|

市场调查报告书

商品编码

1850221

智慧感测器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Smart Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

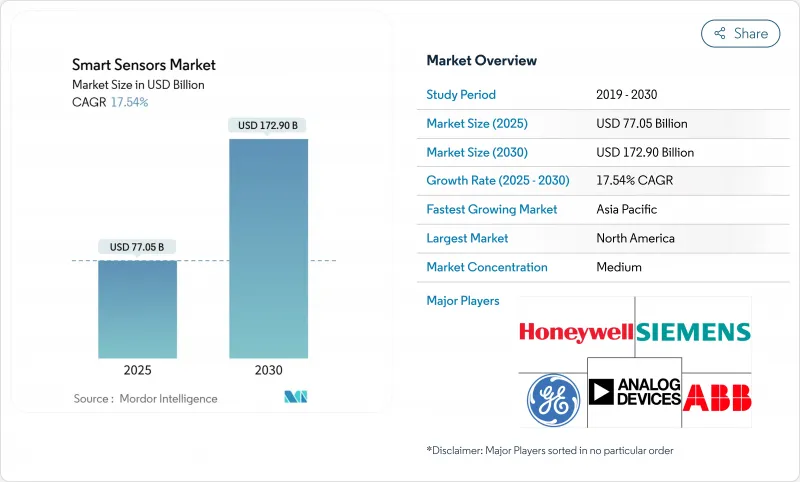

预计到 2025 年,智慧感测器市场规模将达到 770.5 亿美元,到 2030 年将成长至 1,729 亿美元。

这一成长趋势的驱动力来自边缘人工智慧的整合、日益严格的汽车和医疗保健法规,以及工业自动化项目,这些都促使企业从被动监控转向预测智慧。汽车自动紧急煞车和医疗设备持续病患监测等强制性安全功能,正在推动新兴市场对非选择性感测器的需求。同时,嵌入最新一代感测器的边缘人工智慧核心消除了延迟和频宽瓶颈,从而能够在电力受限的环境中实现即时分析。镓和锗的供应链压力以及半导体自给自足的竞争,使得平均售价在销量成长的同时保持稳定,为製造商提供了持续研发投资的空间。在预测期内,性能差异化将从原始灵敏度指标转向车载智慧、网路安全合规性和整合灵活性。

全球智慧感测器市场趋势与洞察

提升工业IoT的能源效率

具有法律约束力的永续性报告正促使製造商部署智慧感测器,从而实现可衡量的节能和二氧化碳减排。欧盟企业永续性报告指令要求提供精细的能源指标,促使工厂安装边缘人工智慧感测器,以持续优化暖通空调、照明和机器利用率。 SECO 的智慧CNC工具机改装使生产废弃物减少了 30%,备件成本降低了 10%。 Lech Stahlwerke 的 5G 赋能工厂也取得了类似的成果,这使得能源效率计划成为董事会层面的优先事项。随着早期采用者报告两位数的成本节约,后进企业面临效仿的竞争压力,从而形成对智慧感测器需求的自我强化循环。

家用电器感测器的普及

智慧型手机和穿戴式装置厂商目前在每个装置中整合多达 12 个感测器,支援空气品质测量、高级生物识别和自学习活动追踪等功能。博世已确认,2025 年推出的行动电话中,超过一半将配备博世多感测器模组。庞大的消费者需求将降低工业和汽车产业的规模经济,从而降低单位成本,并开闢新的性价比阈值。为穿戴式装置而完善的小型化和毫瓦级功耗技术,如今正应用于工厂状态监测节点和自动配送机器人,加速边缘感测器堆迭在各产业的跨产业应用。

初期实施成本高

全面部署智慧感测器通常需要同时投资于边缘网关、专用 5G 网路和员工技能提升。对于许多中小型工厂而言,总投资可能超过年销售额的 0.5%,导致盈亏平衡点推迟四个季度甚至更久。 Milesight 为首尔中小企业提供的承包物联网套件包含 LoRaWAN 闸道器和控制器,降低了整合难度,但即使是这种「一体化」方案也会对资本预算造成压力。虽然随着 MEMS 产量的增加,成本压力有所缓解,但预计在未来 24 个月内,预算的担忧仍将抑制资金紧张的营运商采用该技术。

細項分析

累计到2024年,压力感测器将创造218.8亿美元的收入,占据智慧感测器市场28.40%的最大份额。此细分市场的持久性源于其在高级驾驶辅助系统(ADAS)煞车、电动车电池管理和医疗人工呼吸器等领域不可替代的作用。同时,碳化硅隔膜技术的进步使得航太和氢燃料电池堆能够在超过600°C的动作温度。影像感测器虽然目前以收益为准较小,但随着自动驾驶成为强制性要求以及行人侦测摄影机成为标配,预计将以19.20%的复合年增长率成长。全局百叶窗和基于事件的像素的集成,即使在快速变化的光照条件下也能实现高对比度性能,帮助汽车製造商在无需昂贵的激光雷达冗余设备的情况下满足自动紧急制动(AEB)法规的要求。

需求的多样化也正在改变设备的经济性。温度、湿度和流量感测器正被整合到智慧城市供水网路和资料中心温度控管计划中,而六轴位置感测器正成为协作机器人的必备组件。结合压力、温度和相对湿度感测的混合模组虽然降低了安装成本,但透过增加原始设备製造商 (OEM) 的转换成本,也加剧了供应商锁定。

由于成熟的代工生态系统和专为智慧型手机量身定制的成本结构,MEMS装置将在2024年占据智慧感测器市场46.00%的份额。光是博世一家公司在2024年就将出货超过60亿颗MEMS装置,展现出规模优势。然而,光电感测器和量子感测器预计将以21.50%的复合年增长率成长,这可能会蚕食MEMS在高精度导航和医疗诊断领域的市场份额。花旗集团预测,到2030年,量子感测市场规模将达到14亿美元,将刺激创业投资的流入。 MEMS领域的现有企业正在透过将生物MEMS通路与边缘AI DSP核心结合来应对这一挑战,从而在其技术蓝图中锁定大宗买家。

包括3M公司在内的美国-JOINT)等产业联盟正在加速材料研发,以确保先进基板的国内供应链。同时,嵌入微机电系统(MEMS)模组的神经形态运算单元也在同步研发中,旨在提供认知能力,同时又不牺牲MEMS技术赖以领先的尺寸和成本优势。

区域分析

预计到2024年,亚太地区将占全球销售额的44.30%,并在2030年之前维持19.70%的复合年增长率。这主要得益于中国「十四五」规划对国产感测积体电路的补贴以及日本对量子感测研发的补贴。预计2024年,中国国内市场规模将达2,850亿元人民币(约398亿美元),其中汽车、工厂自动化和网路通讯三大领域分别占比超过20%。亚太地区的晶圆代工厂受益于强劲的需求和较低的投入成本通膨,而垂直整合的原始设备製造商(OEM)正在推进整个供应链的本地化。

北美持续引领科技发展,尤其是在汽车高阶驾驶辅助系统(ADAS)和航太感测领域。Honeywell和恩智浦半导体(NXP)携手伙伴关係,共同开发人工智慧赋能的航空电子设备,充分体现了该地区对功能安全和边缘运算的重视。美国持续的产业政策激励措施,例如《晶片法案》(CHIPS Act)的拨款,促进了ams旗下欧司朗和格罗方德等公司将微机电系统(MEMS)生产线迁回北美,增强了区域韧性。

欧洲虽然在销售上落后于亚太地区,但正受惠于监管上的利多。欧盟的《通用安全法规II》规定所有新车都必须配备感测器套件,确保即使在景气衰退时期也能保持稳定的销售成长。此外,企业减碳目标也刺激了德国、法国和北欧地区对建筑自动化和工业效率感测器的需求。

在中东、非洲和南美洲等新兴市场,智慧城市建设和资源产业数位化带来的挑战正在加速感测器技术的应用。沙乌地阿拉伯的计划需要密集的环境和交通管理感测器网络,而智利的铜矿则正在安装坚固耐用的振动感测器以提高采矿效率。低延迟卫星回程传输解决方案正在降低连接障碍,使这些地区能够在没有传统通讯基础设施的情况下采用先进的感测技术。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概况

- 市场驱动因素

- 提高工业IoT的能源效率

- 感测器在家电中的普及

- 车辆和电子健康安全义务

- 小型化和无线技术的进步

- 感测器边缘人工智慧降低延迟

- 引入 ESG主导的即时监控

- 市场限制

- 初始安装成本高

- 复杂设计和整合技能差距

- 物联网网路安全风险

- 稀土元素包装供应风险

- 价值/供应链分析

- 监管格局

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 流量感测器

- 湿度感测器

- 位置感测器

- 压力感测器

- 温度感测器

- 影像/光学感测器

- 其他类型

- 依技术

- MEMS

- CMOS

- 光谱学

- 量子和光子

- 其他技术

- 按组件

- 类比数位转换器

- 数位类比转换器

- 扩大机

- 收发器/射频前端

- 嵌入式AI核心

- 其他组件

- 按用途

- 航太和国防

- 汽车和运输

- 医疗保健和医疗设备

- 工业自动化

- 楼宇和家居自动化

- 家电

- 农业与环境

- 其他用途

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 其他亚太地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ABB

- Honeywell International

- Eaton Corporation

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- Siemens AG

- TE Connectivity

- Legrand

- General Electric

- Vishay Intertechnology

- Bosch Sensortec

- Texas Instruments

- Omron Corporation

- Sensirion AG

- Murata Manufacturing

- Sony Semiconductor

- Samsung Electronics

- Robert Bosch GmbH

第七章 市场机会与未来展望

The smart sensors market reached USD 77.05 billion in 2025 and is forecast to rise to USD 172.90 billion by 2030, translating into a robust 17.54% CAGR.

This growth trajectory is propelled by the convergence of edge artificial intelligence, tightening automotive and healthcare regulations, and industrial automation programs that are moving enterprises from reactive monitoring to predictive intelligence. Mandatory safety features such as automatic emergency braking in vehicles and continuous patient monitoring in medical devices are translating into non-discretionary sensor demand across developed markets. At the same time, edge-AI cores embedded in the latest sensor generations eliminate latency and bandwidth bottlenecks, allowing real-time analytics within power-constrained environments. Supply-chain pressures around gallium and germanium and the race for semiconductor self-sufficiency are keeping average selling prices firm even as unit volumes rise, giving manufacturers headroom for sustained R&D investment. Over the forecast period, performance differentiation is shifting from raw sensitivity metrics to on-board intelligence, cyber-security compliance, and integration flexibility-factors now decisive in procurement shortlists.

Global Smart Sensors Market Trends and Insights

Energy-efficiency Push Across Industrial IoT

Legally binding sustainability reporting is prompting manufacturers to deploy intelligent sensors that deliver measurable kWh savings and CO2 reductions. The European Corporate Sustainability Reporting Directive requires granular energy metrics, pushing factories to install edge-AI sensors that continuously optimise HVAC, lighting, and machine utilisation. SECO's smart CNC retrofit cut production waste by 30% and spare-parts spend by 10%, showcasing hard-dollar returns that justify fleet-wide rollouts. Similar results at Lech-Stahlwerke's 5G-enabled mill have turned energy-efficiency projects into board-level priorities. As early adopters report double-digit cost reductions, laggards face competitive pressure to follow suit, creating a self-reinforcing demand cycle for intelligent sensors.

Consumer-electronics Sensor Proliferation

Smartphone and wearable OEMs now integrate up to a dozen sensor types per device, supporting features such as air-quality measurement, advanced biometrics, and self-learning activity tracking. Bosch confirms that more than half of 2025 handset launches ship with its multi-sensor modules. High-volume consumer demand delivers scale economies that drive per-unit cost down across industrial and automotive tiers, opening new price-performance thresholds. Miniaturisation and milliwatt-level power consumption perfected for wearables are now migrating into factory condition-monitoring nodes and autonomous delivery robots, accelerating cross-industry adoption of edge-ready sensor stacks.

High Upfront Deployment Cost

Comprehensive smart sensor rollouts frequently require parallel investment in edge gateways, private 5G networks, and workforce reskilling. For many small and midsized plants, total outlay can exceed 0.5% of annual revenue, deferring breakeven beyond four fiscal quarters. Milesight's turnkey IoT kit for Seoul SMEs bundles LoRaWAN gateways and controllers to lower integration friction, yet even this "all-in-one" package strains capital budgets. Cost headwinds are easing as MEMS volumes scale, but budgetary caution is expected to temper adoption among cash-constrained operators over the next 24 months.

Other drivers and restraints analyzed in the detailed report include:

- Automotive & E-health Safety Mandates

- On-sensor Edge-AI Lowers Latency

- Complex Design & Integration Skill Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pressure sensors contributed USD 21.88 billion in 2024, translating to the largest 28.40% share of the smart sensors market. The segment's durability stems from its irreplaceable role in ADAS braking, EV battery management, and medical ventilators. Parallel innovation in silicon-carbide diaphragms now extends operating envelopes above 600 °C for aerospace and hydrogen fuel-cell stacks. Image sensors, while smaller in revenue terms, are forecast to grow at 19.20% CAGR as autonomous driving mandates make pedestrian-detection cameras standard equipment. Integration of global-shutter and event-based pixels is allowing high-contrast performance under rapidly changing lighting, enabling vehicle OEMs to comply with AEB regulations without expensive LiDAR redundancy.

Demand diversification is also reshaping unit economics. Temperature, humidity, and flow sensors are piggy-backing on smart-city water-grid and data-center thermal-management projects, while six-axis position sensors are becoming mandatory in collaborative robots. Hybrid modules that blend pressure, temperature, and relative humidity sensing deliver installation savings and strengthen vendor lock-in by raising switching costs for OEMs.

MEMS devices captured 46.00% of smart sensors market share in 2024 due to mature foundry ecosystems and cost structures tuned for smartphone volumes. Bosch alone shipped over 6 billion MEMS units in 2024, underscoring the scale advantage. However, photonic and quantum-enhanced sensors are projected to expand at 21.50% CAGR and could clip MEMS share in high-precision navigation and medical diagnostics. Citigroup estimates the quantum sensing addressable market could reach USD 1.4 billion by 2030, catalyzing venture capital inflows. MEMS incumbents are responding by co-integrating BioMEMS channels and edge-AI DSP cores to keep volume buyers within their technology roadmap.

Industry consortia such as the US-JOINT program, which includes 3M, are accelerating material R&D to secure domestic supply chains for advanced substrates. A parallel push into neuromorphic compute tiles embedded in MEMS modules aims to deliver cognitive functionality without sacrificing the size-cost advantage that underpin MEMS leadership.

The Smart Sensors Market is Segmented by Type (Flow Sensor, Humidity Sensor, Position Sensor, Pressure Sensor, and More), by Technology (MEMS, CMOS, Optical Spectroscopy, and More), by Component (Analog-To-Digital Converter, Digital-To-Analog Converter, Amplifier, and More), by Application (Aerospace and Defense, Automotive and Transportation, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific delivered 44.30% of 2024 global revenue and is expected to record a 19.70% CAGR through 2030, underpinned by China's 14th Five-Year Plan subsidies for domestic sensing ICs and Japan's coordinated quantum-sensing R&D grants. China's domestic market hit CNY 285 billion (USD 39.8 billion) in 2024, with automotive, factory automation, and network communications each capturing above-20% share. Regional foundries benefit from captive demand and lower input-cost inflation, prompting vertically integrated OEMs to localise entire supply chains.

North America remains technological bellwether, particularly in automotive ADAS and aerospace sensing. Honeywell's strategic partnership with NXP to co-develop AI-ready avionics exemplifies the region's focus on functional safety and edge compute. Ongoing US industrial-policy incentives, including CHIPS Act grants, are encouraging on-shoring of MEMS lines by ams OSRAM and GlobalFoundries, improving regional resilience.

Europe, while trailing APAC in volume, benefits from regulatory pull. The EU General Safety Regulation II sets a baseline of mandatory sensor suites in every new vehicle, guaranteeing steady volume ramps even in economic downturns. Additionally, corporate carbon-reduction targets are stimulating demand for building-automation and industrial-efficiency sensors across Germany, France, and the Nordics.

Emerging markets in the Middle East, Africa, and South America show accelerating sensor uptake through smart-city and resource-sector digitisation agendas. Saudi Arabia's giga-projects require dense environmental and traffic-management sensor grids, whereas Chilean copper mines are installing ruggedised vibration sensors to raise extraction efficiency. Low-latency satellite backhaul solutions are easing connectivity barriers, allowing these regions to adopt advanced sensing without legacy telecom infrastructure.

- ABB

- Honeywell International

- Eaton Corporation

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- Siemens AG

- TE Connectivity

- Legrand

- General Electric

- Vishay Intertechnology

- Bosch Sensortec

- Texas Instruments

- Omron Corporation

- Sensirion AG

- Murata Manufacturing

- Sony Semiconductor

- Samsung Electronics

- Robert Bosch GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency push across industrial IoT

- 4.2.2 Consumer-electronics sensor proliferation

- 4.2.3 Automotive and e-health safety mandates

- 4.2.4 Miniaturisation and wireless advances

- 4.2.5 On-sensor edge-AI lowers latency

- 4.2.6 ESG-driven live-monitoring adoption

- 4.3 Market Restraints

- 4.3.1 High upfront deployment cost

- 4.3.2 Complex design and integration skill gap

- 4.3.3 IoT cybersecurity exposure

- 4.3.4 Rare-earth packaging supply risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Flow Sensors

- 5.1.2 Humidity Sensors

- 5.1.3 Position Sensors

- 5.1.4 Pressure Sensors

- 5.1.5 Temperature Sensors

- 5.1.6 Image/Optical Sensors

- 5.1.7 Other Types

- 5.2 By Technology

- 5.2.1 MEMS

- 5.2.2 CMOS

- 5.2.3 Optical Spectroscopy

- 5.2.4 Quantum and Photonic

- 5.2.5 Other Technologies

- 5.3 By Component

- 5.3.1 Analog-to-Digital Converter

- 5.3.2 Digital-to-Analog Converter

- 5.3.3 Amplifier

- 5.3.4 Transceiver / RF Front-End

- 5.3.5 Embedded AI Core

- 5.3.6 Other Components

- 5.4 By Application

- 5.4.1 Aerospace and Defence

- 5.4.2 Automotive and Transportation

- 5.4.3 Healthcare and Medical Devices

- 5.4.4 Industrial Automation

- 5.4.5 Building and Home Automation

- 5.4.6 Consumer Electronics

- 5.4.7 Agriculture and Environmental

- 5.4.8 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB

- 6.4.2 Honeywell International

- 6.4.3 Eaton Corporation

- 6.4.4 Analog Devices

- 6.4.5 Infineon Technologies

- 6.4.6 NXP Semiconductors

- 6.4.7 STMicroelectronics

- 6.4.8 Siemens AG

- 6.4.9 TE Connectivity

- 6.4.10 Legrand

- 6.4.11 General Electric

- 6.4.12 Vishay Intertechnology

- 6.4.13 Bosch Sensortec

- 6.4.14 Texas Instruments

- 6.4.15 Omron Corporation

- 6.4.16 Sensirion AG

- 6.4.17 Murata Manufacturing

- 6.4.18 Sony Semiconductor

- 6.4.19 Samsung Electronics

- 6.4.20 Robert Bosch GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

3D智慧感测器市场:依技术、组件、平台、产品、应用、通路划分,全球预测(2026-2032年)

3D智慧感测器市场:依技术、组件、平台、产品、应用、通路划分,全球预测(2026-2032年) 智慧感测器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分

智慧感测器市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分 日本工业智慧感测器市场规模、份额、趋势和预测:按类型、最终用户和地区划分,2026-2034年

日本工业智慧感测器市场规模、份额、趋势和预测:按类型、最终用户和地区划分,2026-2034年 2026年全球智慧感测器市场报告

2026年全球智慧感测器市场报告 智慧感测器市场-全球产业规模、份额、趋势、机会、预测:按类型、组件、应用、地区和竞争对手划分,2021-2031年智慧监控感测器市场:依产品类型、技术、连接方式、终端用户产业、应用、分销管道划分-2026-2032年全球预测智慧门窗感测器市场按产品类型、通讯协定、安装类型、价格范围、应用和分销管道划分,全球预测(2026-2032年)日本智慧感测器市场报告(按类型(触控感测器、影像感测器、温度感测器、运动感测器、位置感测器、压力感测器)、最终用户(汽车、消费性电子、基础设施、医疗保健及其他)和地区划分,2026-2034年)

智慧感测器市场-全球产业规模、份额、趋势、机会、预测:按类型、组件、应用、地区和竞争对手划分,2021-2031年智慧监控感测器市场:依产品类型、技术、连接方式、终端用户产业、应用、分销管道划分-2026-2032年全球预测智慧门窗感测器市场按产品类型、通讯协定、安装类型、价格范围、应用和分销管道划分,全球预测(2026-2032年)日本智慧感测器市场报告(按类型(触控感测器、影像感测器、温度感测器、运动感测器、位置感测器、压力感测器)、最终用户(汽车、消费性电子、基础设施、医疗保健及其他)和地区划分,2026-2034年) 智慧感测器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)智慧感测器市场报告,按类型(触控感测器、影像感测器、温度感测器、运动感测器、位置感测器、压力感测器)、最终用户(汽车、消费性电子、基础设施、医疗保健等)和地区(2025-2033 年)

智慧感测器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)智慧感测器市场报告,按类型(触控感测器、影像感测器、温度感测器、运动感测器、位置感测器、压力感测器)、最终用户(汽车、消费性电子、基础设施、医疗保健等)和地区(2025-2033 年)