|

市场调查报告书

商品编码

1851794

增强型分析:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)Augmented Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

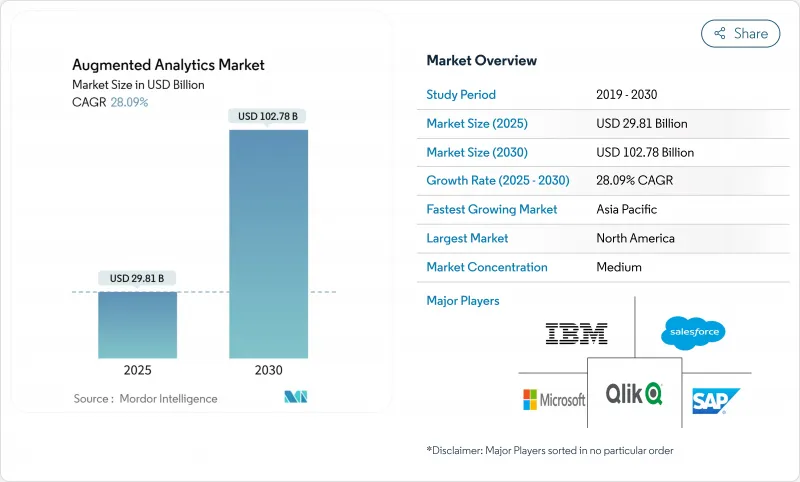

预计增强分析市场规模将在 2025 年达到 298.1 亿美元,到 2030 年达到 1,027.8 亿美元,在预测期(2025-2030 年)内复合年增长率为 28.09%。

随着大型语言模型 (LLM) 功能成为主流商业情报套件的标配,收入成长动能将从概念验证转向企业级部署。能够执行自然语言查询、自动产生洞察和工作流程的 AI 代理将减少分析积压,缩短决策週期,从而在各个业务层面增强资料主导文化。儘管云端平台仍占据主导地位,但随着资料主权要求敏感工作负载在本地处理,混合架构正日益普及。用于协调边缘、私有云端和公有区域 AI 任务的编配工具的供应商竞争日益激烈。随着企业寻求合作伙伴来重新设计管治、提升员工技能并优化特定领域的底层模型,对服务的需求将加速成长。供应链瓶颈和高效能 GPU 推理成本的上升将限制近期扩展计划,但超大规模资料中心业者资料中心的蓝图图投资表明,基础设施建设将持续到 2026 年。

全球增强分析市场趋势与洞察

对多结构化资料分析的需求日益增长

近 80% 的企业资料是非结构化的,涵盖文件、影像和机器日誌等多种形式。先进的语言和视觉模型能够解析这些格式以及传统的表格形式资料集,为分析师提供统一的资讯发现平台。汽车製造商正利用这项能力将感测器远端检测与维修手册融合,将停机时间预测准确率提升 85%。医院则将放射影像、临床记录和基因组图谱结合,以改善诊断流程。利用这些尚未开发的资料资源正推动各组织转向整合原生 AI 解析器的平台,进而促进增强型分析市场的成长。

促进自助式商业智慧和数据民主化

自然语言提示使市场经理、财务主管和客服中心供电督导无需使用 SQL 即可运行复杂的查询。这种转变将请求到获得洞察的周期从数週缩短到数分钟,使数据工程团队能够专注于更高价值的任务。 ThoughtSpot 与 Google Gemini 模型的整合展示了对话式搜寻如何在提供精选且共用的答案的同时,隐藏复杂性。更广泛的应用改善了数据素养的回馈循环,巩固了分析文化,并进一步推动了增强型分析市场的发展。

资料隐私和安全问题

GDPR 和其他行业法规要求明确征得用户同意、数据最小化和审核追踪,这使得自由地进行人工智慧实验存在风险。 MicroStrategy 已与 STACKIT 合作,提供符合欧盟标准的、託管在德国和奥地利的软体栈。合规成本会延缓计划部署,从而降低短期支出,但有助于建立长期信任。

细分市场分析

到2024年,软体收入将占总收入的78%,因为买家倾向于选择包含资料收集、建模和视觉化功能的端到端套件。就以金额为准,该细分市场规模将达到232.7亿美元。持续的功能发布,例如产品内建的LLM聊天机器人,为更新和提升销售提供了可靠的途径。服务细分市场虽然规模较小,但正以28.96%的复合年增长率快速成长,主要得益于实施、模型管理和用户采纳计划的推动。随着多重云端环境的扩展,客户将策略设计、测试和ROI基准等工作外包给合作伙伴。供应商的专业服务团队正在抓住这一机会,而全球系统整合正在组建千人规模的AI工作室以满足市场需求。

次要影响进一步强化了软体优势。 Snowflake 将 Anthropic 的模型整合到其 Cortex 服务中,让客户无需汇出资料即可存取生成式摘要,从而增强了使用者对该平台的依赖性。展望未来,开放原始码AI 元件也将不断发展,但软体产业仍将主导市场细分,因为买家更倾向于选择能够保证安全修补程式和法律赔偿的商业封装产品。

到2024年,云端采用将占总支出的61%。金融服务公司、线上市场和串流媒体网路正在利用弹性架构来应对假日高峰和模型训练的激增。然而,严格的驻留要求正将关键工作负载转移到私人区域,推动混合架构以30.22%的复合年增长率成长。混合架构在增强分析市场中的份额预计将从2025年的181.9亿美元增长到2030年的713.4亿美元。边缘设备在本地处理个人识别讯息,然后将聚合模式传输到云端人工智慧进行更深入的推理,从而在合规性和分析深度之间取得平衡。

边缘到云的编配工具预示着下一个战场的到来。平台需要调度防火墙两侧 Kubernetes 丛集上的 SQL、向量搜寻和强化学习作业。能够自动化容器部署、管理加密金钥并优化延迟的供应商有望获得显着的市场份额。纯本地部署在核能、国防和製药行业仍然十分重要,但由于这些行业资金有限,硬体更新周期较长,其成长速度落后于混合部署。

增强分析市场报告按组件(软体和服务)、部署方式(本地部署、云端部署、混合部署)、组织规模(大型企业和中小企业)、最终用户垂直行业(银行、金融服务和保险、通讯和 IT、零售和消费品、医疗保健和生命科学、製造业、媒体和娱乐、政府和公共部门)以及地区进行细分。

区域分析

北美将在2024年贡献全球48%的收入,并拥有许多结构性优势,包括密集的云端基础设施、创业投资的创投管道以及技术纯熟劳工储备。财富500强企业正在建立人工智慧卓越中心,并将分析技术嵌入财务、供应链和人力资源应用中。联邦政府对人工智慧研究的资助以及简化的IPO流程正在吸引新兴企业,从而重塑产业格局。然而,加拿大的资料本地化规定、加州消费者隐私法案的修订以及反垄断审查,都使得合规成本高昂,并促使企业转向跨司法管辖区的混合架构。

儘管亚太地区目前规模较小,但预计到2030年将以28.80%的复合年增长率成长。各国政府已为人工智慧基础设施、半导体和人才培育累计超过5000亿美元。中国深圳的人工智慧中心为GPU丛集提供补贴,而印度的《数位个人资料保护法》在鼓励国内创新的同时,也设定了监管框架。製造业巨头正聚集在东京、首尔和新加坡,从而形成对现场预测分析的巨大需求。本地供应商正在整合普通话、印地语和印尼语的语音模型,以满足语言需求,并为本地企业带来竞争优势。因此,亚太地区的增强分析市场正以最快的速度成长。

儘管受GDPR和即将推出的人工智慧法规影响,供应商的义务日益增加,但欧洲的成长率仍维持在15%左右。德国中小企业正积极采用跨境主权云。法国公共机构为了遵守公民资料法规,正在偏远地区运作分析系统。供应商蓝图被标记为“欧盟可信区域”,以反映欧洲大陆的法规。南北之间的数位技能差距依然存在,但欧盟资助的技能再培训计画正在缩小这一差距,并支持技术的稳定普及。

拉丁美洲、中东和非洲是新兴市场,预计到2030年将占增强型分析市场近10%的份额。行动优先的经营模式、金融科技的日益普及以及不断增长的无银行帐户人口,正在推动银行帐户评分和诈欺检测领域对分析技术的需求。在圣保罗、利雅德和约翰尼斯堡部署云端区域,可以降低延迟,支援资料驻留规则,并提供试点预算,以便在实现投资回报后迁移到生产工作负载。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 对多结构化资料分析的需求日益增长

- 促进自助式商业智慧和数据民主化

- 利用云端订阅服务吸引中小企业

- 整合生成式人工智慧的分析套件

- 资料主权边缘层部署

- SaaS Copilot主导的嵌入式分析货币化

- 市场限制

- 资料隐私和安全问题

- 劳动市场缺乏保障,面临人力替代问题

- 及时弥补工程技能差距

- GPU稀缺和推理成本上涨

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按组件

- 软体

- 服务

- 透过部署

- 本地部署

- 云

- 杂交种

- 按公司规模

- 大公司

- 小型企业

- 按最终用户行业划分

- BFSI

- 电讯和资讯技术

- 零售和消费品

- 医疗保健和生命科学

- 製造业

- 媒体与娱乐

- 政府和公共部门

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Microsoft Corporation

- Salesforce Inc.(incl. Tableau)

- SAP SE

- International Business Machines Corp.

- QlikTech International AB

- Google LLC(Looker)

- Oracle Corporation

- SAS Institute Inc.

- TIBCO Software Inc.

- ThoughtSpot Inc.

- MicroStrategy Inc.

- Sisense Inc.

- GoodData Corp.

- Alteryx Inc.

- Domo Inc.

- Zoho Corporation(Zoho Analytics)

- Amazon Web Services-QuickSight

- Yellowfin BI

- Board International

第七章 市场机会与未来展望

The Augmented Analytics Market size is estimated at USD 29.81 billion in 2025, and is expected to reach USD 102.78 billion by 2030, at a CAGR of 28.09% during the forecast period (2025-2030).

Revenue momentum shifts from proof-of-concepts to enterprise-wide deployments as large-language-model (LLM) functions become standard features inside mainstream business-intelligence suites. Natural-language querying, automated insight generation, and AI agents that execute workflows reduce analytics backlogs and shorten decision cycles, elevating data-driven culture across every business layer. Cloud platforms remain dominant, yet hybrid architectures gain traction because data-sovereignty mandates require on-premises processing for sensitive workloads. Vendor competition intensifies around orchestration tools that coordinate AI tasks between edge, private cloud, and public regions. Services demand accelerates as organisations seek partners to redesign governance, reskill workers, and fine-tune foundation models for domain specificity. Supply-chain bottlenecks for high-performance GPUs and rising inference costs temper near-term scaling plans, but road-map investments by hyperscalers indicate sustained infrastructure build-out through 2026.

Global Augmented Analytics Market Trends and Insights

Rising demand to analyse multi-structured data

Nearly 80% of enterprise information is unstructured, spanning documents, images, and machine logs. Advanced language and vision models now parse these formats alongside classic tabular datasets, giving analysts a single discovery surface. Automotive manufacturers use the capability to fuse sensor telemetry with maintenance manuals and raise downtime-forecasting accuracy by 85%. Hospitals are combining radiology scans, clinical notes, and genomic profiles to refine diagnostic pathways. The ability to tap these untapped data pools pushes organisations toward platforms that embed AI-native parsers, reinforcing growth for the augmented analytics market.

Self-service BI and data-democratisation push

Natural-language prompts let marketing managers, finance controllers, and call-centre supervisors run complex queries without SQL. This shift cuts request-to-insight cycles from weeks to minutes and frees data-engineering teams for higher-value tasks. ThoughtSpot's integration with Google's Gemini models shows how conversational search hides complexity while returning governed, shareable answers. Higher usage rates improve data-literacy feedback loops, anchoring analytics culture, and lifting the augmented analytics market further.

Data-privacy and security concerns

GDPR and sectoral rules require explicit consent, data minimisation, and audit trails, making unfettered AI experimentation risky. Vendors now launch "sovereign cloud" zones inside regional data centres; MicroStrategy partnered with STACKIT to deliver an EU-compliant stack hosted in Germany and Austria. Compliance overhead slows project rollout, trimming near-term spending even as long-term trust builds.

Other drivers and restraints analyzed in the detailed report include:

- SME uptake via cloud subscriptions

- Generative-AI infused analytics suites

- Workforce anxiety over human-replacement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 78% revenue in 2024 as buyers gravitated toward end-to-end suites bundling ingestion, modelling, and visualisation. In monetary terms, the segment contributed USD 23.27 billion to the augmented analytics market size. Continuous feature releases, such as in-product LLM chatbots, lock in renewals and upsell paths. The services segment, although smaller, is scaling at 28.96% CAGR on the back of implementation, model-governance, and user-adoption projects. As multi-cloud estates grow, clients commission partners to handle policy design, testing, and ROI baselining. Vendor professional-services groups tap this opportunity, while global system integrators build 1,000-person AI studios to capture demand.

Second-order effects reinforce software primacy. When Snowflake embedded Anthropic's models inside its Cortex service, customers accessed generative summarisation without exporting data, tightening platform dependence. Over the forecast horizon, open-source AI components will evolve, yet buyers still prefer commercial wrappers that guarantee security patches and legal indemnities, sustaining the software segment's lead within the augmented analytics market.

Cloud installations generated 61% of total spending in 2024. Financial-services firms, online marketplaces, and streaming networks exploit elasticity for holiday spikes and model-training bursts. However, strict residency mandates push critical workloads to private zones, propelling hybrid setups at a 30.22% CAGR. The hybrid share of the augmented analytics market is projected to rise from USD 18.19 billion in 2025 to USD 71.34 billion by 2030. Edge devices process personally identifiable information locally, then forward aggregated patterns to cloud AI for deeper inference, balancing compliance with analytic depth.

Edge-to-cloud orchestration tools signal the next battleground: platforms must schedule SQL, vector-search, and reinforcement-learning jobs across Kubernetes clusters on both sides of the firewall. Providers able to auto-deploy containers, govern encryption keys, and optimise latency stand to capture an outsized wallet share. On-premises-only deployments remain relevant for nuclear energy, defence, and pharmaceuticals, but growth lags behind hybrid because hardware refresh cycles elongate in capex-constrained sectors.

The Augmented Analytics Market Report is Segmented by Component (Software and Services), Deployment (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises and Small and Mid-Size Enterprises), End-User Industry (BFSI, Telecom and IT, Retail and Consumer Goods, Healthcare and Life Sciences, Manufacturing, Media and Entertainment, and Government and Public Sector), and Geography.

Geography Analysis

North America generated 48% of global revenue in 2024 and retains structural advantages: dense cloud-region footprint, venture-capital pipelines, and AI-skilled labour pools. Fortune 500 firms institutionalise AI centre-of-excellence charters, embedding analytics inside finance, supply-chain, and HR apps. Federal funding for AI research and streamlined IPO pathways attract startups that refresh the competitive arena. However, data-localisation clauses in Canada, California Consumer Privacy Act amendments, and antitrust scrutiny introduce compliance spend, nudging firms toward multi-jurisdictional hybrid architectures.

Asia-Pacific, while smaller today, is on a 28.80% CAGR trajectory through 2030. Government allocations exceed USD 500 billion for AI infrastructure, semiconductors, and talent development. China's AI hub in Shenzhen offers subsidised GPU clusters; India's Digital Personal Data Protection Act sets guardrails while encouraging domestic innovation. Manufacturing conglomerates cluster around Tokyo, Seoul, and Singapore, creating demand flywheels for shop-floor predictive analytics. Local vendors integrate Mandarin, Hindi, and Bahasa speech models, meeting linguistic requirements and giving regional players an edge. The augmented analytics market thus finds its fastest volume expansion in APAC geographies.

Europe continues to post mid-teen growth even as GDPR and the forthcoming AI Act heighten vendor obligations. Enterprises in Germany's Mittelstand adopt sovereign-cloud deployments inside national borders. French public-sector agencies run analytics in isolated regions to comply with citizen-data statutes. Vendor road maps now include "EU trusted zone" labels, reflecting the continent's regulatory pull. North-to-south digital-skills disparities persist, but EU-funded reskilling programmes close gaps, supporting steady adoption.

Latin America, the Middle East, and Africa represent later-stage opportunities, together projected to account for just under 10% of the augmented analytics market by 2030. Mobile-first business models, rising fintech penetration, and under-banked populations create analytics needs around credit scoring and fraud detection. Cloud-region launches in Sao Paulo, Riyadh, and Johannesburg lower latency and address data-residency rules, unlocking pilot budgets that convert to production workloads when ROI materialises.

- Microsoft Corporation

- Salesforce Inc. (incl. Tableau)

- SAP SE

- International Business Machines Corp.

- QlikTech International AB

- Google LLC (Looker)

- Oracle Corporation

- SAS Institute Inc.

- TIBCO Software Inc.

- ThoughtSpot Inc.

- MicroStrategy Inc.

- Sisense Inc.

- GoodData Corp.

- Alteryx Inc.

- Domo Inc.

- Zoho Corporation (Zoho Analytics)

- Amazon Web Services - QuickSight

- Yellowfin BI

- Board International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand to analyse multi-structured data

- 4.2.2 Self-service BI and data-democratisation push

- 4.2.3 SME uptake via cloud subscriptions

- 4.2.4 Generative-AI infused analytics suites

- 4.2.5 Edge-tier deployments for data sovereignty

- 4.2.6 SaaS copilot-led embedded-analytics monetisation

- 4.3 Market Restraints

- 4.3.1 Data-privacy and security concerns

- 4.3.2 Workforce anxiety over human-replacement

- 4.3.3 Prompt-engineering skill gap

- 4.3.4 GPU scarcity and inference cost inflation

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organisation Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Mid-size Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Telecom and IT

- 5.4.3 Retail and Consumer Goods

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 US

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 UK

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce Inc. (incl. Tableau)

- 6.4.3 SAP SE

- 6.4.4 International Business Machines Corp.

- 6.4.5 QlikTech International AB

- 6.4.6 Google LLC (Looker)

- 6.4.7 Oracle Corporation

- 6.4.8 SAS Institute Inc.

- 6.4.9 TIBCO Software Inc.

- 6.4.10 ThoughtSpot Inc.

- 6.4.11 MicroStrategy Inc.

- 6.4.12 Sisense Inc.

- 6.4.13 GoodData Corp.

- 6.4.14 Alteryx Inc.

- 6.4.15 Domo Inc.

- 6.4.16 Zoho Corporation (Zoho Analytics)

- 6.4.17 Amazon Web Services - QuickSight

- 6.4.18 Yellowfin BI

- 6.4.19 Board International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年银行业、金融服务业和保险业(BFSI)扩展分析全球市场报告2026年全球创作者薪酬分析市场报告

2026年银行业、金融服务业和保险业(BFSI)扩展分析全球市场报告2026年全球创作者薪酬分析市场报告 增强型分析市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、部署类型、最终用户及功能划分

增强型分析市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、部署类型、最终用户及功能划分 增强型分析市场 - 全球产业规模、份额、趋势、机会及预测(按部署方式、组织规模、最终用户、地区和竞争格局划分,2021-2031 年)

增强型分析市场 - 全球产业规模、份额、趋势、机会及预测(按部署方式、组织规模、最终用户、地区和竞争格局划分,2021-2031 年) 增强分析市场规模、份额和成长分析(按组件、公司规模、部署类型、垂直产业和地区划分)-2026-2033年产业预测

增强分析市场规模、份额和成长分析(按组件、公司规模、部署类型、垂直产业和地区划分)-2026-2033年产业预测 增强分析市场规模、全球组件、部署模式、组织规模、地区、范围和预测

增强分析市场规模、全球组件、部署模式、组织规模、地区、范围和预测 2025 年至 2033 年增强分析市场规模、份额、趋势及预测(按组件、部署模式、组织规模、产业垂直及地区划分)增强分析市场:未来预测(2025-2030)

2025 年至 2033 年增强分析市场规模、份额、趋势及预测(按组件、部署模式、组织规模、产业垂直及地区划分)增强分析市场:未来预测(2025-2030) 增强分析市场规模、份额、趋势分析报告:按组件、按企业规模、按部署类型、按行业、按地区、细分市场预测,2024-2030 年

增强分析市场规模、份额、趋势分析报告:按组件、按企业规模、按部署类型、按行业、按地区、细分市场预测,2024-2030 年 增强分析市场规模、占有率、预测和趋势分析:按产品、部署方法、组织规模、应用、最终用途行业和地区 - 到 2031 年的全球预测

增强分析市场规模、占有率、预测和趋势分析:按产品、部署方法、组织规模、应用、最终用途行业和地区 - 到 2031 年的全球预测