|

市场调查报告书

商品编码

1639428

北美下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)North America Next Generation Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

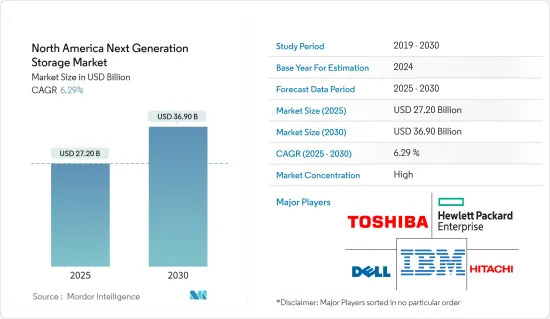

北美下一代储存市场规模预计在2025年为272亿美元,预计到2030年将达到369亿美元,预测期内(2025-2030年)的复合年增长率为6.29%。

主要亮点

- 由于全球供应商和消费者在美国高度集中,下一代储存市场在美国显示出成长迹象。

- 全球范围内云端运算公司和社交网路供应商使用的超大规模资料中心的数量正在增长。北维吉尼亚的资料中心库存量位居美国第一,约 2,060 兆瓦。

- 该地区占据智慧零售市场的很大份额,产生大量资料,从而增加了对储存解决方案的需求。根据美国人口普查局统计,2022年1月至3月美国零售电商销售额约2,500亿美元,较上季成长2.4%。

- 根据Internet World统计,美国地区网路用户约有3.48亿。这是世界上最高的采用率之一。网路使用者的增加与资料产生的增加直接相关,进而影响下一代储存市场。智慧型手机普及率亦最高,达93.4%。爱立信表示,该地区还拥有最高的5G网路覆盖率,5G用户渗透率为41%。

北美下一代储存市场趋势

智慧型手机、连网型设备和电子设备的兴起将推动市场的发展。

- 许多设备,包括智慧型手机、笔记型电脑和平板电脑,都会以影片和影像的形式产生资料。低成本智慧型手机和平板电脑的普及正在推动下一代储存设备的采用。美国消费者越来越多地透过智慧型手机和其他行动装置与数位资讯世界建立联繫。越来越多的人将智慧型手机作为家中主要的上网设备。

- 在美国,消费者对 5G 智慧型手机的需求持续成长,许多人渴望升级行动电话以利用这项新技术。据消费技术协会称,美国智慧型手机销售正在蓬勃发展。 2021年智慧型手机销售额将达730亿美元,2022年将增加至747亿美元。

- 根据国际电信联盟和美国联邦通讯委员会的报告,美国拥有全天宽频网路存取的家庭数量持续增长,预计到2020年将达到1.2亿户,使美国成为全球最大的线上市场。 。

- 行动资料使用量的快速成长产生了大量的资料流量,进一步增加了对强大的下一代储存解决方案的需求。预计到 2028 年,北美的用户平均数据消费量将最高,达到 58 GB。

云端储存占据主要市场占有率

- 近年来,云端平台正在实现新的复杂的经营模式,并协调更多全球一体化的网路。在云端上部署储存解决方案可以降低整体拥有成本并提高便利性,因为服务供应商负责提供最长的执行时间、资料安全性和定期更新。

- 当前的市场趋势,例如计量收费和 SaaS 模式,服务供应商负责维护资料和应用程式讯息,进一步推动了这些解决方案的采用。

- 此外,由于它减少了内部建设必要基础设施所需的资本支出,因此越来越多中小型企业开始采用它。这一持续的趋势为市场成长提供了巨大的推动力。

- 云端还可以作为 IT 转型的催化剂,让您可以灵活地将您首选的云端与现有的内部部署基础架构按照最适合您工作负载的比例相结合。

- 此外,对成本优化和业务敏捷性的日益关注也导致了云端资料中心的扩张。云端服务还能轻鬆适应不断变化的条件以满足新的需求。这使得客户能够专注于他们的核心竞争力,最终实现整体成长。

- 随着先进技术的出现,企业越来越重视更新其储存系统以跟上竞争的步伐。混合云就是这样一种趋势,它正在推动市场大幅成长。然而,安全性和资料传输所需的网路频宽不足对市场成长构成了挑战。

北美下一代储存产业概况

北美新一代储存市场主要集中于科技巨头,它们拥有最尖端科技和经验。为了保持竞争力,公司经常推出具有创新和进步的新产品。为了保持竞争力,市场参与企业采用各种方法,包括收购、合作、投资、合併以及技术开发和采用。

2022 年 11 月,全球网路、储存连接和基础设施解决方案供应商 ATTO Technology, Inc. 宣布与内部资料储存公司 AC&NC 合作,为电影和影像服务供应商5600°K productions 开发新的资料中心。宣布将提供预先建置的高效能储存解决方案。该解决方案包括一个 JetStor 816FX 光纤通道储存区域网路平台,该平台配备 16 个 12 TB SAS 硬碟和该公司的 Celerity 16 Gb/s 光纤通道主机汇流排适配器。

2022 年 6 月,以资料为中心的安全供应商 StorCentric 宣布其网路附加储存 (NAS) Nexsan EZ-NAS 正式上市 (GA)。专为中小型企业 (SMB) 和企业边缘部署而设计。该平台提供先进的企业级功能,例如 AD 支援、线上压缩和静态资料加密。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- COVID-19 的影响

第五章 市场动态

- 市场驱动因素

- 数位资料量不断增加

- 固态设备的应用日益广泛

- 智慧型手机、笔记型电脑和平板电脑日益普及

- 市场限制

- 云端和基于伺服器的服务缺乏资料安全性

第六章 市场细分

- 按储存系统

- 直接附加储存 (DAS)

- 网路附加储存 (NAS)

- 储存区域网路 (SAN)

- 依储存架构

- 基于檔案物件的储存 (FOBS)

- 区块储存

- 按最终用户产业

- BFSI

- 零售

- 资讯科技和电讯

- 卫生保健

- 媒体与娱乐

第七章 竞争格局

- 公司简介

- Dell Inc.

- Hewlett Packard Enterprise Company

- NetApp Inc.

- Hitachi Ltd.

- IBM Corporation

- Toshiba Corp.

- Pure Storage Inc.

- DataDirect Networks.

- Scality Inc.

- Fujitsu Ltd.

- Netgear Inc.

第八章投资分析

第九章:市场的未来

The North America Next Generation Storage Market size is estimated at USD 27.20 billion in 2025, and is expected to reach USD 36.90 billion by 2030, at a CAGR of 6.29% during the forecast period (2025-2030).

Key Highlights

- The next-generation storage market is showing signs of growth in the United States, owing to the regional concentration of global vendors and consumers in the country.

- The number of hyperscale data centers that cloud companies and social network providers use has increased globally. North Virginia recorded around 2060 megawatts of inventory of data centers in the United States.

- The region holds a significant smart retail market share, which generates a huge amount of data, in turn creating the demand for storage solutions. According to the U.S. Census Bureau, from January to March 2022, U.S. retail e-commerce sales amounted to approximately USD 250 billion, marking a 2.4% increase compared to the last quarter.

- The United States region has approximately 348 million Internet users, according to Internet World stats. This is one of the highest penetration rates in the world. The growth in Internet users is directly connected to growth in data generation and, in turn, influencing the next-generation storage market. The country also possesses the highest smartphone penetration, which is around 93.4%. The region also has the widest coverage of the 5G network, with a 5G subscription penetration of 41%, according to Ericsson.

North America Next Generation Storage Market Trends

Increasing Proliferation of Smartphones, connected devices and electronic devices will drive the market.

- Many devices, such as smartphones, laptops, and tablets, are generating data in the form of videos and images. The proliferation of low-cost smartphones and tablets provides increased potential for adopting next-generation storage devices. American consumers are increasingly connected to the world of digital information via smartphones and other mobile devices. A growing number of people are using smartphones as their primary online access at home.

- Consumer demand for 5G smartphones will continue to rise in the United States, with many people eager to upgrade their phones to take advantage of the new technology's benefits. According to the Consumer Technology Association, the United States is witnessing a surge in smartphone sales. In 2021, smartphone sales were USD 73 billion, which increased to USD 74.7 billion in 2022.

- According to ITU and Federal Communications Commission reports, the number of households in the United States with permanent internet access via broadband continues to climb, with the number of households with permanent internet access via broadband expected to reach 120 million by 2020, making the United States one of the largest online markets in the world.

- The surge in mobile data usage is generating a large volume of data traffic, which further needs a robust next-generation storage solution. North America is expected to have the greatest average consumption per subscriber in 2028, with 58 gigabytes per user.

Cloud Storage to Gain Significant Market Share

- Cloud platforms enabled new, complex business models and have been orchestrating more global-based integration networks in recent years. The deployment of storage solutions over the cloud offers greater convenience, as the service vendor is solely responsible for providing maximum uptime, data security, and periodic updates, thus decreasing the total cost of ownership.

- The current market trends, including the delivery of these solutions on the pay-as-you-go model and SaaS models, wherein the service vendors also assume the responsibility of maintaining data and application information, are further driving the adoption of these solutions.

- Moreover, this mode has recorded an increase in deployment in small-/medium-scale businesses, as it cuts down the capital expenditure involved in building the required infrastructure on their premises. This continuing trend is significantly driving the growth of the market.

- In addition, the cloud acts as a catalyst for IT transformation, providing the flexibility to combine the preferred clouds and existing on-premises infrastructure in the ratio best suited for the workload.

- Furthermore, the rising focus on cost optimization and business agility has led to the expansion of cloud data centers. Also, cloud services adapt easily to the changing landscape to meet new requirements. This allows the client organization to focus on its core competency, which, in turn, results in its overall growth.

- The foray of advanced technologies prompts companies to emphasize updating their storage system to match with the competition. The hybrid cloud is one such trend that provides a significant boost to market growth. However, security and the lack of network bandwidth for data transfer can challenge the market's growth.

North America Next Generation Storage Industry Overview

The North America next-generation storage market is essentially concentrated, with technology behemoths wielding dominance through cutting-edge technology and experience. Companies frequently introduce new products with innovations and advances to stay competitive. Major market participants use a range of techniques to stay competitive, including acquisitions, partnerships, investments, mergers, and technology developments and introductions.

In November 2022, ATTO Technology, Inc., a global network, storage connectivity, and infrastructure solutions provider, announced its collaboration with AC&NC, on-premise data storage, to offer a developed, high-performance storage solution to 5600 °K productions, a film and video services provider. The solution includes a JetStor 816FX Fibre Channel Storage Area Network platform along with 16 12 TB SAS drives and the company's Celerity 16 Gb/s Fibre Channel Host Bus Adapters.

In June 2022, StorCentric, a data-centric security provider, announced the general availability (GA) launch of Nexsan EZ-NAS, network attached storage (NAS). It is designed for small and medium-sized businesses (SMBs) and large enterprises' edge deployments. The platform offers advanced enterprise-class features such as AD support, in-line compression, and data-at-rest encryption.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Volume of Digital Data

- 5.1.2 Rising Adoption of Solid-state Devices

- 5.1.3 Increasing Proliferation of Smartphones, Laptops, and Tablets

- 5.2 Market Restraints

- 5.2.1 Lack of Data Security in Cloud- and Server-based Services

6 MARKET SEGMENTATION

- 6.1 Storage System

- 6.1.1 Direct Attached Storage (DAS)

- 6.1.2 Network Attached Storage (NAS)

- 6.1.3 Storage Area Network (SAN)

- 6.2 Storage Architecture

- 6.2.1 File and Object-based Storage (FOBS)

- 6.2.2 Block Storage

- 6.3 End-User Industry

- 6.3.1 BFSI

- 6.3.2 Retail

- 6.3.3 IT and Telecom

- 6.3.4 Healthcare

- 6.3.5 Media and Entertainment

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Dell Inc.

- 7.1.2 Hewlett Packard Enterprise Company

- 7.1.3 NetApp Inc.

- 7.1.4 Hitachi Ltd.

- 7.1.5 IBM Corporation

- 7.1.6 Toshiba Corp.

- 7.1.7 Pure Storage Inc.

- 7.1.8 DataDirect Networks.

- 7.1.9 Scality Inc.

- 7.1.10 Fujitsu Ltd.

- 7.1.11 Netgear Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2026年全球天基资料记录市场报告2026年全球下一代资料储存市场报告

2026年全球天基资料记录市场报告2026年全球下一代资料储存市场报告 全像资料储存市场机会、成长要素、产业趋势分析及2026-2035年预测

全像资料储存市场机会、成长要素、产业趋势分析及2026-2035年预测 新一代资料储存市场:依储存类型(DAS、NAS、SAN)、储存媒体、架构、最终用户(银行、金融服务和保险(BFSI)、零售、医疗保健、製造业、政府、IT 和电信、其他最终用户)和地区划分 - 至2027年的全球预测

新一代资料储存市场:依储存类型(DAS、NAS、SAN)、储存媒体、架构、最终用户(银行、金融服务和保险(BFSI)、零售、医疗保健、製造业、政府、IT 和电信、其他最终用户)和地区划分 - 至2027年的全球预测 新一代资料储存技术市场-全球产业规模、份额、趋势、机会与预测:按类型、解决方案、记忆体、地区和竞争格局划分,2021-2031年

新一代资料储存技术市场-全球产业规模、份额、趋势、机会与预测:按类型、解决方案、记忆体、地区和竞争格局划分,2021-2031年 下一代资料储存市场规模、份额和成长分析(按储存系统、储存媒体和地区划分)—产业预测(2026-2033 年)

下一代资料储存市场规模、份额和成长分析(按储存系统、储存媒体和地区划分)—产业预测(2026-2033 年) 下一代资料储存市场:2025 年至 2030 年的未来预测

下一代资料储存市场:2025 年至 2030 年的未来预测 2025-2029年全球AI优化储存市场

2025-2029年全球AI优化储存市场 下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)亚太地区下一代储存:市场占有率分析、产业趋势和成长预测(2025-2030 年)

下一代储存:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)亚太地区下一代储存:市场占有率分析、产业趋势和成长预测(2025-2030 年)