|

市场调查报告书

商品编码

1642158

智慧食品物流-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Smart Food Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

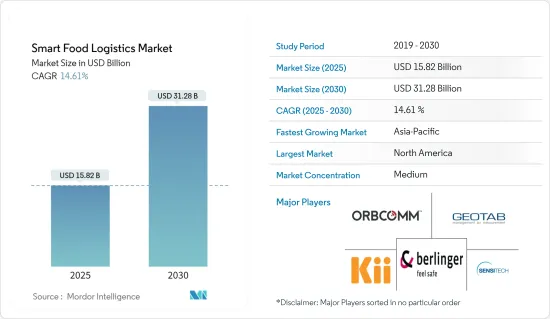

2025年智慧食品物流市场规模预估为158.2亿美元,预估至2030年将达312.8亿美元,预测期间(2025-2030年)复合年增长率为14.61%。

尤其是智慧食品物流公司利用低温运输监控技术协助食品製造商管理温控产品的运输、储存和配送的趋势日益明显。由于交通堵塞、机械故障等原因造成的温度波动会导致未保存的食品变质或变得不安全,这也是市场成长如此迅速的一个重要原因。

关键亮点

- 随着数位经济的扩张,物联网技术正在从一个未来的想法演变为物流公司在其供应链中使用的实用工具。感测器和物联网工具正在将传统的资产追踪转变为智慧供应链,可以为物流公司带来更高的投资报酬率。这些支援物联网的感测器提供有关资产和车队位置、车队行驶速度、温度条件以及其他对食品行业至关重要的资料集的即时资讯。

- 此外,透过物流和技术以及涵盖整个供应链的云端基础的协作解决方案,可以实现整个供应链中仓库、运输和最终消费者资讯的更紧密整合和透明度。这被认为是研究市场成长的主要驱动因素。此外,不同地区的各种食品法律法规,如《食品药品安全法》,对供应链施加了很大的压力,要求其记录更多信息、更加开放,这可能会促进整体市场的增长率. 这是导致

- 此外,市场正在见证主要企业进行的各种策略合併、收购和投资,以改善业务并扩大影响力,接触客户并满足各种应用的需求。例如,2022年8月20日,对抗饥饿和营养不良区域中心(CERFAM)与HELP Logistics签署了一份谅解备忘录。其主要目标是推出一个跨技术、科学和教育研究各领域的合作新平台。该平台的活动旨在加强农业食品价值链和非洲社区对社会经济衝击的整体抵御能力。

- 然而,由于整个安装过程的复杂程度不同,未来几年市场成长可能会放缓。

- COVID-19 疫情严重扰乱了全球几乎所有终端用户行业,扰乱了公司的供应链管理,并导致远端工作或全面封锁导致营运停工。为了抵御疫情并保持业务平稳运行,疫情导致的业务中断促使企业采用技术数位化。因此,预计未来几年市场将经历大量成长机会。

智慧食品物流市场趋势

低温运输监控占比很大

低温运输监控解决方案可协助食品製造商管理温控物品的储存、运输和分销。由于机械故障、运输延误或其他原因导致的冷却链不完整,可能导致温度变化,从而影响生鲜食品的腐败和安全。此外,无法即时了解货物的位置也会导致工作流程效率低落。

- 因此,透过采用低温运输监控,您可以确保货物运输和储存的温度稳定。配备温度感测器的蓝牙低功耗 (BLE) 信标等技术可以追踪相关查核点的货物位置,从而可以在整个运输过程和供应链中持续无缝地追踪温度资料。然而,在整个分销过程中维持低温运输的需求对于许多生鲜产品农产品生产商、手工食品生产商和农业工人来说是一个重大障碍,因为他们本身缺乏或根本没有物流能力。

- 此外,快速变化的饮食习惯推动了对包装食品的需求,严格的包装和储存规定导致权力从製造商转移到分销商。推动食品和饮料物流自动化和技术采用的关键驱动因素包括专注于零污染、精确储存以及快速储存和搜寻作业的流程。

- 沃尔玛等公司正在对自动化杂货分类机器人进行大量投资。无人商店将从仓库内部挑选订单,并使用自动推车挑选常温冷冻和冷藏食品杂货。机器人识别、拾取并将物品运送到工作站供工作人员检查。预计工业自动化的兴起将为低温运输监控解决方案的采用带来巨大的前景。

- 据印度製药协会称,2019 年印度低温运输行业总规模约为 3,300 亿卢比(3,987,307,500 美元),预计到 2022 年将增长至 4,200 亿卢比(5,076,288,000 美元)。 2020年,印度低温运输储存能力预计将达到3,740万吨左右。由于低温运输产业的兴起,预计市场在整个预测期内将见证显着的成长机会。

北美占主要份额

由于供应商数量众多且越来越注重消除浪费和优化资源,预计北美地区将占据智慧物流应用的最大份额。此外,由于北美在製造业、运输业和物流业中占有重要地位,且拥有各种技术进步,因此也是资产追踪的重要市场。此外,各个终端用户领域的政府措施和政策可能会促进该地区的市场扩张。

- 政府采取技术措施消除供应链中的浪费,推动了该地区市场的成长。例如,美国州公路和运输官员协会、联邦公路协会和地方交通部门都支持运输和物流业采用资产追踪。

- 此外,市场正在见证主要企业进行各种重大收购、合併和投资,以改善业务、接触客户并提高整体影响力,满足各种关键应用的需求。预计这将为智慧食品物流市场在预测期内扩张和改善带来无数机会。

- 例如,2022 年 2 月,美国农业部部长汤姆·维尔萨克表示,美国将扩大鸡肉和肉类加工选择,加强整体食品供应链,创造就业机会和粮食安全,特别是在农村地区。承诺提供高达约 2.15 亿美元的赠款和其他援助,以创造经济机会。因此,美国非常注重采取措施提高加工能力并提高家禽和肉类加工行业的竞争力。这将使美国农业市场对牧场主和农民更具竞争力、更公平、更方便、更稳定。

- 此外,美国部长汤姆·维尔萨克于2022 年10 月宣布,将主要透过食品供应链担保贷款计划向Crystal Freeze Dry LLC 提供资金,以扩大其冻干蛋製品生产能力,并为爱荷华州农村地区提供额外资金。这笔资金是拜登-哈里斯政府致力于加强关键食品供应链基础设施、为美国人民建立更繁荣的社区的重要组成部分。

智慧食品物流产业概览

智慧食品物流市场适度细分。拥有突出市场份额的大型公司正高度重视扩大其在各国的基本客群。这些公司正在利用多项关键的策略合作措施来最大限度地提高市场占有率并提高盈利。它揭示了市场的一些关键发展。

2022 年 12 月即将伙伴关係,全球智慧端到端供应链物流供应商 DP World 和温控仓储和物流公司 Americold 将联手打造更具弹性、更有效率和永续的运输解决方案。协议,为全球食品供应链提供数百万美元的投资。该组织希望透过制定从农场到餐桌的全球食品分销新标准来帮助世界上最大的食品公司。

2022 年 3 月,中西部着名的卡车运输和物流供应商 Hill Brothers, Inc. 选择 ORBCOMM Inc. 提供干燥和冷藏拖车整合监控解决方案,以管理其整个车队。 ORBCOMM 的一体化解决方案包括业界领先的无线连接硬体和整合的云端基础的分析平台,可简化跨多个资产类别的营运。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 市场定义与研究假设

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场动态

- 市场驱动因素

- 为改善资产管理,高效监控和追踪的需求日益增加

- 市场限制

- 安装复杂性

6. 新冠疫情对食品饮料物流业的影响

第七章 市场区隔

- 成分

- 硬体(感测器、远端资讯处理、网路设备等)

- 软体和服务

- 科技

- 车队管理

- 资产追踪

- 低温运输监控

- 地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第八章 竞争格局

- 公司简介

- Orbcomm

- Sensitech(Carrier Global Corporation)

- Berlinger & Co. AG

- Geotab Inc.

- Kii Corporation

- Verizon Connect

- Teletrac Navman

- Monnit Corporation

- Controlant

- Samsara Inc.

- Seaos

- Nippon Express co. Ltd.

- YUSEN LOGISTICS CO. LTD(Nippon Yusen Kabushiki Kaisha(NYK))

- Hacobu Co. Ltd(MOVO)

- Kouei system ltd.

- LYNA LOGICS, Inc.

第九章投资分析

第十章:市场的未来

The Smart Food Logistics Market size is estimated at USD 15.82 billion in 2025, and is expected to reach USD 31.28 billion by 2030, at a CAGR of 14.61% during the forecast period (2025-2030).

There is a rising trend of utilizing cold chain monitoring technologies by smart food logistics companies, especially to assist food makers in managing the transport, storage, and distribution of temperature-controlled products. Temperature changes caused by traffic jams, mechanical problems, and other things can ruin and make unsafe food that hasn't been preserved, which is a big reason why the market is growing so quickly.

Key Highlights

- As the digital economy expands, IoT technology has evolved from a futuristic idea to a practical tool for logistics companies to use in their supply chains. Sensors and IoT tools are changing traditional asset tracking toward intelligent supply chains that can generate a higher ROI for logistics firms. These IoT-enabled sensors provide real-time information on asset or fleet location, fleet mobility speed, temperature conditions, and other critical data sets for the food industry.

- Also, the tight integration of warehouse, transport, and end-consumer information and transparency through the supply chain has been made possible by logistics and technology, along with cloud-based collaborative solutions that extend through the entire supply chain. This, in turn, has been recognized as a key driver of the growth of the market under study. Also, different food laws and regulations in different areas, like the Food and Drug Safety Act, put a lot of pressure on supply chains to record more information and be more open, which is a big reason for the market's overall growth rate.

- Moreover, the market is witnessing various strategic mergers, acquisitions, and investments by key players as part of its strategy to improve business and their presence to reach customers and meet their requirements for various applications. For example, on August 20, 2022, the Regional Centre of Excellence against Hunger and Malnutrition (CERFAM) and HELP Logistics signed a Memorandum of Understanding. The main goal was to set up a new platform for collaboration in different areas of technical, scientific, and educational research. The activities of this platform would be aimed at strengthening agri-food value chains and the overall resilience of communities in Africa to socio-economic shocks.

- But different levels of complexity in the overall installation processes could slow the market's growth over the next few years.

- The COVID-19 pandemic significantly interrupted practically all end-user industries worldwide, disrupting company supply chain management owing to remote working circumstances or total lockdown, resulting in the halt of operations. In order to survive the pandemic and keep their operations running smoothly, the disruption caused companies to use technology and digitalization more. As a result, the market is expected to have many growth opportunities over the next few years.

Smart Food Logistics Market Trends

Cold Chain Monitoring to Hold a Significant Share

A cold chain monitoring solution helps food manufacturers manage temperature-controlled items' storage, shipment, and distribution. Incomplete cooling chains caused by mechanical breakdowns, traffic delays, and other reasons result in shifting temperatures, which can influence the spoilage and safety of perishable foods. In addition, a lack of real-time visibility of goods' locations might contribute to an inefficient operating process.

- As a result, the adoption of cold chain monitoring ensures stable temperatures for transporting and storing goods. Technologies like Bluetooth Low Energy (BLE) beacons with temperature sensors enable tracking goods' locations at relevant checkpoints and tracing temperature data continuously and seamlessly during shipment or throughout the supply chain. However, the need to maintain the cold chain throughout the delivery process raised a significant barrier for many producers of perishable goods, artisanal food producers, and farmers with little or no logistical capacities of their own.

- Moreover, rapidly changing food habits have boosted demand for packaged food, and stringent packing and storage regulations have resulted in a power transfer from manufacturers to merchants. The primary reasons propelling automation and technology adoption in food and beverage logistics include processes focusing on zero contamination, precise storage, and high-speed storage and retrieval operations.

- Companies such as Walmart have made considerable investments in automated grocery selection robots. Alphabot picks orders within the warehouse, utilizing autonomous carts to pick frozen and refrigerated groceries stored at ambient temperature. The robot identifies an item, picks it up, and carries it to a workstation for inspection by a staff person. Such industry automation advancements are projected to generate considerable prospects for cold chain monitoring solution adoption.

- As per the Indian Pharmaceutical Association, in 2019, the total size of the cold chain industry in India was around 330 billion rupees (USD 3987307500), and it was estimated to reach 420 billion rupees (USD 5076288000) in 2022. In 2020, it was predicted that India would have approximately 37.4 million metric tons of cold chain storage capacity. Due to the rise in the cold chain industry, the market is expected to witness significant growth opportunities throughout the forecast period.

North America Holds Major Share

Because of the presence of many vendors and the growing concern to eliminate waste and optimize resources, the North American region is expected to have the largest share of smart logistics adoption.Moreover, North America is a significant asset tracking market due to the region's strong presence in the manufacturing, transportation, and logistics industries and various technological advancements. Furthermore, government initiatives and policies in different end-user sectors will likely boost regional market expansion.

- The government's drive to adopt technology to reduce waste in the supply chain is fueling the region's market growth. For example, the American Association of State Highway and Transportation Officials, the Federal Highway Association, and local departments of transportation have all supported the adoption of asset tracking in the transportation and logistics industry.

- Moreover, the market is witnessing various significant acquisitions, mergers, and investments by key players as part of their crucial growth strategy to improve business and their overall presence to reach customers and meet their requirements for various key applications. This is expected to open up a plethora of opportunities for the smart food logistics market to expand and improve over the forecast period.

- For instance, in February 2022, U.S. Department of Agriculture (USDA) Secretary Tom Vilsack declared that USDA is making available up to a sum of around USD 215 million in grants and other support to extend poultry and meat processing options, strengthen the overall food supply chain, and create jobs and economic opportunities, especially in rural areas. So, the USDA is very focused on taking steps to increase processing capacity and boost competition in the poultry and meat processing industries. This will make agricultural markets in the United States more competitive, fair, accessible, and stable for ranchers and farmers.

- Furthermore, U.S. Department of Agriculture (USDA) Secretary Tom Vilsack announced in October 2022 that the Department is investing approximately USD 11.1 million, primarily through the Food Supply Chain Guaranteed Loan Program, to assist Crystal Freeze Dry LLC in expanding its capacity to manufacture freeze-dried egg products and creating job opportunities in rural Iowa. The funding is a crucial part of the Biden-Harris Administration's commitment to strengthening the critical food supply chain infrastructure to build more thriving communities for the American people.

Smart Food Logistics Industry Overview

The market for smart food logistics is moderately fragmented. The major players with a prominent share of the market are greatly focusing on extending their customer base across various foreign countries. These companies are leveraging several key strategic collaborative initiatives to maximize their market share and increase their profitability. Some of the key developments in the market are:

In December 2022, DP World, the provider of worldwide smart end-to-end supply chain logistics, and Americold, the provider of temperature-controlled warehousing and logistics, signed a strategic partnership agreement that would enable multi-million dollar investment in a more resilient, efficient, and sustainable global food supply chain. This group wants to help the biggest food companies in the world by setting a new standard for global food distribution, from the farm to the table.

In March 2022, Hill Brothers, Inc., a prominent trucking and logistics provider in the Midwest, will choose ORBCOMM Inc. to supply its integrated dry and refrigerated trailer monitoring solutions for fleet-wide management. ORBCOMM's all-in-one solutions include industry-leading hardware for wireless connectivity and a unified cloud-based analytics platform to streamline operations across multiple asset classes.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Need for Efficient Monitoring and Tracking for Better Control of Assets

- 5.2 Market Restraints

- 5.2.1 Installation Complexities

6 IMPACT OF COVID-19 ON THE LOGISTICS INDUSTRY IN THE FOOD AND BEVERAGE SECTOR

7 MARKET SEGMENTATION

- 7.1 Component

- 7.1.1 Hardware (Sensors, Telematics, Networking Devices, etc.)

- 7.1.2 Software and Services

- 7.2 Technology

- 7.2.1 Fleet Management

- 7.2.2 Asset Tracking

- 7.2.3 Cold Chain Monitoring

- 7.3 Geography

- 7.3.1 North America

- 7.3.2 Europe

- 7.3.3 Asia-Pacific

- 7.3.4 Latin America

- 7.3.5 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Orbcomm

- 8.1.2 Sensitech (Carrier Global Corporation)

- 8.1.3 Berlinger & Co. AG

- 8.1.4 Geotab Inc.

- 8.1.5 Kii Corporation

- 8.1.6 Verizon Connect

- 8.1.7 Teletrac Navman

- 8.1.8 Monnit Corporation

- 8.1.9 Controlant

- 8.1.10 Samsara Inc.

- 8.1.11 Seaos

- 8.1.12 Nippon Express co. Ltd.

- 8.1.13 YUSEN LOGISTICS CO. LTD (Nippon Yusen Kabushiki Kaisha(NYK)

- 8.1.14 Hacobu Co. Ltd (MOVO)

- 8.1.15 Kouei system ltd.

- 8.1.16 LYNA LOGICS, Inc.

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

全球食品冷藏物流服务市场(依运输方式、附加价值服务、仓储配送及运输划分)预测(2026-2032年)食品冷藏和冷冻供应链物流市场:按仓储、包装和标籤、订单履行和运输划分,全球预测,2026-2032年

全球食品冷藏物流服务市场(依运输方式、附加价值服务、仓储配送及运输划分)预测(2026-2032年)食品冷藏和冷冻供应链物流市场:按仓储、包装和标籤、订单履行和运输划分,全球预测,2026-2032年 日本食品物流市场规模、份额、趋势及预测(依运输方式、产品类型、服务类型、细分市场及地区划分),2026-2034年

日本食品物流市场规模、份额、趋势及预测(依运输方式、产品类型、服务类型、细分市场及地区划分),2026-2034年 食品物流市场规模、份额及成长分析(依运输方式、服务、产品、仓储设施及地区划分)-2026-2033年产业预测

食品物流市场规模、份额及成长分析(依运输方式、服务、产品、仓储设施及地区划分)-2026-2033年产业预测 食品低温运输:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

食品低温运输:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 食品低温运输市场规模、份额和趋势分析报告:按类型、建设类型、应用、地区和细分市场预测,2025-2033 年

食品低温运输市场规模、份额和趋势分析报告:按类型、建设类型、应用、地区和细分市场预测,2025-2033 年 食品冷链物流市场-全球产业规模、份额、趋势、机会及预测(依产品类型、应用、建筑类型、地区及竞争情况划分,2020-2030 年)2025-2033年按产品类型(蔬菜和水果、乳製品、肉类和海鲜等)、运输方式(公路、铁路、海运、航空)和地区分類的杂货运输市场非洲食品低温运输物流 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

食品冷链物流市场-全球产业规模、份额、趋势、机会及预测(依产品类型、应用、建筑类型、地区及竞争情况划分,2020-2030 年)2025-2033年按产品类型(蔬菜和水果、乳製品、肉类和海鲜等)、运输方式(公路、铁路、海运、航空)和地区分類的杂货运输市场非洲食品低温运输物流 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 全球冷冻食品低温运输市场2024-2028

全球冷冻食品低温运输市场2024-2028