|

市场调查报告书

商品编码

1636193

艺术品物流:市场占有率分析、产业趋势/统计、成长预测(2025-2030)Art Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

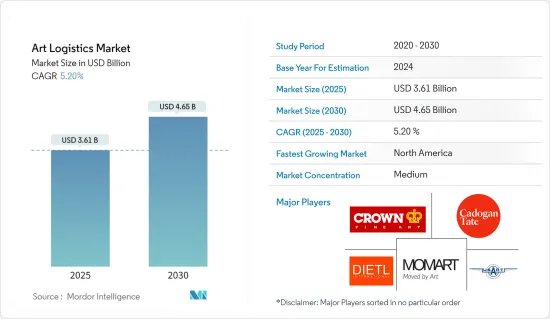

艺术品物流市场规模预计到 2025 年为 36.1 亿美元,预计到 2030 年将达到 46.5 亿美元,预测期内(2025-2030 年)复合年增长率为 5.2%。

艺术品物流市场主要受到高价值艺术品投资增加等因素的推动。

面对全球动盪,艺术市场展现了非凡的韧性。儘管遭受 2008 年金融危机和新冠肺炎 (COVID-19) 等重大经济挑战的挫折,我们仍持续反弹。儘管疫情期间下降了22%,但隔年迅速恢復,并于2022年成为全球第二大市场。儘管成长在 2023 年趋于稳定,但全球艺术品销售额仍超过 2019 年的水平,达到惊人的 650 亿美元。

过去十年,美国一直主导全球艺术市场,紧随其后的是中国和英国。到 2023 年,这三个国家总合将占市场销售额的近 80%。具体检验全球艺术品和NFT公开竞标销售情况,美国和中国已成为主要竞争对手,在艺术品竞标领域的差距正在缩小。

佳士得和苏富比这两家总部位于伦敦的竞标行都可以追溯到 18 世纪,是市场中的佼佼者。继2022年创下历史新高后,佳士得2023年全球销售额下降26%至60亿美元左右。相较之下,苏富比则小幅下滑,不到 1.5%,2023 年销售额略低于 80 亿美元。 2023年,Heritage 竞标、Bonhams和Phillips是销售额最高的竞标行,销售额均低于20亿美元。

艺术品物流市场趋势

艺术价值的上升推动了对专业运输服务的需求

随着艺术品价值的增加,对专业物流服务的需求也随之增加,以确保其安全运输和储存。艺术收藏家正在认识到他们作品的价值,并且越来越愿意为这些服务付费。随着收藏家和画廊参与全球艺术品贸易,对精通复杂的国际艺术品运输的物流提供者的需求正在迅速增加。由于收藏家经常需要为展览或新环境重新安置他们的藏品,因此这项需求进一步增加。 2023 年 2 月,印度艺术博览会总监强调了这一趋势,指出印度和南亚艺术品范围和多样性的扩大支撑了当代艺术品物流市场的成长。

私人收藏家要求对他们的作品格外小心,尤其是在气候控制环境中的运输过程中。对一流服务不断增长的需求推动了专业艺术品物流公司的崛起。

亚太地区成为领先的艺术品物流服务中心

在成熟的展览业的推动下,亚太艺术品物流市场正经历显着成长。这种演变正在推动艺术品物流公司的整合和标准化,使他们能够满足对可靠和专业的艺术品运输服务不断增长的需求。随着亚太艺术市场在艺术品收购和转售兴趣日益浓厚的推动下不断扩大,高效的艺术品运输、储存和处理变得至关重要。

为了满足这项需求,艺术品物流公司根据珍贵艺术品的独特需求提供专业的运输和仓储服务。 2023 年印度艺术博览会 85 家参展和 71 家画廊展示了这种增长,展示了来自印度和南亚的各种当代、现代和数位艺术。除了参展和画廊外,各种机构也参加了展会,凸显了艺术品物流市场的区域重要性。值得注意的是,印度及海外画廊的积极参与进一步提升了市场关注。

随着线上画廊的兴起和电子商务的扩张,该地区对艺术品物流服务的需求预计将激增。亚太地区正在大力投资建造新的博物馆和画廊,帮助创造新的商机。因此,亚太地区预计将在未来几年主导艺术品物流市场。

艺术品物流行业概况

艺术品物流市场较为分散。少数大公司的集中是显而易见的。 Crown Fine Art、Cadogan Tate、 美国 Art Company、Momart 和 Dietl International 等知名公司因其在处理和运输稀有艺术品方面的专业知识而脱颖而出。多年的行业经验和良好的业绩记录巩固了主导地位。

其他好处:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

- 分析方法

- 调查阶段

第三章执行摘要

第四章市场动态与洞察

- 目前的市场状况

- 市场动态

- 促进因素

- 艺术产品的需求不断增长推动市场

- 永续实践推动市场

- 抑制因素

- 影响市场的复杂运输挑战

- 气候条件如何影响市场

- 机会

- 艺术市场的全球化

- 促进因素

- 价值链/供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间的敌对关係

- 废弃物回收服务市场的技术开发

- COVID-19 对市场的影响

第五章市场区隔

- 按类型

- 运输

- 仓储及其他服务

- 按用途

- 艺术品经销商和画廊

- 竞标行

- 美术馆/博物馆

- 艺术博览会

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 英国

- 德国

- 法国

- 俄罗斯

- 义大利

- 西班牙

- 其他欧洲国家

- 亚太地区

- 印度

- 中国

- 日本

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东/非洲

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲

- 北美洲

第六章 竞争状况

- 市场集中度概况

- 公司简介

- Crown Fine Art

- Cadogan Tate

- US Art Company

- Momart

- Dietl International

- Gander & White

- Atelier4

- Helutrans Artmove

- Constantine

- 其他公司

第七章 市场的未来

第8章附录

- 总体经济指标

- 按部门分類的 GDP 分布

The Art Logistics Market size is estimated at USD 3.61 billion in 2025, and is expected to reach USD 4.65 billion by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

The art logistics market is mainly driven by factors such as an increase in investment in high-value art pieces.

The art market has showcased remarkable resilience in the face of global disruptions. Despite setbacks from major economic challenges, such as the 2008 financial crisis and the COVID-19 pandemic, it has consistently bounced back. Following a 22% decline at the onset of the pandemic, the global art market swiftly rebounded the next year, culminating in its second-highest value in 2022. Although the growth plateaued in 2023, global art sales still surpassed 2019 levels, reaching a notable USD 65 billion.

For the past decade, the United States has consistently dominated the global art market, with China and the United Kingdom following closely behind. In 2023, these three nations collectively accounted for nearly 80% of the market's sales. When specifically examining public auction revenues for fine art and NFTs worldwide, the United States and China emerged as the primary contenders, with a narrower gap separating them in the fine art auction arena.

Two London-based auction houses, Christie's and Sotheby's, both established in the 18th century, stand out as the market leaders. Christie's, after achieving a record high in 2022, saw a notable 26% decline in its global sales in 2023, settling at approximately USD 6 billion. In contrast, Sotheby's experienced a marginal drop of less than 1.5%, with its 2023 sales just shy of USD 8 billion. Following closely in 2023, Heritage Auctions, Bonhams, and Phillips emerged as the top revenue-generating auction houses, each with sales below USD 2 billion.

Art Logistics Market Trends

Rising Art Values Propel Demand for Specialized Transportation Services

As the value of art rises, so does the need for specialized logistics services to ensure its safe transport and storage. Art collectors, recognizing the value of their pieces, are increasingly willing to pay for these services. With collectors and galleries engaging in global art transactions, there is a surging demand for logistics providers adept at navigating the complexities of international art transport. This demand is further fueled by collectors often needing to relocate their collections for exhibitions or new environments. Highlighting this trend, in February 2023, the Director of the Indian Art Fair noted how the expanding scope and diversity of art in India and South Asia underscore the growth of the modern art logistics market.

Private collectors, particularly during transport in climate-controlled settings, demand meticulous care for their artworks. This heightened demand for top-tier service has spurred the rise of specialized fine art logistics firms.

Asia-Pacific Emerges as a Lucrative Hub for Art Logistics Services

The art logistics market in Asia-Pacific is witnessing substantial growth, driven by a maturing exhibition sector. This evolution has prompted art logistics companies to consolidate and standardize, enabling them to cater to the rising demand for reliable and professional art transport services. As the Asia-Pacific art market expands, fueled by a heightened interest in art acquisition and resale, the importance of efficient art transport, storage, and handling is paramount.

To address these demands, art logistics firms offer specialized transport and safekeeping services tailored to the unique needs of valuable artworks. Illustrating this growth, the India Art Fair 2023 featured 85 exhibitors and 71 galleries, showcasing a diverse array of contemporary, modern, and digital art from India and South Asia. The fair attracted not only exhibitors and galleries but also various institutions, underscoring the regional significance of the art logistics market. Notably, the event saw the active participation of Indian and international galleries, further emphasizing the market's prominence.

With the rise of online galleries and expanding e-commerce in the region, the demand for art logistics services is poised to surge. Asia-Pacific is witnessing substantial investments in the construction of new museums and art galleries, signaling a push to create fresh business avenues. Consequently, Asia-Pacific is anticipated to dominate the art logistics market in the coming years.

Art Logistics Industry Overview

The art logistics market is fragmented. It is marked by a notable concentration, largely steered by a handful of major players. Notable names such as Crown Fine Art, Cadogan Tate, U.S. Art Company, Momart, and Dietl International stand out for their expertise in handling and transporting valuable artworks. Their industry tenure and stellar track record have cemented their leading positions in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increased Demand for Art Driving the Market

- 4.2.1.2 Sustainable Practices Driving the Market

- 4.2.2 Restraints

- 4.2.2.1 Complex Transportation Challenges Affecting the Market

- 4.2.2.2 Climatic Conditions Might Affect the Market

- 4.2.3 Opportunities

- 4.2.3.1 Globalization of Art Market

- 4.2.1 Drivers

- 4.3 Value Chain/Supply Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technological Developments in the Waste Recycling Services Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Transportation

- 5.1.2 Storage and Other Services

- 5.2 By Application

- 5.2.1 Art Dealers and Galleries

- 5.2.2 Auction Houses

- 5.2.3 Museums

- 5.2.4 Art Fairs

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Italy

- 5.3.2.6 Spain

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Crown Fine Art

- 6.2.2 Cadogan Tate

- 6.2.3 U.S. Art Company

- 6.2.4 Momart

- 6.2.5 Dietl International

- 6.2.6 Gander & White

- 6.2.7 Atelier4

- 6.2.8 Helutrans Artmove

- 6.2.9 Constantine

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX

- 8.1 Macroeconomic Indicators

- 8.2 GDP Distribution by Sector

2026-2030年全球艺术品经销市场

2026-2030年全球艺术品经销市场 艺术基金市场:按基金类型、用途和地区划分

艺术基金市场:按基金类型、用途和地区划分 美术品·雕刻的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年)

美术品·雕刻的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年) 艺术品物流的世界市场

艺术品物流的世界市场 艺术品物流:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

艺术品物流:市场占有率分析、产业趋势与统计、成长预测(2024-2029)