|

市场调查报告书

商品编码

1939003

无菌包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Aseptic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

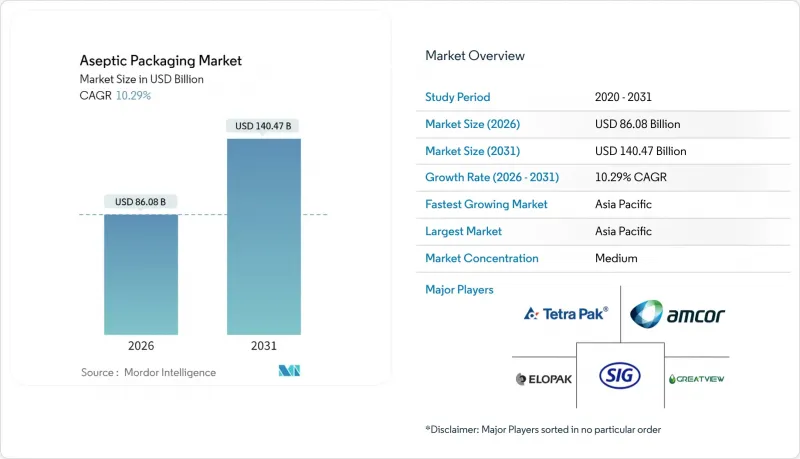

2025年无菌包装市场价值为780.5亿美元,预计到2031年将达到1,404.7亿美元,高于2026年的860.8亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 10.29%。

对常温保存食品和饮料的需求不断增长、食品安全法规日益严格以及降低低温运输成本的必要性,都提升了无菌和常温配送方式的吸引力。品牌商正在扩大无菌生产线,以满足缺乏冷藏基础设施地区对即饮机能饮料和常温保存乳製品日益增长的需求。同时,生物製药製造和个人化疗法的进步正在扩大製药业在无菌包装市场的收入基础。材料科学的创新,例如无铝阻隔性纸盒和不含PFAS的涂层,使製造商能够在不影响无菌性的前提下满足新的永续性要求。加工商和树脂製造商之间的整合增强了他们在波动较大的聚合物市场中的购买力。此外,数位印刷技术能够实现经济高效的小批量生产,适用于日益增多的SKU(库存单位)。

全球无菌包装市场趋势与洞察

即饮机能饮料的快速成长

功能性即饮饮料需要无菌解决方案,以在室温下保存微量营养素、益生菌和植物成分长达 12 个月。品牌商正在使用高阻隔阻隔性纸盒和多层瓶,以阻隔氧气、光线和紫外线,方便在便利商店进行最后一公里配送。美国、中国和泰国的饮料填充商正在安装新的高速无菌生产线,产能超过每小时 48,000 瓶,以满足新型运动营养、能量和植物蛋白饮料产品的产品推出。随着食品级无菌和药品级验证之间的界限日益模糊,管瓶和小瓶供应商正致力于吸引那些寻求高端产品定位的饮料客户。原料供应商指出,无菌加工实现的长保质期允许减少防腐剂的使用,增加活性成分的含量,从而支持洁净标示和更高的零售价格。

扩大常温乳製品在亚洲新兴市场的分销

印度、越南和印尼正迅速从管控鬆散的冷藏供应链转向无菌常温牛奶和优格。都市区乳製品加工商正投资超高温灭菌器和Brick包装灌装机,以服务电网不稳定导致冷藏成本居高不下的农村地区。在中国,2024年起禁止在常温饮料中使用復原奶粉,这推动了对纯牛奶无菌生产线的投资,进而带动了对能够耐受135℃高温灭菌的低酸纸盒复合材料的需求。跨国品牌正与当地合作社成立合资企业,以确保原乳供应,并在农场附近安装模组化无菌微型工厂,从而显着降低道路运输成本并防止牛奶变质。因此,无菌包装市场正成为新兴亚洲国家政府长期粮食安全政策的重要组成部分。

多层聚合物价格波动

2024年聚乙烯和聚丙烯价格每磅上涨5美分,挤压了加工商的利润空间,并导致季度附加费的增加。原料市场(例如石脑油和乙烷)的波动,使得纸箱吸嘴、瓶盖和阻隔膜的预算编制变得更加复杂。大规模买家透过签订多年期合约对冲树脂价格,而小规模填充商则受到现货价格波动的影响,并且由于需要推迟将热填充线更换为无菌设备,导致资本计划延期。全球树脂供应的结构性限制,包括裂解装置意外停产和运输瓶颈,可能会在可预见的未来继续导致价格波动。

细分市场分析

在无菌包装市场,纸盒包装预计到2025年将占销售额的63.30%,主要得益于其在乳製品、果汁和即饮咖啡领域的高渗透率。纸盒的矩形设计最大限度地提高了托盘利用率和商店面积,而新型的无吸管瓶盖也符合减少塑胶使用的目标。同时,受注射用生物製药、疫苗和细胞疗法广泛应用的推动,管瓶和安瓿瓶预计到2031年将以12.98%的复合年增长率增长。管瓶和安瓿瓶的无菌包装市场预计到2031年将达到109.4亿美元,这反映了它们在人用和动物用药品的广泛应用。对于冰沙和风味牛奶等高黏度饮料而言,瓶装仍然是重要的包装选择,可重复密封的大容量包装提升了饮用的便利性。罐装产品凭藉其高抗穿刺性,已在超高温灭菌椰子水和高酸度食物泥等细分市场占据一席之地,但铝价波动和年轻消费者偏好纸质包装限制了其增长。袋装衬袋纸盒系统因其便于运输和开封后保质期长而受到餐饮服务商的青睐,而单份吸嘴袋则为婴儿饮品和运动营养凝胶提供了便携性。

减少碳足迹的努力正在推动产品层面的创新。 SIG公司计划于2025年推出一款完全可回收、不含铝的1升纸盒,该纸盒在室温下可保持12个月的保质期,并已被欧洲主要乳製品品牌率先采用。同时,管瓶製造商开发出聚合物包覆玻璃的复合容器,在保持惰性接触面的同时,重量减轻了30%,有助于减少全球疫苗接种宣传活动中的运输排放。随着新材料的不断涌现,产品在阻隔性能、可回收性和填充速度方面的差异化将继续塑造无菌包装市场的竞争优势。

区域分析

到2025年,亚太地区将占全球销售额的38.05%,其中中国、印度和印尼将引领这一市场。印度的国家营养计画旨在2027年将包装牛奶的普及率提高到15%以上,鼓励公私部门投资无菌包装产能。 SIG在古吉拉突邦新建的价值9000万欧元的工厂将新增40亿包的年产能,以供应当地的乳製品和饮用型优格市场。在中国,一项禁止将復原奶粉灌装到超高温灭菌(UHT)纸盒中的政策迫使加工商转向更可靠的製造商,从而加强了价格管控并提高了利润率。一家东南亚新兴企业正在推出一款采用250毫升纤薄纸盒包装的维生素强化茶,以吸引消费者随时随地饮用。

南美洲是成长最快的地区,预计到2031年将以14.02%的复合年增长率成长。在巴西,通膨压力促使消费者偏好散装和常温保存产品,推动包装食品市场到2024年达到1,136亿美元。柴油和电力成本的上涨促使内陆物流中心加大投资,以优先运输常温保存产品。阿根廷乳製品出口商正在利用软包装袋线将无乳糖牛奶运往智利和秘鲁,因此无需冷藏。北美和欧洲预计将实现中等个位数的成长,这主要得益于对永续性材料的转向,而非销售的扩张。欧盟对全氟烷基和多氟烷基物质(PFAS)的禁令正在推动基于氧化硅的纸盒阻隔材料的商业化,而美国填充商正在高风险地区应用机器人技术以应对劳动力短缺问题。儘管中东和非洲地区规模较小,但在人口成长和政府粮食安全战略的推动下,该地区具有巨大的长期成长潜力。埃及工业区是 UFlex 公司投资 2 亿美元兴建的层压板综合体的位置,该综合体旨在为该地区供应产品。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 即饮机能饮料的快速成长

- 扩大常温乳製品在亚洲新兴地区的销售

- 严格的食品安全法规推动了无菌包装的普及

- 受通货膨胀影响,物流方式从低温运输转向常温(通报不足)

- 转向永续、轻量化的包装至关重要。

- D2C品牌数位印刷短SKU的兴起(报道不足)

- 市场限制

- 多层聚合物价格波动

- 无菌灌装生产线需要较高的初始资本投入

- 铝箔复合材料回收基础设施有限(数据瞒报)

- 关于 PFAS 阻隔涂层的管制不确定性(未充分通报)

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 定价分析

- 饮料无菌包装-需求洞察

第五章 市场规模与成长预测

- 副产品

- 纸盒

- 瓶子

- 罐头

- 袋子和小袋

- 管瓶和安瓿

- 按材料组成

- 纸和纸板

- 塑胶(聚丙烯、聚乙烯、聚对苯二甲酸乙二醇酯)

- 玻璃

- 金属(铝、钢)

- 复合层压板

- 透过使用

- 饮料

- 即饮饮料

- 乳製品饮料

- 食物

- 加工食品

- 水果和蔬菜

- 乳製品

- 製药

- 个人护理及化妆品

- 饮料

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 以色列

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Tetra Pak International SA

- SIG Combibloc Group

- Amcor PLC

- Elopak ASA

- IPI SRL(Coesia Group)

- DS Smith PLC

- Smurfit Kappa Group

- Mondi PLC

- Uflex Limited

- Schott AG

- Gerresheimer AG

- Toyo Seikan Group

- CDF Corporation

- BIBP Sp. z oo

- Nampak Ltd

- Greatview Aseptic Packaging

- Liqui-Box(Graphic Packaging)

- OPLATEK Group

- Sealed Air Corporation

- ProAmpac

第七章 市场机会与未来展望

The aseptic packaging market was valued at USD 78.05 billion in 2025 and estimated to grow from USD 86.08 billion in 2026 to reach USD 140.47 billion by 2031, at a CAGR of 10.29% during the forecast period (2026-2031).

Growing demand for shelf-stable foods and beverages, stricter food-safety rules, and the need to trim cold-chain costs are reinforcing the appeal of sterile, ambient-distribution formats. Brand owners are scaling aseptic lines to meet rising demand for ready-to-drink (RTD) functional beverages and for shelf-stable dairy in regions where refrigeration infrastructures remain patchy. At the same time, biologics manufacturing and personalized therapies are widening the pharmaceutical revenue base for the aseptic packaging market. Material science breakthroughs-such as aluminum-free high-barrier cartons and PFAS-free coatings-help manufacturers comply with new sustainability mandates without sacrificing sterility. Consolidation among converters and resin producers is bolstering purchasing leverage in a volatile polymer market, while digital printing is enabling cost-effective short runs that suit proliferating stock-keeping units.

Global Aseptic Packaging Market Trends and Insights

Rapid Growth of RTD Functional Beverages

Functional RTD drinks now demand aseptic solutions that lock in sensitive micronutrients, probiotics, and botanicals for up to 12 months at ambient temperatures. Brands are selecting high-barrier cartons and multilayer bottles that offer oxygen, light, and UV protection while easing last-mile distribution in convenience stores. Beverage fillers in the United States, China, and Thailand have installed new high-speed aseptic lines rated above 48,000 bottles per hour to serve sports-nutrition, energy-tea, and plant-based protein launches. The overlap between food-grade sterility and pharmaceutical-grade validation is narrowing, encouraging suppliers of vials & ampoules to court beverage customers seeking premium positioning. Ingredient suppliers note that the longer shelf life afforded by aseptic processing allows them to blend less preservative and more active compounds, supporting cleaner labels and higher retail prices.

Expansion of Ambient Dairy Distribution in Emerging Asia

India, Vietnam, and Indonesia are rapidly upgrading from loosely supervised chilled supply chains to aseptic shelf-stable milk and yogurt. Urban dairy processors are investing in UHT sterilizers and brick-pack fillers to reach rural districts where grid instability inflates refrigeration costs. In China, the 2024 decision to prohibit reconstituted milk powder in shelf-stable beverages elicited a wave of capex for pure-milk aseptic lines, driving demand for low-acid carton laminates that can withstand 135 °C sterilization. Multinational brands are forming joint ventures with local cooperatives to secure raw milk and deploy modular aseptic micro-plants close to farms, slashing road-haul costs and mitigating spoilage. As a result, the aseptic packaging market is becoming integral to the long-term food-security agendas of emerging Asian governments.

Volatility in Multilayer Polymer Prices

Polyethylene and polypropylene prices rose by 5 cents per pound in 2024, tightening converter margins and prompting quarterly surcharges. Fluctuating naphtha and ethane feedstock markets complicate budgeting for carton spouts, caps, and barrier films. While large purchasers hedge through multi-year resin contracts, small fillers experience spot-price pain that slows capital projects aimed at replacing hot-fill lines with aseptic equipment. Structural constraints in global resin supply, including unplanned outages at cracker complexes and shipping bottlenecks, signal that price volatility will persist for the near term.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Food-Safety Regulations Pushing Sterile Packaging Adoption

- Inflation-Linked Shift From Cold-Chain to Shelf-Stable Logistics

- High Initial CAPEX for Aseptic Filling Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cartons secured 63.30% of 2025 revenue within the aseptic packaging market thanks to deep penetration in dairy, juice, and RTD coffee. Their rectangular footprint maximizes pallet efficiency and shelf facings, and new straw-less closures appeal to plastic-reduction goals. Meanwhile, vials & ampoules are expanding at a 12.98% CAGR through 2031 as injectable biologics, vaccines, and cell therapies proliferate. The aseptic packaging market size for vials & ampoules is projected to reach USD 10.94 billion by 2031, reflecting adoption in both human and veterinary medicine. Bottles remain important for high-viscosity drinks such as smoothies and for flavored milk where larger resealable formats enhance consumption convenience. Cans hold niche positions in UHT coconut water and high-acid fruit purees due to their robust puncture resistance, though growth is tempered by aluminum price swings and by younger consumers' preference for paper-based packs. Pouch-based bag-in-box systems attract food-service operators seeking compact shipping and extended post-opening shelf life; single-serve spouted pouches offer portability for early-childhood beverages and sports nutrition gels.

The pursuit of carbon-footprint cuts is stimulating product-level innovation. SIG's 2025 launch of a fully recyclable, aluminum-free 1 L carton that maintains a 12-month ambient shelf life won early adoption from leading European dairy brands. Separately, glass vial manufacturers have developed polymer-over-glass hybrid containers that reduce weight by 30% while retaining inert contact surfaces, easing freight emissions in global vaccine campaigns. As new materials emerge, product-level differentiation in barrier performance, recyclability, and filling speed will continue to shape competitive advantage within the aseptic packaging market.

Aseptic Packaging Market Report is Segmented by Product (Cartons, Bottles, Cans, Bags and Pouches, and More), Material Composition (Paper and Paperboard, Plastics, Glass, Metal, Composite Laminates), Application (Beverage, Food, Pharmaceuticals, Personal Care and Cosmetics), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.05% of revenues in 2025, driven by China, India, and Indonesia. National nutrition programs in India aim to increase packaged milk penetration above 15% by 2027, catalyzing public-private investment in aseptic capacity. SIG's EUR 90 million green-field plant in Gujarat adds 4 billion pack annual output devoted to local dairy and drinkable yogurt. China's policy forbidding reconstituted milk powder in UHT cartons is pushing processors toward higher-integrity manufacturers, reinforcing price discipline and lifting margins. Southeast Asian start-ups are launching vitamin-fortified teas in 250 mL slim cartons to capture on-the-go consumption.

South America is the fastest growing region, projected to rise at 14.02% CAGR through 2031. Brazil's packaged-food market reached USD 113.6 billion in 2024 as inflationary pressures encouraged consumers to favor large-format, shelf-stable purchases. Investments in inland distribution centers favor ambient products due to high diesel and electricity costs. Argentina's dairy exporters are leveraging flexible pouch lines to ship lactose-free milk to Chile and Peru without refrigeration. North America and Europe show mid-single-digit growth, propelled by sustainability-driven material swaps rather than volume expansion. The EU PFAS ban stimulates the commercialization of silicon-oxide-based carton barriers, while US fillers adopt robotics in high-care zones to offset labor shortages. The Middle East and Africa, although smaller in value, present long-term upside tied to demographic growth and government food-security strategies. Egypt's industrial zones host UFlex's USD 200 million laminated-board complex aimed at regional supply

- Tetra Pak International SA

- SIG Combibloc Group

- Amcor PLC

- Elopak ASA

- IPI SRL (Coesia Group)

- DS Smith PLC

- Smurfit Kappa Group

- Mondi PLC

- Uflex Limited

- Schott AG

- Gerresheimer AG

- Toyo Seikan Group

- CDF Corporation

- BIBP Sp. z o.o.

- Nampak Ltd

- Greatview Aseptic Packaging

- Liqui-Box (Graphic Packaging)

- OPLATEK Group

- Sealed Air Corporation

- ProAmpac

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of RTD functional beverages

- 4.2.2 Expansion of ambient dairy distribution in emerging Asia

- 4.2.3 Stringent food-safety regulations pushing sterile packaging adoption

- 4.2.4 Inflation-linked shift from cold-chain to shelf-stable logistics (under-reported)

- 4.2.5 Shift toward sustainable, lightweight packaging mandates

- 4.2.6 Rise of digital?print-enabled short SKUs for D2C brands (under-reported)

- 4.3 Market Restraints

- 4.3.1 Volatility in multilayer polymer prices

- 4.3.2 High initial CAPEX for aseptic filling lines

- 4.3.3 Limited recycling infrastructure for aluminum-foil laminates (under-reported)

- 4.3.4 Regulatory uncertainty around PFAS barrier coatings (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Aseptic Packaging for Beverages - Demand Insights

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Cartons

- 5.1.2 Bottles

- 5.1.3 Cans

- 5.1.4 Bags and Pouches

- 5.1.5 Vials and Ampoules

- 5.2 By Material Composition

- 5.2.1 Paper and Paperboard

- 5.2.2 Plastics (PP, PE, PET)

- 5.2.3 Glass

- 5.2.4 Metal (Aluminum, Steel)

- 5.2.5 Composite Laminates

- 5.3 By Application

- 5.3.1 Beverage

- 5.3.1.1 Ready-to-drink (RTD) Beverages

- 5.3.1.2 Dairy-based Beverages

- 5.3.2 Food

- 5.3.2.1 Processed Food

- 5.3.2.2 Fruits and Vegetables

- 5.3.2.3 Dairy Food

- 5.3.3 Pharmaceuticals

- 5.3.4 Personal Care and Cosmetics

- 5.3.1 Beverage

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Middle East

- 5.4.4.1 Israel

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Turkey

- 5.4.4.5 Rest of Middle East

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Egypt

- 5.4.5.3 Rest of Africa

- 5.4.6 South America

- 5.4.6.1 Brazil

- 5.4.6.2 Argentina

- 5.4.6.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Tetra Pak International SA

- 6.4.2 SIG Combibloc Group

- 6.4.3 Amcor PLC

- 6.4.4 Elopak ASA

- 6.4.5 IPI SRL (Coesia Group)

- 6.4.6 DS Smith PLC

- 6.4.7 Smurfit Kappa Group

- 6.4.8 Mondi PLC

- 6.4.9 Uflex Limited

- 6.4.10 Schott AG

- 6.4.11 Gerresheimer AG

- 6.4.12 Toyo Seikan Group

- 6.4.13 CDF Corporation

- 6.4.14 BIBP Sp. z o.o.

- 6.4.15 Nampak Ltd

- 6.4.16 Greatview Aseptic Packaging

- 6.4.17 Liqui-Box (Graphic Packaging)

- 6.4.18 OPLATEK Group

- 6.4.19 Sealed Air Corporation

- 6.4.20 ProAmpac

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

无菌包装食品市场规模、份额和成长分析:按材料类型、包装类型、应用、最终用途和地区划分-2026-2033年产业预测

无菌包装食品市场规模、份额和成长分析:按材料类型、包装类型、应用、最终用途和地区划分-2026-2033年产业预测 无菌包装市场分析及预测(至2035年):依类型、产品类型、技术、材料类型、应用、组件、製程、最终用户、功能划分

无菌包装市场分析及预测(至2035年):依类型、产品类型、技术、材料类型、应用、组件、製程、最终用户、功能划分 2026年全球无菌包装市场报告2026年全球植物性食品包装市场报告

2026年全球无菌包装市场报告2026年全球植物性食品包装市场报告 外科手术袋市场 - 全球产业规模、份额、趋势、机会及预测(按袋类型、形状、治疗领域、最终用户、地区和竞争格局划分,2021-2031年)

外科手术袋市场 - 全球产业规模、份额、趋势、机会及预测(按袋类型、形状、治疗领域、最终用户、地区和竞争格局划分,2021-2031年) 全球蒸煮包装解决方案市场预测至2032年:按材料类型、包装类型、通路、技术、最终用户和地区蒸馏的分析

全球蒸煮包装解决方案市场预测至2032年:按材料类型、包装类型、通路、技术、最终用户和地区蒸馏的分析 无菌包装市场规模、份额和成长分析(按材料、类型、应用和地区划分)—产业预测(2026-2033 年)无菌包装市场预测至2032年:按包装类型、材料、应用和地区分類的全球分析

无菌包装市场规模、份额和成长分析(按材料、类型、应用和地区划分)—产业预测(2026-2033 年)无菌包装市场预测至2032年:按包装类型、材料、应用和地区分類的全球分析 无菌包装:全球市场份额和排名、总收入和需求预测(2025-2031年)

无菌包装:全球市场份额和排名、总收入和需求预测(2025-2031年) 无菌包装市场按应用、技术、材料、产品类型、最终用户和分销管道划分-2025-2032 年全球预测

无菌包装市场按应用、技术、材料、产品类型、最终用户和分销管道划分-2025-2032 年全球预测