|

市场调查报告书

商品编码

1640417

控制阀:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Control Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

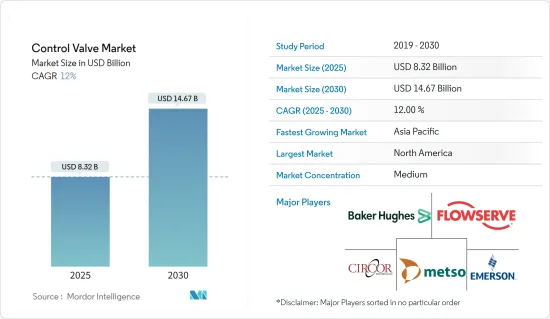

控制阀市场规模预计在 2025 年为 83.2 亿美元,预计到 2030 年将达到 146.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 12%。

在预计预测期内,管道和基础设施扩建投资的增加以及多个行业自动化程度的提高将推动对控制阀的需求。

主要亮点

- 控制阀是一种根据控制器的讯号调节流道大小来调节流体流量的装置。这有助于精确的流量控制和随后的压力、温度和液位等製程变数的调节,这对于石油和天然气、水资源管理、发电、食品和饮料以及汽车等行业至关重要。一般来说,各行业都采用线性和旋转两种类型的控制阀来提供卓越的效率和安全性。

- 控制阀可以透过电动、气动或液压方式操作。它接收来自控制器(例如可程式逻辑控制器 (PLC))的讯号来启动运动,从而改变流量。控制器(无论是 PLC 或分散式控制系统 (DCS))都会将目前流速与所需设定值进行比较。然后,控制器调节阀门产生输出,以实现所需的流速。

- 技术进步在形成创新解决方案方面发挥了关键作用,透过简化操作来提高加工厂的效率。随着产业需求的不断发展,控制阀和阀门自动化解决方案的供应商需要开发产品和流程来应对这些新的挑战。由于各个製程工业的自动化程度不断提高、石油和天然气行业的投资不断增加以及高功率需求,控制阀市场预计在未来几年将会成长。

- 控制阀市场的成长受到多种因素的推动,例如对用于监控各个工厂设备的无线基础设施的需求不断增加、对自动化的日益关注以及製程工业中机构数量的不断增加。为了满足市场需求,我们开发了能够承受多次循环和高温的控制阀。此外,对替代能源,特别是可再生能源的投资日益重视,为控制阀创造了新的机会和潜在的应用。例如,国际能源总署预测全球70%的能源投资将流向可再生能源。

- 预计预测期内,工业自动化的普及和智慧控制阀的使用增加将进一步推动市场成长。控制阀的需求是由全球发电厂数量的不断增长以及新兴经济体对能源和电力的不断增长的需求所推动的。这些阀门也用于核能发电厂,特别是在化学处理、给水、冷却水和蒸气涡轮控制系统中。

- 原物料价格波动是控制阀市场成长的一大障碍。原材料成本在决定控制阀的价格时起着关键作用,原材料价格上涨对供应商构成了重大挑战,因为它会降低他们的利润率。铜、不銹钢、铸铁、铝、黄铜和青铜是製造控制阀的主要原料。预计缺乏标准化认证和政府政策将抑制市场成长。

控制阀市场趋势

石油和天然气板块可望引领市场

- 在石油和天然气工业中,阀门发挥着至关重要的作用,因为它们是管道系统的重要组成部分。阀门的主要作用包括隔离和保护设备、控制流量、引导和指挥原油精製过程。这些阀门旨在透过控制器的电、液压和气动讯号调节流量、温度和压力。其自主操作允许远端操作,无需操作员不断监控和调整。

- 控制阀因其调节流量、压力和温度的能力而在石油和天然气行业越来越受欢迎。这些阀门根据液压、气动或电气控制器的讯号调整流路大小,从而实现远端操作。此外,对流体处理技术的投资不断增加,特别是在石油和天然气领域,对控制阀市场的成长做出了重大贡献。

- 石油和天然气行业数位化和自动化的日益发展趋势推动了对控制阀的需求。因此,控制阀製造商正在致力于研发和改进他们的产品,以满足最终用户产业的需求。中东和非洲、中国和北美等地区的石油和天然气探勘活动的增加预计将显着增强市场成长。

- 2023年6月,挪威宣布核准在挪威大陆棚进行19项石油和天然气作业,总投资超过190亿美元。这些计划包括对新开发、现有矿区的扩建以及现有矿区的扩建计划的投资。由于先前依赖俄罗斯的欧洲国家开始寻求替代能源,乌克兰衝突增加了挪威的收益。因此,欧盟为使石油和天然气产业更加自力更生而进行的大规模投资将扩大控制阀的商机。

- 石油和天然气行业依赖控制阀,并且是其使用至关重要的行业。新的石油和天然气探勘计划、输送管道计划和维护作业使得控制阀在世界范围内的需求量很大。

- 根据国际能源总署(IEA)预测,到2030年,全球对石油、天然气和煤炭等石化燃料的需求将达到前所未有的高峰。天然气需求激增的原因是全球能源政策的不断演变、太阳能电池板和电动车等干净科技的快速发展、热泵的日益普及以及俄罗斯入侵乌克兰后欧洲被迫放弃天然气。此外,该领域不断发展的自动化技术预计将显着推动市场成长。

- 随着石油和天然气运输量的增加,预计陆上应用控制阀的需求将会增加。例如,根据美国能源资讯署的数据,预计到2025年,全球原油产量的28%将来自海上,其余72%将来自陆上。

- 截至 2024 年 2 月,该地区共有 296 个陆上钻机,另有 95 个陆上钻机、53 个中东海上钻井平台和 16 个非洲海上钻井平台。这些值得关注的能力以及石油和天然气行业的预期成长无疑对市场有利。

预计北美将占据较大的市场占有率

- 北美是世界上最重要的控制阀市场之一。在美国和加拿大,各行业都有巨大的需求,包括石油和天然气、电力、食品和包装以及化学品。随着工业自动化的快速发展,该地区预计将成为控制阀需求的前沿。

- 这些国家的快速工业化和交通运输业的成长预计将增加对石油和天然气的需求。此外,向不断增长的人口提供饮用水的需求导致了海水淡化厂的安装,进一步增加了对控制阀的需求。废弃物和污水管理也是预计推动未来需求的关键领域。

- 与加拿大相比,美国在增加该地区的需求方面发挥关键作用。几乎所有终端用户领域的需求都在增加,尤其是石油和天然气、精製和发电领域。该国的重点产业,包括石油和天然气、可再生能源以及水和用水和污水处理,正在转向具有嵌入式处理器和网路功能的阀门技术,以便与透过中央控制站协调的先进监控技术配合使用。

- 美国石油产量正在大幅扩大。美国最大的石油生产商埃克森美孚公司宣布,计划提高西德克萨斯州州二迭纪盆地的石油产量,目标是到 2024 年实现日产超过 100 万桶油当量的目标。与目前的生产能力相比,这增加了约 80%。雪佛龙预测,到 2020 年净生产量将增加至 60 万桶/天,到 2023 年将增加至 90 万桶/天。

- 北美页岩油的繁荣带来了对流体处理设备和组件,尤其是控制阀的巨大需求。这些阀门对于规范页岩油探勘生产过程,确保页岩油通过管道的顺利输送起着至关重要的作用。新的上游油气探勘计划的启动预计将推动石油和天然气产业对控制阀的需求。

- 在美国,开发新的页岩油计划需要建造额外的管道来输送页岩油。贝克休斯称,北美目前拥有世界上最多的石油和天然气钻机。截至 2023 年 5 月,该地区总合776 个陆上钻井钻机,另有 22 个海上钻机。随着俄罗斯出口制裁逐渐生效以及北美探勘活动的活性化,2022 年下半年石油和天然气钻机数量激增。

- 随着该地区对可再生能源计画的重视,太阳能热能装置的数量急剧增加,控制阀的使用也随之激增。该地区拥有丰富的风能、太阳能、地热能、水力和生物质资源。丰富的资金筹措机会和高技能劳动力推动了可再生能源计划的需求。

- 由于有关水处理和清洁度的规定日益严格,用水和污水产业是流体处理技术的重要消费者。预计该地区对用水和污水行业的投资增加将提供巨大的市场成长机会。

控制阀产业概况

控制阀市场高度分散,既有全球参与者,也有中小型企业。市场的主要参与者包括艾默生电气公司、福斯公司、贝克休斯公司、美卓公司和 CIRCOR 国际公司。市场参与者正在采取联盟和收购等策略来加强其产品供应并获得永续的竞争优势。

- 2024年2月,艾默生向全球发布了一项创新解决方案,将改变阀门在工业应用中的安装方式以及与最终用户的互动方式。最终用户需要了解控制阀的性能、解决问题、减少维护并提高整体阀门的性能。 Fisher(TM) FieldView(TM) DVC7K 数位阀门控制器透过建立最佳化操作的路径解决了这些问题以及更多问题。

- 2023年10月,安德里兹与福斯签署协议,收购NAF AB阀门业务。交付的生产装置和设备已配备NAF控制阀多年。此次收购进一步扩大并加强了安德里茨在製程控制领域的产品和服务组合。

- 2023 年 5 月,艾默生推出 ASCO 系列 209 比例流量控制阀,该阀采用专门设计的节省空间的结构,具有无与伦比的精度、压力等级、流量特性和能源效率。该阀门的最佳尺寸和出色性能使其能够在需要精确度的各种应用中实现精确的流体流量调节,包括医疗设备、食品和饮料以及暖通空调行业。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 产业影响评估

第五章 市场动态

- 产业供应链分析

- 市场驱动因素

- 更关注新兴市场的电力和用水和污水

- 最终用户关注环境问题和老化基础设施维修以保持竞争力

- 市场挑战

- 为了保持竞争力,最终用户关注环境问题和老化基础设施的维修

- 预计油价的动态波动将影响整体计划支出。

- 市场机会

第六章 市场细分

- 按类型

- 手套

- 球

- 蝴蝶

- 插头

- 隔膜

- 其他阀门

- 按最终用户产业

- 石油和天然气

- 化工、石化、化肥

- 能源和电力

- 用水和污水处理

- 金属与矿业

- 其他最终用户产业(食品和饮料、製药、纸浆和造纸等)

- 按地区

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 亚洲

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 拉丁美洲

- 中东和非洲

- 北美洲

第七章 竞争格局

- 公司简介

- Emerson Electric Co.

- Flowserve Corporation

- Baker Hughes Company

- Metso Corporation

- CIRCOR International Inc.

- IMI PLC

- Christian Burkert GmbH & Co. KG

- GEA Group Aktiengesellschaft

- Neway Valve(Suzhou)Co. Ltd

第八章投资分析

第 9 章:未来趋势

The Control Valve Market size is estimated at USD 8.32 billion in 2025, and is expected to reach USD 14.67 billion by 2030, at a CAGR of 12% during the forecast period (2025-2030).

Over the forecast period, increasing investments in pipeline and infrastructure expansion and the increasing adoption of automation across several industries are expected to boost the demand for control valves.

Key Highlights

- A control valve is a device utilized to regulate fluid flow by adjusting the size of the flow passage in response to a signal from a controller. This facilitates the precise flow rate management and subsequent regulation of process variables such as pressure, temperature, and liquid level, which are crucial in industries such as oil and gas, water management, power generation, food and beverages, and automotive. Typically, two control valves, linear and rotary, are employed in various industries, offering superior efficiency and safety.

- A control valve can be operated through electrical, pneumatic, or hydraulic means. It receives a signal from a controller, such as a Programmable Logic Controller (PLC), to initiate movement and consequently alter the flow. Whether a PLC or a Distributed Control System (DCS), the controller compares the current flow rate with the desired setpoint value. Subsequently, the controller generates an output to adjust the valve and achieve the desired flow rate.

- Technological advancements have played a key role in shaping innovative solutions that enhance the efficiency of process plants by streamlining their operations. As industry requirements continue to evolve, suppliers of control valves and valve automation solutions are expected to develop products and processes that address these new challenges. The control valves market is anticipated to grow in the coming years, driven by increasing automation in various process industries, rising investment in the oil and gas sector, and high-power requirements.

- The growth of the control valve market is being propelled by several factors, including the escalating requirement for wireless infrastructure to monitor equipment in diverse plants, an increased emphasis on automation, and a rising number of process industry establishments. In response to market demand, control valves with many cycles and the ability to withstand high temperatures have been developed. Additionally, the growing emphasis on investing in alternative energy sources, particularly renewable energy, has created new opportunities and potential uses for control valves. For example, the IEA forecasts that 70% of all global energy investment will be directed toward renewable energy.

- Market growth is expected to be further boosted over the forecast period due to the increasing adoption of industrial automation, which will drive the use of smart control valves. The demand for control valves is driven by the growing number of power generation plants worldwide and the increasing need for energy and power from developing economies. These valves are also utilized in nuclear power plants, particularly in chemical treatment, feed water, cooling water, and steam turbine control systems.

- Fluctuations significantly hinder the control valve market's growth in terms of raw material prices. The costs of raw materials play a crucial role in determining the prices of control valves, and an increase in raw material prices poses a significant challenge for vendors as it can diminish their profit margin. Copper, stainless steel, cast iron, aluminum, brass, and bronze are the primary raw materials used to produce control valves. The absence of standardized certifications and government policies is anticipated to serve as restraints to market growth.

Control Valve Market Trends

The Oil and Gas Segment is Expected to Drive the Market

- Valves play a crucial role in the oil and gas sector as they are vital to any piping system. Their primary functions include equipment isolation and protection, flow rate control, and guidance and direction of the crude oil refining process. These valves are designed to regulate flow rate, temperature, and pressure through a controller's electrical, hydraulic, or pneumatic signals. Their automatic operation allows for remote operation, eliminating an operator's need for constant monitoring and adjustment.

- Control valves are gaining popularity in the oil and gas sector owing to their ability to regulate flow rate, pressure, and temperature. These valves adjust the flow passage size based on signals from a hydraulic, pneumatic, or electrical controller, enabling remote operation. Furthermore, increased investments in fluid handling technology, particularly in the oil and gas sector, are significantly contributing to the growth of the control valve market.

- The increasing inclination toward digitalization and automation within the oil and gas sector is increasing the need for control valves. Consequently, manufacturers of control valves are consistently involved in research and development endeavors to create and enhance their offerings in accordance with the demands of end-user industries. The escalating number of oil and gas exploration ventures in regions like the Middle East, Africa, China, and North America is projected to bolster the market's growth significantly.

- In June 2023, Norway declared its endorsement of 19 oil and gas ventures on the Norwegian continental shelf, with a total investment value exceeding USD 19 billion. These projects encompass novel developments, expanding existing fields, and investing in projects to augment extraction at existing areas. The Ukraine conflict augmented Norway's revenues as European nations previously dependent on Russia sought alternative energy sources. Consequently, significant investments in the European Union to enhance self-reliance in the oil and gas sector will amplify opportunities for control valves.

- The oil and gas sector relies on control valves, making it a pivotal sector for their utilization. Control valves are in high demand globally due to new oil and gas exploration projects, transportation pipeline initiatives, and maintenance operations.

- As per the International Energy Agency (IEA), the global demand for fossil fuels such as oil, gas, and coal is projected to reach an unprecedented peak by 2030. This surge can be attributed to evolving energy policies worldwide, the rapid advancement of clean technologies like solar panels and electric vehicles, the growing adoption of heat pumps, and the compelled transition from gas in Europe following Russia's invasion of Ukraine. Furthermore, the sector's escalating automation technologies are anticipated to propel the market growth significantly.

- The demand for control valves across onshore applications is expected to rise with the increasing distribution of oil and gas. For instance, according to EIA, in 2025, it is projected that 28% of the world's crude oil production will be derived from offshore sources, with the remaining 72% being extracted onshore.

- As of February 2024, there were 296 land rigs in that region, with a further 53 rigs located offshore in the Middle East and 95 land rigs in that region, with 16 rigs located offshore in Africa. These notable capabilities and the anticipated growth in the oil and gas industry will undoubtedly generate substantial prospects for the market.

North America is Expected to Hold a Significant Market Share

- North America is one of the world's most significant markets for control valves. There is immense demand from various industries in the United States and Canada, including oil and gas, electricity, food and packaging, and chemicals. With rapid industrial automation, the region is expected to spearhead the need for control valves.

- Rapid industrialization and the growing transportation sector in these nations are expected to increase the demand for oil and gas. The need to provide potable water to the ever-increasing population also leads to the setting up of desalination plants, further resulting in the demand for control valves. Waste and wastewater management is also a considerable segment that is expected to drive future demand.

- The United States plays a critical role in increasing the demand from the region compared to Canada. The demand from almost all the end-user segments is increasing, especially from the oil and gas, refining, and power generation segments. Major industries in the country, such as oil and gas, renewable energy, and water and wastewater treatment, are moving toward valve technology with embedded processors and networking capability to work alongside sophisticated monitoring technology coordinated through a central control station.

- The United States is experiencing a significant expansion in oil production. ExxonMobil, a prominent oil producer in the country, announced its intention to augment production activity in the Permian Basin of West Texas, with a target of producing over 1 million barrels per day (bpd) of oil equivalent by 2024. This represents an increase of almost 80% compared to the current production capacity. Chevron was projected to increase its net oil-equivalent production to 600,000 bpd by 2020 and 900,000 bpd by 2023.

- The shale oil boom in North America generated a significant need for fluid handling equipment and components, particularly control valves. These valves play a crucial role in regulating the shale oil exploration and production process and ensuring the smooth transportation of shale oil through pipelines. The initiation of new upstream oil and gas exploration projects is anticipated to fuel the demand for control valves in the oil and gas industry.

- In the United States, developing new shale oil projects necessitates the construction of additional pipelines for the transportation of shale oil. According to Baker Hughes, North America currently boasts the highest number of oil and gas rigs worldwide. As of May 2023, the region had a total of 776 land rigs, with an additional 22 rigs situated offshore. The number of oil and gas rigs experienced a surge in late 2022 due to the gradual impact of sanctions on Russian exports, resulting in increased exploration activities in North America.

- The region has experienced a surge in the utilization of control valves due to the heightened emphasis on renewable energy initiatives, resulting in a rapid rise in the number of solar thermal energy facilities. The region boasts an abundance of wind, solar, geothermal, hydro, and biomass resources. The demand for renewable energy projects is fueled by ample financing opportunities and a highly skilled workforce.

- The water and wastewater industry is a significant consumer of fluid handling technology due to increasingly stringent regulations regarding the treatment and cleanliness of water. The increasing investments in the region's water and wastewater industry are expected to offer significant market growth opportunities.

Control Valve Indsutry Overview

The control valve market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Emerson Electric Co., Flowserve Corporation, Baker Hughes Company, Metso Corporation, and CIRCOR International Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- February 2024: Emerson released innovative solutions that transform valves installed in industrial applications and interact with end users globally. End users need to know how their control valves are performing, address any issues, and improve valve performance in general, for instance, by reducing maintenance. The Fisher(TM) FIELDVUE(TM) DVC7K digital valve controller addresses these and other issues by creating an optimized path to action.

- October 2023: Andritz signed an agreement with Flowserve Corporation to acquire its NAF AB valve business. The production plant and equipment deliveries have been equipped with NAF control valves for many years. This acquisition further extended and strengthened Andritz's product and service portfolio in process control.

- May 2023: Emerson unveiled the ASCO Series 209 proportional flow control valves, which boast unparalleled precision, pressure ratings, flow characteristics, and energy efficiency within a specially designed, space-saving structure. These valves, with their optimal size and exceptional performance, enable users to accurately regulate fluid flow in various devices demanding meticulous performance, such as those utilized in medical equipment, food and beverage, and HVAC industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Industry Supply Chain Analysis

- 5.2 Market Drivers

- 5.2.1 Growing emphasis on Power and Water and Wastewater in Emerging Markets

- 5.2.2 Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

- 5.3 Market Challenges

- 5.3.1 Focus of End Users on Environmental Issues and Refurbishment of Aging Infrastructure to Stay Competitive

- 5.3.2 Dynamic Change in Oil Prices is Expected to Influence the Overall Spending on the Projects

- 5.4 Market Opportunities

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Globe

- 6.1.2 Ball

- 6.1.3 Butterfly

- 6.1.4 Plug

- 6.1.5 Diaphragm

- 6.1.6 Other Types of Valves

- 6.2 By End-user Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemical, Petrochemical, and Fertilizer

- 6.2.3 Energy and Power

- 6.2.4 Water and Wastewater Treatment

- 6.2.5 Metal and Mining

- 6.2.6 Other End-user Industries (Food and Beverage, Pharmaceutical, Pulp and Paper, etc.)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 Germany

- 6.3.2.3 France

- 6.3.2.4 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 India

- 6.3.3.4 South Korea

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Emerson Electric Co.

- 7.1.2 Flowserve Corporation

- 7.1.3 Baker Hughes Company

- 7.1.4 Metso Corporation

- 7.1.5 CIRCOR International Inc.

- 7.1.6 IMI PLC

- 7.1.7 Christian Burkert GmbH & Co. KG

- 7.1.8 GEA Group Aktiengesellschaft

- 7.1.9 Neway Valve (Suzhou) Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE TRENDS

控制阀市场按阀门类型、材料类型、驱动技术、最终用途行业、销售管道和应用划分 - 全球预测 2025-2032

控制阀市场按阀门类型、材料类型、驱动技术、最终用途行业、销售管道和应用划分 - 全球预测 2025-2032 2025年全球控制阀市场报告半导体气动阀市场:按阀门类型、材料类型、操作类型、端口配置、功能、压力范围、分销渠道和应用 - 2025-2030 年全球预测

2025年全球控制阀市场报告半导体气动阀市场:按阀门类型、材料类型、操作类型、端口配置、功能、压力范围、分销渠道和应用 - 2025-2030 年全球预测 全球多孔流量控制阀市场

全球多孔流量控制阀市场 全球控制阀市场(按组件、材质、类型、尺寸、行业和地区划分)- 预测至 2030 年

全球控制阀市场(按组件、材质、类型、尺寸、行业和地区划分)- 预测至 2030 年 2025-2033 年控制阀市场报告(按类型、技术、组件、材料、最终用途行业和地区)2025年全球进气压力控制阀市场报告全球陶瓷控制阀市场全球飞机空气阀市场日本控制阀市场报告(按类型、尺寸、技术、组件、材料、最终用途行业和地区)2025-2033

2025-2033 年控制阀市场报告(按类型、技术、组件、材料、最终用途行业和地区)2025年全球进气压力控制阀市场报告全球陶瓷控制阀市场全球飞机空气阀市场日本控制阀市场报告(按类型、尺寸、技术、组件、材料、最终用途行业和地区)2025-2033