|

市场调查报告书

商品编码

1636269

东南亚国协插电式混合动力汽车电池:市场占有率分析、产业趋势与成长预测(2025-2030)ASEAN Countries Plug-in Hybrid Electric Vehicle Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

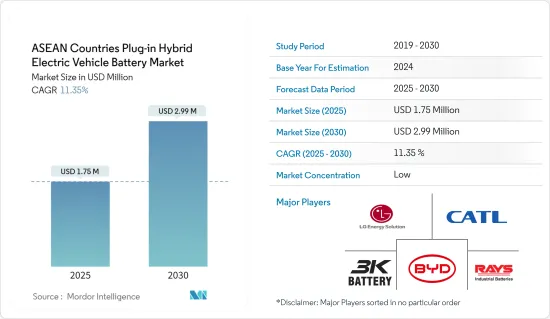

东南亚国协插电式混合动力汽车电池市场规模预计到2025年为175万美元,预计到2030年将达到299万美元,预测期内(2025-2030年)复合年增长率为11.35%。

主要亮点

- 未来几年,东南亚国协插电式混合动力车电池市场预计将受到电动车销售快速成长和锂离子电池成本下降的显着影响。

- 然而,市场面临更换成本上升的阻力,尤其是插电式混合动力汽车电池。

- 然而,旨在提高能量容量和续航里程的电池化学技术的不断进步预计将为市场带来许多机会。

- 预计印尼将在未来几年在所有国家的市场中占据主导地位。

东南亚国协插电式混合动力汽车电池市场趋势

乘用车带动成长

- 在政府措施、环境问题和技术进步的共同推动下,东协(东南亚国家联盟)国家的插混合动力汽车(PHEV)电池市场的乘用车领域正在经历显着增长。

- 随着都市化的加速和中阶的迅速壮大,东南亚国协对汽车的需求迅速增加。随着城市拥挤和污染加剧,世界各国政府正在采取更严格的排放法规和奖励来应对,以鼓励采用电动和混合动力汽车。

- 根据东协汽车联合会的资料,印尼将在 2023 年以 779,326 辆的销量领先,其次是马来西亚,销量为 719,160 辆。泰国表现出色,销量为 406,501 辆,其次是越南,销量为 230,706 辆,菲律宾则销量为 111,980 辆。新加坡有 32,511 套,缅甸有 2,832 套。这些销售数据证实了该地区对乘用车的需求不断增长。

- 补贴、退税和改善充电基础设施等政府措施正在支持整个东协插电式混合动力汽车的普及。此外,区域合作和研发投资正在巩固插电式混合动力汽车电池市场在东协汽车领域的重要性。

- 为了促进国内PHEV电池生产,泰国政府于2023年11月推出了「EV3.5」补贴计画。该政策的有效期为 2024 年至 2027 年,为生产的每个电池提供最高 2,760 美元的补贴。

- 两个主要目标是吸引外国投资并将泰国打造成东南亚插电式混合动力汽车汽车电池的领先生产国。随着中国插电式混合动力汽车品牌目前占据主导地位以及欧洲兴趣的增加,这项策略倡议可能有助于泰国在快速发展的插电式混合动力汽车电池领域的发展轨迹。

- 电池技术的进步正在决定性地塑造东协插电式混合动力汽车市场。尤其是锂离子电池的技术创新,透过提高能量密度、延长生命週期和实现快速充电,增加了插电式混合动力汽车的吸引力。

- 鑑于这些发展,乘用车市场在未来几年可能会成长。

印尼主导市场的前景

- 在政府政策、经济成长、消费行为和技术进步等因素的推动下,东协插电式混合动力汽车(PHEV)电池市场的印尼部分正在经历显着的转变。作为东南亚最大的经济体,印尼快速成长的汽车市场为插电式混合动力汽车产业带来了巨大的潜力。

- 印尼政府正积极致力于透过措施和措施减少碳排放并促进永续交通。这些倡议包括税收优惠、补贴,以及更重要的是充电基础设施的发展,旨在减轻通常与插电式混合动力电动车相关的高初始成本。

- 印尼工业部正在为电动和混合动力汽车汽车(包括电动摩托车)提供购买补贴。政府还计划为传统内燃机摩托车改装为电动摩托车提供补贴。购买新型电池驱动的电动车将获得5,130美元的补贴,而传统混合动力汽车将获得一半的补贴。

- 过去十年,电池技术和製造的突破加速了锂离子电池在印尼混合动力汽车中的采用。这些进步不仅降低了成本,还提高了性能和可靠性,使锂离子电池成为製造商和消费者的首选。

- 最近,锂离子电池和电池组的价格呈下降趋势,对终端用户产业有吸引力。继2022年小幅上涨后,2023年价格又恢復下跌,锂离子电池组价格创下139美元/kWh的历史低点,跌幅达14%。

- 此外,插电式混合动力汽车电池本地製造设施的兴起预计将降低製造成本。因此,插电式混合动力电动车将变得更容易被消费者接受。加上政府的激励措施和技术进步,经济转向负担得起的可持续交通将推动印尼插电式混合动力汽车市场的显着成长。

- 例如,2023年6月,印尼与四家着名的中国汽车製造商:哈普科内塔、五菱、奇瑞和小康签署了重要协议,将印尼定位为潜在的电动车出口中心。在与奇瑞汽车的讨论中,有明确的意图探索插电式混合动力汽车(PHEV)的国内製造途径。插电式混合动力车在中国已经很流行,因为它们比传统混合动力汽车更省油。奇瑞制定了雄心勃勃的计划,目标是到 2030 年部署 10 万辆电动车。

- 鑑于新兴市场的发展,印尼有望在未来几年引领市场。

东南亚国协插电式混合动力汽车电池产业概况

东南亚国协插电式混合动力汽车电池市场呈现半脱节结构。市场的主要企业(排名不分先后)包括 LG Energy Solution、Contemporary Amperex Technology、比亚迪公司、HDS Global Pte Ltd 和 3K Battery。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查范围

- 市场定义

- 研究场所

第 2 章执行摘要

第三章调查方法

第四章市场概况

- 介绍

- 2029年之前的市场规模与需求预测(单位:美元)

- 最新趋势和发展

- 政府法规和措施

- 市场动态

- 促进因素

- 电动车销量成长

- 锂离子电池价格下降

- 抑制因素

- 电池更换成本高

- 促进因素

- 供应链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品/服务的威胁

- 竞争公司之间的敌对关係

- 投资分析

第五章市场区隔

- 电池类型

- 锂离子电池

- 铅酸电池

- 钠离子电池

- 其他的

- 车型

- 客车

- 商用车

- 地区

- 新加坡

- 菲律宾

- 越南

- 泰国

- 马来西亚

- 印尼

- 其他东南亚国协

第六章 竞争状况

- 併购、合资、联盟、协议

- 主要企业策略

- 公司简介

- LG Energy Solution

- Contemporary Amperex Technology Co Ltd.

- BYD Company

- Panasonic Holdings Corporation

- Toshiba Corporation

- Enersys Sarl

- Exide Industries Ltd

- HDS Global Pte Ltd

- 3K Battery

- Clarios, LLC

- 其他知名公司名单

- 市场排名/份额(%)分析

第七章 市场机会及未来趋势

- 持续研究开发新的电池化学物质

简介目录

Product Code: 50003556

The ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market size is estimated at USD 1.75 million in 2025, and is expected to reach USD 2.99 million by 2030, at a CAGR of 11.35% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market is poised to be significantly influenced by surging electric vehicle sales and the plummeting costs of lithium-ion batteries.

- However, the market faces headwinds, notably from the steep replacement costs associated with plug-in hybrid electric vehicle batteries.

- Yet, ongoing advancements in battery chemistries, aimed at enhancing energy capacity and extending driving range, promise to unlock numerous opportunities for the market.

- Among all the countries, Indonesia is expected to dominate the market during the upcoming years.

ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Market Trends

Passenger Vehicles to Witness Growth

- Driven by a mix of government policies, environmental concerns, and technological advancements, the passenger vehicle segment of the plug-in hybrid electric vehicle (PHEV) battery market is experiencing notable growth in ASEAN (Association of Southeast Asian Nations) countries.

- With rapid urbanization and a burgeoning middle class, ASEAN nations are witnessing a surge in vehicle demand. As urban congestion and pollution escalate, governments are responding with stringent emission regulations and incentives to promote electric and hybrid vehicle adoption.

- Data from the ASEAN Automotive Federation highlights Indonesia's lead in 2023 with 779,326 units sold, trailed by Malaysia at 719,160 units. Thailand's market stands robust at 406,501 units, while Vietnam and the Philippines report 230,706 and 111,980 units, respectively. Singapore and Myanmar round out the figures with 32,511 and 2,832 units. Such sales figures underscore the growing appetite for passenger vehicles in the region.

- Government initiatives, including subsidies, tax rebates, and charging infrastructure development, are propelling the adoption of plug-in hybrid vehicles across ASEAN. Furthermore, regional collaborations and R&D investments are solidifying the plug-in hybrid vehicle battery market's significance in the ASEAN automotive arena.

- In a move to boost domestic PHEV battery production, the Thai government, in November 2023, introduced the "EV3.5" subsidy program. This initiative offers a subsidy of up to USD 2,760 per battery produced, valid from 2024 to 2027.

- The primary objective is two fold: to entice foreign investments and cement Thailand's stature as a pivotal player in the Southeast Asian plug-in hybrid vehicle battery manufacturing landscape. Given the current dominance of Chinese plug-in hybrid vehicle brands and the growing interest from European counterparts, this strategic move is poised to redefine Thailand's trajectory in the swiftly evolving plug-in hybrid vehicle battery sector.

- Battery technology advancements are crucially shaping the plug-in hybrid vehicle market in ASEAN. Innovations, especially in lithium-ion batteries, are boosting energy density, extending life cycles, and enabling faster charging, thereby enhancing the allure of plug-in hybrids.

- Given these dynamics, the passenger vehicle segment is poised for growth in the coming years.

Indonesia is Expected to Dominate the Market

- Driven by factors such as government policies, economic growth, consumer behavior, and technological advancements, the Indonesian segment of the ASEAN plug-in hybrid electric vehicle (PHEV) battery market is undergoing a notable transformation. As Southeast Asia's largest economy, Indonesia's burgeoning automotive market holds immense promise for the plug-in hybrid electric vehicle sector.

- Through policies and initiatives, the Indonesian government is actively working to reduce carbon emissions and champion sustainable transportation. These efforts, including tax incentives, subsidies, and crucially, the development of charging infrastructure, aim to alleviate the higher upfront costs typically associated with plug-in hybrid electric vehicles.

- The Indonesian Ministry of Industry has rolled out purchase subsidies for electric and hybrid vehicles, including electric motorbikes. Furthermore, there's a push to subsidize converting traditional combustion-engine motorbikes to electric. New battery-electric vehicle purchases can benefit from a generous subsidy of USD 5,130, while conventional hybrids enjoy a subsidy that's half that amount.

- Over the past decade, breakthroughs in battery technology and manufacturing have accelerated the adoption of lithium-ion batteries in Indonesia's hybrid electric vehicle landscape. These advancements have not only reduced costs but also enhanced performance and reliability, making lithium-ion batteries a favored choice for both manufacturers and consumers.

- Recently, lithium-ion battery and cell pack prices have been on a downward trajectory, appealing to end-user industries. After a minor uptick in 2022, prices resumed their decline in 2023, with lithium-ion battery packs hitting a historic low at USD 139/kWh, marking a 14% decrease.

- Moreover, the rise of local manufacturing facilities for plug-in hybrid electric vehicle batteries is poised to drive down production costs. This, in turn, is set to make plug-in hybrid electric vehicles more accessible to consumers. Coupled with government incentives and technological strides, this economic pivot towards affordable and sustainable transportation is primed to spur substantial growth in Indonesia's plug-in hybrid electric vehicle market.

- For example, in June 2023, Indonesia sealed a significant agreement with four prominent Chinese automakers - Hapco Neta, Wuling, Chery, and Xiaokang - positioning Indonesia as a potential electric vehicle export hub. In talks with Chery Automobile, there's a clear intent to explore research avenues for manufacturing plug-in hybrid electric vehicles (PHEVs) domestically. Given their enhanced fuel efficiency over traditional hybrids, plug-in hybrid electric vehicles are already popular in China. Chery has ambitious plans, targeting a rollout of 100,000 electric vehicles by 2030.

- Given these developments, Indonesia is poised to lead the market in the coming years.

ASEAN Countries Plug-in Hybrid Electric Vehicle Battery Industry Overview

The ASEAN Countries Plug-in Plug-in Hybrid Electric Vehicle Battery Market is semi-fragmented. Some of the key players in this market (in no particular order) are LG Energy Solution, Contemporary Amperex Technology Co Ltd., BYD Company, HDS Global Pte Ltd, and 3K Battery

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Electric Vehicle Sales

- 4.5.1.2 Decreasing Lithium-ion Battery Price

- 4.5.2 Restraints

- 4.5.2.1 High Battery Replacment Costs

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Battery Type

- 5.1.1 Lithium-ion Battery

- 5.1.2 Lead-Acid Battery

- 5.1.3 Sodium-ion Battery

- 5.1.4 Others

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 Singapore

- 5.3.2 Philippines

- 5.3.3 Vietnam

- 5.3.4 Thailand

- 5.3.5 Malaysia

- 5.3.6 Indonesia

- 5.3.7 Rest of ASEAN Countries

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 LG Energy Solution

- 6.3.2 Contemporary Amperex Technology Co Ltd.

- 6.3.3 BYD Company

- 6.3.4 Panasonic Holdings Corporation

- 6.3.5 Toshiba Corporation

- 6.3.6 Enersys Sarl

- 6.3.7 Exide Industries Ltd

- 6.3.8 HDS Global Pte Ltd

- 6.3.9 3K Battery

- 6.3.10 Clarios, LLC

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Continued Research and Development In New Battery Chemistries

02-2729-4219

+886-2-2729-4219

2026年全球插电式混合动力汽车电池市场报告

2026年全球插电式混合动力汽车电池市场报告 插电式混合动力汽车电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030)

插电式混合动力汽车电池:市场占有率分析、产业趋势/统计、成长预测(2025-2030) 2030年插电式混合动力汽车电池市场预测:按电池类型、车辆类型、充电类型、容量、应用和地区进行的全球分析

2030年插电式混合动力汽车电池市场预测:按电池类型、车辆类型、充电类型、容量、应用和地区进行的全球分析