|

市场调查报告书

商品编码

1640656

拉丁美洲软包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)Latin America Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

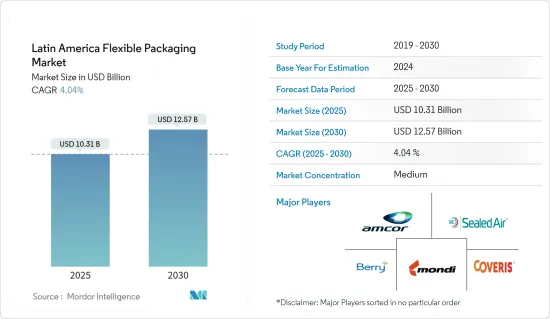

预计 2025 年拉丁美洲软包装市场规模为 103.1 亿美元,预计到 2030 年将达到 125.7 亿美元,预测期内(2025-2030 年)的复合年增长率为 4.04%。

关键亮点

- 软包装生产时消耗的原料和能源较少,因此製造商可节省大量成本。高效的包装功能和减少的储存空间将进一步提升其在市场的需求。

- 创新包装和数位印刷等趋势正在推动市场发展并预示着技术进步。其中包括序列化二维码等富有创意的消费者参与解决方案。软包装重量也更轻,降低了运输成本和燃料使用量,因此在研究区域中成为包装零嘴零食和薯片的首选。

- 为了满足日益增长的需求,一些市场参与企业正在建立联盟和伙伴关係关係,以提高收益。例如,2024年5月,巴西SGK团队与强生巴西合作推出SEMPRE LIVRE。这项永续性倡议使该公司赢得了第 20 届 ABRE 巴西包装奖的最受欢迎投票奖。 SGK 和强生公司首次推出柔性薄膜包装,开闢了新领域。我们开发了一种用于女性护理用品的低调插入物,其中 33% 使用消费后树脂,与传统包装相比,可减少 10.25% 的碳足迹。

- 阿根廷的包装产业在景气衰退,疫情加剧了这一困境。中低收入族群的购买力大幅下降,抑制了创新和奢侈品包装企业的发展。随着工资下降、失业率上升和消费者习惯改变,各种类型和尺寸的包装都受到了影响。

- 过去十年来,公众对塑胶有害影响的认识显着提高。拉丁美洲各国政府已经发起了许多公共宣传活动和倡议来增强这种意识。因此,近年来塑胶包装消费发生了显着变化。

拉丁美洲软包装市场的趋势

预计袋装包装市场将强劲成长

- 欧洲广泛使用的袋子有立式袋子和平式袋子两种。立式袋包括杀菌袋、底折袋、平底袋、侧折袋、吸嘴袋、改良袋等。平口袋分为枕头式、四边封、三边封、真空等类型。

- 市场对袋子的需求是由其耐用性和物流便利性决定的。它的成本效益鼓励製造商越来越多地采用袋装包装,进一步推动这种灵活形式的成长。此外,袋子重量轻,比宝特瓶传统包装形式更受欢迎。

- 牛皮纸在包装、小袋和袋子等领域的需求量很大。环保包装的日益普及引起了人们对牛皮纸的兴趣,特别是因为其製浆过程使得废弃物更容易回收和再利用。为了顺应这一趋势,总部位于蒙特利尔、业务遍及美国和拉丁美洲的包装製造商 TC Transcontinental 于 2020 年宣布计划增加其软包装产品(如包装袋)中的消费后再生纸含量。该公司还投资了设备,将从分类设施和其他地方获得的软质塑胶进行转化。

- 2023 年 2 月,软包装和材料科学领域的领导者 ProAmpac 在其主动永续发展产品组合中增加了新产品:ProActive Recyclable R~2050 和 ProActive Post Industrial Recycled Content (PIR)。

- 袋子已成为包装电子商务产品的热门选择。食品饮料、个人护理和医药领域越来越青睐包装袋,尤其是针对电子商务市场的产品。由于袋装包装效率高、成本效益高,电子商务参与企业越来越倾向使用袋装包装。

预计巴西将占据很大市场份额

- 巴西是拉丁美洲的领先国家,经济成长强劲,吸引了大量外国直接投资 (FDI)。由于该国对食品和工业产品的需求旺盛,严重依赖进口。该地区正在采用灵活的包装解决方案来保护这些产品免受损坏。随着中产阶级的扩大,对包装食品的需求也随之增加,为软包装市场的扩张铺平了道路。

- 根据巴西美容护理协会(ABIHPEC&ApexBrasil)报告,2023年巴西在美容和个人保健产品领域实现了贸易顺差。这个南美巨头向全球市场出口了价值超过 9.11 亿美元的化妆品和卫生产品。

- 2024 年 3 月,主要企业SIG 与着名乳製品公司 DPA Brasil 合作,为其 Chamyto 优格品牌推出创新的带嘴袋包装。新包装采用 SIG CloverCap 85RO 封盖和 SIG Prime 120 填充机制,设计轻巧而坚固,易于使用,尤其是对于儿童而言。草莓口味 Chamyto 优格是 DPA Brasil 首款采用这种尖端包装形式的产品。 DPA Brasil 还计划将这种包装创新扩展到其其他产品,包括 Chamyto 水果维生素优格、Chambinho Recreio 和 Ninho Lancheirinha。

- 此外,市场呈现优质化趋势。儘管巴西人整体对价格比较敏感,但他们在化妆品上的投资意愿却越来越大。这种转变正在推动对软包装的需求。聚胺和聚丙烯等软质塑胶材料增强了包装的可见度和吸引力,并具有必要的安全特性。

拉丁美洲软包装产业概况

拉丁美洲软包装市场适度整合,由多家全球和区域参与企业组成。由于新参与企业的进入门槛较低,市场一直受到许多新参与企业的推动。该市场的特征是产品差异化低、产品扩散度高、竞争激烈。透过设计、技术和应用的创新可以获得可持续的竞争优势。市场的一些主要参与企业包括 Amcor PLC、Berry Global Inc.、Mondi Group 和 Sealed Air Corporation。

- 2024年5月,巴西SGK团队与强生巴西公司合作推出了SEMPRE LIVRE。为了表彰其永续性的努力,该公司在第 20 届 ABRE 巴西包装奖中赢得了大众投票奖。 SGK 与强生公司合作开发了首个软膜包装,一直处于创新前沿。 SGK 为女性护理用品设计了一种低调插入物,该产品使用 33% 的消费后树脂,与现有包装相比,碳足迹减少了 10.25%。

- 2023 年10 月,PAC Worldwide 将从墨西哥佩德罗埃斯科韦多搬迁至维斯塔圣胡安德尔里奥占地83,000 平方英尺的新工厂,这是提高其在中美洲製造能力的策略的一部分。此综合软包装设施位于墨西哥城以北两小时车程。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场动态

- 市场概况

- 市场驱动因素

- 便捷包装需求不断成长

- 市场问题

- 环境和回收问题

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 产业价值链分析

- 产业微观经济因素评估

5. 拉丁美洲软包装市场的永续包装和技术进步

- 轻的

- 回收/再生聚合物

- 袋装包装的可持续涂料

- 屏障开发

- 活性包装

第六章 市场细分

- 材料类型

- 塑胶

- 聚乙烯 (PE)

- 双轴延伸聚丙烯(BOPP)

- 流延聚丙烯(CPP)

- 聚氯乙烯(PVC)

- 乙烯 - 乙烯醇(EVOH)

- 纸

- 铝箔

- 塑胶

- 产品类型

- 小袋

- 包包

- 薄膜和包装

- 其他的

- 最终用户产业

- 食物

- 冷冻食品

- 乳製品

- 水果和蔬菜

- 肉类、家禽和鱼贝类

- 烘焙点心和零嘴零食

- 糖果和糖果零食

- 其他的

- 饮料

- 药品和医疗用品

- 家庭和个人护理

- 其他的

- 食物

- 地区

- 巴西

- 阿根廷

- 墨西哥

- 其他拉丁美洲国家(哥伦比亚、委内瑞拉等)

第七章 竞争格局

- 公司简介

- Amcor PLC

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Coveris Holdings SA

- Tetra Pak International SA

- Cascades Flexible Packaging

- Novolex Holdings Inc.

- WIPF Doypack(Wipf AG)

- FlexPak Services LLC

- Transcontinental Inc.

- American Packaging Corporation

- Sonoco Products Company

- Inteplast Group

- Oben Holding Group

- Toray Plastics(America)Inc.

- Sigma Plastic Group

- Clifton Packaging SA De CV

- PO Empaques Flexibles SA De CV

- ProAmpac LLC

第八章投资分析

第九章:市场的未来

The Latin America Flexible Packaging Market size is estimated at USD 10.31 billion in 2025, and is expected to reach USD 12.57 billion by 2030, at a CAGR of 4.04% during the forecast period (2025-2030).

Key Highlights

- Manufacturers benefit from substantial cost savings as flexible packaging consumes less raw materials and energy during production. Its efficient wrapping capabilities and reduced storage space requirements further boost its demand in the market.

- Trends like innovative packaging and digital printing are energizing the market, showcasing technological advancements. These include creative consumer engagement solutions, such as serialized QR codes. Additionally, the lightweight nature of flexible packaging cuts down transportation costs and fuel usage, making it a favored choice for snacks and potato chip packaging in the studied regions.

- In response to rising demand, several market players are forging collaborations and partnerships to enhance their revenues. For example, in May 2024, SGK's team in Brazil partnered with Johnson & Johnson Brazil to launch SEMPRE LIVRE. Their sustainability efforts earned them the Popular Vote category at the 20th ABRE Brazilian Packaging Award. SGK and Johnson & Johnson broke new ground with their first flexible film packaging. They crafted a thinner insert for female care products, using 33% post-consumer resin, and achieved a commendable 10.25% carbon footprint reduction over traditional packaging.

- The Argentine packaging sector grappled with challenges during the economic downturn, worsened by the pandemic. A significant drop in purchasing power among low and middle-income groups stifled innovation and premium packaging ventures. With wages plummeting, unemployment rising, and consumption habits shifting, the effects were felt across various packaging types and sizes.

- In the past decade, there has been a marked surge in public awareness about the detrimental effects of plastic. Latin American governments have spearheaded numerous public campaigns and initiatives, amplifying this awareness. Consequently, the consumption of plastic packaging has seen a pronounced shift in recent years.

Latin America Flexible Packaging Market Trends

The Pouches Segment is Expected to Grow Significantly

- Pouches, widely utilized across Europe, can be categorized into stand-up and flat types. Stand-up pouches encompass a range of varieties, including retort, bottom gusset, flat bottom, side gusset, spouted, and shaped pouches. Flat pouches are divided into pillow, four-side seal, three-side seal, and vacuum pouches.

- The demand for pouches in the market is fueled by their durability and logistical convenience. Their cost-effectiveness is prompting manufacturers to increasingly adopt pouch packaging, further propelling the growth of this flexible format. Additionally, pouches' lightweight nature makes them a preferred choice over traditional packaging formats like PET bottles.

- Kraft paper is in high demand for applications like wrapping, pouches, and sacks. The rising trend of eco-friendly packaging has spurred interest in kraft papers, especially since their pulping process facilitates easy waste recovery and recycling. In line with this trend, in 2020, TC Transcontinental, a Montreal-based packaging manufacturer with operations in the United States and Latin America, unveiled plans to boost post-consumer recycled content in its flexible offerings, including pouches. The company has also invested in equipment to convert flexible plastics sourced from sorting facilities and other avenues.

- In February 2023, ProAmpac, a frontrunner in flexible packaging and material science, introduced new additions to its ProActive Sustainability Portfolio: ProActive Recyclable R-2050 and ProActive Post Industrial Recycled Content (PIR).

- Pouches emerged as a dominant choice for packaging e-commerce products. They are increasingly favored in the food, beverage, personal care, and pharmaceutical sectors, especially for products targeting the e-commerce market. E-commerce players are gravitating toward pouch packaging due to its efficiency and cost-effectiveness.

Brazil is Expected to Hold a Significant Share in the Market

- Brazil is a frontrunner in Latin America, showcasing robust economic growth and attracting significant foreign direct investment (FDI). The nation, with its substantial appetite for food and industrial goods, heavily relies on imports. The region is increasingly turning to flexible packaging solutions to safeguard these products from damage. As the middle class expands, so does the appetite for packaged foods, paving the way for the expanding flexible packaging market.

- In 2023, Brazil achieved a trade surplus in beauty and personal care products, as per a report by Beautycare Brazil (ABIHPEC & ApexBrasil). The South American powerhouse exported cosmetics and hygiene products worth over USD 911 million to global markets.

- In March 2024, SIG, a leading supplier of aseptic cartons, partnered with DPA Brasil, a prominent dairy company, to roll out innovative spouted pouch packaging for the Chamyto yogurt brand. This new packaging, featuring the SIG CloverCap 85RO closure and SIG Prime 120 filling equipment, has a lightweight yet robust design, making it especially user-friendly for children. The strawberry-flavored Chamyto yogurt marks DPA Brasil's inaugural product to adopt this cutting-edge packaging format. DPA Brasil also plans to expand this packaging innovation to other offerings, including Chamyto fruit vitamin yogurts, Chambinho Recreio, and Ninho Lancheirinha.

- Additionally, the market is witnessing a trend towards premiumization. While Brazilians are generally price-sensitive but increasingly willing to invest in cosmetics. This shift is driving the demand for flexible packaging. Flexible plastic materials like polyamine and polypropylene enhance package visibility and appeal and incorporate essential safety features.

Latin America Flexible Packaging Industry Overview

The Latin American flexible packaging market comprises several global and regional players and is moderately consolidated. As the market poses low barriers to entry for the new players, several new entrants have gained traction. This market is characterized by low product differentiation, growing levels of product penetration, and high levels of competition. Sustainable competitive advantage can be gained through design, technology, and application innovation. Some of the major players operating in the market are Amcor PLC, Berry Global Inc., Mondi Group, and Sealed Air Corporation.

- May 2024: SGK's team in Brazil collaborated with Johnson & Johnson Brazil to introduce SEMPRE LIVRE. Their sustainability initiatives garnered them the Popular Vote category at the 20th ABRE Brazilian Packaging Award. In partnership with Johnson & Johnson, SGK spearheaded innovation by developing the inaugural flexible film packaging. They designed a thinner insert, incorporating 33% post-consumer resin for female care products, achieving a notable 10.25% reduction in carbon footprint compared to existing packaging.

- October 2023: PAC Worldwide relocated its operations from Pedro Escobedo, Mexico, to a new 83,000 sq. ft plant in Vistha San Juan Del Rio as part of its strategy to enhance manufacturing capabilities in Central America. This comprehensive, flexible packaging facility is two hours north of Mexico City.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Demand for Convenient Packaging

- 4.3 Market Challenges

- 4.3.1 Concerns Regarding Environment and Recycling

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Industry Value Chain Analysis

- 4.6 Assessment of the Microeconomic Factors on the Industry

5 SUSTAINABLE PACKAGING AND TECHNOLOGICAL ADVANCEMENTS IN THE LATIN AMERICAN FLEXIBLE PACKAGING MARKET

- 5.1 Light Weighting

- 5.2 Recycled and Recyclable Polymers

- 5.3 Sustainable Coatings for Pouch Packaging

- 5.4 Barrier Developments

- 5.5 Active Packaging

6 MARKET SEGMENTATION

- 6.1 Material Type

- 6.1.1 Plastics

- 6.1.1.1 Polyethene (PE)

- 6.1.1.2 Bi-orientated Polypropylene (BOPP)

- 6.1.1.3 Cast Polypropylene (CPP)

- 6.1.1.4 Polyvinyl Chloride (PVC)

- 6.1.1.5 Ethylene Vinyl Alcohol (EVOH)

- 6.1.2 Paper

- 6.1.3 Aluminum Foil

- 6.1.1 Plastics

- 6.2 Product Type

- 6.2.1 Pouches

- 6.2.2 Bags

- 6.2.3 Films and Wraps

- 6.2.4 Other Product Types

- 6.3 End-user Industry

- 6.3.1 Food

- 6.3.1.1 Frozen Food

- 6.3.1.2 Dairy Products

- 6.3.1.3 Fruits and Vegetables

- 6.3.1.4 Meat, Poultry, and Seafood

- 6.3.1.5 Baked Goods and Snack Foods

- 6.3.1.6 Candy and Confections

- 6.3.1.7 Other Food Products

- 6.3.2 Beverage

- 6.3.3 Pharmaceutical and Medical

- 6.3.4 Household and Personal Care

- 6.3.5 Other End-user Industries

- 6.3.1 Food

- 6.4 Geography

- 6.4.1 Brazil

- 6.4.2 Argentina

- 6.4.3 Mexico

- 6.4.4 Rest of Latin America (Colombia, Venezuela, etc.)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Berry Global Inc.

- 7.1.3 Mondi Group

- 7.1.4 Sealed Air Corporation

- 7.1.5 Coveris Holdings SA

- 7.1.6 Tetra Pak International SA

- 7.1.7 Cascades Flexible Packaging

- 7.1.8 Novolex Holdings Inc.

- 7.1.9 WIPF Doypack (Wipf AG)

- 7.1.10 FlexPak Services LLC

- 7.1.11 Transcontinental Inc.

- 7.1.12 American Packaging Corporation

- 7.1.13 Sonoco Products Company

- 7.1.14 Inteplast Group

- 7.1.15 Oben Holding Group

- 7.1.16 Toray Plastics (America) Inc.

- 7.1.17 Sigma Plastic Group

- 7.1.18 Clifton Packaging SA De CV

- 7.1.19 PO Empaques Flexibles SA De CV

- 7.1.20 ProAmpac LLC

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球柔性纸包装市场:预测(至2032年)-按包装类型、材料类型、通路、技术、应用和地区进行分析

全球柔性纸包装市场:预测(至2032年)-按包装类型、材料类型、通路、技术、应用和地区进行分析 软质包装市场按材料、包装类型、印刷技术、应用和地区划分-预测至2030年

软质包装市场按材料、包装类型、印刷技术、应用和地区划分-预测至2030年 包装贴合机机:全球市占率及排名、总收入及需求预测(2025-2031年)

包装贴合机机:全球市占率及排名、总收入及需求预测(2025-2031年) 软质包装的全球市场的未来(~2030年)2032 年软包装市场预测:按包装类型、结构、印刷、封口、密封、最终用户和地区进行的全球分析

软质包装的全球市场的未来(~2030年)2032 年软包装市场预测:按包装类型、结构、印刷、封口、密封、最终用户和地区进行的全球分析 按材料、产品类型、包装形式、最终用途和分销管道分類的柔性工业包装市场 - 2025-2030 年全球预测软包装市场按产品类型、材料类型、技术、封盖类型、最终用户和分销管道划分 - 2025-2030 年全球预测

按材料、产品类型、包装形式、最终用途和分销管道分類的柔性工业包装市场 - 2025-2030 年全球预测软包装市场按产品类型、材料类型、技术、封盖类型、最终用户和分销管道划分 - 2025-2030 年全球预测 全球软包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球软包装市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 欧洲软包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)2032年全球BOPP包装薄膜市场预测:依产品、材料、厚度、应用、最终用户和地区分析

欧洲软包装:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)2032年全球BOPP包装薄膜市场预测:依产品、材料、厚度、应用、最终用户和地区分析