|

市场调查报告书

商品编码

1636085

整车物流 -市场占有率分析、产业趋势/统计、成长预测(2025-2030)Finished Vehicles Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

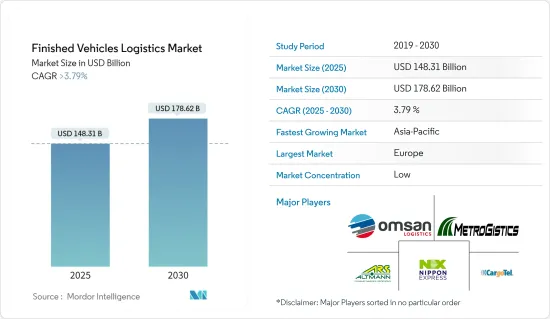

预计2025年整车物流市场规模为1,483.1亿美元,2030年将达1,786.2亿美元,预测期间(2025-2030年)复合年增长率将超过3.79%。

整车物流市场是全球汽车供应链的重要组成部分,负责车辆从製造地到最终消费者的无缝运输。 2024年,由于技术进步、环境法规收紧以及客户期望的变化,市场将发生重大演变,为相关人员创造机会和挑战。

塑造市场的显着趋势之一是越来越多地采用电动和替代燃料卡车。例如,CEVA Logistics于2024年9月宣布与比亚迪建立合作关係,并决定在2025年1月之前将四辆比亚迪ETH8电动卡车纳入其欧洲业务。这些车辆采用先进技术设计,续航里程达 250 公里,并具有快速充电功能,满足 CEVA 到 2050 年实现净零排放的更广泛目标。诸如此类的倡议强调物流业务的脱碳,同时保持效率。

此外,人们越来越重视多式联运,以优化物流效率和永续性。作为其绿色运输和物流计划的一部分,宝马正在其莱比锡工厂部署电动卡车,以展示公路和铁路系统的整合以减少排放。这些卡车每天行驶约 100 公里,凸显了该公司如何采用多式联运策略来满足监管要求并最大限度地减少对环境的影响。此外,物流公司正在利用数位双胞胎和远端资讯处理等技术来追踪车辆并提高业务效率。在 2024 年 IAA 运输活动上,此类创新被宣布为驾驭当今复杂物流网络的重要工具。

整车物流市场趋势

北美整车销售热潮刺激物流投资

2024年,汽车销售的快速成长将带动北美整车物流市场。这种繁荣正在推动对交通基础设施和物流解决方案的重大投资,特别是在美国、墨西哥和加拿大。为了满足这一需求,製造商和服务供应商正在微调其网络,以确保在整个全部区域及时交付。

United Road 于 2024 年 5 月进行扩张,利用其庞大的北美网路来提高服务速度和效率。此举凸显了对强大交通系统日益增长的需求。同时,主要企业Jack Cooper 扩大了在墨西哥的业务范围,推出了5 个新地点,并于 2024 年迎来 12 个新客户。这项扩张凸显了墨西哥快速成长的汽车产业在更广泛的区域物流框架中的至关重要性。

例如,通用汽车于 2024 年与北美物流供应商合作,简化供应链路线,以降低成本并缩短交货时间。这些努力由人工智慧驱动的路线优化和数数位双胞胎等最尖端科技提供支持,这些技术正在成为现代物流的主要内容。这些趋势凸显了北美物流格局,强调可扩展性和技术整合。

全球仓储和製造物流的成长

在全球范围内,整车物流市场正在发生重大变化。製造商和物流提供者正在大力投资先进的仓储和製造支援系统。这项变更主要是由于对高效车辆储存、加强库存管理以及最大限度地减少环境影响的共同努力的需求增加所推动的。

BMW透过制定 2024 年计画来强调这一趋势,该计画旨在将自动化和永续性发展纳入全球物流框架。透过在多个设施中实施自动化储存和搜寻系统,BMW不仅提高了效率,而且在实现碳中和目标方面取得了进展。这些升级后的仓库在BMW全球物流业务转型的综合策略中发挥着至关重要的作用。

此外,物流公司也越来越多地转向绿色解决方案来增强其仓库管理业务。 Vascor 就是一个例子,该公司于 2024 年中期推出了用于陆路物流的电动接驳车系统。除了抑制排放之外,此举还加强了製造地的永续性努力,并呼应了该行业对环保仓储业务的更广泛承诺。

CEVA Logistics 等全球领先公司正在倡导无缝整合公路、铁路和海运枢纽的多模态仓储策略,进一步凸显了这一趋势。 CEVA 的策略重点是将人工智慧和物联网技术纳入其仓库管理系统,帮助缩短储存週期并实现密切库存追踪。这些努力巩固了仓储和製造物流作为整车供应链业务效率的关键驱动因素日益增长的重要性。

整车物流行业概况

由于市场竞争极为激烈且分散,参与企业并没有占据很大的市场占有率。一些公司进行併购以扩大其地理足迹和专有资讯。例如,2022年10月,DFDS与土耳其领先的物流公司Ekol Logistics开始讨论收购Ekol Logistics的国际道路运输业务。地中海网路中渡轮和物流服务的结合将效仿北欧 DFDS 的成功经济模式。

主要参与企业包括 MetroGistics LLC、Nippon Express Holdings Inc.、Omsan Logistics、ARS Altmann 和 CargoTel Inc.。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究成果

- 研究场所

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态与洞察

- 市场概况

- 市场动态

- 市场驱动因素

- 新兴市场汽车销售成长

- 物流业务的技术进步

- 市场限制因素

- 司机短缺,劳动成本高

- 燃料成本上升和监管挑战

- 市场机会

- 拓展综合物流解决方案

- 市场驱动因素

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间的敌对关係

- 政府法规和倡议

- 供应链/价值链分析

- 洞察活动和物流领域的技术创新

- 地缘政治与疫情如何影响市场

第五章市场区隔

- 按活动

- 运输(铁路、公路、航空、海运)

- 仓库

- 附加价值服务

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 俄罗斯

- 欧洲其他地区

- 亚太地区

- 中国

- 日本

- 印度

- 孟加拉

- 土耳其

- 韩国

- 澳洲

- 印尼

- 其他亚太地区

- 中东/非洲

- 埃及

- 南非

- 沙乌地阿拉伯

- 其他中东/非洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 北美洲

第六章 竞争状况

- Market Concentration Analysis

- 公司简介

- MetroGistics LLC

- Nippon Express Holdings Inc

- Omsan Logistics

- CargoTel Inc.

- ARS Altmann

- CMA CGM SA

- Pound Gates Vehicle Management Services Ltd.

- CEVA Logistics

- Penske Corporation

- XPO Logistics*

- 其他公司

第七章 市场未来展望

第8章附录

- 宏观经济指标(GDP 分布,依活动划分)

- 经济统计-交通运输和仓储业对经济的贡献

- 对外贸易统计-进出口(分项)

The Finished Vehicles Logistics Market size is estimated at USD 148.31 billion in 2025, and is expected to reach USD 178.62 billion by 2030, at a CAGR of greater than 3.79% during the forecast period (2025-2030).

The finished vehicles logistics market is a critical component of the global automotive supply chain, responsible for the seamless transportation of vehicles from manufacturing hubs to end consumers. In 2024, the market is witnessing significant evolution driven by advancements in technology, stricter environmental regulations, and changing customer expectations, creating opportunities and challenges for stakeholders.

One prominent trend shaping the market is the increasing adoption of electric and alternative fuel-powered trucks. For instance, CEVA Logistics announced a partnership with BYD in September 2024 to incorporate four BYD ETH8 electric trucks into its European operations by January 2025. These vehicles, designed with advanced technology, support a range of 250 km and feature fast-charging capabilities, aligning with CEVA's broader goal to achieve net zero emissions by 2050. Such initiatives underscore the push toward decarbonizing logistics operations while maintaining efficiency.

Additionally, there is a growing emphasis on multimodal transportation to optimize logistics efficiency and sustainability. BMW has adopted electric trucks for its Leipzig facility as part of its "Green Transport Logistics Project," demonstrating the integration of road and rail systems to reduce emissions. These trucks cover approximately 100 km daily, highlighting how companies are embracing multimodal strategies to meet regulatory demands and minimize environmental impact. Furthermore, logistics companies are leveraging technology like digital twins and telematics to enhance vehicle tracking and operational efficiency. At the 2024 IAA Transportation event, such innovations were showcased as vital tools to navigate the complexities of modern logistics networks.

Finished Vehicles Logistics Market Trends

North America Finished Vehicle Sales Boom Driving Logistics Investments

In 2024, a surge in vehicle sales is propelling the North American finished vehicle logistics market. This upswing is prompting substantial investments in transport infrastructure and logistics solutions, especially in the U.S., Mexico, and Canada. In response to this demand, manufacturers and service providers are fine-tuning their networks to guarantee timely deliveries throughout the region.

Highlighting this trend, United Road expanded its operations in May 2024, capitalizing on its vast North American network to boost service speed and efficiency. This move underscores the growing demand for robust transport systems. In a parallel development, Jack Cooper, a key player in logistics, broadened its footprint in Mexico by launching five new locations and welcoming 12 new customers in 2024. This expansion underscores the pivotal significance of Mexico's burgeoning automotive sector in the broader regional logistics framework.

Furthermore, regional OEMs are gravitating towards collaborative logistics models.For instance, General Motors teamed up with North American logistics providers in 2024, streamlining its supply chain routes, which led to cost reductions and enhanced delivery timelines. Such initiatives are bolstered by cutting-edge technologies like AI-driven route optimization and digital twins, which are swiftly becoming staples in contemporary logistics. These trends highlight North America's evolving logistics landscape, marked by a keen emphasis on both scalability and technological integration.

Growth in Warehousing and Manufacturing Logistics Across the Globe

Across the globe, the logistics market for finished vehicles is witnessing a significant transformation. Manufacturers and logistics providers are channeling substantial investments into advanced warehousing and manufacturing support systems. This shift is primarily driven by a rising demand for efficient vehicle storage, enhanced inventory management, and a concerted effort to minimize environmental impact.

Highlighting this trend, BMW has rolled out a 2024 initiative aimed at weaving automation and sustainability into its global logistics framework. By deploying automated storage and retrieval systems across multiple facilities, BMW has not only boosted efficiency but also made strides towards its carbon neutrality objectives. These upgraded warehouses play a pivotal role in BMW's overarching strategy to revamp its global logistics operations.

Moreover, logistics companies are increasingly turning to green solutions to bolster their warehousing activities. A case in point is Vascor, which, in mid-2024, unveiled electric shuttle systems for landside logistics. This move not only curtails emissions but also bolsters sustainability efforts at manufacturing hubs, echoing the industry's broader commitment to eco-friendly warehouse practices.

Further underscoring this trend, global giants like CEVA Logistics are championing multimodal warehousing strategies, seamlessly integrating road, rail, and maritime transport hubs. CEVA's strategic emphasis on embedding AI and IoT technologies into its warehouse management systems has been instrumental in slashing storage durations and achieving meticulous inventory tracking. Such initiatives underscore the growing significance of warehousing and manufacturing logistics as pivotal drivers of operational efficiency in the finished vehicle supply chain.

Finished Vehicles Logistics Industry Overview

Because the market is extremely competitive and fragmented, players in the Finished Vehicles Logistics Market do not have a significant market share. Several firms are merging and acquiring to extend their geographical footprint and proprietary information. For instance, in October 2022, DFDS and Ekol Logistics, a major Turkish logistics firm, began discussions about acquiring Ekol Logistics' international road haulage operations. A combination of ferry and logistics services in the Mediterranean network would mimic DFDS' successful economic model in Northern Europe.

Some of the major players are MetroGistics LLC, Nippon Express Holdings Inc., Omsan Logistics, ARS Altmann, and CargoTel Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 Growing Vehicle Sales in Emerging Markets

- 4.2.1.2 Technological Advancements in Logistics Operations

- 4.2.2 Market Restraints

- 4.2.2.1 Driver Shortages and High Labour Costs

- 4.2.2.2 Rising Fuel Costs and Regulatory Challenges

- 4.2.3 Market Opportunities

- 4.2.3.1 Expansion of Multimodal Logistics Solutions

- 4.2.1 Market Drivers

- 4.3 Value Chain / Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Government Regulations and Initiatives

- 4.6 Supply Chain/Value Chain Analysis

- 4.7 Insights into Technological Innovation in the Events Logistics Sector

- 4.8 Impact of Geopolitics and Pandemic on the Market

5 MARKET SEGMENTATION

- 5.1 By Activity

- 5.1.1 Transport (Rail, Road, Air, Sea)

- 5.1.2 Warehouse

- 5.1.3 Value-added Services

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 France

- 5.2.2.3 United Kingdom

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Bangladesh

- 5.2.3.5 Turkey

- 5.2.3.6 South Korea

- 5.2.3.7 Australia

- 5.2.3.8 Indonesia

- 5.2.3.9 Rest of Asia-Pacific

- 5.2.4 Middle East & Africa

- 5.2.4.1 Egypt

- 5.2.4.2 South Africa

- 5.2.4.3 Saudi Arabia

- 5.2.4.4 Rest of Middle East & Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Company Profiles

- 6.2.1 MetroGistics LLC

- 6.2.2 Nippon Express Holdings Inc

- 6.2.3 Omsan Logistics

- 6.2.4 CargoTel Inc.

- 6.2.5 ARS Altmann

- 6.2.6 CMA CGM S.A

- 6.2.7 Pound Gates Vehicle Management Services Ltd.

- 6.2.8 CEVA Logistics

- 6.2.9 Penske Corporation

- 6.2.10 XPO Logistics*

- 6.3 Other Companies

7 FUTURE OUTLOOK OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators (GDP Distribution, by Activity)

- 8.2 Economic Statistics - Transport and Storage Sector Contribution to the Economy

- 8.3 External Trade Statistics - Export and Import, by Product

2026-2030年全球成品车物流市场

2026-2030年全球成品车物流市场 成品车物流市场规模、份额及成长分析(依运输方式、车辆类型、服务类型、最终用途及地区划分)-2026-2033年产业预测

成品车物流市场规模、份额及成长分析(依运输方式、车辆类型、服务类型、最终用途及地区划分)-2026-2033年产业预测 全球整车物流市场

全球整车物流市场 2024-2032年整车物流市场、机会、成长动力、产业趋势分析与预测

2024-2032年整车物流市场、机会、成长动力、产业趋势分析与预测