|

市场调查报告书

商品编码

1637917

北美过程自动化:市场占有率分析、行业趋势和成长预测(2025-2030 年)North America Process Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

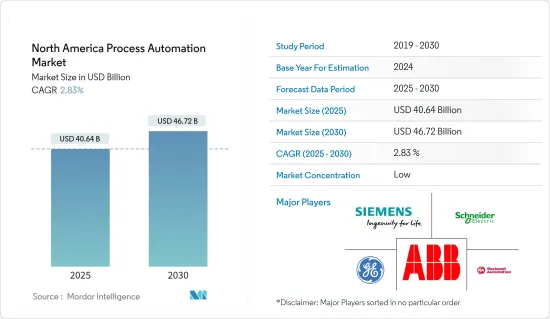

北美製程自动化市场规模预计在 2025 年为 406.4 亿美元,预计到 2030 年将达到 467.2 亿美元,预测期内(2025-2030 年)的复合年增长率为 2.83%。

流程自动化利用科技来简化复杂的业务流程。它通常包含三个关键功能:自动化流程、集中资讯和最大限度地减少人工干预的需要。其主要目标是消除瓶颈,最大限度地减少错误和资料遗失,提高透明度、部门间沟通和处理速度。技术进步和对生产力的日益关注正在推动过程自动化市场的发展。

主要亮点

- 流程自动化是一种透过消除人工干预来提高系统效率的技术。结果是错误更少、交货更快、品质更高、成本更低、整体业务流程更简单。这涉及利用软体工具、人员和程序来建立完全自动化的工作流程。透过采用流程挖掘来优化您的业务营运效率。这使您能够对数位解决方案获得宝贵的见解,并帮助您确定可以付出努力以获得最大收益的领域。预计该地区各行业将越来越多地采用自动化技术将推动市场的发展。

- 过程自动化市场的成长源于对提高生产力和减少危险的手动任务的日益关注。北美是一个成熟的市场,为引进最尖端科技、建立关键合作伙伴关係和发展电力和公共产业、石油和天然气、製药和化学品等领域的产品协同效应提供了绝佳的机会。这些因素在推动製程自动化市场扩张方面发挥关键作用。

- 製造业中数位和实体元素的融合已经改变了北美自动化产业。这些进步的主要目标是实现最佳效率。自动化製造流程有许多好处,包括无缝监控、减少废弃物和加快生产力。自动化提高了消费者的产品质量,并确保快速且经济地交付标准化、可靠的产品。工业物联网和工业 4.0 是重塑物流网路开发、生产和监控的尖端技术策略,并将推动市场成长。

- 市场成长的动力来自于寻求改善数位消费者体验、生产力和效率的组织越来越多地采用机器人流程自动化。人工智慧和机器学习与机器人流程自动化的结合有助于实现复杂任务的自动化,进一步推动了这种成长。製药、石油和天然气以及食品和饮料等行业在该地区采用机器人技术以增强其市场潜力方面表现突出。

- 例如,美国製药业蓬勃发展,是世界上最大的市场之一。自动化技术的进步现在使製药公司能够提高业务,包括填充、包装和测试过程。这些自动化系统高度准确,消除了称重、混合和包装药品等关键任务中人为错误的风险。因此,该地区製药业的投资正在激增,预计将创造大量的市场机会。

- 与製程自动化系统相关的大量费用与可靠、耐用的硬体和精简的软体有关。流程自动化的实施需要大量的资金投入来加强包括IT、机械等在内的整个基础设施。此外,还需要持续的维护,与手动系统相比,这可能会阻碍市场扩张。

北美流程自动化市场趋势

石油和天然气产业强劲成长

- 自动化对于推动石油和天然气产业的发展至关重要。自动化、数位化和先进技术的采用使操作员和技术人员能够快速获取关键性能、状况和技术资料。流程自动化涉及利用软体和技术来自动化业务流程和功能,并最终实现石油和天然气行业的特定组织目标。在研究的产业中,企业越来越依赖流程自动化来增强决策、故障排除和整体效能。

- 自动化对于推动石油和天然气产业的发展至关重要。数位化、自动化和先进技术的采用使操作员和技术人员能够即时存取关键性能、状况和技术资料。该地区的公司越来越依赖流程自动化来增强决策、故障排除和整体效能。

- 石油和天然气市场正在经历快速成长,自动化在该行业的扩张中发挥关键作用。特别是在美国,对增加石油和天然气供应的需求很高,部分原因是这些地区的人口成长。监控和资料采集 (SCADA) 是石油和天然气领域的一种常见自动化形式。 SCADA 系统从远端石油和天然气站点收集资讯和资料,从而无需监督和负责人亲自访问站点。由于该地区对石油和天然气的需求不断增长以及对石油和天然气行业的投资不断增加,预计市场将会成长。

- 例如,根据美国能源资讯署的数据,美国已连续六年维持全球第一大原油生产国地位。至2023年,原油和冷凝油油日均产量预计将达到1,290万桶,超过2019年的1,230万桶。美国丰富的石油和天然气资源降低了能源成本,鼓励了私部门的投资,从而推动了美国的经济成长。

- 此外,加拿大修订后的联邦气候变迁策略还包括一个值得注意的新目标,即减少温室气体排放。该计画的目标是到2030年减少32-40%的排放,在2050年实现完全排放。这些目标将在减轻气候变迁的最严重影响方面发挥关键作用。石油和天然气产业占加拿大温室气体排放的四分之一以上,是减排倡议的重点。预计这些重大倡议将刺激对自动化技术的需求,并促进该地区石油和天然气产业的节能实践。

- 透过提高自动化程度和营运分析能力来升级内部程序,该行业可以提高生产和分销效率,从而产量比率。该行业越来越重视安全性和可靠性。该行业复杂的供应链导致人们更加关注自动化、行业专业知识和更紧密的合作。流程自动化不仅仅是提高效率;它是一种适应全球市场不断变化的需求的策略决策。

美国经济强劲成长

- 预计该地区将占据大部分市场占有率。在工业4.0的推动下,美国正在加强其在工厂自动化和工业控制系统的全球地位。该领域采用智慧技术不仅可以提高业务效率,还可以增强国家经济。随着全球製造业的互联互通日益紧密,美国製造商面临越来越大的采用自动化的压力。他们努力实现成本效益和高品质标准。

- 针对美国智慧工厂的网路攻击增多,引发了人们对工业控制系统的担忧。各国政府正采取措施来应对这些风险。同时,采用国产工业控制系统作为减少智慧工厂网路安全漏洞的战略方针也日益成为趋势。Panasonic北美等公司透过提供包括 ERP 系统在内的广泛创新製造解决方案,处于领先地位。

- 作为拜登政府疫情后经济復苏战略的一部分,美国正在对基础设施和电子产业进行大量投资。这对中小企业来说是个好兆头,因为基础设施和电子产业是工业控制系统的主要消费者,并将直接受益。在机器人流程自动化(RPA)中,流程发现、最佳化、智慧和编配等术语越来越受欢迎。业务流程管理 (BPM) 与 RPA 之间深度整合的轨迹十分清晰。

- 《食品安全现代化法案》等严格的政府法规正在迫使美国食品和饮料公司实施自动化系统。这将加强美国自动化市场,简化运营,降低成本并提高产品品质。此外,该地区餐饮业产能的提高预计将进一步推动市场发展。根据美国农业部的数据,2023年,农业、食品和相关产业对美国国内生产总值(GDP)的贡献约为1.53兆美元,占5.6%。

- 此外,自动化在简化石油和天然气输送、开采和精製所涉及的各种流程方面发挥关键作用。目前,美国对石油和天然气领域的投资显着增加,这主要受到不断升级的地缘政治局势的推动。根据美国地质调查局预测,到2023年美国石油和天然气开采产业生产指数将达到140人。这较 2017 年的 100 指数和 2022 年的 130 指数有显着成长。预计这些重大进步将推动这一特定领域的成长。

北美製程自动化产业概况

由于生产这些系统所需设备高成本,退出障碍难以维持。儘管预测期内市场会出现整合,但预计市场竞争仍将加剧,因为许多市场参与者正在透过收购、策略性合併或新的智慧倡议来消除竞争对手。

2024 年 5 月-西门子宣布在工厂管理方面取得重大进展,以解决处理多个硬体控制点的复杂性。答案是西门子 Simatic 自动化工作站。这种创新的解决方案使製造商能够将硬体 PLC、传统 HMI 和边缘设备整合到基于软体的工作站中。这种整合将资讯技术 (IT) 实践无缝整合到操作技术(OT) 设置中。

2023 年 10 月-艾默生宣布支持其无边界自动化愿景的新技术,这是一个以软体为中心的工业自动化平台,连接来自现场、边缘和云端的资料。新技术的发布超越了传统的控制系统,提供了更先进的自动化平台,这些平台将资料情境化、民主化,为人们和塑造世界运作方式的人工智慧 (AI) 引擎提供服务。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 美国和加拿大主要工业自动化中心分析(根据过去三年的投资和扩张活动确定的中心)

- 主要宏观经济趋势对北美过程自动化产业的影响

- 根据疫情V型復苏、中期復苏、低迷復苏的短期和中期影响所确定的关键主题分析

- 根据美国流程自动化市场最终用户表现进行基础变数分析

- 加拿大流程自动化市场:基于最终用户绩效的变数分析

- 供应挑战的影响以及市场监管在振兴市场中的作用

第五章 市场动态

- 市场驱动因素

- 更加重视能源效率和降低成本

- 安全自动化系统的需求

- 工业物联网的出现

- 市场挑战

- 成本和实施挑战

第六章 行业标准及规范

第七章 市场区隔

- 按通讯协定

- 有线

- 无线的

- 依系统类型

- 按系统硬体

- 监控和资料采集系统 (SCADA)

- 分散式控制系统(DCS)

- 可程式逻辑控制器(PLC)

- 阀门和致动器

- 马达

- 人机介面 (HMI)

- 製程安全系统

- 感应器和变送器

- 依软体类型

- APC(独立和客製化解决方案)

- 严格监管

- 多元模型

- 推理和顺序

- 基于资料分析和彙报的软体

- 製造执行系统(MES)

- 其他软体和服务

- 按系统硬体

- 按最终用户产业

- 石油和天然气

- 化工和石化

- 电力和公共产业

- 用水和污水

- 饮食

- 纸和纸浆

- 药品

- 其他最终用户产业

- 按国家

- 美国

- 加拿大

第八章 竞争格局

- 公司简介

- ABB Limited

- Siemens AG

- Schneider Electric SE

- General Electric Co.

- Rockwell Automation Inc.

- Emerson Electric Co.

- Mitsubishi Electric

- Honeywell International Inc.

- Omron Corporation

- Fuji Electric

- Delta Electronics Limited

- Yokogawa Electric

第九章投资分析

第十章:未来市场展望

The North America Process Automation Market size is estimated at USD 40.64 billion in 2025, and is expected to reach USD 46.72 billion by 2030, at a CAGR of 2.83% during the forecast period (2025-2030).

Process automation leverages technology to streamline intricate business processes. It generally encompasses three essential functions: process automation, information centralization, and minimizing the need for human intervention. Its primary objective is to eliminate bottlenecks and and minimize errors and data loss while enhancing transparency, communication between departments, and processing speed. Growing technological advancements and a increasing focus on productivity fuel the market for process automation.

Key Highlights

- Process automation has become a a method that enhances a system's efficiency by eliminating human involvement. This results in reduced errors, an acceleration in delivery speed, an improvement in quality, a decrease in costs, and a simplification of the overall business process. It involves utilizing software tools, individuals, and procedures to establish a fully automated workflow. By employing process mining, it optimizes the effectiveness of business operations. This enables the acquisition of valuable insights into the user's digital solutions and facilitates the identification of areas where efforts can be applied for maximum advantage. The increasing adoption of automated technologies across the region's various sectors is expected to drive the market.

- The growth of the process automation market is driven by the rising emphasis on boosting productivity and reducing hazardous manual activities. North America, being a well-established market, presents an excellent opportunity for embracing cutting-edge technologies, establishing key alliances, and fostering product synergies in sectors like power and utilities, oil and gas, pharmaceuticals, and chemicals. These elements play a crucial role in propelling the expansion of the process automation market.

- Integrating digital and physical elements in manufacturing has transformed the North American automation industry. The primary goal of these advancements is to achieve optimal efficiency. Automating manufacturing processes has realized numerous advantages, including seamless monitoring, waste reduction, and accelerated production rates. Automation enhances product quality for consumers and ensures standardized, reliable goods are delivered quickly and affordably. The Industrial Internet of Things and Industry 4.0 represent cutting-edge technological strategies reshaping the development, production, and oversight of the logistics network, poised to propel market growth.

- The market's growth is growing due to the increasing adoption of robotic process automation by organizations aiming to improve digital consumer experience, productivity, and efficiency. This growth is further fueled by the integration of AI and machine learning in robotic process automation, facilitating the automation of intricate tasks. Industries such as pharmaceuticals, Oil and Gas, , and F&B are notably embracing robotic technology in the region to boost the market's potential.

- For instance, the pharmaceutical industry in the United States is thriving, making it one of the largest markets globally. Thanks to advancements in automation technology, pharmaceutical companies can now enhance the efficiency and precision of their operations, including filling, packaging, and inspection processes. These automated systems are highly accurate and eliminate the risk of human errors in crucial tasks like weighing, blending, and packaging pharmaceutical products. As a result, the region's pharmaceutical sector is witnessing a surge in investments, which is anticipated to create numerous market opportunities.

- The substantial expenses associated with process automation systems are linked to reliable and durable hardware and streamlined software. Implementing process automation necessitates significant financial investments to enhance the entire infrastructure, encompassing IT, machinery, and more. Additionally, it demands ongoing maintenance, which can impede market expansion compared to manual systems.

North America Process Automation Market Trends

Oil and Gas Industry to Witness Significant Growth

- Automation is essential for propelling the oil and gas sector forward. By adopting automation, digitization, and advanced technologies, operators and technicians can promptly access vital performance, condition, and technical data. Process automation involves utilizing software and technologies to automate business processes and functions, ultimately achieving specific organizational objectives within the oil and gas industry. In the examined area, companies increasingly rely on process automation to enhance decision-making, troubleshooting, and overall performance.

- Automation is crucial in propelling the oil and gas industry towards progress. By adopting digitization, automation, and advanced technologies, operators and technicians gain instant access to vital performance, condition, and technical data. Companies in the examined region increasingly rely on process automation to enhance decision-making, troubleshooting, and overall performance.

- The oil and gas market is experiencing rapid growth, and automation plays a significant role in this industry's expansion. The United States, in particular, is witnessing a high demand for increased oil and gas supply, partly due to population growth in these regions. Supervisory control and data acquisition (SCADA) is a prevalent form of automation in the oil and gas sector. SCADA systems gather information and data from remote oil and gas locations, eliminating supervisors and personnel needing to visit these sites physically. The market's growth is anticipated to rise owing to the growing need for oil and gas and rising investments in the region's oil and gas sector.

- For instance, according to the US EIA, the United States has maintained its position as the top producer of crude oil globally for the last six years. By 2023, the average daily production of crude oil and condensate will hit 12.9 million barrels, exceeding the previous record of 12.3 million barrels set in 2019, both domestically and worldwide. The ample oil and gas supply in the country has reduced energy expenses, fostering investments in the private sector and bolstering economic expansion in the United States.

- Moreover, the revised climate strategy of the Canadian federal government sets forth a notable new goal to diminish greenhouse gas emissions. The plan's objective is to reduce emissions by 32-40% by 2030, aiming to achieve complete emissions neutrality by 2050. These targets play a vital role in mitigating the most severe consequences of climate change. The oil & gas industry, which accounts for over a quarter of Canada's total GHG emissions, has become a focal point for reduction initiatives. Such substantial initiatives are anticipated to increase the demand for automation technology in the oil and gas sector of the region, thereby promoting energy-efficient practices.

- The sector can improve production and distribution effectiveness by upgrading its internal procedures with automation and enhanced operational analytics, leading to increased yields. The industry's focus on safety and dependability is growing stronger. With the industry's intricate supply chain, there is an increasing interest in automation, specialized industry expertise, and intense collaborations. Process automation goes beyond efficiency; it represents a strategic decision to adapt to the constantly changing global market demands.

United States to Witness Major Growth

- The region is expected to contribute a significant portion of the market share. Fueled by Industry 4.0, the United States is strengthening its position on a global scale in factory automation and industrial control systems. The incorporation of intelligent technologies in this field not only improves operational effectiveness but also reinforces the country's economy. With the increasing interconnectedness of global manufacturing, American manufacturers are facing growing pressure to adopt automation. They are aiming and working towards achieving a balance between cost-effectiveness and elevated quality benchmarks.

- With the increase in cyber-attacks targeting U.S. smart factories, worries about Industrial Control Systems are growing. The government is implementing measures to address these dangers. At the same time, there is a noticeable trend towards using domestically produced industrial control systems as a strategic approach to reduce cybersecurity vulnerabilities in intelligent factories. Companies such as Panasonic North America are leading the way by providing extensive innovative manufacturing solutions including ERP systems and beyond.

- Significant investment is being made in infrastructure and the electronics industry as part of the Biden administration's economic recovery strategy post-pandemic. This bodes well for small and medium-sized enterprises, as the infrastructure and electronics sectors are major consumers of industrial control systems and are poised to benefit directly. Terms like process discovery, optimization, intelligence, and orchestration are gaining prominence in Robotic Process Automation (RPA). A clear trajectory towards deeper integration between business process management (BPM) and RPA exists.

- Stringent government regulations, exemplified by the Food Safety Modernization Act, are compelling food and beverage firms in the U.S. to adopt automation systems. This enhances the nation's automation market and streamlines operations, reducing costs and elevating product quality. Moreover, the increasing region's F&B industry capabilities is further expected to drive the market. The USDA stated that in 2023, the agriculture, food, and related industries made a contribution of around USD 1.530 trillion to the U.S. gross domestic product (GDP), accounting for a 5.6% share.

- Moreover, automation plays an important role in streamlining the various processes involved in the transmission, extraction, and refining of oil and gas within the industry. The United States is currently experiencing a notable surge in investments within the oil and gas sector, largely due to the escalating geopolitical circumstances. As per the U.S. Geological Survey, the production index for the oil and gas extraction industry in the United States is projected to reach an estimated 140 by 2023. This represents a substantial increase compared to the index of 100 in 2017 and 130 in 2022. These significant advancements are anticipated to drive the growth of this particular segment.

North America Process Automation Industry Overview

The barriers to exit are non-supportive, considering the high-cost equipment needed for producing these systems. Many companies operating in the market eliminate the competition through acquisitions and strategic mergers or new smart initiatives, and hence, the market is expected to become more competitive despite consolidation during the forecast period.

May 2024 - Siemens unveiled a significant advancement in factory management, addressing the complexity of handling multiple hardware control points. The answer comes in the form of the Siemens Simatic Automation Workstation. This innovative solution enables manufacturers to consolidate a hardware PLC, a traditional HMI, and an edge device into a unified, software-based workstation. This integration seamlessly merges Information Technology (IT) practices into Operational Technology (OT) settings.

October 2023 - Emerson announced new technologies that support its Boundless Automation vision, a software-centric industrial automation platform that connects data from the field, the edge, and the cloud. The new technology releases will transcend a traditional control system, creating a more advanced automation platform that contextualizes and democratizes data for both people and the artificial intelligence (AI) engines that shape the way the world operates.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Analysis of the Major Industrial Automation Hubs in the United States and Canada (Hubs Identified Based on the Investor Activity and Expansion Activities Undertaken over the Last Three Years)

- 4.5 Impact of Key Macroeconomic Trends on the Process Automation Industry in North America

- 4.6 Analysis of the Key Themes Identified Based on the Short- and Medium-term Effects of the Pandemic V-shaped Recovery, Mid-range Recovery, and Slump Recovery

- 4.7 US Process Automation Market Base Variable Analysis Based on End-user Performance

- 4.8 Canada Process Automation Market Base Variable Analysis Based on End-user Performance

- 4.9 Impact of Supply-related Challenges and the Role of Market Regulations in Spurring Activity

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Energy Efficiency and Cost Reduction

- 5.1.2 Demand for Safety Automation Systems

- 5.1.3 Emergence of IIoT

- 5.2 Market Challenges

- 5.2.1 Cost and Implementation Challenges

6 INDUSTRY STANDARDS AND REGULATIONS

7 MARKET SEGMENTATION

- 7.1 By Communication Protocol

- 7.1.1 Wired

- 7.1.2 Wireless

- 7.2 By System Type

- 7.2.1 By System Hardware

- 7.2.1.1 Supervisory Control and Data Acquisition System (SCADA)

- 7.2.1.2 Distributed Control System (DCS)

- 7.2.1.3 Programmable Logic Controller (PLC)

- 7.2.1.4 Valves and Actuators

- 7.2.1.5 Electric Motors

- 7.2.1.6 Human Machine Interface (HMI)

- 7.2.1.7 Process Safety Systems

- 7.2.1.8 Sensors and Transmitters

- 7.2.2 By Software Type

- 7.2.2.1 APC (Standalone and Customized Solutions)

- 7.2.2.1.1 Advanced Regulatory Control

- 7.2.2.1.2 Multivariable Model

- 7.2.2.1.3 Inferential and Sequential

- 7.2.2.2 Data Analytics and Reporting-based Software

- 7.2.2.3 Manufacturing Execution Systems (MES)

- 7.2.2.4 Other Software and Services

- 7.2.1 By System Hardware

- 7.3 By End-user Industry

- 7.3.1 Oil and Gas

- 7.3.2 Chemical and Petrochemical

- 7.3.3 Power and Utilities

- 7.3.4 Water and Wastewater

- 7.3.5 Food and Beverage

- 7.3.6 Paper and Pulp

- 7.3.7 Pharmaceutical

- 7.3.8 Other End-user Industries

- 7.4 By Country

- 7.4.1 United States

- 7.4.2 Canada

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 ABB Limited

- 8.1.2 Siemens AG

- 8.1.3 Schneider Electric SE

- 8.1.4 General Electric Co.

- 8.1.5 Rockwell Automation Inc.

- 8.1.6 Emerson Electric Co.

- 8.1.7 Mitsubishi Electric

- 8.1.8 Honeywell International Inc.

- 8.1.9 Omron Corporation

- 8.1.10 Fuji Electric

- 8.1.11 Delta Electronics Limited

- 8.1.12 Yokogawa Electric

9 INVESTMENT ANALYSIS

10 FUTURE OUTLOOK OF THE MARKET

全球过程自动化市场分析与预测(至2031年)

全球过程自动化市场分析与预测(至2031年) 流程自动化市场预测至2032年:按产品、通讯协定、部署类型、最终用户和地区分類的全球分析

流程自动化市场预测至2032年:按产品、通讯协定、部署类型、最终用户和地区分類的全球分析 按组织规模、组件、部署模式、流程类型和行业垂直领域分類的数位化流程自动化市场 - 全球预测 2025-2032流程自动化和测量设备市场(按产品、部署模式和最终用户划分)—2025-2032 年全球预测认知流程自动化市场按组件、部署类型、组织规模、应用和最终用户行业划分 - 全球预测 2025-2032

按组织规模、组件、部署模式、流程类型和行业垂直领域分類的数位化流程自动化市场 - 全球预测 2025-2032流程自动化和测量设备市场(按产品、部署模式和最终用户划分)—2025-2032 年全球预测认知流程自动化市场按组件、部署类型、组织规模、应用和最终用户行业划分 - 全球预测 2025-2032 2025年全球数位化流程自动化市场报告2025年全球流程自动化与仪器市场报告2025年全球製程自动化工业控制市场报告2025年全球认知过程自动化市场报告2025年全球零接触配置市场报告

2025年全球数位化流程自动化市场报告2025年全球流程自动化与仪器市场报告2025年全球製程自动化工业控制市场报告2025年全球认知过程自动化市场报告2025年全球零接触配置市场报告