|

市场调查报告书

商品编码

1635377

短波红外线成像:市场占有率分析、行业趋势和统计、成长预测(2025-2030)Short-wave Infrared Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

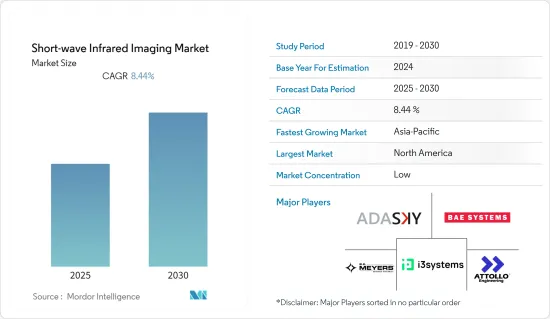

预计短波红外线成像市场在预测期内的复合年增长率为8.44%。

主要亮点

- 短波红外线 (SWIR) 成像是一种先进技术,可根据肉眼看不见的电磁波频谱区域的辐射产生影像。短波长红外线(SWIR) 成像的优点是感兴趣的辐射接近可见频谱,但通常可以检测 100°C 以上的温度。

- 短波长红外线(SWIR) 成像的波段为 0.7 至 2.5 μm。 SWIR 影像可用于多种应用,包括太阳能电池检查、电子基板检查、识别和分类、监控、防伪和製程品管。

- 车辆导航越来越依赖短波红外线相机。随着自动驾驶汽车的兴起,短波红外线技术可以帮助雾、雪、灰尘和雨中的导航。最近,以色列新兴企业TriEye 为消费汽车市场推出了一款安装在仪表板上的短波红外线相机,它可以成功地应对雪、雾、灰尘和雨水,解决了短波红外线相机在自动驾驶汽车中日益增长的使用问题。

- 世界各地正在对短波长红外线成像技术的开发进行大量投资。例如,2022年1月,利用奈米材料开发高性能短波长红外线成像的公司Emberion筹集了600万欧元,以加速其红外线成像业务的成长。

- 最近,以色列新兴企业TriEye针对消费性汽车市场推出了一款安装在仪表板上的SWIR相机,可在雪、雾、灰尘和雨中成功导航,并且支援SWIR相机在自动驾驶汽车中的使用扩展。根据纳斯达克的数据,到 2030 年,无人驾驶汽车可能会主导市场。因此,这些投资可能会为该领域的已开发市场创造空间。

- 随着公司之间不断测试、研究和合作开发自动驾驶汽车,自动驾驶汽车的数量预计在未来几年将稳定成长。例如,法国自动驾驶汽车製造商 Navya 宣布推出全电动式Autonom Cab,这是首款 100% 自动驾驶机器人计程车。法雷奥也与 Docomo 合作,共同开发联网汽车。

短波长红外线成像市场趋势

军事国防领域预计将大幅成长

- 热成像用于国防应用,因为它可以在近乎或完全黑暗的情况下实现高解析度视觉和识别。红外线 (IR) 波长对于军事和国防研究与开发至关重要,因为监视和瞄准是在夜间进行的。

- SWIR 系列弥补了可见光波长和红外线峰值热灵敏度之间的差距,散射小于可见光波长,并可检测远距的低水平反射光,使其成为透过烟雾和雾进行成像的理想选择。此外,短波红外线相机是用于安全和监控的有用设备,有时单独使用或与其他成像器结合使用。

- 2021 年 5 月,一家总部位于墨尔本的公司获得了一份合同,为陆军无人机配备下一代监视感测器,这些感测器使用红外线摄影机昼夜提供稳定的影像。该感测器技术旨在透过利用使用光电、短波和中波红外线摄影机、雷射测距和目标指定技术的成像系统来增强情报、监视和侦察 (ISR) 能力。

- 此外,2021 年 11 月,作为 ENVision 计画的一部分,DARPA 聘请了三个小组来开发增强型直视夜视设备,其尺寸和重量与普通眼镜相似。这三个组织开发了紧凑、轻巧的夜视眼镜,可从通用频宽提供 1.5 微米至 12 微米的频谱带,其中包括近红外线以及短波、中波和长波红外频谱频宽。

- 英国国会称,2020/21年度国防支出将为424亿英镑现金。与前一年同期比较,名义价值增加了 25 亿英镑,实际价值增加了 17 亿英镑。因此,2024/25年度国防现金预算将比2020/21年度增加62亿英镑。然而,这种支出成长的实际价值很低,特别是考虑到通货膨胀不断上升。经通货膨胀调整后,国防支出预计将增加 15 亿英镑。

北美占最大市场占有率

- 美国拥有世界上最高的国防开支,是短波红外线相机和技术的主要市场之一。据美国国防部称,总统预算请求为7,054亿美元,较2020财年核准的7,046亿美元预算(不包括自然灾害应急资金)小幅增加约0.1%。面对资金减少,美国做出了一些艰难的决定,将资源集中在最重要的优先事项上。

- 为了促进这项决策,国防部长埃斯珀发起了一项全面的全国防审查,结果削减了近 57 亿美元,2021 财年的营运成本融资效率提高了2 亿美元,并进行了额外的活动和职能重组实现了价值 10 亿美元的服务业投资。该计划使国防部能够更有效地为更高级别的国防战略 (NDS) 优先事项提供资源。

- 该地区的公司正在寻求国内外公司的各种投资,以加强其热成像业务。例如,2021 年 10 月,工业自动化、自动驾驶汽车和其他应用的影像感测器解决方案提供商 SWIR Vision Systems Inc. 筹集了 500 万美元。这笔资金将用于推进该公司的 CQD 感测器解决方案,并发展其在全球工业和国防市场的 SWIR 相机业务。

- 2021 年5 月,Elbit Systems 宣布推出下一代先进多感测器有效负载系统(AMPS NG),主要在现有日间CCD(电荷耦合元件)电视感测器中添加短波红外线(SWIR) 技术,并具有独特的高性能双感测器。

- 此外,2022 年 1 月,大众市场短波红外线 (SWIR) 感测技术供应商 TriEye 宣布与汽车产品供应商 Hitachi Astemo 合作。两家公司将携手合作,透过加速TriEye技术的推出,进一步增强ADAS(高级驾驶辅助系统)在恶劣天气和照度条件下的能力。

短波红外线成像产业概述

短波红外线成像市场竞争激烈,国内外厂商活跃。国际玩家透过与当地玩家的合作在每个国家开展业务。随着市场预计将扩大并提供更多机会,更多参与者可能很快就会进入该市场。该市场的主要企业包括 BAE Systems、BE Myers & Company 和 Attro Engineering。

- 2022 年 2 月 - 总部位于芬兰埃斯波的 Emberion 推出具有宽频谱和宽动态范围成像性能的 VIS-SWIR(可见光/短波红外线)相机,以满足机器视觉和监控市场的需求,并宣布资金筹措。

- 2021 年11 月- 短波红外线(SWIR) 感测技术供应商TriEye 与英特尔和三星合作,将一种帮助自动驾驶和驾驶员辅助系统提高恶劣条件下的能见度的感测技术商业化,获得保时捷7400 万美元的融资。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 产业价值链分析

- COVID-19 对市场的影响

第五章市场动态

- 市场驱动因素

- 短波红外线相机在军事和国防领域的扩展

- 对小型化和低功耗技术的需求

- 自动驾驶汽车的扩张

- 市场挑战/限制

- SWIR 相机和检测器高成本

第六章 市场细分

- 按波长

- 1微米

- 1.7微米

- 2.1微米

- 依感测器类型

- 线感测器

- 影像仪

- 按集成级别

- 成像仪/线检测器

- 相机/系统

- 按最终用户产业

- 军事/国防

- 医疗保健与研究

- 车

- 其他最终用户产业

- 按地区

- 北美洲

- 亚太地区

- 欧洲

- 拉丁美洲

- 中东/非洲

第七章 竞争格局

- 公司简介

- Adasky, Ltd.

- BAE Systems Plc

- BE Meyers & Co.

- i3system

- Attollo Engineering

- Aixtron SE

- Alkeria SRL

- Allied Vision

- BaySpec

- Raptor Photonics

- STMicroelectronics NV

- Lockheed Martin

第八章投资分析

第9章 市场的未来

The Short-wave Infrared Imaging Market is expected to register a CAGR of 8.44% during the forecast period.

Key Highlights

- Short-wave infrared imaging (SWIR) is an advanced technique for producing images based on radiation in the region of the electromagnetic spectrum, which is invisible to the naked eye. Short-wave infrared (SWIR) imaging is distinct because the radiation of interest is nearer to the visible spectrum but will still permit temperature sensing, usually over 100 °C.

- Short-wave infrared (SWIR) imaging consists of a wavelength band from 0.7 - 2.5μm. SWIR imaging is used in various applications, including solar cell inspection, electronic board inspection, identification and sorting, surveillance, anti-counterfeiting, process quality control, etc.

- Vehicle navigation is increasingly relying on SWIR cameras. With the rise of self-driving cars, SWIR technology can assist in navigating through fog, snow, dust, and rain. Recently, Israeli start-up TriEye introduced a dashboard-mounted SWIR camera for the consumer car market that can successfully navigate through snow, fog, dust, and rain, responding to the expanding use of SWIR cameras in autonomous vehicles.

- A lot of investments are going on around the globe to develop short-wave infrared imaging technology. For instance, in January 2022, Emberion, a developer of high-performance short-wave infrared imaging using nanomaterials, raised EUR 6 million to accelerate infrared imaging business growth.

- Recently, Israeli start-up TriEye introduced a dashboard-mounted SWIR camera for the consumer car market that can successfully navigate through snow, fog, dust, and rain, responding to the expanding use of SWIR cameras in autonomous vehicles. According to a NASDAQ, driverless automobiles will likely dominate the market by 2030. Thus, these investments are also likely to create a scope for the market studied in this sector.

- Due to ongoing testing, research, and collaborations between companies to develop autonomous cars, the number of autonomous vehicles is anticipated to grow robustly in the upcoming years. For instance, French autonomous vehicle maker, Navya introduced an all-electric and fully autonomous Autonom Cab, the first 100% autonomous robot taxi. Another company, Valeo, partnered with Docomo to jointly develop connected cars.

Short-wave Infrared Imaging Market Trends

Military & Defense Segment is Expected to Have a Significant Growth

- Infrared imaging is used in defense applications to enable high-resolution vision and identification in near and total darkness. The infrared (IR) wavelengths are essential for military and defense research and development because surveillance and targeting occur at night.

- The SWIR region bridges the gap between visible wavelengths and peak thermal sensitivity of infrared, scattering less than visible wavelengths and detecting low-level reflected light at longer distances, which is ideal for imaging through smoke and fog. Moreover, SWIR cameras are useful security and surveillance devices, sometimes by themselves and often combined with other imagers.

- In May 2021, a Melbourne-based firm received a contract to equip the Army drones with next-generation surveillance sensors to provide stable images day or night using infrared cameras. The sensor technology aims to enhance intelligence, surveillance, and reconnaissance (ISR) capability by leveraging an imaging system that uses electro-optical, short wave, and medium wave infrared cameras, along with laser range finding and target designation technology.

- Moreover, in November 2021, DARPA hired three groups to develop enhanced direct-view night-vision systems of a size and weight near those of typical eyeglasses as a part of its ENVision program. These three organizations will develop small and lightweight night-vision eyeglasses to extend visual access beyond near-infrared to include short-wave, mid-wave, and long-wave infrared spectral bands through a common aperture giving users access to spectral ranges from 1.5 to 12 microns.

- According to the UK parliament, defense spending in 2020/21 was GBP 42.4 billion in cash terms. This is a nominal rise of GBP 2.5 billion over the previous year and a real increase of GBP 1.7 billion. As a result, the yearly defense budget in 2024/25 will be GBP 6.2 billion more in cash terms than in 2020/21. However, the real worth of this spending rise is lower, especially in light of growing inflation. Defense spending is estimated to rise by GBP 1.5 billion when adjusted for inflation.

North America Accounts For the Largest Market Share

- US defense spending is the highest in the world and one of the prominent markets for SWIR cameras and technology. According to the US Department of Defense, compared to the FY 2020 authorized amount of USD 704.6B (excluding natural disaster emergency funds), the President's budget request of USD 705.4B represents a minor gain of around 0.1%. Given this reduced funding level, the Department made several difficult decisions to ensure that resources are focused on the Department's top priorities.

- To facilitate that decision-making, Secretary of Defense Esper launched a comprehensive Defense-Wide Review, which resulted in nearly USD 5.7 billion in savings for FY 2021, USD 0.2 billion in Working Capital Fund efficiencies, and another USD 2.1 billion in activities and functions realigned to the Services. This program enabled the Department to better resource higher-level National Defense Strategy (NDS) priorities.

- Companies in the region are seeking various investments from national and international firms to boost their infrared imaging business. For instance, in October 2021, SWIR Vision Systems Inc., a provider of image sensor solutions for industrial automation, autonomous vehicles, and other applications, has raised USD 5 million, which will be used to advance the company's CQD sensor solutions to grow the company's SWIR camera business in the global industrial and defense markets.

- In May 2021, Elbit Systems announced the next generation of its Advanced Multi-Sensor Payload System (AMPS NG), primarily adding Shortwave Infrared (SWIR) technology into the existing day CCD (Charge-Coupled Device) TV sensors and a unique, highly capable dual FLIR sensor design.

- Furthermore, in January 2022, TriEye, the mass-market Short-Wave Infrared (SWIR) sensing technology provider, announced the collaboration with Hitachi Astemo, a supplier of automotive products. The companies will work together to further enhance the capabilities of advanced driver assistance systems (ADAS) for adverse weather and low-light conditions by accelerating the launch of TriEye technology.

Short-wave Infrared Imaging Industry Overview

The Short-wave Infrared Imaging Market is highly competitive, with several local and international players active. International participants operate in the countries through partnerships with local players. With the market expected to broaden and yield more opportunities, more players will enter the market soon. Key players in the market include BAE Systems, B.E Meyers & Co., and Attollo Engineering, among others. The recent developments in the market are -

- February 2022 - Espoo, Finland-based Emberion announced that the company had raised EUR 6 million in funding to address the needs of the machine vision and surveillance markets for VIS-SWIR (Visible/Short Wave Infrared) cameras with broad-spectrum and wide dynamic range imaging performance.

- November 2021 - TriEye, a Short-Wave Infrared (SWIR) sensing technology provider, has received USD 74 million in funding from Intel, Samsung, and Porsche to commercialize a type of sensing technology that can be used to help autonomous and driver assistance systems to see better in adverse conditions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption And Market Definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power Of Suppliers

- 4.2.2 Bargaining Power Of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat Of Substitutes

- 4.2.5 Intensity Of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Covid-19 on the market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in penetration of SWIR cameras in military & defense vertical

- 5.1.2 Need for Miniaturization and Low-power Consumption Technology

- 5.1.3 Increasing Adoption of Autonomous Vehicles

- 5.2 Market Challenges/Restraints

- 5.2.1 High Cost of SWIR Cameras and Detectors

6 MARKET SEGMENTATION

- 6.1 By Wavelength

- 6.1.1 1 micron

- 6.1.2 1.7 micron

- 6.1.3 2.1 micron

- 6.2 By Type of Sensors

- 6.2.1 Line detectors

- 6.2.2 Imagers

- 6.3 By Level of Integration

- 6.3.1 Imagers/ Line detectors

- 6.3.2 Cameras/Systems

- 6.4 By End-User Industries

- 6.4.1 Military & Defense

- 6.4.2 Healthcare & Research

- 6.4.3 Automotive

- 6.4.4 Other End-user Industries

- 6.5 By Geography

- 6.5.1 North America

- 6.5.2 Asia Pacific

- 6.5.3 Europe

- 6.5.4 Latin America

- 6.5.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Adasky, Ltd.

- 7.1.2 BAE Systems Plc

- 7.1.3 B.E Meyers & Co.

- 7.1.4 i3system

- 7.1.5 Attollo Engineering

- 7.1.6 Aixtron SE

- 7.1.7 Alkeria S.R.L

- 7.1.8 Allied Vision

- 7.1.9 BaySpec

- 7.1.10 Raptor Photonics

- 7.1.11 STMicroelectronics N.V

- 7.1.12 Lockheed Martin

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

短波红外线成像市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测

短波红外线成像市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察,以及2024-2032年预测 红外线成像市场—全球及区域分析:按技术、波长、应用、产业和地区划分-分析与预测(2025-2035)

红外线成像市场—全球及区域分析:按技术、波长、应用、产业和地区划分-分析与预测(2025-2035) 热成像建筑检测市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、最终用户、流程、安装类型、设备

热成像建筑检测市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、最终用户、流程、安装类型、设备 红外线成像软体市场:2025-2032年全球预测(依最终用户产业、应用、技术类型、波段范围、部署模式和产品类型划分)红外线成像市场(按产品、技术、波长、应用和分销管道)—2025-2030 年全球预测红外线成像市场:2025-2030 年预测

红外线成像软体市场:2025-2032年全球预测(依最终用户产业、应用、技术类型、波段范围、部署模式和产品类型划分)红外线成像市场(按产品、技术、波长、应用和分销管道)—2025-2030 年全球预测红外线成像市场:2025-2030 年预测 全球红外线热成像市场

全球红外线热成像市场 短波红外线成像市场预测(至 2032 年):按材料、扫描类型、波长、技术、应用、最终用户和地区进行的全球分析

短波红外线成像市场预测(至 2032 年):按材料、扫描类型、波长、技术、应用、最终用户和地区进行的全球分析 全球红外线成像市场(按类型、波长、组件、技术和应用)预测至 2030 年

全球红外线成像市场(按类型、波长、组件、技术和应用)预测至 2030 年 红外线热成像市场:全球产业分析、市场规模、份额、成长、趋势和未来预测(2025-2032)

红外线热成像市场:全球产业分析、市场规模、份额、成长、趋势和未来预测(2025-2032)