 燃料类型

- 空气涡轮燃料 (ATF)

- 航空生质燃料

- 其他燃料类型

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东/非洲

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- 传统航空燃油供应商

- Exxon Mobil Corporation

- Shell PLC

- TotalEnergies SE

- BP PLC

- Chevron Corporation

- 可再生航空燃料供应商

- Neste Oyj

- Swedish Biofuels AB

- Gevo Inc.

- Honeywell International Inc.

- 传统航空燃油供应商

第七章 市场机会及未来趋势

简介目录

Product Code: 71516

The Commercial Aircraft Aviation Fuel Market is expected to register a CAGR of greater than 20.86% during the forecast period.

The commercial aviation fuel market was adversely affected by COVID-19 due to regional lockdowns. However, the market rebounded in 2021.

Key Highlights

- Scheduled and non-scheduled aircraft are a part of commercial aviation. These planes carry people or goods for a fee.During the next few years, the market is likely to be driven by things like the growing number of air travelers and aircraft fleets around the world.

- However, the high cost of aviation fuel is expected to restrain market growth.

- Concerns about emissions from the airline industry are growing, and governments in developed economies are taking steps to reduce airline emissions. In the coming years, this is likely to create a lot of opportunities for commercial aircraft aviation fuel.

- Asia-Pacific is expected to be the fastest-growing market during the forecast period, with the majority of the demand coming from countries like China, India, Japan, etc.

Commercial Aircraft Aviation Fuel Market Trends

Air Turbine Fuel (ATF) Type to Dominate the Market

- Jet-A-specified fuel has been used in the United States since the 1950s, and it is usually not available outside the United States and a few Canadian airports, such as Toronto and Vancouver. Jet-A has the same flash point as Jet-A1 but a higher freeze point maximum (-40°C). It is supplied against the ASTM D1655 (Jet A) specification. Jet A1 is suitable for most turbine-engine aircraft. It has a flash point minimum of 38 °C (100°F) and a freeze point maximum of -47 °C. Jet A1 is widely available outside of the United States.

- LanzaTech's ethanol-based ATJ-SPK was made eligible for use as a blending component with standard Jet-A for commercial airline use in the United States and in most countries around the world. Under the revised ASTM D7566, LanzaTech ATJ-SPK is eligible to be used up to a 50% blend in conventional jet fuel for commercial flights.

- Jet-A fuels have been witnessing developments from universities in recent years. For instance, in June 2021, researchers at Washington State University developed a process for turning waste plastics into sustainable jet-A fuel. If the process is refined and applied on a large scale, the procedure is expected to address major environmental problems, including greenhouse gas emissions and plastic pollution.

- The primary industry classifies the cities with the most aviation connectivity and international passengers as "aviation megacities" (AMC). According to Airbus, there are 66 AMCs, with over 60% of traffic flying to and from these cities and 17% between AMCs alone. With the increase in AMCs across the world, long-haul flights are increasing exponentially, driving the demand for jet fuels and thus increasing the demand for aviation fuel in the commercial sector.

- Therefore, based on the above-mentioned factors, air turbine fuel (ATF) is expected to dominate the commercial aircraft aviation fuel market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is one of the significant aviation fuel markets in the commercial segment. In recent years, the fastest-growing markets, such as India and Southeast Asia, are increasingly contributing to the region's growth as these emerging economies have been endorsing robust passenger growth. As per the International Air Transport Association (IATA), in the Asia-Pacific region, countries including China, India, Indonesia, and Vietnam are expected to witness the highest passenger traffic by 2035.

- Furthermore, the Boeing Commercial Market Outlook (CMO) 2021-2040 says that the number of people traveling between the regions will go up a lot by 2040. So, the rise in passenger traffic is likely to give everyone in the supply chain, especially in emerging regions, a lot of chances to grow and meet the growing demand in the future.

- Also, commercial airline fleets have been growing over the past ten years, and as of January 2022, there were 22,799 planes in use around the world. The number of passengers is directly related to the number of commercial flights, and both Boeing and Airbus are steadily getting more orders and delivering more planes.

- China is one of the largest aviation fuel markets globally, and it is also one of the largest in terms of air passengers carried. As of 2021, domestic passengers in China were the second largest in the aviation market after the United States.

- Japan Airlines (JAL) and All Nippon Airways (ANA) are the two largest commercial airlines in Japan. However, low-cost carriers (LCCs) like Peach Aviation, Jetstar Japan, and Vanilla Air are gaining market share and boosting the aviation market in the country.

- Based on all of these factors, Asia-Pacific is expected to lead the market for aviation fuel for commercial aircraft during the forecast period.

Commercial Aircraft Aviation Fuel Industry Overview

The commercial aviation fuel market is fragmented. Some of the major players (in no particular order) include Exxon Mobil Corporation, Chevron Corporation, Shell PLC, TotalEnergies SE, and BP PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Fuel Type

- 5.1.1 Air Turbine Fuel (ATF)

- 5.1.2 Aviation Biofuel

- 5.1.3 Other Fuel Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 South America

- 5.2.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Conventional Aviation Fuel Suppliers

- 6.3.1.1 Exxon Mobil Corporation

- 6.3.1.2 Shell PLC

- 6.3.1.3 TotalEnergies SE

- 6.3.1.4 BP PLC

- 6.3.1.5 Chevron Corporation

- 6.3.2 Renewable Aviation Fuel Suppliers

- 6.3.2.1 Neste Oyj

- 6.3.2.2 Swedish Biofuels AB

- 6.3.2.3 Gevo Inc.

- 6.3.2.4 Honeywell International Inc.

- 6.3.1 Conventional Aviation Fuel Suppliers