|

市场调查报告书

商品编码

1640454

VaaS:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)VaaS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

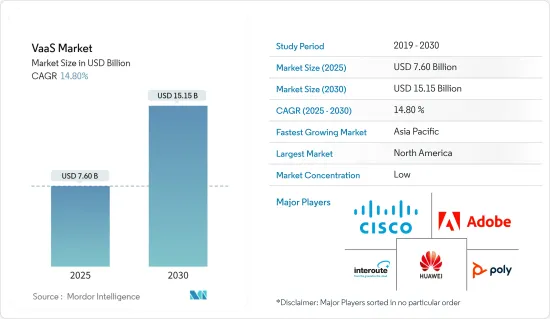

2025 年 VaaS 市场规模估计为 76 亿美元,预计到 2030 年将达到 151.5 亿美元,在市场估计和预测期(2025-2030 年)内以 14.8% 的复合年增长率增长。

视讯即服务 (VaaS) 是一种云端基础的视讯通讯服务,允许用户透过网路进行视讯会议、视讯通话和即时视讯串流。 VaaS 供应商提供必要的基础设施、软体和工具,使企业和个人能够透过视讯进行沟通。

主要亮点

- 由于云端架构提供的扩充性、灵活性和可负担性,需求明显从内部视讯会议 (VC) 和协作解决方案转向基于云端基础的解决方案。云端基础的解决方案的普及正在加速对视讯即服务 (VaaS) 的需求。 VaaS 允许参与者从任何有网路连线的地方进行协作,从而节省时间和旅行费用。 VaaS 还提供会议记录服务,并可协助进行产品演示、财务审查和其他类型的会议。

- VaaS 让参与者轻鬆即时分享和协作文件和简报,从而提高生产力和效率。一些视讯会议解决方案供应商已经实施了不同的经营模式,以更好地服务他们的客户。解决方案提供者专注于提供专门客製化的解决方案来满足多种企业的需求。

- 云端基础的解决方案的使用也在增加,同时也花费大量资金来增加新功能,例如身临其境型远距临场系统、语音和脸部辨识、高清音讯视讯和人工智慧(AI)。随着技术进步、创新和新的 VaaS 解决方案提供商的进入,市场参与者之间的竞争预计将进一步加剧,中小企业希望获得价格合理的云端为基础的协作和VC 解决方案。更容易实现。

- 此外,VaaS 可用于医疗保健领域的多种用途,包括远端医疗服务、远端医疗、视讯咨询和医学教育。视讯会议使医生和医务人员能够与患者即时互动,无论他们身在何处。此外,医务人员可以使用视讯会议接受远端培训并与其他专业人员即时协作,从而提高他们为患者提供的护理品质。

- 市场参与者正在策略性地部署先进的 VaaS 产品,以扩大其影响力并占领市场占有率。例如,国际视讯技术供应商 Pexip 于 2022 年 10 月推出了 Pexip 视讯平台即服务。透过这项服务,该公司希望帮助大型企业创造突破性的新产品,将影片融入其工作流程并进行创新。我们已经推出了VPaaS。 Pexip 的组织结构现在由新的业务部门组成,这些部门在美洲、欧洲、中东和非洲地区以及亚太地区拥有专门的技术和商业资源,以支持公司对影片创新的关注。客户和公民参与、医疗保健以及视讯扩增实境是团队重点关注的三大成长领域。

- 此外,国防领域还有多种视讯即服务应用程式。视讯监控就是其中之一,其中摄影机用于安全目的。此外,政府和国防部门可以使用视讯会议进行沟通和协作。国防部门还可以使用云端服务来储存和存取关键任务资料。此外,军事和国防通讯业还可以利用创新的数位应用和服务。国防工业受到各种宏观经济趋势的影响,包括政府支出、经济成长和全球经济状况。

- 另一方面,高昂的收购和整合成本以及对资料安全和隐私的担忧正在抑制所研究市场的成长。误报是由于设备故障、恶劣的天气或环境条件引起的。由于服务整合度差和系统同步不足,资料安全和隐私问题预计将成为障碍。

视讯即服务 (VaaS) 市场趋势

混合云端领域预计将推动市场需求

- 与其他云端服务相比,混合云近年来整体成长显着。混合云允许企业扩展其运算资源。它还减少了为满足短期需求高峰而投入大量资金的需要,有助于释放本地资源用于敏感资料和应用程式。使用云端服务的企业无需购买、编程和维护多余的资源和设备,而只需为暂时使用的资源付费。这使您可以减少非收益成本。

- 当处理和运算需求波动时,混合云允许公司将其内部基础设施扩展到公有云并溢出,而无需将所有资料暴露给第三方资料中心。事实证明,这些技术创新有助于缓解那些先前由于资料安全问题而不愿迁移到此解决方案的最终用户的担忧。上市公司可以利用公有云的灵活性和运算能力来完成基本的、非敏感的运算任务,同时将业务关键型程式和资料保留在本地并受到公司防火墙的安全保护。为了开发混合云,服务供应商寻求创建共用网路连接的内部私有云端的组合。

- 此外,当使用者希望在一个平台上同时利用私有云端云和公有云解决方案和服务时,混合云是具有成本效益的。此外,混合云使得向多重云端过渡变得更加容易,并且不需要客户在硬体组件上进行额外投资。与私有云端云和公有云不同,混合云的所有控制权仍属于组织,而不是由第三方或供应商管理。这意味着政府机构和银行部门不需要担心其敏感资产和工作负载的安全。

- 安全性已成为混合云发展的关键挑战,近年来该领域的投资呈指数级增长。提供混合云解决方案的公司非常重视安全性。解决方案提供者正在提供全面安全服务,透过提供多层次的安全和监控来满足消费者的需求。例如,McAfee、HP 和 Cisco 正在致力于开发先进的安全系统来保护储存在混合云中的资料。随着市场呈指数级增长以及企业扩展其混合云功能,安全性越来越受到关注。使用者依赖第三方混合云端安全解决方案供应商来进一步增强其功能。

- 据Service Express称,2022年在美国进行的一项民意调查发现,受访的组织的IT基础设施环境平均有48%是内部部署资料中心。公共云端占18%,而主机託管和託管私有云端各占17%。云端运算的大规模采用可能会推动市场参与者在云端部署他们的解决方案。

预计北美将占据最大市场占有率

- 美国是世界上最大的经济体,也是北美视讯即服务(VaaS)的主要市场。灵活性、舒适性、内容个人化、内容多样性和内容量是采用视讯即服务的主要驱动力。随着智慧型手机传输速度大幅提升,我国在从4G转型为5G过程中正在取得初步进展。

- 随着 5G 速度的提升,对更高解析度影片的需求预计也会成长。 5G将实现更快、更可靠的影片串流,同时也有望实现高清影片和XR服务等新型影片服务。此外,5G的引入预计将对企业视讯监控和视讯串流产业产生影响,从而带动互联生态系统的快速成长。 5G 预计将对视讯即服务 (VaaS) 市场产生重大影响,为消费者带来新服务和改善体验。

- 此外,由于许多企业突然转向在家工作文化,Zoom、Microsoft Teams 和 Google Workspace 的视讯软体和服务的需求都激增。积极使用这些网站的人数已显着增加。根据报道,2022 年 1 月,Microsoft Teams 的每月有效用户数为 2.7 亿,比 2021 年 7 月增加了 2,000 万。

- 该地区的主要行业参与者正在不断增强其产品供应,以保持竞争力并满足最终用户不断变化的需求。为了实现这一目标,我们将 VaaS 与 AI、深度学习和机器学习等先进技术结合。此外,VaaS 市场参与者正在采用先进的基于 AI 的 VaaS,以提供一种自足式的方式即时监控和增强视讯内容服务。

- 例如,美国通讯技术公司 Zoom Video Communications 最近宣布,将在其视讯即服务产品中添加端到端加密功能,该产品目前已向全球免费和付费用户提供。此外,将这些先进技术整合到 VaaS 中有望显着提高准确性并减少误报。预计这些因素将在未来几年为该行业创造新的机会。

- 2023 年 3 月,亚马逊网路服务 (AWS) 宣布推出亚马逊互动视讯服务 (Amazon IVS),这是一种託管直播解决方案,可协助开发人员创建互动视讯体验。如今,开发人员正在使用 Amazon IVS 为社交网路、电子商务和健身等各行各业创建应用程式。自从 Amazon IVS 推出以来,协作直播已经成为显着的趋势。 Twitch 等公司推出了 Guest Star 之类的工具,让主播能够让观众沉浸在他们的直播视讯节目中,从而使节目更加精彩、互动性更强。

视讯即服务 (VaaS) 产业概览

视讯即服务 (VaaS) 市场呈现分散化,全球参与者正在创新其服务,为用户提供具有成本效益的服务,从而为市场竞争对手提供较高的竞争优势。主要参与者包括Cisco、华为技术、Adobe 系统和 Polycom。近期市场发展有何趋势?

- 2022年7月,浙江行动、精优科技、华为联合发布全新呼叫解决方案New Calling。解决方案采用「1个平台+3个功能+N个服务」的架构模式,重新定义现有的呼叫服务,为个人用户和企业客户提供卓越的语音和视讯通话品质。 New Calling系统透过在核心语音网路上建构New Calling平台和统一媒体功能,实现超高清视讯通话、智慧视讯通话、互动式视讯呼叫三种互相竞争的通话功能。

- 2022年3月-行动互联网通讯、企业和消费者技术解决方案的全球主要供应商中兴通讯股份有限公司宣布首次推出其优质视讯平台2.0(PVP2.0)大视讯解决方案。 「新生态」PVP2.0解决方案可以提供以营运商为中心的ATV启动器,让营运商可以根据需要采用自己喜欢的服务展示风格。营运商可以快速且有效率地整合第三方功能和应用程序,例如 Google Assistant 和 Google Ads。在融合视讯平台的支援下,营运商可以将服务拓展到更多新市场,并创造商业伙伴关係机会。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 购买者/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争强度

- 评估宏观经济趋势对市场的影响

第五章 市场动态

- 市场驱动因素

- 增加对云端基础的视讯服务的投资

- 赋能数位化劳动力

- 市场限制

- 製作和检验影片内容的高成本

第六章 市场细分

- 按平台

- 应用程式管理

- 设备管理

- 网管

- 按设备

- 行动装置

- 企业运算

- 按服务

- 託管

- 专业的

- 按部署模型

- 公有云

- 私有云端

- 混合云

- 按最终用户产业

- 政府和国防

- BFSI

- 卫生保健

- 资讯科技/通讯

- 媒体与娱乐

- 製造业

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚洲

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- Cisco Systems, Inc.

- Huawei Technologies Co., Limited

- Adobe Systems

- Interoute Communications Limited

- Polycom, Inc.

- Avaya, Inc.

- Vidyo, Inc.

- BlueJeans Network

- Applied Global Technologies, LLC

- AVI-SPL, Inc.

第八章投资分析

第九章 市场机会与未来趋势

The VaaS Market size is estimated at USD 7.60 billion in 2025, and is expected to reach USD 15.15 billion by 2030, at a CAGR of 14.8% during the forecast period (2025-2030).

Video as a Service (VaaS) is a cloud-based video communication service that allows users to conduct video conferences, video calls, and live video streaming over the Internet. VaaS providers offer the necessary infrastructure, software, and tools to enable businesses and individuals to communicate through video.

Key Highlights

- Due to the high scalability, flexibility, and affordability provided by the cloud architecture, there is a discernible movement in demand away from on-premises video conferencing (VC) and collaboration solutions to cloud-based solutions. The popularity of cloud-based solutions has accelerated the demand for video as a service (VaaS). It saves time and travel expenses, as participants can collaborate from anywhere with an Internet connection. It also provides meeting transcription services, which can assist with product presentations, financial reviews, and other types of meetings.

- VaaS enhances productivity and efficiency, as participants can easily share and collaborate on documents and presentations in real time. Several video conferencing solutions vendors have implemented various business models to better serve their clients. Solution providers are putting their efforts into providing solutions specifically tailored to satisfy the needs of multiple enterprises.

- The use of cloud-based solutions is also increasing, as are the expenditures made to add new capabilities like immersive telepresence, voice and face recognition, HD audio and video, and artificial intelligence (AI). There will likely be more competition among the market players due to advancements in technology, innovations, and the entry of new VaaS solution providers, which would facilitate small and medium businesses to utilize affordable hybrid cloud-based collaboration and VC solutions.

- Further, VaaS can have various uses in the healthcare sector, such as remote healthcare services, telemedicine, video consultations, medical education, etc. With video conferencing, physicians and medical staff can interact with patients in real time, regardless of their physical location, which can be beneficial for patients who may have difficulty traveling. Additionally, medical staff can receive remote training and collaborate with other professionals in real time using video conferencing, which can improve the quality of care provided to patients.

- The market players are strategically deploying advanced VaaS to expand their presence and capture the market share. For instance, in October 2022, Pexip, an international provider of video technology, launched Pexip's Video Platform as a Service. With the service, the company hopes to empower big businesses to create innovative new products, incorporate video into workflows, and innovate. (VPaaS). Pexip's organizational structure, which currently comprises a new business unit with dedicated technical and commercial resources throughout the Americas, EMEA, and APAC, supports the company's focus on video innovation. Customer and citizen engagement, healthcare, and video-enabled extended reality are claimed to be the three major growth areas that this team is focusing on.

- Additionally, there are several uses of video as a service in the defense sector. Video surveillance is one such use, where cameras are used for security purposes. Additionally, video conferencing can be used by the government and defense sector for communication and collaboration. The defense sector can also use cloud services to store and access mission-critical data. Furthermore, innovative digital applications and services can be leveraged by the military and defense communication industry. The defense sector is influenced by various macroeconomic trends such as government spending, economic growth, and global economic conditions.

- On the other side, high acquisition and integration costs and data security and privacy concerns restrain the growth of the studied market. Several false alarms are triggered as a result of malfunctioning equipment and unfavorable weather or environmental conditions. Data security and privacy issues are anticipated to be a roadblock due to the service's poor integration or lack of system synchronization.

Video as a Service Market Trends

The Hybrid Cloud Segment is Anticipated to Drive the Market Demand

- The hybrid cloud has seen significant overall growth in recent years compared to other cloud services, as it provides several benefits to organizations with large data volumes. Companies can scale computing resources by using a hybrid cloud. It also reduces the need to invest large sums of money to handle short-term surges in demand, which is useful when the company has to free up local resources for sensitive data or applications. Companies that use cloud services must pay only for the resources they use momentarily rather than purchasing, programming, and maintaining extra resources and equipment that sit dormant for long periods. This assists businesses in reducing costs that do not generate revenue.

- When processing and computing demand fluctuates, hybrid cloud computing enables businesses to scale out their on-premises infrastructure to the public cloud to address any overflow without exposing all of their data to third-party data centers. These innovations have proved beneficial in addressing the worries of end-users who were previously unwilling to migrate to this solution due to concerns about data security. Organizations benefit from the public cloud's flexibility and computing capacity for basic and non-sensitive computing tasks while keeping business-critical programs and data on-premises and secure behind a company firewall. To develop a hybrid cloud, service providers strive to create a combination of on-premise private cloud and public cloud that share a network connection.

- Further, a hybrid cloud is cost-effective when the user wishes to use both private and public cloud solutions or services on a single platform. In addition, the hybrid cloud allows an easy transition to the multi-cloud and does not require the customers to invest in an additional hardware component. Unlike private and public clouds, in the hybrid cloud, all the control is given to the organization and is not managed by a third party or the provider. Therefore, government organizations and banking sectors need not worry about the security of sensitive assets or workloads.

- The investment in this space has also grown exponentially over the past few years, as security is becoming one of the significant challenges for the growth of the technology. Companies offering hybrid cloud solutions are focusing heavily on security. Solution providers are offering integrated security services to cater to the consumer's requirements by providing multilayer security and monitoring. For example, McAfee, HP, and Cisco are working towards the development of high-level security systems to protect the data stored on hybrid clouds. With the market size growing significantly and companies expanding their hybrid cloud capabilities, the focus on security is increasing. Users rely on third-party hybrid cloud security solution providers to improve their abilities further.

- According to Service Express, an average of 48% of surveyed organizations' IT infrastructure environments were on-premises data centers, according to a 2022 poll in the United States. The public cloud accounted for 18%, while colocation and hosted private cloud both accounted for 17%. Such massive usage of the cloud would push the market players to deploy their solutions to the cloud.

North America is Anticipated to Hold the Largest Market Share

- The United States is the largest economy in the world and has been a significant market for Video as a Service in the North America region. The flexibility, comfort, content personalization, availability of diverse content, and content volume have primarily driven the adoption of Video as a Service. With smartphone transmission speeds increasing dramatically, the country is witnessing an early transition from 4G to 5G.

- With increased rates of 5G, higher-resolution videos are expected to witness an uptick in demand. It is expected that 5G will enable faster and more reliable video streaming, as well as new video services such as HD video and XR services. Moreover, the introduction of 5G is anticipated to affect video surveillance for businesses and the video streaming industry, leading to rapid growth in the connected ecosystem. 5G would have a significant impact on the Video as a Service market, allowing for new and improved services and experiences for consumers.

- Further, Zoom, Microsoft Teams, and Google Workspace have all seen a spike in demand for video software and services as a result of the abrupt shift of many firms to a work-from-home culture. The number of individuals who are actively using these sites is significantly increasing. Microsoft Teams reported 270 million monthly active users in January 2022, an increase of 20 million from July 2021.

- Major industry players in the region are constantly enhancing their product offerings to maintain a competitive edge and suit the evolving needs of end customers. Therefore, they combine VaaS with advanced technologies like AI, deep learning, and machine learning. Additionally, VaaS market players embrace advanced AI-based VaaS to offer a self-contained way to monitor and enhance video content services in real time.

- For instance, the American company Zoom Video Communications, Inc., which develops communications technology, recently announced the addition of end-to-end encryption capabilities to its already-available video-as-a-service offerings for free and premium users worldwide. Additionally, integrating these sophisticated technologies into VaaS can lead to significant improvements in accuracy and a decrease in false alarms. These factors are anticipated to present new chances for the industry in the coming years.

- In March 2023, Amazon Interactive Video Service (Amazon IVS), a managed live streaming solution enabling developers to create interactive video experiences, was introduced by Amazon Web Services (AWS). Currently, developers create apps for various industries, such as social networking, e-commerce, and fitness, using Amazon IVS. Since the introduction of the Amazon IVS, collaborative live streaming has been a significant trend. Companies like Twitch have introduced tools like Guest Star that let streamers draw viewers into live video shows, resulting in more exciting and interactive programming.

Video as a Service Industry Overview

The video as a service market is fragmented as the global players are innovating their services to provide cost-benefit offers to the users, which gives a high rivalry to the market competitors. Key players are Cisco Systems, Inc., Huawei Technologies Co., Adobe Systems, Polycom, Inc., etc. Recent developments in the market are -

- July 2022 - New Calling, a brand-new calling solution, was jointly launched by Zhejiang Mobile, Jingyou Technology, and Huawei. To redefine current call services and offer great audio and video call quality to individual users as well as business customers, this solution uses the "1 platform + 3 capabilities + N services" architectural model. The New Calling system allows three competitive calling capabilities-UHD video calling, intelligent video calling, and interactive video calling-by creating the New Calling Platform and Unified Media Function on top of the core voice network.

- March 2022 - ZTE Corporation, a significant global supplier of telecommunications, enterprise, and customer technology solutions for the mobile internet, announced the debut of its Premium Video Platform 2.0 (PVP2.0) big video solution. The PVP2.0 solution for "New Ecosystem" can offer an operator-centric ATV launcher, allowing operators to adopt their preferred service display styles as necessary. Operators can rapidly and efficiently incorporate third-party features and apps like Google Assistant and Google Ads. With the support of a converged video platform, it enables operators to expand their service into more new markets, creating opportunities for business partnerships.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Investment on Cloud-Based Video Services

- 5.1.2 Enabling Digital Workforce

- 5.2 Market Restraints

- 5.2.1 High Cost of Video Content Creation and Validity

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 Application Management

- 6.1.2 Device Management

- 6.1.3 Network Management

- 6.2 By Device

- 6.2.1 Mobility Devices

- 6.2.2 Enterprise Computing

- 6.3 By Service

- 6.3.1 Managed

- 6.3.2 Professional

- 6.4 By Deployment Model

- 6.4.1 Public Cloud

- 6.4.2 Private Cloud

- 6.4.3 Hybrid Cloud

- 6.5 By End-user Industry

- 6.5.1 Government and Defense

- 6.5.2 BFSI

- 6.5.3 Healthcare

- 6.5.4 IT & Telecom

- 6.5.5 Media & Entertainment

- 6.5.6 Manufacturing

- 6.5.7 Other End-user Industries

- 6.6 Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia

- 6.6.4 Latin America

- 6.6.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems, Inc.

- 7.1.2 Huawei Technologies Co., Limited

- 7.1.3 Adobe Systems

- 7.1.4 Interoute Communications Limited

- 7.1.5 Polycom, Inc.

- 7.1.6 Avaya, Inc.

- 7.1.7 Vidyo, Inc.

- 7.1.8 BlueJeans Network

- 7.1.9 Applied Global Technologies, LLC

- 7.1.10 AVI-SPL, Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2025年视讯即服务(VaaS)全球市场报告

2025年视讯即服务(VaaS)全球市场报告 2025-2029 年全球视讯即服务市场

2025-2029 年全球视讯即服务市场 全球视讯即服务市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球视讯即服务市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 视讯即服务市场-全球产业规模、份额、趋势、机会与预测(按应用程式、按云端部署模式、按垂直产业、按地区、按竞争细分,2020-2030 年)

视讯即服务市场-全球产业规模、份额、趋势、机会与预测(按应用程式、按云端部署模式、按垂直产业、按地区、按竞争细分,2020-2030 年) 视讯即服务市场规模、份额及成长分析(按应用、部署、垂直领域和地区)-2025 年至 2032 年产业预测

视讯即服务市场规模、份额及成长分析(按应用、部署、垂直领域和地区)-2025 年至 2032 年产业预测 VaaS(视讯即服务)市场规模、份额、趋势分析报告:按应用程式、云端部署模式、产业、地区和细分市场预测,2025-2030 年

VaaS(视讯即服务)市场规模、份额、趋势分析报告:按应用程式、云端部署模式、产业、地区和细分市场预测,2025-2030 年 视讯即服务市场:按元件、应用程式、云端部署模式和产业划分 - 2025-2030 年全球预测

视讯即服务市场:按元件、应用程式、云端部署模式和产业划分 - 2025-2030 年全球预测 亚太地区视讯即服务市场预测至 2030 年 - 区域分析 - 按部署模式和产业垂直

亚太地区视讯即服务市场预测至 2030 年 - 区域分析 - 按部署模式和产业垂直 北美视讯即服务市场预测至 2030 年 - 区域分析 - 按部署模式和产业垂直

北美视讯即服务市场预测至 2030 年 - 区域分析 - 按部署模式和产业垂直 欧洲视讯即服务市场预测至 2030 年 - 区域分析 - 按部署模式和产业垂直

欧洲视讯即服务市场预测至 2030 年 - 区域分析 - 按部署模式和产业垂直