|

市场调查报告书

商品编码

1640447

二甲苯:市场占有率分析、产业趋势、统计数据、成长预测(2025-2030 年)Xylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

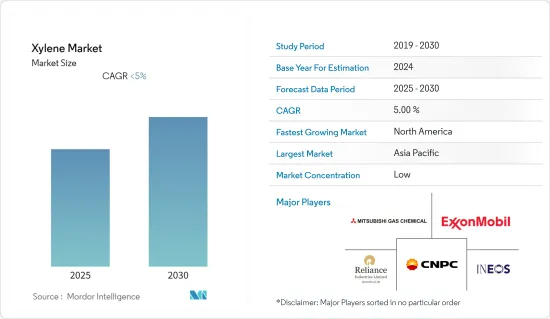

预测期内,二甲苯市场预计将以低于 5% 的复合年增长率成长。

新冠肺炎疫情对市场产生了中等影响。二甲苯用作油漆稀释剂的溶剂。新冠疫情导致全球建设活动停顿。然而,面罩、透明口罩、食品和电子商务包装的使用增加,刺激了对精对苯二甲酸、对苯二甲酸二甲酯和聚对苯二甲酸乙二醇酯等二甲苯衍生物的需求。这刺激了对二甲苯的需求。然而,由于终端用户产业的成长趋势,预计 2022 年市场将稳定成长。

关键亮点

- 短期内,市场受到快速成长的终端用户产业需求的推动。

- 然而,二甲苯的毒性作用和消费者对无塑胶产品的日益增强的认识预计会阻碍市场的成长。

- 由于页岩油的发现而产生的廉价原料和生物基二甲苯产量的上升趋势可能会在预测期内带来有利的机会。

- 预计在评估期内,亚太地区的二甲苯市场将出现健康成长,因为二甲苯因其优良性能将在塑胶、聚合物、油漆和涂料以及黏合剂等终端用途领域大量使用。

二甲苯市场趋势

市场主导的溶剂应用

- 二甲苯大部分被用作橡胶、皮革、油漆和印刷工业的溶剂。二甲苯的其他用途包括作为化学中间体、节能燃料和航空燃料以及作为呼吸设备(吸入器)的混合剂。

- 由于其特性和化学结构,二甲苯非常适合溶解难溶于水的化合物。二甲苯具有挥发性,容易蒸发。因此,当化合物需要溶解但溶剂需要蒸发时,就会使用它们。

- 二甲苯是硅片和钢的良好清洗,也用于对多种材料进行消毒。二甲苯是生产汽油、石油和喷射机燃料的原料。

- 由于投资和扩建,油漆和涂料领域的二甲苯使用量正在增加。例如,根据美国油漆协会的数据,2022 年美国油漆和涂料行业的产量约为 13.6 亿加仑。预计到 2023 年将超过 13.8 亿加仑。

- 此外,根据美国涂料协会的数据,到 2022 年,建筑涂料将占美国油漆和涂料市值的 51%。 OEM涂料占29%,特殊用途涂料占20%。同年,美国油漆和涂料市场价值约 310 亿美元。

- 因此,由于这些因素,市场溶剂部分在预测期内可能会出现成长。

中国主宰亚太地区

- 在亚太地区,中国是全球最大的生产基地。它也是对二甲苯的最大生产国和消费国。

- 中国有20个二甲苯产能扩张计画正在规划或宣布,到2025年总产能将达到约2,436万吨/年。该国的资本支出(CapEx)预计为 106.9 亿美元。浙江石化岱山二甲苯工厂二期预计将成为新增产能的主要项目。

- 中国石化企业正大幅扩张PTA产能。 2022年12月,英力士与中石化成立合资企业,在中国天津建造新的石化综合体。这些合约的总合为每年 700 万吨,总价值约为 100 亿美元。

- INEOS 同意收购中国石油化学股份有限公司子公司上海赛科石油化学有限公司(「赛科」) 50% 的股份。赛科目前生产420万吨石化产品,包括二甲苯、甲苯、乙烯、丙烯、聚乙烯、聚丙烯、苯乙烯、聚苯乙烯、丙烯腈、丁二烯和苯。该综合体占地 200 公顷,位于上海化学工业园区。

- 中国是PET树脂的重要生产国,其中中油集团和江苏三房巷是全球产量最大的生产商,产能都超过200万吨。因此,终端用户产业对 PET 的需求不断增加,推动了对二甲苯的需求。

- 杜邦公司决定投资约 3,000 万美元在中国东部江苏省张家港市建造一个新的黏合剂生产工厂。该工程预计将于 2021 年底开工,并预计于 2023 年初投入运作。

- 因此,由于投资增加和终端用户行业需求增加,二甲苯市场在预测期内可能会成长。

二甲苯产业概况

二甲苯市场较为分散。主要企业(不分先后顺序)包括埃克森美孚、信实工业有限公司、英力士、中国石油天然气集团公司、三菱瓦斯化学株式会社。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 调查前提条件

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 驱动程式

- 扩大二甲苯作为溶剂和单体的用途

- 快速成长的终端用户产业的需求不断增加

- 限制因素

- 二甲苯使用的有害健康影响及管制

- 其他限制因素

- 产业价值链分析

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场区隔(市场规模(基于数量))

- 类型

- 邻二甲苯

- 间二甲苯

- 对二甲苯

- 混合二甲苯

- 应用

- 溶剂

- 单体

- 其他的

- 最终用户产业

- 塑胶和聚合物

- 油漆和涂料

- 胶水

- 其他的

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 欧洲其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争格局

- 併购、合资、合作与协议

- 市场占有率(%)**/排名分析

- 主要企业策略

- 公司简介

- Braskem

- China Petroleum & Chemical Corporation

- CNPC(China National Petroleum Corporation)

- ENEOS Corporation

- Exxon Mobil Corporation

- Fujan Refining & Petrochemical Company Limited

- Indian Oil Corporation Ltd

- INEOS

- Mangalore Refinery & Petrochemicals Ltd

- Mitsubishi Gas Chemical Company, Inc.

- Reliance Industries Limited

- SK geo centric Co., Ltd.

- S-Oil Corporation

- TotalEnergies

第七章 市场机会与未来趋势

- 生物基二甲苯产量呈成长趋势

The Xylene Market is expected to register a CAGR of less than 5% during the forecast period.

The COVID-19 pandemic moderately impacted the market. Xylenes are used in paint thinners as solvents. Construction activities were halted globally due to the COVID-19 outbreak. However, the use of face shields, transparent masks, food, and e-commerce packaging increased, thus, enhancing the demand for xylene derivatives, including purified terephthalate acid, dimethyl terephthalate, and polyethylene terephthalate. This factor stimulated the xylene demand. However, the market is projected to grow steadily, owing to growth trends in the end-user industries in 2022.

Key Highlights

- Over the short term, the increasing demand from the rapidly growing end-user industries is driving the market.

- However, the toxic effects of xylenes and increased consumer awareness regarding plastic-free products are expected to hinder the market's growth.

- Nevertheless, cheaper feedstock through shale oil discoveries and a rising trend for the production of bio-based xylene are likely to act as an opportunity during the forecast period.

- Asia-Pacific is estimated to witness healthy growth over the assessment period in the xylene market due to the vast usage of xylene in end-use application segments, such as plastics, polymers, paints and coatings, adhesives, etc., due to their desirable properties.

Xylene Market Trends

Solvent Application to Dominate the Market

- The majority of xylene is used as a solvent for rubber, leather, paints, and printing industries. Other applications of xylene include chemical intermediates and blending agents for high-motor and aviation fuels and breathing devices (inhalers).

- It is very good at dissolving compounds that dissolve poorly in water, owing to its properties and chemical structure. Xylene is volatile, which means it evaporates readily. For this reason, it is used in applications where the manufacturer needs to dissolve a compound but evaporate the solvent.

- It is a good cleaning agent for silicon wafers and steel and is also used to sterilize several substances. Xylene is used as a feedstock in the production of petrol, gasoline, and jet fuel.

- The use of xylene in the paints and coatings sector is increasing due to investments and expansions. For instance, according to the American Coatings Association, the paint and coatings industry in the United States produced around 1.36 billion gallons in 2022. In 2023, the industry's output is expected to exceed 1.38 billion gallons.

- Moreover, according to the American Coatings Association, architectural coatings accounted for 51% of the paint and coatings market value in the United States in 2022. OEM and special purpose coatings held 29 and 20% of the market, respectively. The worth of the US paints and coatings market was approximately USD 31 billion in the same year.

- Thus, due to these factors, the solvents segment of the market may register growth during the forecast period.

China to Dominate the Asia-Pacific Region

- In Asia-Pacific, China includes the biggest production houses in the world. It is also the largest manufacturer and consumer of paraxylene.

- China includes 20 planned and announced xylene capacity additions, with a total capacity of about 24.36 Mtpa by 2025. The country is expected to spend a capital expenditure (CapEx) of USD 10.69 billion. Major capacity additions are expected from Zhejiang Petrochemical Daishan Xylene Plant 2.

- Petrochemical companies in China are massively increasing their PTA capacities. In December 2022, INEOS and SINOPEC formed a joint venture to construct a new petrochemicals complex in Tianjin, China. The agreements will have a combined capacity of 7 million tonnes per year, with a total value of roughly USD 10 billion.

- INEOS agreed to acquire a 50% stake in Shanghai SECCO Petrochemical Company Limited ("SECCO"), a China Petroleum & Chemical Corporation subsidiary. SECCO presently includes a 4.2 million-tonne capacity for petrochemicals such as xylene, toluene, ethylene, propylene, polyethylene, polypropylene, styrene, polystyrene, acrylonitrile, butadiene, and benzene. It is a 200-hectare complex in the Shanghai Chemical Industry Park.

- China is a significant producer of PET resins, with the PetroChina Group and Jiangsu Sangfangxiang among the most prominent global manufacturers in terms of volume, with more than 2 million ton capacity. Thus, the rising demand for PET from end-user industries is driving the demand for paraxylene.

- DuPont decided to invest approximately USD 30 million in building a new manufacturing facility in the adhesive sector in Zhangjiagang, Jiangsu Province, in East China. Construction began in late 2021, and the facility is expected to be operational by early 2023.

- Therefore, the xylene market will likely grow with the increasing investments and demand from end-user industries during the forecast period.

Xylene Industry Overview

The xylene market is fragmented in nature. The major companies (not in any particular order) include Exxon Mobil Corporation, Reliance Industries Limited, INEOS, CNPC (China National Petroleum Corporation), and Mitsubishi Gas Chemical Company, Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage of Xylene as Solvents and Monomers

- 4.1.2 Increasing Demand from the Rapidly Growing End-user Industries

- 4.2 Restraints

- 4.2.1 Toxic Health Effects and Regylations on Usage of Xylenes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Ortho-xylene

- 5.1.2 Meta-xylene

- 5.1.3 Para-xylene

- 5.1.4 Mixed Xylene

- 5.2 Application

- 5.2.1 Solvent

- 5.2.2 Monomer

- 5.2.3 Other Applications

- 5.3 End-user Industry

- 5.3.1 Plastics and Polymers

- 5.3.2 Paints and Coatings

- 5.3.3 Adhesives

- 5.3.4 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Braskem

- 6.4.2 China Petroleum & Chemical Corporation

- 6.4.3 CNPC (China National Petroleum Corporation)

- 6.4.4 ENEOS Corporation

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 Fujan Refining & Petrochemical Company Limited

- 6.4.7 Indian Oil Corporation Ltd

- 6.4.8 INEOS

- 6.4.9 Mangalore Refinery & Petrochemicals Ltd

- 6.4.10 Mitsubishi Gas Chemical Company, Inc.

- 6.4.11 Reliance Industries Limited

- 6.4.12 SK geo centric Co., Ltd.

- 6.4.13 S-Oil Corporation

- 6.4.14 TotalEnergies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Trend for the Production of Bio-based Xylene

全球二甲苯市场:2032 年预测-按类型、配方、应用、最终用户和地区进行分析

全球二甲苯市场:2032 年预测-按类型、配方、应用、最终用户和地区进行分析 2025年全球二甲苯市场报告

2025年全球二甲苯市场报告 混合二甲苯市场报告:趋势、预测和竞争分析(至 2031 年)

混合二甲苯市场报告:趋势、预测和竞争分析(至 2031 年) 2025 年至 2033 年邻二甲苯市场报告(按应用、最终用途和地区)

2025 年至 2033 年邻二甲苯市场报告(按应用、最终用途和地区) 混合二甲苯市场规模、份额和成长分析(按等级、应用、最终用途和地区)- 产业预测 2025-2032

混合二甲苯市场规模、份额和成长分析(按等级、应用、最终用途和地区)- 产业预测 2025-2032 2025 - 2034 年混合二甲苯市场机会、成长动力、产业趋势分析与预测

2025 - 2034 年混合二甲苯市场机会、成长动力、产业趋势分析与预测 二甲苯市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2019-2029F

二甲苯市场 - 全球产业规模、份额、趋势、机会和预测,按类型、应用、地区和竞争细分,2019-2029F 二甲苯市场:按类型、应用和最终用途分类 - 2025-2030 年全球预测

二甲苯市场:按类型、应用和最终用途分类 - 2025-2030 年全球预测 邻二甲苯:市场占有率分析、产业趋势与统计、成长预测(2024-2029)

邻二甲苯:市场占有率分析、产业趋势与统计、成长预测(2024-2029) 邻二甲苯市场 - 2024 年至 2029 年预测

邻二甲苯市场 - 2024 年至 2029 年预测