|

市场调查报告书

商品编码

1639514

拉丁美洲的无菌包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)Latin America Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

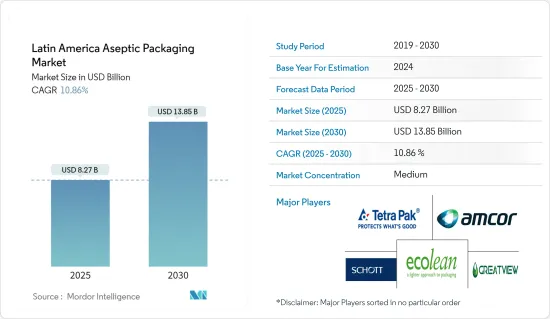

拉丁美洲无菌包装市场规模预计到2025年为82.7亿美元,预计2030年将达到138.5亿美元,预测期内(2025-2030年)复合年增长率为10.86%。

主要亮点

- 拉丁美洲为市场研究提供了极好的可能性,因为它是一个生产许多原材料和食品的地区。巴西、阿根廷、哥伦比亚和墨西哥等国的快速工业化正在推动经济成长。与其他大陆一样,新的、更环保的技术的使用正在为整个食物链的反应和解决方案铺平道路,以适应负责任和有意识消费的不断增长的趋势。这些发展在加工和保存阶段最为明显,确保了食品的品质和安全并延长了保质期。无菌包装作为更安全、更盈利的食品包装选择越来越受欢迎

- 儘管存在与这种形式相关的潜在技术和成本问题,但消费者对更健康食品替代品的偏好导致了对无菌包装的投资激增。由于消费者偏好更健康的替代品,无菌包装越来越受欢迎,製造商正在投资包装和填充技术来满足这一需求。在巴西,消费者对功能性和健康选择的偏好正在推动产品开发。乳製品製造商正在转向无菌灌装机,以满足对乳製品不断增长的需求。

- 因此,巴西乳製品公司 Shefa 和 Lider Alimentos 选择 SIG 作为供应和安装无菌灌装机和包装解决方案的首选合作伙伴。 SIG 在巴西提供先进的无菌填充技术。我们位于圣保罗和巴拉那的生产基地已安装了九台无菌填充机,并已投入运作。

- 波尔公司宣布在南美洲扩张,在秘鲁奇尔卡开设新製造工厂。扩建后,该工厂将具备年产超过10亿个饮料罐的能力。随着消费者不断要求清爽、新口味和优质包装,优质化已成为酒类产业公司的关键驱动力。工业公司将投资重点放在建立多元化的全球和专业优质品牌组合。

- 此外,墨西哥对软性饮料和其他非酒精饮料的需求正在增长,预计在预测期内对无菌包装的需求将会增加。例如,根据国家统计和地理研究所 (INEGI) 的数据,2023 年 4 月墨西哥风味软性饮料产值增至 2,811,060,000 墨西哥比索(167,510,000 美元),而 2023 年 2 月为 2,811,060,000 美元。 4.7471 亿(2.0705 亿美元)。

- 然而,无菌纸盒含有铝和聚乙烯成分,因此很难从包装中去除这种材料。为了实现精确的回收(材料被回收到生产週期的前几个阶段而不损失品质),利乐的所有层都被分离,并且为了生产更多的利乐必须被重复使用。而且,此类机器仅适用于某些参与企业。回收需要大量的设备和投入,例如水和能源,而许多回收中心不具备这些。这些因素可能会阻碍市场成长。

拉丁美洲无菌包装市场趋势

无菌纸盒证实受调查市场的需求不断增加

- 无菌纸盒是一种采用多层包装製成的食品容器,特别适用于橙汁或汤等液体。这些容器由纸、塑胶和金属层製成。如果将材料加工成干净的水流,则可以回收。无菌纸盒由约 70% 的纸张(用于硬度和强度)、约 24% 的聚乙烯(用于 4 层密封包装)和约 6% 的铝箔(用作空气和光线的屏障)製成的。此盒子无需冷藏即可安全保存液体一年以上。

- 因此,食品和饮料供应商由于其成本和环境效益而倾向于无菌包装,特别是在常温运输和储存方面。此外,无菌包装支持使用可回收且环保的小袋进行包装,这通常针对喜欢少量且购买频率较高的消费者,因此这些产品的需求量很大。

- 这种成长主要是由方便的即食产品的日益普及和改进的储存技术所推动的。此外,对有机和健康食品不断增长的需求也导致巴西无菌包装的使用增加。利乐、Amcor 和 SIG 康美包等主要无菌包装製造商已在巴西进行了大量投资,并且预计将继续这样做。

- 生活方式的改变以及消费者对加工、包装和已调理食品和饮料的依赖正在推动对无菌包装解决方案的需求。超级市场文化的出现也改变了购物格局,增加了对包装的需求,特别是在食品和饮料领域。人们生活方式的变化导致人们转向即食产品。此外,这些产品均采用无菌包装,以确保产品不会被污染、不被窜改且可安全食用。

- 无菌牛奶盒在非常高的温度下进行处理,以消除牛奶中存在的任何有害细菌。然后,牛奶立即在无菌环境中以特殊包装装入纸箱,以防止空气进入。这个过程显着延长了牛奶的保质期。无菌牛奶纸盒在全球范围内的需求量很大,因为它们可以保护产品免受光和环境氧气的影响。

- 据美国农业部称,墨西哥乳製品产业到 2023 年将生产 1,342 万公升牛奶,高于 2018 年的约 1,254 万吨。预计这种产量成长将支持预测期内的市场成长。

巴西预计将占很大份额

- 巴西食品工业是无菌包装的主要消费者之一,可延长食品的保存期限并减少污染。包装也用于製药和医疗领域,以最大限度地减少腐败,提高产品安全性,并在与灭菌和其他包装技术结合使用时确保产品安全。

- 市场先驱正在投资研发,以保持在新兴市场产业的领先地位。新产品推出的趋势支撑了市场需求。特别是製药业对无菌包装的需求也不断增加。各国政府正在加强对医疗领域的监管,以促进无菌包装市场的成长。

- 巴西卫生署负责监管无菌包装并确保遵守该国的良好生产规范 (GMP) 法规。此外,巴西政府于 2019 年成立了工作小组,讨论和製定在巴西使用无菌包装的策略。

- 预计未来几年该国无菌包装市场将呈指数级增长。成长包括早餐用麦片谷类家常小菜、早餐麦片、婴儿食品、酱汁、调味料、调味品、加工肉品、水产品、汤等。据有机贸易协会称,巴西有机包装食品和饮料的消费量预计将从 2020 年的 7,400 万美元增加到 2025 年的 1.05 亿美元。

- 随着新技术和创新使製造商能够创造更有效率、更永续的无菌包装解决方案,该市场预计在未来几年将成长。该地区酒精饮料的消费量正在增加,我们预计葡萄酒、罐装啤酒和瓶装烈酒将更多地使用盒中袋包装。例如,根据北欧银行发表的报导,巴西的酒精饮料消费量预计将从 2021 年的 110.9 亿升增至 2024 年的 122.9 亿公升。

拉丁美洲无菌包装产业概况

拉丁美洲无菌包装市场是半静态的,只有少数供应商在国内和国际市场上运作。市场似乎已适度整合,参与企业采取产品创新、併购和收购等各种策略来扩大影响力并保持竞争力。该市场的主要参与企业包括 Bemis Company Incorporation、DS Smith PLC、SIG Combibloc Group AG 和 Tetra Pak International。

- 2023年3月,总部位于智利的食品科技独角兽NotCo与SIG合作,让NotCo在SIG的纸盒包装中推出NotCreme,这是一种动物性食品的植物来源替代品。此次合作将进一步加强 Notco 在植物来源食品方面的专业知识和适应性。原味奶、零糖奶、半糖奶和巧克力奶产品也将采用 SIG 的无菌纸盒包装推出。

其他好处

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 买方议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场动态

- 市场驱动因素

- 食品和饮料业对无菌包装的需求不断增长

- 市场问题

- 包装材料回收困难

第六章 市场细分

- 副产品

- 纸盒

- 包包/袋

- 能

- 瓶子

- 按用途

- 饮料

- 准备喝

- 乳类饮料

- 食物

- 加工食品

- 水果和蔬菜

- 乳製品

- 药品

- 饮料

- 按国家/地区

- 巴西

- 阿根廷

- 墨西哥

第七章 竞争格局

- 公司简介

- Amcor PLC

- Bemis Company Inc.

- DS Smith PLC

- Elopak AS

- Mondi PLC

- Reynold Group Holdings PLC

- Sonoco Products Company

- Smurfit Kappa Group PLC

- SIG Combibloc Group AG

- Stora Enso Oyj

第八章投资分析

第9章市场的未来

The Latin America Aseptic Packaging Market size is estimated at USD 8.27 billion in 2025, and is expected to reach USD 13.85 billion by 2030, at a CAGR of 10.86% during the forecast period (2025-2030).

Key Highlights

- Latin America offers excellent potential in the market studied as a region that produces a lot of raw resources and food products. Rapid industrialization in countries like Brazil, Argentina, Columbia, and Mexico is driving economic growth. As in other continents, the use of new, more environmentally friendly technology is paving the way for the provision of reactions and solutions along the whole food chain to the trend of rising responsible and conscious consumption. These developments are most apparent throughout the processing and preservation stages when they assure quality and safety and extend the food's shelf life. Aseptic packaging is becoming increasingly popular as a safer and more profitable food packaging option.

- Consumers' preference for healthier alternatives is leading to a surge in investment in aseptic packaging despite the potential technical and cost issues associated with the formats. As aseptic designs become increasingly popular due to consumer preference for healthier alternatives, manufacturers are investing in packaging and fill technologies to meet this demand. In Brazil, product development is being driven by consumer preference for functional and healthier options. Dairy companies are focusing on installing aseptic fill machines to cater to the increasing demand for dairy-based products.

- In line with this, Shefa and Lider Alimentos, two Brazilian dairy companies, selected SIG as their preferred partner for supplying and installing aseptic fillers and packaging solutions. SIG is the provider of advanced aseptic fill technology in Brazil. It installed nine aseptic fill machines at production sites in Sao Paulo and Parana, where the systems have already started operating.

- Ball Corporation announced it was expanding its operations in South America, landing in Peru with a new manufacturing plant in Chilca. After expansion, the plant will have a production capacity of over 1 billion beverage cans annually. Premiumization has been a critical growth driver for players in the alcohol space due to consumers' continued desire for refreshing and newer tastes and premium packaging. The companies in the industry have been focused on investing in crafting a diverse portfolio of global and specialty premium brands.

- Additionally, the growing demand for soft drinks and other non-alcoholic beverages in Mexico is expected to support the need for aseptic packaging in the forecast timeframe. For instance, according to the National Institute of Statistics and Geography (INEGI), the production value of flavored soft drinks in Mexico amounted to over MXN 3474.71 million (USD 207.05 million) in April 2023, compared to MXN 2811.06 million (USD 167.51 million) in February 2023.

- However, it is difficult to remove this material from packaging due to the presence of aluminum and polyethylene components in aseptic cartooning. To achieve accurate recycling (where materials are recycled to a previous stage of the production cycle without loss of quality), all the layers of Tetra Pak would need to be separated and reused to produce more Tetra Pak. Additionally, the availability of such machines is limited to certain players. Recycling requires a lot of equipment and inputs, such as water and energy, and many recycling centers do not have these. Such factors might hinder market growth.

Latin America Aseptic Packaging Market Trends

Aseptic Cartons to Witness Increased Demand in the Market Studied

- Aseptic cartons are food containers built from multi-layer packing, particularly for liquids like orange juice and soups. These containers are made of layers of paper, plastic, and metal. Once processed into a clean stream, the material is recyclable. Aseptic cartons are made up of approximately 70% paper (for stiffness and strength), roughly 24% polyethylene (used in four layers to seal the package hermetically), and nearly 6% aluminum foil (used as a barrier against air and light). The boxes keep liquids safe for a year or longer without refrigeration.

- As a result, food and beverage vendors are inclining toward aseptic packaging, considering cost and environmental benefits, especially in terms of ambient shipping and storage. Also, as aseptic packaging supports packaging through recyclable and eco-friendly pouches, which often target consumers who prefer small quantities and make purchases more frequently, the demand for such products is considerably high.

- This growth has been primarily driven by the increasing popularity of convenience and ready-to-eat products and the improvement in preservation technologies. In addition, the rising demand for organic and healthy foods has also led to the increased use of aseptic packaging in Brazil. Major aseptic packaging manufacturers, such as Tetra Pak, Amcor, and SIG Combibloc, have invested heavily in Brazil and are expected to continue in the coming years.

- Changing lifestyles and the consequent dependence of consumers on processed, packaged, and pre-cooked food and beverages are increasing the demand for aseptic packaging solutions. The advent of the supermarket culture has also altered the shopping landscape and has increased the need for packaging, especially in food and beverage products. The altering lifestyle of people has resulted in the shift to ready-to-eat products. In addition, these products are packed in aseptic packaging to ensure that the products remain uncontaminated, tamper-proof, and safe for consumption.

- Aseptic cartons for milk are processed at extremely high temperatures, which destroy any harmful bacteria in the milk. The milk is then instantly cartooned in a sterile environment into specialized packaging that prevents air from penetrating. The shelf-life of the milk becomes much longer after this operation. The demand for aseptic cartons for milk is increasing globally, as they protect the product from light and ambient oxygen, resulting in increased shelf life.

- According to the US Department of Agriculture, the Mexican dairy industry produced 13.42 million liters of milk in 2023, up from around 12.54 million metric tons in 2018. Such production growth is expected to support the market growth during the forecast period.

Brazil is Expected to Hold a Significant Share

- The Brazilian food industry is one of the primary consumers of aseptic packing, which extends the shelf life of food products and reduces contamination. Packaging is also employed in the pharmaceutical and medical sectors to minimize spoilage, improve product safety, and ensure product safety when used with sterilization or other packaging technologies.

- Market players invest in research and development to stay ahead of developing industries. Market trends in new product launches support market demand. Notably, the pharmaceutical industry's demand for aseptic packaging is also increasing. Governments across the country are increasing regulations on the healthcare sector to boost the growth of the aseptic packaging market.

- The Ministry of Health in Brazil regulates aseptic packing and ensures that it complies with the country's Good Manufacturing Practices regulations. Additionally, the Brazilian government established a Working Group in 2019 to discuss and develop strategies for using aseptic packing in Brazil.

- The aseptic packaging market is expected to expand in the country exponentially over the next couple of years. The growth rates included ready meals, breakfast cereals, baby food, sauces, dressings and condiments, processed meat, seafood, and soup. According to the Organic Trade Association, the consumption of organic packaged food and beverages in Brazil is expected to increase from USD 74 million in 2020 to USD 105 million in 2025.

- The market is expected to grow in the coming years as new technologies and innovations enable manufacturers to create more efficient and sustainable aseptic packaging solutions. Increasing consumption of alcoholic beverages in the region will boost the use of the bag in the box for wine packaging, cans for beers, and bottles for spirits. For instance, according to an article published by Banco do Nordeste, the consumption of alcoholic beverages in Brazil is expected to reach 12.29 billion liters by 2024 from 11.09 billion liters in 2021.

Latin America Aseptic Packaging Industry Overview

The Latin American aseptic packaging market is semi-consolidated, as a few vendors operate in the domestic and international markets. The market appears to be moderately consolidated, with the players adopting various strategies, such as product innovation, mergers, and acquisitions, to expand their reach and stay competitive. Some of the major players in the market are Bemis Company Incorporation, DS Smith PLC, SIG Combibloc Group AG, and Tetra Pak International.

- In March 2023, Chile-based NotCo, a food-tech unicorn, partnered with SIG, enabling NotCo to launch NotCreme, a plant-based alternative to animal-derived food products, in SIG's carton packaging. This partnership further strengthens NotCo's expertise and adaptability in plant-based foods. NotMilk Originals, zero-sugar, semi-sugar, and chocolate milk products will also be available in aseptic carton packs from SIG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Aseptic Packaging in the Food and Beverage Industry

- 5.2 Market Challenges

- 5.2.1 Difficulty in Recycling the Packaging Material

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Cartons

- 6.1.2 Bags and Pouches

- 6.1.3 Cans

- 6.1.4 Bottles

- 6.2 By Application

- 6.2.1 Beverages

- 6.2.1.1 Ready-to-Drink

- 6.2.1.2 Dairy-based Beverages

- 6.2.2 Food

- 6.2.2.1 Processed Food

- 6.2.2.2 Fruits and Vegetables

- 6.2.2.3 Dairy Food

- 6.2.3 Pharmaceutical

- 6.2.1 Beverages

- 6.3 By Country

- 6.3.1 Brazil

- 6.3.2 Argentina

- 6.3.3 Mexico

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Bemis Company Inc.

- 7.1.3 DS Smith PLC

- 7.1.4 Elopak AS

- 7.1.5 Mondi PLC

- 7.1.6 Reynold Group Holdings PLC

- 7.1.7 Sonoco Products Company

- 7.1.8 Smurfit Kappa Group PLC

- 7.1.9 SIG Combibloc Group AG

- 7.1.10 Stora Enso Oyj

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

无菌包装食品市场规模、份额和成长分析:按材料类型、包装类型、应用、最终用途和地区划分-2026-2033年产业预测

无菌包装食品市场规模、份额和成长分析:按材料类型、包装类型、应用、最终用途和地区划分-2026-2033年产业预测 无菌包装市场分析及预测(至2035年):依类型、产品类型、技术、材料类型、应用、组件、製程、最终用户、功能划分

无菌包装市场分析及预测(至2035年):依类型、产品类型、技术、材料类型、应用、组件、製程、最终用户、功能划分 无菌包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

无菌包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球无菌包装市场报告2026年全球植物性食品包装市场报告

2026年全球无菌包装市场报告2026年全球植物性食品包装市场报告 外科手术袋市场 - 全球产业规模、份额、趋势、机会及预测(按袋类型、形状、治疗领域、最终用户、地区和竞争格局划分,2021-2031年)

外科手术袋市场 - 全球产业规模、份额、趋势、机会及预测(按袋类型、形状、治疗领域、最终用户、地区和竞争格局划分,2021-2031年) 全球蒸煮包装解决方案市场预测至2032年:按材料类型、包装类型、通路、技术、最终用户和地区蒸馏的分析

全球蒸煮包装解决方案市场预测至2032年:按材料类型、包装类型、通路、技术、最终用户和地区蒸馏的分析 无菌包装市场规模、份额和成长分析(按材料、类型、应用和地区划分)—产业预测(2026-2033 年)无菌包装市场预测至2032年:按包装类型、材料、应用和地区分類的全球分析

无菌包装市场规模、份额和成长分析(按材料、类型、应用和地区划分)—产业预测(2026-2033 年)无菌包装市场预测至2032年:按包装类型、材料、应用和地区分類的全球分析 无菌包装:全球市场份额和排名、总收入和需求预测(2025-2031年)

无菌包装:全球市场份额和排名、总收入和需求预测(2025-2031年)