|

市场调查报告书

商品编码

1640544

中国玻璃包装:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)China Glass Container Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

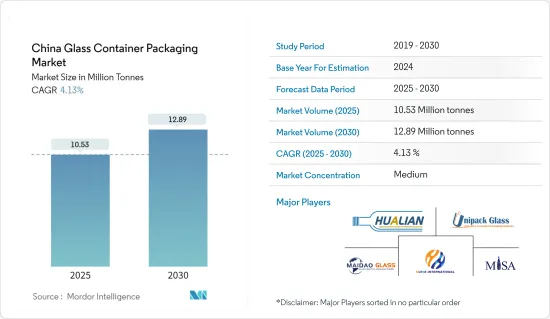

2025年中国玻璃容器包装市场规模预估为1,053万吨,预估2030年将达1,289万吨,预测期(2025-2030年)复合年增长率为4.13%。

主要亮点

- 玻璃已成为包装行业的主要组成部分,对玻璃容器市场的成长产生了重大影响。玻璃容器主要用于食品和饮料领域的储存,具有耐用性、强度以及能够保持口感和风味等优点。这些属性使得玻璃容器特别适合需要长保质期或对外部因素敏感的产品。

- 玻璃具有100%可回收的特性,在全球市场向环保包装解决方案转变的背景下,玻璃的永续性为中国的容器玻璃产业提供了良好的发展条件。这种可回收性不仅减少了废弃物,而且还减少了生产对原材料的需求。中国成熟的玻璃产业完全有能力满足日益增长的对塑胶包装永续替代品的需求。

主要亮点

- 根据世界主要出口商(WTEx)的数据,2023年,中国以约260亿美元的玻璃出口领先全球。这一出口领先地位彰显了中国在全球玻璃容器市场的重要角色及其影响产业趋势的潜力。

- 酒精饮料经常使用玻璃包装,因为其非反应特性可以保留饮料的香气、浓度和风味。这种偏好在啤酒行业尤其明显,因为大多数啤酒都是用玻璃容器运输的。玻璃的惰性确保不会有化学物质渗入饮料中,从而长期保持饮料的品质。

主要亮点

- 根据东北银行的报告,预计2023年中国年酒精饮料消费量将达到约516亿公升。如此庞大的消费量凸显了玻璃容器等可靠包装解决方案在酒精饮料产业的重要性。

- 啤酒消费量的增加也是推动市场成长的因素。啤酒通常装在深色玻璃瓶中,以防止内容物因紫外线而变质。深色玻璃起到屏障的作用,防止光线引起化学反应,从而改变啤酒的味道和品质。玻璃包装的这种保护功能对于在储存和运输过程中保持光敏饮料的完整性至关重要。

- 受原物料价格波动影响,中国玻璃包装市场面临挑战。占玻璃容器製造总原料成本50%以上的碱灰成本一直在稳定上涨。这一趋势可能会导致 PET 和生质塑胶等替代包装材料的采用增加。然而,玻璃产业正在探索缓解这些挑战的方法,包括提高生产效率、开发新的玻璃配方和投资回收基础设施以减少对原材料的依赖。

- 儘管面临这些挑战,中国的玻璃容器市场仍在不断发展。製造商正在投资先进技术来生产更轻、更坚固的玻璃容器,以保持材料固有的优势,同时解决对重量和运输成本的担忧。此外,化妆品和烈酒等各行业对高端和奢华包装的日益重视,为高品质玻璃包装产品创造了新的机会。

中国容器玻璃市场趋势

酒精饮料占了很大的市场占有率

- 玻璃已成为酒精饮料行业的有效包装选择。玻璃容器可保护内容物免受光、温度变化和空气暴露等外部因素的影响,从而确保产品品质。这种保存能力对于对环境变化敏感的酒精饮料尤其重要。

- 随着消费者越来越多地寻求环保解决方案,玻璃包装提供了完全可回收的塑胶替代品。玻璃是100%可回收的,可以重复使用而不会造成任何品质损失,这使其成为有环保意识的消费者和企业的永续选择。

- 中国都市区的酒精和非酒精饮料消费量正在增加。这一趋势是由可支配收入的增加、生活方式的改变以及对多样化饮料选择的日益欣赏所推动的。

- 具有历史根源的酒精饮料包括米酒、葡萄酒、啤酒、威士忌和各种蒸馏酒。每个类别都有其自身的文化意义和市场动态。白酒是一种中国传统蒸馏酒,是中国消费量最大的烈酒,体现了其持久的文化重要性和广泛的受欢迎程度。

- 根据港交所新闻报道,2021年,浓香型白酒销售额约2,860亿元(404.2亿美元),占中国白酒销售额的一半以上。如此大的市场占有率证实了这种特殊风味在中国消费者中的受欢迎程度。预计到 2026 年浓香型白酒销售额将达到 3,129 亿元(442.2 亿美元),显示白酒市场这一领域将稳定成长。

- 具有历史根源的酒精饮料包括米酒、葡萄酒、啤酒、威士忌和各种蒸馏酒。每个类别都有其自身的文化意义和市场动态。白酒是一种中国传统蒸馏酒,是中国消费量最大的烈酒,体现了其持久的文化重要性和广泛的受欢迎程度。

- 由于铝罐越来越受欢迎,玻璃包装的成长速度比啤酒包装慢。这种变化是由于罐头更轻、运输和储存更容易以及消费者偏好改变等因素造成的。十多年来,中国金属饮料罐市场一直以铝罐为主,铝罐在生产效率、成本效益上具有优势。

- 然而,玻璃瓶预计将保持相当大的市场占有率,特别是在高级啤酒和精酿啤酒领域。

- 根据联合国商品贸易统计资料库,2023年中国啤酒出口额将约为4.5176亿美元,高于2022年的约3.2712亿美元。出口量的大幅增长表明国际上对中国啤酒的需求不断增长。随着啤酒出口的增加,酿酒商可能会增加生产能力,这可能会导致对玻璃包装的需求增加。

- 这一趋势可能会鼓励容器玻璃製造商扩大生产能力以满足日益增长的市场需求。产能扩张可能涉及投资新製造设施、实施先进技术以及开发创新玻璃包装解决方案,以满足国内外市场不断变化的消费者偏好。

化妆品:有望实现巨大成长的市场

- 消费者在美容产品上的支出增加,推动品牌扩大其产品范围、创新并推出新产品。玻璃具有高度可客製化,并且是创新、美观的化妆品包装的首选,因此需求不断增长。这一趋势鼓励玻璃容器製造商投资新设计、新材料和新技术,从而扩大市场。

- 根据中国国家统计局的报告,2022年中国人均化妆品年度总支出约407元人民币(57.5美元)。预计到2025年,这数字将达到600元人民币(84.8美元),超过中国居民可支配所得的成长速度。

- 人均化妆品支出的增加预计将推动中国电子商务产业的扩张并促进化妆品出口。玻璃容器因其耐用性和高檔外观而受到青睐,在全球市场和电子商务平台的包装产品中发挥越来越重要的作用,从而进一步加强了容器玻璃市场。

- 许多化妆品,包括香水、护肤霜、精华液和奢侈化妆品,都采用玻璃容器包装,以彰显其奢华、耐用和免受污染的特点。化妆品行业的扩张带动了玻璃容器需求的增加,利好容器玻璃市场。

- 根据中国国家统计局的资料,预计2023年中国化妆品零售额将达到约585.4亿美元,高于2022年的556.3亿美元。

- 随着消费者越来越追求高端、奢华的化妆品,品牌纷纷选择玻璃包装来提升产品展示效果和感知价值。化妆品市场优质化的趋势推动了对高品质和独特设计玻璃包装的需求。

中国玻璃容器市场概况

中国玻璃容器包装市场正趋于半固体,众多参与者进入市场并占有相当大的市场占有率。参与的人员如下:麦道实业、上海维斯塔包装、上海米莎玻璃等企业正专注于创新和建立战略合作伙伴关係以维持其市场份额,并进行产能扩张、合併、收购和合作。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 容器玻璃进出口资料

- 容器玻璃市场的PESTEL分析

- 玻璃包装行业标准和法规

- 包装玻璃的原料分析及材料考量

- 玻璃包装的永续性趋势

- 容器玻璃熔炉及位置

第五章 市场动态

- 市场驱动因素

- 增加可支配收入并融入高端包装

- 改进技术以提供更好的解决方案

- 市场挑战

- 生产过程中的健康问题可能会抑制市场成长

- 贸易概况-中国容器玻璃产业过去与现在进出口模式分析

第六章 市场细分

- 按最终用户产业

- 饮料

- 酒精饮料(葡萄酒、烈酒、啤酒、苹果酒)

- 非酒精饮料(碳酸饮料、果汁、水、乳类饮料、调味饮料等)

- 食物

- 化妆品

- 药品(不含管瓶和安瓿瓶)

- 其他最终用户领域(例如消费应用)

- 饮料

第七章 竞争格局

- 公司简介

- Maidao Industry Co. Ltd

- Shanghai Vista Packaging Co., Ltd

- ShangHai Misa Glass Co., Ltd

- Xuzhou Huihe International Trade Co., Ltd

- Jiangsu Rongtai Glass Products Co., Ltd

- Unipack Glass

- Hualian Glass Manufacturers Co., Ltd

- Chongqing Hechuan Jinxing Glass Products Co., Ltd

- DANFA GLASS LIMITED

- Zhangjiagang Guochao Glassware Co., Ltd

第 8 章 附加覆盖范围-该地区主要玻璃容器玻璃厂的主要窑炉供应商的分析

第九章:未来市场展望

The China Glass Container Packaging Market size is estimated at 10.53 million tonnes in 2025, and is expected to reach 12.89 million tonnes by 2030, at a CAGR of 4.13% during the forecast period (2025-2030).

Key Highlights

- Glass has become a key component in the packaging industry, significantly influencing the growth of the glass container market. Primarily used for storage in the food and beverage sector, glass containers offer advantages such as durability, strength, and the ability to preserve taste and flavor. These qualities make glass containers particularly suitable for products that require long shelf life or are sensitive to external factors.

- Glass's sustainability, being 100% recyclable, positions China's container glass sector favorably as global markets shift towards environmentally friendly packaging solutions. This recyclability not only reduces waste but also decreases the need for raw materials in production. China's established glass industry can meet the increasing demand for sustainable alternatives to plastic packaging.

- In 2023, China led global glass exports with a value of nearly USD 26 billion, according to the World's Top Exports (WTEx). This leadership in exports demonstrates China's significant role in the global glass container market and its potential to influence industry trends.

- Alcoholic drinks frequently use glass packaging due to its non-reactive properties, which preserve beverages' aroma, strength, and flavor. This preference is particularly evident in the beer industry, where most volume is transported in glass containers. The inert nature of glass ensures that no chemicals leach into the beverage, maintaining its quality over time.

- Banco do Nordeste reports that China's annual consumption of alcoholic beverages is expected to reach approximately 51.6 billion liters in 2023. This substantial consumption volume underscores the importance of reliable packaging solutions like glass containers in the alcoholic beverage industry.

- The increase in beer consumption is another factor driving market growth. Beer is typically packed in dark-colored glass bottles to protect the contents from UV light-induced spoilage. The dark glass acts as a barrier, preventing light from causing chemical reactions that can alter the beer's taste and quality. This protective feature of glass packaging is crucial for maintaining the integrity of light-sensitive beverages during storage and transportation.

- The China glass container packaging market faces challenges due to fluctuating raw material prices. The cost of soda ash, which comprises more than 50% of the overall raw material cost for glass container production, has been steadily increasing. This trend may lead to increased adoption of alternative packaging materials such as PET and bioplastics. However, the glass industry is exploring ways to mitigate these challenges, including improving production efficiency, developing new glass formulations, and investing in recycling infrastructure to reduce reliance on raw materials.

- Despite these challenges, the glass container market in China continues to evolve. Manufacturers are investing in advanced technologies to produce lighter, stronger glass containers that maintain the material's inherent benefits while addressing concerns about weight and transportation costs. Additionally, the growing emphasis on premium and luxury packaging in various sectors, including cosmetics and spirits, is creating new opportunities for high-quality glass container products.

Key Highlights

Key Highlights

China Container Glass Market Trends

Alcoholic Segment to Hold Significant Market Share

- Glass has emerged as an effective packaging option for the alcohol beverage industry. Glass containers maintain product quality by protecting contents from external factors such as light, temperature fluctuations, and air exposure. This preservation capability is particularly crucial for alcoholic beverages, which can be sensitive to environmental changes.

- As consumers increasingly seek eco-friendly solutions, glass packaging offers a fully recyclable alternative to plastic. Glass can be 100% recycled and reused without quality loss, making it a sustainable choice for environmentally conscious consumers and businesses alike.

- Major urban areas in China have experienced increased consumption of both alcoholic and non-alcoholic beverages. This trend is driven by factors such as rising disposable incomes, changing lifestyles, and a growing appreciation for diverse beverage options.

- Alcoholic beverages with historical roots include rice wine, grape wine, beer, whiskey, and various spirits. Each of these categories has its own cultural significance and market dynamics. Baijiu, a traditional Chinese spirit, remains the most consumed distilled spirit in China, reflecting its deep-rooted cultural importance and widespread popularity.

- According to HKEXnews, in 2021, Nongxiang flavor baijiu generated revenue of approximately CNY 286 billion (USD 40.42 billion), accounting for over half of China's baijiu sales revenue. This significant market share underscores the popularity of this particular flavor profile among Chinese consumers. The revenue from Nongxiang flavor baijiu is projected to reach CNY 312.9 billion (USD 44.22 billion) by 2026, indicating a steady growth trajectory for this segment of the baijiu market.

- Glass packaging has experienced slower growth than beer packaging due to the increasing popularity of aluminum cans. This shift is attributed to factors such as the lighter weight of cans, their convenience for transportation and storage, and changing consumer preferences. For over a decade, aluminum has dominated the metal can market for beverages in China, offering advantages in terms of production efficiency and cost-effectiveness.

- However, glass bottles are expected to maintain a significant market share, particularly in premium and craft beer segments, where glass packaging is often associated with higher quality and better taste preservation.

- According to UN Comtrade, in 2023, China exported beer worth approximately USD 451.76 million, up from around USD 327.12 million in 2022. This substantial increase in export value indicates growing international demand for Chinese beer. As beer exports grow, breweries may increase their production capacity, potentially leading to greater demand for glass packaging.

- This trend could encourage container glass companies to expand their production capabilities to meet the growing market needs. The expansion may involve investments in new manufacturing facilities, adoption of advanced technologies, and development of innovative glass packaging solutions to cater to evolving consumer preferences and regulatory requirements in both domestic and international markets.

Cosmetics Expected to Witness Major Growth

- Increased consumer spending on cosmetics prompts brands to expand product ranges, innovate, and launch new lines. Glass, being highly customizable and preferred for packaging innovative and aesthetically appealing cosmetic products, is experiencing growing demand. This trend encourages container glass manufacturers to invest in new designs, materials, and technologies, thereby expanding the market.

- The National Bureau of Statistics of China reports that in 2022, the total per capita annual spending on cosmetics in China was approximately CNY 407 (USD 57.5). This figure is projected to reach CNY 600 (USD 84.8) by 2025, outpacing the growth of per capita disposable income in China.

- The increase in per capita cosmetics spending is expected to drive the expansion of China's e-commerce sector and boost cosmetic product exports. Glass containers, valued for their durability and premium appearance, are becoming increasingly important for packaging products destined for global markets and e-commerce platforms, further strengthening the container glass market.

- Many cosmetic products, including perfumes, skincare creams, serums, and luxury makeup, are packaged in glass containers due to their premium appeal, durability, and protection from contaminants. The expansion of the cosmetics industry is leading to a corresponding increase in demand for glass containers, benefiting the container glass market.

- Data from the National Bureau of Statistics of China shows that retail cosmetics sales in China reached approximately USD 58.54 billion in 2023, an increase from USD 55.63 billion in 2022.

- As consumers increasingly seek high-end and luxury cosmetic products, brands are opting for glass packaging to enhance product presentation and perceived value. This trend towards premiumization in the cosmetics market is driving demand for high-quality and uniquely designed glass packaging.

China Container Glass Market Industry Overview

The China container glass packaging market is semi-consolidated, with many players operating in the market with considerable market share. The players such as Maidao Industry Co. Ltd, Shanghai Vista Packaging Co., Ltd., ShangHai Misa Glass Co., Ltd, and others are focusing on innovating and entering into strategic partnerships in order to retain their market share and undergoing capacity expansion, mergers, acquisitions, and collaboration.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 PESTEL Analysis of Container Glass Market

- 4.4 Industry Standard and Regulation for Container Glass Use for Packaging

- 4.5 Raw Material Analysis and Material Consideration for Packaging

- 4.6 Sustainability Trends for Glass Packaging

- 4.7 Container Glass Furnace and Location

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Higher Disposable Income and Integration in Premium Packaging

- 5.1.2 Improved Technology Offering Better Solutions

- 5.2 Market Challenges

- 5.2.1 Health Concerns Involved During Manufacturing may Restrain the Market Growth

- 5.3 Trade Scenerio - Analysis of the Historical and Current Export Import Paradigm for Container Glass Industry in China

6 MARKET SEGMENTATION

- 6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic (Wines and Spirits, Beer, and Cider)

- 6.1.1.2 Non-alcoholic (Carbonated Drinks, Juices, Water, Dairy-based, Flavored Drinks, etc.)

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical (Excluding Vials and Ampoules)

- 6.1.5 Other End-User Vertical (Consumer Applications, etc.)

- 6.1.1 Bevarages

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Maidao Industry Co. Ltd

- 7.1.2 Shanghai Vista Packaging Co., Ltd

- 7.1.3 ShangHai Misa Glass Co., Ltd

- 7.1.4 Xuzhou Huihe International Trade Co., Ltd

- 7.1.5 Jiangsu Rongtai Glass Products Co., Ltd

- 7.1.6 Unipack Glass

- 7.1.7 Hualian Glass Manufacturers Co., Ltd

- 7.1.8 Chongqing Hechuan Jinxing Glass Products Co., Ltd

- 7.1.9 DANFA GLASS LIMITED

- 7.1.10 Zhangjiagang Guochao Glassware Co., Ltd

8 SUPPLEMENTARY COVERAGE - ANALYSIS OF MAJOR FURNACE SUPPLIERS TO MAJOR CONTAINER GLASS PLANTS IN THE REGION

9 FUTURE OUTLOOK OF THE MARKET

復古包装市场:按材料、类型、最终用途、印刷技术和通路-2026-2032年全球预测纸质復古包装市场:依材料、包装类型、销售管道、最终用户、应用程式划分,全球预测(2026-2032)多功能零件市场按产品类型、价格范围、应用、垂直产业和分销管道划分,全球预测(2026-2032年)纸塑包装器材市场:依机器类型、材料、操作类型和应用划分,全球预测(2026-2032年)全球电子顺磁共振波谱仪市场(按产品类型、频率、工作模式、组件、应用和最终用户划分)预测(2026-2032年)按包装类型、材料、最终用途、分销管道和应用分類的常温纸盒市场—全球预测,2026-2032年

復古包装市场:按材料、类型、最终用途、印刷技术和通路-2026-2032年全球预测纸质復古包装市场:依材料、包装类型、销售管道、最终用户、应用程式划分,全球预测(2026-2032)多功能零件市场按产品类型、价格范围、应用、垂直产业和分销管道划分,全球预测(2026-2032年)纸塑包装器材市场:依机器类型、材料、操作类型和应用划分,全球预测(2026-2032年)全球电子顺磁共振波谱仪市场(按产品类型、频率、工作模式、组件、应用和最终用户划分)预测(2026-2032年)按包装类型、材料、最终用途、分销管道和应用分類的常温纸盒市场—全球预测,2026-2032年 新加坡包装市场

新加坡包装市场 包装市场分析及预测(至2035年):类型、产品类型、材料类型、技术、应用、最终用户、功能、服务、流程、解决方案

包装市场分析及预测(至2035年):类型、产品类型、材料类型、技术、应用、最终用户、功能、服务、流程、解决方案 化妆品和香水玻璃瓶包装:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)英国包装业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

化妆品和香水玻璃瓶包装:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)英国包装业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)